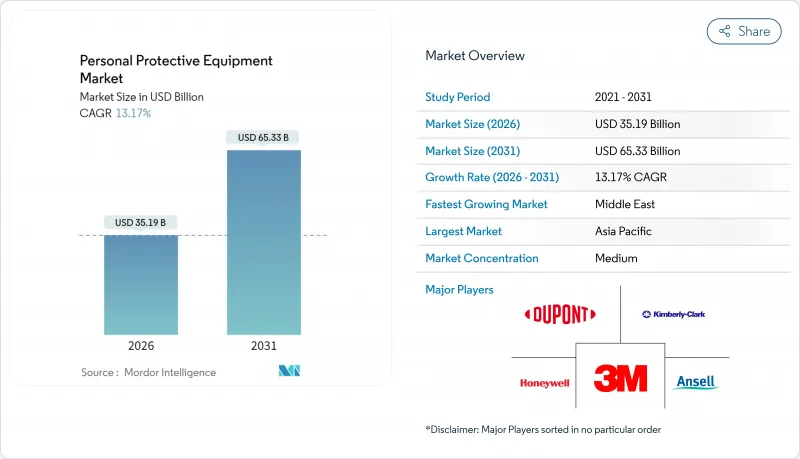

개인보호장비(PPE) 시장은 2025년 311억 달러에서 2026년 351억 9,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 13.17%로 성장을 지속하여 2031년까지 653억 3,000만 달러에 달할 것으로 예측됩니다.

규제의 지속적인 강화, 고용주의 책임 리스크 증가, 제로함 문화에 대한 기업 전체의 노력은 성숙 경제권과 신흥 경제권 모두에서 수요를 견인하고 있습니다. 센서의 급속한 소형화, 연결 비용의 하락, 클라우드 분석의 보급 확대에 의해 기존의 수동 장비가 데이터가 풍부한 안전 노드로 변모하면서 기본적인 보호 기능을 넘은 가치 제안이 강화되고 있습니다. 증가하는 지속가능성에 대한 기대는 재료 선택과 수명 주기 모델을 재구성하는 반면, 티어 1 공급업체 간의 통합은 밸류체인 전반의 협상력을 재조정하고 있습니다. 이러한 요인들이 결합되어 개인보호장비 시장은 2020년대 후반부터 지속적인 두 자릿수 성장이 예상됩니다.

중국에서 개정된 노동안전보건법에 따라 고위험 업종에서는 노출 데이터를 실시간으로 전송하는 연결형 PPE의 도입이 의무화되어 지역 전체에서 고급품에 대한 수요가 높아지고 있습니다. 인도의 '노동안전보건 및 노동조건에 관한 법령'도 비슷한 움직임을 보이고 있으며 Malcom은 국내 생산능력 확대를 위해 100캐롤 루피(1,200만 달러)를 투자하고 있습니다. 이를 통해 현지 공급업체는 저비용 경쟁에서 성능 차별화로 전환하여 평균 판매 가격을 인상하면서 공급망 전체의 컴플라이언스 강화를 도모하고 있습니다.

EU의 새로운 '생산자 책임 재활용' 제도에 의해 제조업체는 사용한 마스크나 장갑의 회수 및 재활용 비용을 부담하게 되어, 생분해성 폴리머의 연구 개발이 가속하고 있습니다. 초기 파일럿 프로그램에서는 일회용 제품 카테고리에서 최대 60%의 재료 회수에 성공하여 UVEX나 3M 독일 등 기업의 컴플라이언스가 브랜딩 우위성으로 전환하고 있습니다.

의료 분야에서만 2005년 이후 일회용 PPE의 사용량이 두배로 늘어나면서 매립지에 대한 부하와 탄소 실적이 증가하고 있습니다. 현재, 지원단체는 기후에 대한 석유화학 유래의 장갑이나 마스크의 영향에 초점을 맞추고 있으며, 병원이 입찰 서류에 지속가능성 조항을 포함하도록 촉구하고 있습니다. 바이오 폴리하이드록시알카노에이트 장갑과 같은 대체품은 유망하지만 여전히 비용이 높으며 엄격한 여과 성능과 인장 강도 요구 사항을 충족하기 위해 어려움을 겪고 있습니다. 이 때문에 제조업체 각사는 현행 생산 라인을 유지하면서, 연구 개발을 진행하게 되어 수익성의 압박에 직면하고 있습니다. 특히 높은 일회용 제품 사용량에 의존하는 기업에서는 중장기적인 이익률 확대에 가해지는 영향이 높을 것으로 예상됩니다.

호흡기 보호는 비정상적인 호흡 패턴을 사용자에게 경고하는 생체 인증 센서를 내장한 스마트 필터를 원동력으로 2031년까지 12.48%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되고 있습니다. 장갑은 디지털화된 현장에서의 작업 흐름에 적합한 내절단성 섬유와 터치스크린 대응 코팅에 의해 2025년에는 개인보호장비 시장에서 점유율 28.82%를 유지했습니다.

설계 개선으로 통기성과 경량화가 중요해졌습니다. 존스 홉킨스 대학의 전문가들은 전통적인 일회용 모델을 대체하는 재사용 가능 엘라스토머 호흡 보호구에 대한 투자를 권장합니다. 구매자는 구매 가격보다 수명 주기 비용으로 장비를 평가하기 때문에 IoT 지원 고급 모델은 주로 기관 투자자 및 전자상거래 채널에서 도입됩니다.

아시아태평양은 거대한 제조 거점과 확대하는 건설 파이프라인에 의해 2025년 개인보호장비 시장에서 39.05%의 점유율을 차지했습니다. 중국의 화학, 일렉트로닉스, 조선 클러스터가 대량 주문을 견인하고 있는 한편, 인도의 의료기기 부문은 2029년까지 205억 1,000만 달러에 달할 전망이며, 이는 클린 룸 등급 소모품에 대한 국내 수요를 높이고 있습니다. 각국 정부는 현지 PPE 생산에 대한 재정적 인센티브를 확대하여 수입 의존도를 줄이고 공급망 회복력을 강화하고 있습니다.

북미는 OSHA(미국노동안전보건국)의 엄격한 감독과 석유, 가스 및 의료분야에서 스마트 PPE의 조기 도입을 특징으로 하는 견조한 지위를 유지하고 있습니다. 반도체 확장에 연방 자금을 투입하면서 오염 방지 의류에 대한 수요가 높아지고 이 지역의 프리미엄 제품 지향이 강화될 전망입니다. 유럽 시장은 환경 규제 대응으로 전환하고 있으며, 순환형 경제의 기한이 다가오는 가운데, 공급자는 회수 방식이나 재생 소재 함유 제품의 제공을 요구받고 있습니다. 이러한 지속가능성의 전제조건은 무역 장벽을 높여 지역 조달을 촉진하고 있습니다.

중동은 가장 성장하는 시장이며 사우디아라비아와 UAE의 2조 달러 규모 메가 프로젝트를 배경으로 2031년까지 연평균 복합 성장률(CAGR) 13.86%로 확대될 것으로 예측됩니다. 현지 규제에 의해 현장 작업원은 국제 인증을 취득한 PPE 착용이 의무화되고, 따라서 프리미엄 브랜드에 새로운 판로가 열리고 있습니다. 남미에서는 도입에 편차가 나타나고 있습니다. 브라질에서는 대규모 산업 사고로 인해 규제 강화가 진행되는 한편, 다른 지역에서는 재정 제약이 확대의 걸림돌이 되고 있습니다. 아프리카는 장기적인 기회를 보유하고 있으며 산업화와 광업 확대에 의해 안전기준의 시행이 강화되는 한편, 공급망은 미성숙하기 때문에 라스트마일 배송의 현지화가 가능한 선도기업에게 유리한 상황입니다.

The personal protective equipment market is expected to grow from USD 31.10 billion in 2025 to USD 35.19 billion in 2026 and is forecast to reach USD 65.33 billion by 2031 at 13.17% CAGR over 2026-2031.

Continuous regulatory tightening, higher employer liability exposure, and a widespread corporate commitment to zero-harm cultures are propelling demand across both mature and emerging economies. Rapid miniaturisation of sensors, falling connectivity costs, and increased cloud analytics adoption are turning formerly passive gear into data-rich safety nodes, sharpening the value proposition beyond basic protection. Mounting sustainability expectations are reshaping material choices and lifecycle models, while consolidation among tier-one suppliers is realigning bargaining power across the value chain. Collectively, these forces position the personal protective equipment market for sustained double-digit expansion during the second half of the decade.

China's updated Work Safety Law obliges high-risk sectors to deploy connected PPE that streams exposure data in real time, boosting premium-grade demand across the region . India's Occupational Safety, Health and Working Conditions Code is generating similar momentum, prompting Mallcom to invest INR 100 crore (USD 12 million) to expand domestic capacity. Local suppliers are therefore pivoting from low-cost competition toward performance differentiation, raising average selling prices and tightening compliance across supply chains.

The EU's new Extended Producer Responsibility schemes force manufacturers to finance end-of-life collection and recycling of masks and gloves, accelerating R&D in biodegradable polymers. Early pilot programs have recovered up to 60% of materials in single-use categories, turning compliance into a branding advantage for companies such as UVEX and 3M Deutschland.

Healthcare alone has doubled disposable PPE use since 2005, amplifying landfill pressures and carbon footprints. Advocacy groups now spotlight the climate impact of petro-chemical gloves and masks, prompting hospitals to insert sustainability clauses into tender documents. Alternatives such as bio-based polyhydroxyalkanoate gloves are promising but still cost a premium and struggle to meet stringent filtration or tensile requirements. Manufacturers therefore face a profitability squeeze as they pursue parallel R&D paths while maintaining current production lines to satisfy mandatory performance standards. The net effect is a medium-to-long-term drag on margin expansion, particularly for firms heavily weighted toward high-volume disposables.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Respiratory Protection is projected to grow at a 12.48% CAGR through 2031, powered by smart filters with embedded biometric sensors that warn users of abnormal breathing patterns. Gloves retained 28.82% personal protective equipment market share in 2025, supported by cut-resistant fibres and touchscreen-compatible coatings that suit digital shop-floor workflows.

Design improvements now emphasise breathability and weight reduction; Johns Hopkins experts recommend investment in reusable elastomeric respirators to replace legacy single-use models. As buyers evaluate gear on lifecycle cost rather than ticket price, premium variants-often IoT-enabled-are gaining shelf space across institutional and e-commerce channels.

The Personal Protective Equipment (PPE) Market Report is Segmented by Product (Masks, Respirators, Gloves, Suits, Eyewear, Footwear, Helmets, Fall Protection), End-User Industry (Healthcare, Manufacturing, Construction, and More), Distribution Channel (Direct Contracts, Distributors, E-Commerce, Retail), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific held 39.05% of the personal protective equipment market in 2025, underwritten by its outsized manufacturing footprint and expanding construction pipeline. China's chemical, electronics, and ship-building clusters drive bulk orders, while India's medical-device sector is on track to reach USD 20.51 billion by 2029, boosting domestic demand for cleanroom-grade consumables. Governments are scaling fiscal incentives for local PPE production, reducing import dependence and enhancing supply-chain resilience.

North America maintains a robust position characterised by stringent OSHA oversight and early adoption of smart PPE in oil and gas and healthcare. Federal funding for semiconductor expansion is set to lift demand for contamination-control garments, reinforcing the region's premium-product bias. Europe's market is pivoting toward eco-compliance, with circularity deadlines pressuring suppliers to offer take-back schemes and recycled-content portfolios. These sustainability prerequisites act as soft trade barriers that encourage regional sourcing.

The Middle East is the fastest-growing pocket, forecast at a 13.86% CAGR to 2031 on the back of USD 2 trillion worth of mega-projects across Saudi Arabia and the UAE. National regulations now require internationally certified PPE for site workers, opening avenues for premium brands. South America exhibits uneven adoption; Brazil is raising enforcement after high-profile industrial incidents, while fiscal constraints temper acceleration elsewhere. Africa presents a long-horizon opportunity: industrialisation and mining expansion are stepping up enforcement of safety codes, yet supply chains remain nascent, favouring first movers able to localise last-mile distribution.