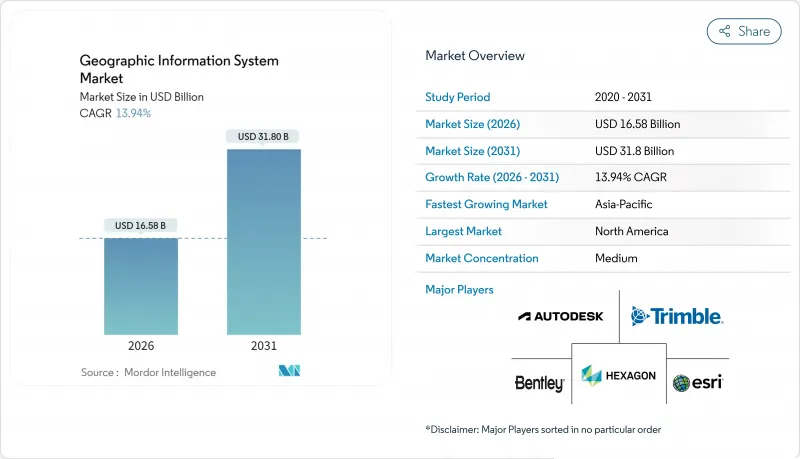

지리정보시스템(GIS) 시장은 2025년에 145억 6,000만 달러로 평가되었고, 2026년 165억 8,000만 달러에서 2031년까지 318억 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 13.94%로 전망됩니다.

스마트 시티의 급속한 전개, 국가 차원의 오픈 데이터 의무화, 클라우드 네이티브의 도입으로 수요는 상승세를 유지하고 있습니다. 30cm 미만의 해상도 화상으로부터의 자동 특징 추출과 실시간 공간 분석에 의해 의사결정이 수주에서 수분으로 단축되어 운송, 석유 및 가스, 공공 안전 분야에서의 도입이 촉진되고 있습니다. 기업이 운영 네트워크와의 확장성과 사이버 보안 확보를 우선시하는 가운데, AI, 엣지 처리, 매니지드 서비스를 통합적으로 제공하는 벤더의 점유율 확대가 계속되고 있습니다.

도시 기관은 지리정보시스템 플랫폼을 5G, IoT, 엣지 컴퓨팅과 통합하여 도시 서비스를 조정합니다. 싱가포르의 오픈 디지털 플랫폼은 지리공간 스트리밍 피드를 통해 지역 냉방, 폐기물, 에너지를 동기화하여 사고 대응력과 인프라 가동률을 향상시키고 있습니다. 로스앤젤레스는 실시간 대시보드를 활용하여 긴급 대응 팀을 지원하며 피크 시에는 350만회의 상황 인식 맵 열람 횟수를 기록하고 있습니다. 지자체가 디지털 트윈의 도입 예산을 계상하는 가운데 확장 가능한 3D 시각화, 센서 API, 사이버 보안 강화를 제공하는 벤더가 공공 부문의 IT 지출에서 점유율을 획득하고 있습니다.

Bell Canada는 클라우드 네이티브 지리공간 데이터 플랫폼으로 전환하여 인프라 지출을 40-60% 절감했습니다. 이는 컨테이너화된 마이크로서비스와 매니지드 업그레이드가 배포 사이클을 단축하는 좋은 예입니다. Kubernetes의 ArcGIS Enterprise 및 유사한 솔루션은 GIS 운영을 DevOps 파이프라인과 통합하여 재해 발생 시 조달 지연 없이 동적 스케일링을 가능하게 합니다. 클라우드 데이터 웨어하우스의 푸시다운 분석은 ETL의 병목 현상을 없애고 지리정보시스템(GIS) 시장의 범위를 기존 매핑 팀을 넘어 확대합니다.

현대 GIS와 수십년전부터 사용되고 있는 SCADA를 통합하는 유틸리티 제공자는 데이터 모델 불일치, 프로토콜 격차, 새로운 사이버 위협의 표면화에 직면해 있습니다. Liberty Utilities는 반복적인 테스트와 미들웨어 개발로 마이그레이션 일정을 18개월 연장했습니다. 이러한 지연은 지출을 전문 서비스로 이동시키고 지리정보시스템 시장에서 소프트웨어 전환을 지연시킵니다.

지리정보시스템 시장에서 서비스 부문의 매출은 2026년에 급증하여 기업 클라우드 마이그레이션, AI 모델 조정, 수명 주기 지원의 외부 위탁으로 15.45%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다. 매니지드 서비스 번들은 현재 데이터 품질 감사, 보안 패치 적용, 24시간 365일 모니터링을 제공하면서 지출을 자본 예산에서 운영 예산으로 전환하고 있습니다. 소프트웨어는 여전히 2025년 매출의 53.60%를 차지하였으며, ArcGIS, Hexagon NetWorks 및 Trimble Cityworks 포트폴리오가 핵심을 이루고 있습니다. 지속적인 업데이트 사이클에서 Esri는 연간 매출의 약 28%를 R&D에 재투자하여 기능 개발 속도를 유지하고 있습니다. 한편, 오픈 API 프레임워크는 타사 확장 기능의 채택을 촉진하고 있습니다. GNSS 수신기, 라이더 스캐너, 내충격 태블릿 등 하드웨어는 여전히 필수적이지만, 기능이 소프트웨어 계층으로 전환함에 따라 이익률은 감소하는 경향이 있습니다. 그러므로 센서 수가 증가함에도 불구하고 순수한 하드웨어 출하에 연결되는 지리정보시스템 시장의 규모는 점점 더 낮은 성장률을 보이고 있습니다.

업계의 구매 담당자는 성과 지향 서비스 수준의 계약을 제공할 수 있는 공급업체를 선호합니다. 예를 들어, 헥사곤이 2025년 비핵심 자산을 매각한 결정은 구독 지원 제공을 강화하기 위한 자본 해방 사례입니다. 교육 아카데미, DevOps 툴체인 및 공인 파트너 네트워크는 현재 중요한 선정 기준을 형성하고 있으며 GIS 시장 전반에 걸쳐 라이선스 수에서 고객 성공 지표로 전환하고 있습니다.

2025년 매핑은 34.10%의 점유율을 차지하였으며 모든 다운스트림 워크플로에 공간적 맥락을 제공합니다. 그러나 엣지 추론, 파운데이션 모델 및 데이터 레이크 하우스 아키텍처를 지원하는 애널리틱스 하위 부문이 15.70%의 연평균 복합 성장률(CAGR)로 가장 빠르게 확대되고 있습니다. 기업은 예측형 지오펜싱을 ERP에 통합하고, 행정기관은 멀티스펙트럼 스택에 의한 도시 히트 아일랜드의 모델링을 실시했습니다. 측량 분야는 안정적이면서도 드론 사진 측량 기술에 의해 혁신이 진행되어, 기존에 1주일이 소요되었던 지형 데이터 취득을 당일 납품 가능한 수준으로 단축하고 있습니다.

텔레매틱스는 전기자동차의 경로 최적화와 콜드체인 모니터링으로 성과를 올리고 있으며 EV 전용 항속 거리 계산을 통합하고 있습니다. 위치 서비스는 상점 내 홍보를 제공하는 하이퍼 개인화 소매 앱을 통해 발전하고 있지만, 네이티브 스마트폰 OS API와의 경쟁에 의해 벤더의 이익률은 억제되고 있습니다. 전반적으로 지리정보시스템 시장에서는 종합적인 데이터 패브릭 원칙에 따라 기능 로드맵을 조정하고 통합, 카탈로그화 및 AI 파이프라인을 단일 거버넌스 산하에 통합하고 있습니다.

북미는 2025년 매출의 37.80%를 유지했습니다. 이는 성숙한 클라우드 인프라, 견조한 R&D 자금, 상호 운용성 및 메타데이터를 표준화하는 미국 지리공간 데이터법 등 정부 기관의 의무화 때문입니다. 연방 프로그램은 산불 모델링, 광대역 자산 매핑 및 중요 인프라의 내성 강화를 위해 다개년 예산을 확보하고 있습니다. Trimble과 같은 기업들은 연간 6억 6,000만 달러 이상을 혁신에 투자하여 이 지역의 기술적 우위를 강화하는 특허 기술을 개발하고 있습니다. 그러나 클라우드 스토리지 요금의 상승은 페타바이트급 이미지 분석에서 비용 과제가 되어 지역 주권형 클라우드 구축을 위한 협의를 촉진하고 있습니다.

아시아태평양은 메가시티의 현대화와 인프라 자극책에 힘입어 가장 높은 15.95%의 연평균 복합 성장률(CAGR)을 달성할 전망입니다. 싱가포르는 공간 제약 완화를 위해 3D 지하 매핑을 확대하고 인도의 디지털 트윈 계획은 물류 회랑과 통합된 구획 수준의 지적 정보를 연계시킵니다. 사우디아라비아가 네이버와 10억 달러 규모로 진행하는 디지털 트윈 협업은 걸프 국가의 스마트 시티 주도권 획득에 대한 의욕을 부각하고 있습니다. 지역적 과제로는 단편화된 데이터 거주 규칙과 수출 규제의 차이를 들 수 있지만, 국내 위성 발사와 주권 클라우드 존의 정비에 의해 의존도가 낮아지고 있습니다.

유럽의 성장은 안정적이며 고부가가치 데이터 세트의 민주화를 추진하는 INSPIRE 지침이 기반이 되고 있습니다. 오픈 액세스로 기후 위험 평가와 신재생 에너지 입지 분석을 전문으로 하는 스타트업이 탄생했습니다. GDPR(EU 개인정보보호규정)은 아키텍처 설계에 영향을 미치며 개인정보 보호 강화 계산과 역내 처리를 촉진합니다. 남미, 중동 및 아프리카는 전체적으로 규모는 작지만, 광물 탐사, 정밀 농업, 인프라 보안 분야에서 도입이 급증하고 있습니다. 이러한 시장에서는 기존 시스템을 건너 뛰고 클라우드 네이티브 GIS를 처음부터 도입하는 경우가 많아 신규 수요에 의한 지리정보시스템 시장의 확대에 기여하고 있습니다.

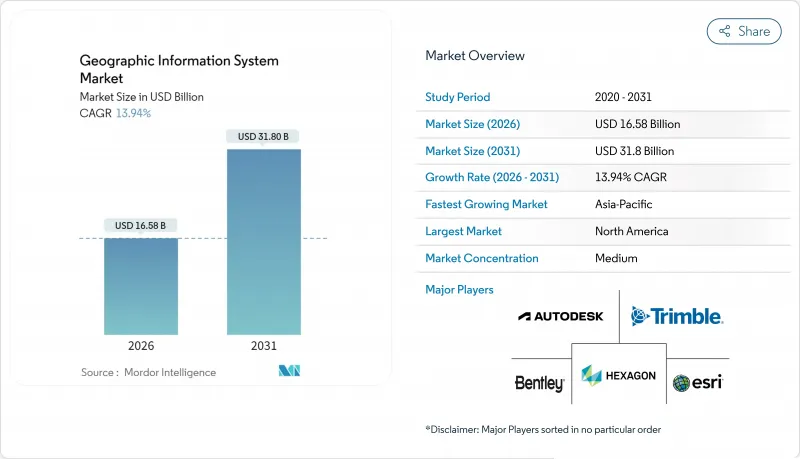

The Geographic Information System market was valued at USD 14.56 billion in 2025 and estimated to grow from USD 16.58 billion in 2026 to reach USD 31.8 billion by 2031, at a CAGR of 13.94% during the forecast period (2026-2031).

Rapid smart-city roll-outs, national open-data mandates, and cloud-native deployments keep demand on an upward slope. Automated feature extraction from sub-30 cm imagery and real-time spatial analytics now reduce decision latency from weeks to minutes, pushing adoption in transportation, oil and gas, and public safety applications. Vendors that bundle AI, edge processing, and managed services continue to gain share as enterprises prioritize scalability and cyber-secure integration with operational networks.

City agencies are integrating the Geographic information system market platforms with 5G, IoT, and edge compute to orchestrate urban services. Singapore's Open Digital Platform synchronizes district cooling, waste, and energy through streaming geospatial feeds, improving incident response and infrastructure uptime. Los Angeles uses real-time dashboards to route emergency crews, drawing 3.5 million situational-awareness map views during peak events. As municipalities budget for digital twins, vendors that deliver scalable 3D visualization, sensor APIs, and cybersecurity hardening capture a growing portion of public-sector IT spend.

Bell Canada saved 40-60% in infrastructure outlay by shifting to a cloud-native geospatial data platform, illustrating how containerized micro-services and managed upgrades shorten deployment cycles. ArcGIS Enterprise on Kubernetes and similar offerings align GIS operations with DevOps pipelines, allowing dynamic scaling during disaster events without procurement delays. Push-down analytics in cloud data warehouses eliminate ETL bottlenecks, widening the Geographic information system market addressable base beyond traditional mapping teams.

Utilities merging modern GIS with decades-old SCADA confront data-model mismatches, protocol gaps, and new cyber-threat surfaces. Liberty Utilities extended its migration timeline by 18 months due to iterative testing and middleware development. These overruns shift spending toward professional services, slowing software conversions in the Geographic information system market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Services revenue in the Geographic information system market rose sharply in 2026, advancing at a 15.45% CAGR as enterprises outsourced cloud migration, AI model tuning, and lifecycle support. Managed-service bundles now cover data-quality audits, security patching, and 24/7 monitoring, shifting spending from capital to operating budgets. Software still accounts for 53.60% of 2025 sales, anchored by the ArcGIS, Hexagon NetWorks, and Trimble Cityworks portfolios. Their continuous update cadence, Esri reinvests roughly 28% of annual turnover into R&D, keeping feature velocity high, while open-API frameworks welcome third-party extensions. Hardware remains essential for GNSS receivers, lidar scanners, and rugged tablets, yet margins compress as more functions migrate into the software layer. The geographic information system market size tied to pure hardware shipments therefore grows more slowly, even as sensor count climbs.

Industry buyers favor vendors that can deliver outcome-oriented service-level agreements; for example, Hexagon's 2025 decision to divest non-core assets freed capital to bolster subscription support offerings. Training academies, DevOps toolchains, and certified partner networks now form critical selection criteria, signaling a pivot from license counts to customer success metrics across the Geographic information system market.

Mapping held a 34.10% share in 2025, furnishing the spatial context for every downstream workflow. Yet the analytics sub-segment is expanding fastest at 15.70% CAGR, powered by edge inference, foundation models, and data-lakehouse architectures. Enterprises embed predictive geofencing into ERPs, while authorities model urban heat islands through multi-spectral stacks. Surveying remains steady, reinvented through drone photogrammetry that compresses week-long terrain captures into same-day deliverables.

Telematics gains from electric-vehicle routing and cold-chain monitoring, integrating EV-specific range calculations. Location-based services flourish via hyper-personalized retail apps that trigger in-store promotions, though competition from native smartphone OS APIs keeps vendor margins in check. Overall, the Geographic information system market aligns functional roadmaps around holistic data-fabric principles, merging ingestion, cataloging, and AI pipelines under a single governance umbrella.

The Geographic Information System (GIS) Market Report is Segmented by Component (Hardware, Software, and Services), Function (Mapping, Surveying, and More), Deployment Mode (On-Premise and Cloud), End-User Industry (Agriculture, Utilities, Mining, Construction, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America preserved 37.80% of 2025 spending, thanks to mature cloud infrastructure, robust R&D funding, and agency mandates like the U.S. Geospatial Data Act that standardize interoperability and metadata. Federal programs secure multi-year budgets for wildfire modeling, broadband equity mapping, and critical-infrastructure resilience. Enterprises such as Trimble invest more than USD 660 million annually in innovation, generating patents that reinforce the region's technological edge. Yet rising cloud-de-storage fees pose cost challenges for petabyte-class imagery analytics, motivating negotiations for localized sovereign clouds.

Asia-Pacific is on track for the highest 15.95% regional CAGR, fuelled by megacity modernization and infrastructure stimulus. Singapore scales 3D underground mapping to mitigate space constraints, while India's Digital Twin Mission links logistics corridors with unified parcel-level cadasters. Saudi Arabia's USD 1 billion digital-twin collaboration with Naver underscores Gulf ambitions for smart-city leadership. Regional hurdles include fragmented data-residency rules and varying export controls, yet domestic satellite launches and sovereign cloud zones are mitigating dependencies.

Europe's growth remains steady, anchored by the INSPIRE directive that democratizes high-value datasets. Open access spawns start-ups specializing in climate-risk scoring and renewable-siting analytics. GDPR influences architecture design, spurring privacy-enhancing computation and in-region processing. South America, the Middle East, and Africa together represent a smaller base but display accelerated adoption in mineral exploration, precision agriculture, and infrastructure security. These markets often leapfrog legacy systems, adopting cloud-native GIS from inception, thereby enlarging the Geographic information system market size through greenfield demand.