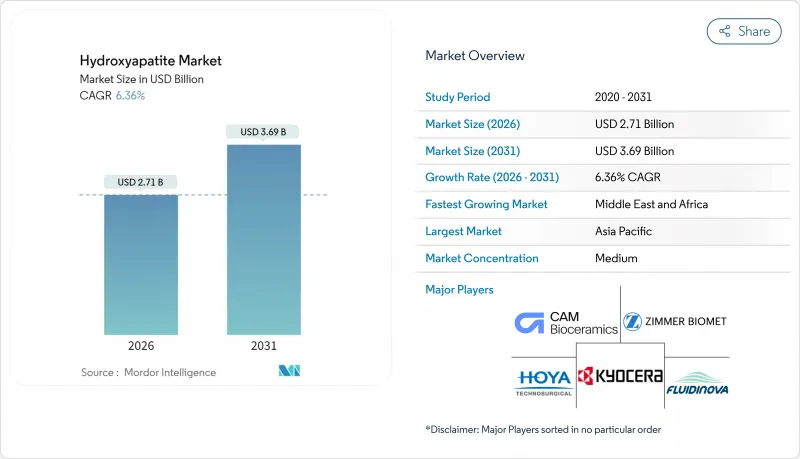

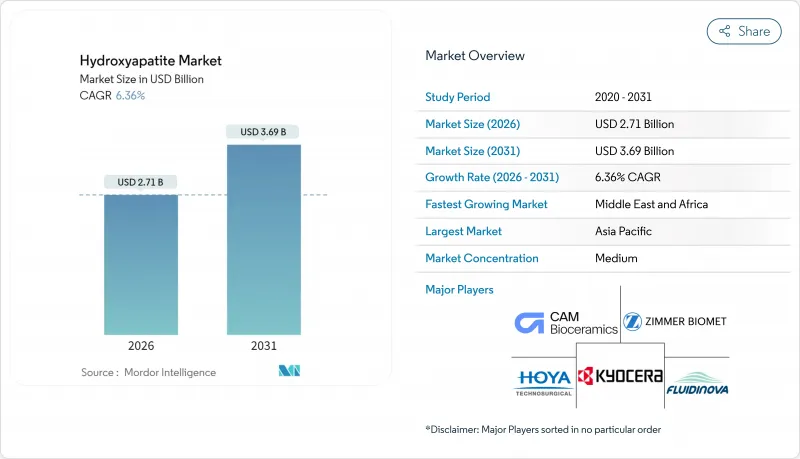

2026년 하이드록시아파타이트 시장 규모는 27억 1,000만 달러로 추정되고, 2025년 25억 5,000만 달러에서 성장하며, 2031년에는 36억 9,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년까지는 CAGR 6.36%를 나타낼 전망입니다.

이 꾸준한 성장 궤적은 하이드록시아파타이트 시장이 광범위한 생체재료 분야에서 확대되는 기둥임을 뒷받침합니다. 성장의 원동력은 인구의 고령화, 임상 현장에서의 채용 확대, 나노 스케일 제조 기술의 급속한 진전에 있습니다. 수요는 재수술률을 저감하는 생체활성 코팅을 외과의사가 선호하는 경향, 불소를 포함하지 않는 재석회화 제품으로 전환하는 구강 케어 브랜드, 이온 방출을 억제하는 세라믹 임플란트를 규제 당국이 명확하게 추천하는 자세에 의해 더욱 강화되고 있습니다. 제조 공정의 혁신으로 생산 비용이 저하되고, 약물 전달, 영상 진단, 특수 화장품 분야로의 재료의 다양성이 확대됨에 따라 경쟁력이 커지고 있습니다. 상환에 관한 역풍이나 엄격한 의료기기 승인이 단기적인 가속을 억제하고 있는 것, 기업이 맞춤형 의료와 지속가능성을 축으로 포트폴리오를 재편하는 중, 하이드록시아파타이트 시장의 장기적인 전망은 계속 양호합니다.

OECD 국가의 노화와 관련된 치아 손실은 수복 치과 치료의 환자층을 확대하고 있으며, 보험 회사는 하이드 록시 아파타이트 코팅으로 신속하게 통합되는 단일 치아 임플란트의 상환을 증가 시켰습니다. 임상 등록 데이터에 따르면, 코팅된 조명기의 생존율은 95-98%인 반면, 코팅되지 않은 티타늄의 생존율은 90-92%이며, 이 차이는 수정 비용을 직접적으로 감소시킵니다. 단가 저하, 의자 사이드 디지털 워크플로우 및 교육 과정의 보급 확대로 의료 종사자 채용이 확대되고 있습니다. 그 결과, 중소득층에 있어서도 고품질 코팅 수요가 높아지고 있어 어버트먼트용 스프레이나 소켓 필러에 사용되는 나노 강화 분말 수요 증가를 지지하고 있습니다. 미국 및 EU 규제 당국은 2025년에 생체적합성 시험의 필요성을 강조하는 공식적인 지침을 수립했습니다. 하이드록시아파타이트는 이러한 과제를 일관되게 클리어하고 있으며, 병원 네트워크에서 공급업체 계약의 획득을 가속화하고 있습니다.

2024년에는 외래 수술 센터(ASC)가 유방교육에 의한 수술 지연을 해소하여 선택적 관절 재건 수술이 회복되었습니다. 부분 무릎 관절 치환술, 외상용 플레이트, 척추 케이지의 보급에 의해 임플란트 전체의 기반이 확대되고, 하이드록시아파타이트 피복 표면은 소지 티타늄에 비해 뼈 결합 시간을 20-30% 단축하기 때문에 포괄 지불 제도에 있어서 입원 일수가 삭감되었습니다. 아시아태평양의 수탁 제조 업체는 플라즈마 용사 라인을 활용하여 세계 OEM 제조 업체에 공급함으로써 규모의 경제를 실현하고 있습니다. 하이드록시아파타이트 페이스트를 포함한 3D 프린팅 래티스는 고정을 더욱 가속화하고, 특히 젊은 환자를 위한 맞춤형 대퇴골 줄기에서 장기적인 재수술 회피의 높은 가치를 제공합니다.

고품질 하이드록시아파타이트 코팅은 임플란트의 청구 가격을 15-25% 끌어올려 자기 부담에 의존하는 신흥 시장에서는 병원 예산을 압박합니다. 미국에서는 종합적 의료에 의해 재수술률 저하에 의한 장기적인 절약 효과가 실현되고 있지만, 동남아시아의 많은 지불 기관에서는 여전히 품목 마다의 상환 방식을 채용하고 있어, 이것에 의해 외과의가 코팅 끝난 하드웨어를 선택하는 재량이 제한되고 있습니다. 고에너지 플라즈마 건과 같은 훈련 및 설비 요구 사항은 현지 제조업체에 대한 추가 초기 비용 요인입니다. 프랑스와 브라질에서 확산되고 있는 재수술 회피분을 평가하는 라이프사이클 평가를 중앙 조달 틀에 통합하는 동향에 의해 코스트면에서의 역풍이 완화될 가능성이 있습니다.

2025년 매출액에서는 미립자 크기가 47.65%를 차지했지만, 나노그레이드 재료는 프리미엄 치과 제품 및 약물 전달 제품의 확대에 따라 CAGR 7.09%를 기록했습니다. 나노하이드록시아파타이트는 단백질 흡착성을 높여 스플릿 마우스 시험에서 미립자 등급에 비해 35% 높은 에나멜 재석회화 효과를 나타냅니다. 수요는 일본, 한국, 서유럽에 집중되어 있으며 소비자는 기능성 구강 케어 효과에 대해 지불할 의지가 있습니다. 약물 전달 분야에서 초상자성 나노HAp는 화학요법제를 골전이 부위로 수송하고 단일 구조로 영상 진단과 치료를 통합합니다.

스케일업은 여전히 과제이며, 1차 입자의 응집이 치약이나 주사용 겔의 유변학을 손상시킬 우려가 있습니다. Fluidinova의 독특한 분산제는 수성 매체에서 100 나노미터 미만의 결정을 안정화시켜 배합자가 점도 급상승 없이 높은 부하 수준을 달성할 수 있게 합니다. 나노부문의 고가격화는 제어 분위기 반응기와 관련된 높은 자본 비용을 상쇄합니다. 마이크로그레이드는 벌크 정형외과 시멘트에서 비용면과 입수성의 우위를 유지하며, 거시 입자는 기계적 강도가 표면 반응성보다 우선하는 하중 지지용 스캐폴드에 계속 사용되고 있습니다.

2025년 매출의 71.85%는 합성 원료가 차지하고 임플란트에 필수적인 균일한 순도를 실현하는 습식 침전법 및 수열법이 기반이 되었습니다. 그러나 순환 경제에 대한 적합성으로 인해 바이오 유래 하위 부문은 6.83%의 연평균 복합 성장률(CAGR)로 성장했습니다. 달걀 껍질과 생선 비늘 유래의 전구체는 골 전도성을 향상시키는 다공성 휘스커 형태의 HAp을 생성합니다. 산호에서 유래된 하이드록시아파타이트는 상호 연결된 관 구조를 가지며 혈관 내 성장을 가속합니다. 이 특성은 고밀도 합성 펠릿에 비해 척추 케이지의 융합 성공률이 12% 향상되는 것으로 입증되었습니다.

제조 공정의 변동은 한때 외과의사의 우려 재료였지만, 새로운 소성 프로토콜에 의해 광물상이 균질화되어 Ca/P비가 99% 이상이라는 화학양론적 조성이 달성되고 있습니다. 인증 기준은 여전히 엄격하며 바이오 유래 제품은 미량 원소 수준과 인체 공통 감염 위험의 안전성을 입증해야합니다. 그러나 녹색 조달 기준을 도입하는 병원에서는 특히 스칸디나비아 국가와 캐나다에서 바이오 유래 시멘트의 채용이 점차 증가하고 있습니다. 한편 합성제법은 무릎 관절용 피복 경골 트레이 분야에서 우위성을 유지하고 있습니다. 이 분야에서는 로트간의 균일성, 색조 관리, 저엔도톡신레벨이 필수 조건이 되고 있습니다.

아시아태평양의 주도적 지위는 중국 후베이성의 인광산에서 일본의 시즈오카에 있는 마감 공장까지를 연결하는 수직 통합 에코시스템에 기인합니다. 지역 연구 프로그램은 나노 분산 화학 기술에 대한 특허를 안정적으로 생산하고 경쟁 우위를 뒷받침합니다. 국내 소비도 증가 추세에 있으며, 중국에서는 2024년에 약 60만건의 고관절 무릎 관절 치환술이 실시되어 전년대비 11% 증가하여 현지 분말 수요를 지지했습니다. 일본의 고령화는 임플란트의 고수준 수요와 고급 미용 필러의 보급을 지원하고 있습니다. 한편 ASEAN 국가에서는 CE 마크 취득 치과 제품의 수입 관세 장벽이 완화되고 있습니다.

북미 공급업체는 임상의의 신뢰를 구축하는 FDA 분류를 통해 점유율을 보호하고 있습니다. 미국의 스타트업 기업은 국립위생연구소(NIH)의 자금을 활용하여 부위 특이적 암 치료를 위한 자성 나노하이드록시아파타이트의 개량을 추진하고 있으며, 이 최첨단 응용 분야는 전문적인 수탁 제조 업체를 만들어낼 가능성이 있습니다.

유럽 공급업체는 시판 후 조사 컨소시엄을 조성하고 장기 데이터를 축적함으로써 의료기기 규칙(MDR)의 임상 증거 요건이라는 장벽을 극복하고 있습니다. 이 환경은 신규 진입 페이스를 억제하는 한편, 규제 준수 기업의 마진 향상에 기여하고 있습니다.

중동 및 아프리카은 석유 수출국이 의료 관광으로 다각화하는 움직임으로 성장률이 돌출하고 있습니다. 아부다비의 고성능 정형외과 센터에서는 스위스·미국제 인공 관절을 수입하고 있어 지역 유통업체가 일관된 분말 로트의 재고 확보를 강요하고 있습니다. 튀르키예의 민간 병원은 비용 우위성과 유럽에 대한 지리적 근접성을 활용하여 의료 관광 패키지의 차별화 요소로서 하이드록시아파타이트 피복 척추 시스템을 추진하고 있습니다. 남미 시장에서는 통화변동의 영향으로 하이드록시아파타이트의 채용은 신중하지만, 브라질의 ANVISA가 2025년에 의료기기 승인을 효율화함으로써 피복치과 임플란트의 승인 파이프라인이 해소되고 있습니다.

Hydroxyapatite market size in 2026 is estimated at USD 2.71 billion, growing from 2025 value of USD 2.55 billion with 2031 projections showing USD 3.69 billion, growing at 6.36% CAGR over 2026-2031.

This steady trajectory confirms the hydroxyapatite market as an expanding pillar of the broader biomaterials landscape, with growth powered by demographic aging, widening clinical adoption, and rapid gains in nano-scale manufacturing. Demand is reinforced by surgeons' preference for bioactive coatings that cut revision rates, oral-care brands pivoting toward fluoride-free remineralization, and regulators signaling a clear preference for ceramic implants that limit ion release. Competitive momentum intensifies as process innovation lowers production cost and extends material versatility into drug delivery, imaging, and specialty cosmetics. Although reimbursement headwinds and stringent device approvals temper near-term acceleration, the hydroxyapatite market's long-range outlook remains positive as companies align portfolios around personalized medicine and sustainability.

Age-associated tooth loss in OECD nations is expanding the patient pool for restorative dentistry, and insurers increasingly reimburse single-tooth implants that integrate faster with hydroxyapatite coatings. Clinical registries show 95-98% survival for coated fixtures versus 90-92% for uncoated titanium, a difference that directly lowers revision costs. Lower unit prices, chair-side digital workflows, and wider availability of training courses widen practitioner adoption. As a result, premium coating demand rises even in mid-income segments, supporting higher volumes for nano-enhanced powders used in abutment sprays and socket fillers. U.S. and EU regulators formalized guidance in 2025 that underscores the need for biocompatibility testing; hydroxyapatite consistently clears these hurdles, accelerating supplier contract awards in hospital networks.

Elective joint reconstruction rebounded in 2024 as outpatient surgery centers overcame pandemic backlogs. Broader use of partial knees, trauma plates, and spinal cages enlarges the overall implant base, and hydroxyapatite-coated surfaces shorten osseointegration time by 20-30% compared with bare titanium, cutting hospitalization days for bundled-payment episodes. APAC contract manufacturers leverage plasma-spray lines to supply global OEMs, creating scale economies. 3D-printed lattices incorporating hydroxyapatite paste further accelerate fixation, particularly in custom femoral stems for younger patients where long-term revision avoidance carries high value.

Premium hydroxyapatite coatings lift implant invoice prices by 15-25%, stretching hospital budgets in emerging markets that rely on out-of-pocket payments. While bundled care in the United States captures long-term savings from lower revision incidence, many payers in Southeast Asia still reimburse on a per-item basis, which limits surgeons' discretion in selecting coated hardware. Training and equipment requirements, such as high-energy plasma guns, add further upfront cost for local manufacturers. Cost headwinds may ease as centralized procurement frameworks incorporate life-cycle assessments that credit avoided revision surgeries, a trend gaining traction in France and Brazil.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Although micro-sized powders retained 47.65% of the 2025 revenue, nano-grade materials registered a 7.09% CAGR as premium dental and drug-delivery products scaled. Nano-hydroxyapatite enhances protein adsorption, resulting in 35% higher enamel remineralization compared to micro-scale grades in split-mouth trials. Demand is concentrated in Japan, South Korea, and Western Europe, where consumers are willing to pay for functional oral-care claims. In drug delivery, superparamagnetic nano-HAp ferries chemotherapeutics to bone metastases, combining imaging and therapy in a single construct.

Scale-up remains challenging; primary particle aggregation jeopardizes rheology in toothpaste and injectable gels. Fluidinova's proprietary dispersants stabilize sub-100 nm crystals in aqueous media, allowing formulators to hit higher loading levels without viscosity spikes. The nano segment's premium pricing offsets the higher capital costs associated with controlled-atmosphere reactors. Micro-grades retain cost and availability advantages for bulk orthopedic cements, while macro particles continue to be used in load-bearing scaffolds, where mechanical strength takes precedence over surface reactivity.

Synthetic feedstock accounted for 71.85% of 2025 sales, anchored by wet-precipitation and hydrothermal routes that deliver consistent purity essential for implants. Nevertheless, the bio-derived sub-segment is experiencing a 6.83% CAGR driven by its circular-economy appeal. Eggshell and fish-scale precursors yield HAp with porous whisker morphologies that enhance osteoconduction. Coral-derived hydroxyapatite exhibits interconnected canals that facilitate vascular ingrowth, a property that has been documented to increase fusion success in spinal cages by 12 percentage points compared to dense synthetic pellets.

Process variability once deterred surgeons, but new calcination protocols homogenize mineral phases to a stoichiometry of greater than or equal to 99% Ca/P. Certification remains stricter; bio-routes must document trace element levels and zoonotic safety. Yet hospitals deploying green procurement metrics are beginning to prefer bio-sourced cements, particularly in Scandinavia and Canada. Synthetic routes keep dominance in coated knee tibial trays, where batch-to-batch uniformity, color control, and low endotoxin levels are mandatory.

The Hydroxyapatite Market Report is Segmented by Particle Size (Nano-Sized, Micro-Sized, Macro-Sized), Source (Synthetic, Bio-Derived), Form (Powder, Granules, Coatings and Pastes), Application (Dental Care, Orthopedics, Plastic and Cosmetic Surgery, Other Industrial Uses), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific's leadership stems from a vertically integrated ecosystem that links phosphate mines in China's Hubei province to finishing plants in Shizuoka, Japan. Regional research programs produce steady patent output on nano-dispersion chemistries, underlining competitive superiority. Domestic consumption also rises; China performed nearly 600,000 hip and knee replacements in 2024, up 11% year on year, feeding local powder demand. Japan's aging demographic sustains high implant volumes and premium cosmetic filler uptake, while ASEAN nations ease tariff barriers to import CE-marked dental products.

North American suppliers defend share through FDA classifications that build clinician confidence. U.S. start-ups exploit NIH funding to refine magnetic nano-hydroxyapatite for site-directed oncologic therapies, a frontier application likely to spin off specialized contract manufacturers.

European vendors navigate MDR's clinical-evidence hurdles by forming post-market surveillance consortia to aggregate long-term data. This environment moderates new-entrant pace yet enriches margins for compliant players.

Middle East and Africa outpaces in growth as oil-exporting nations diversify into health tourism. High-spec orthopedic centers in Abu Dhabi import Swiss and U.S. prosthetics, spurring regional distributors to stock consistent powder lots. Turkish private hospitals leverage cost advantage and geographic proximity to Europe, marketing hydroxyapatite-coated spinal systems as a differentiator in medical-tour packages. South American markets adopt hydroxyapatite more cautiously, slowed by currency volatility, though Brazil's ANVISA streamlined device approvals in 2025, unclogging a pipeline of coated dental implants.