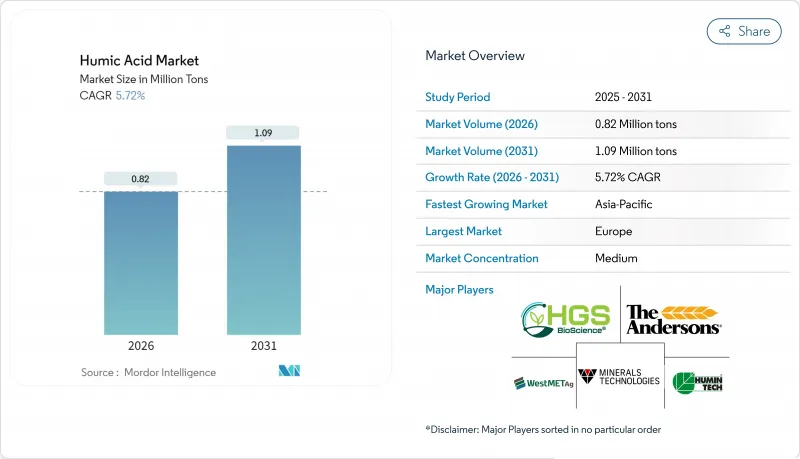

후민산 시장은 2025년 78만톤에서 2026년에는 82만톤으로 성장하고 2026년부터 2031년에 걸쳐 CAGR 5.72%를 나타낼 전망입니다. 2031년까지 109만톤에 달할 것으로 예측되고 있습니다.

이 성장 궤적은 정부에 의한 비료 규제의 강화와 탄소 시장에서의 토양 유기 탄소 증가분의 금전적 평가가 진행됨에 따라 생물 유래의 토양 건강 솔루션의 수용이 확산되고 있음을 반영하고 있습니다. 재생 농업의 확대와 환경 제어 농업 수요가 함께 농업 밸류 체인 전체의 조달 전략이 재구성되고 있습니다. 품질의 일관성을 증명하고 정밀 적용 기술과 통합하는 제조업체는 고부가가치 작물 부문에서 선구자 우위를 확보했습니다. 한편, 기후 변화 관련 금융 메커니즘은 토양탄소를 증가시키는 투입자재에 대한 농가의 투자 의욕을 촉진하고, 후민산제품을 임의의 토양개량제로부터 수익을 창출하는 기후자산으로 격상하고 있습니다.

정부기관은 현재 토양유기탄소를 거래가능한 지표로 정량화하고 있으며, 후민계 자재를 코스트센터에서 수익원으로 전환하고 있습니다. 미국 농무부(USDA)는 2024년 '프랙티스 코드 336'을 도입하여 퇴비와 바이오 찰을 적용하여 토양 유기물을 증가시킨 생산자에게 상환을 시작했습니다. 유럽의 탄소 프로그램도 마찬가지로 측정 가능한 토양 탄소 저장량 증가에 대한 크레딧을 부여하고, 후민계 제품을 규제 준수를 충족시키면서 농가에게 추가 수입원을 가져오는 툴로 변용하고 있습니다. 금융기관은 이러한 크레딧을 녹색 금융 상품에 통합하여 투입 자재 구매를 위한 자금 조달 수단을 확대하고 있습니다. 검증 프로토콜이 엄격해지면서 감사된 추적성은 후민산 시장에서 제품 차별화 요인이 되어 표준화된 시험과 디지털 보고 플랫폼을 가진 기업을 우위로 하고 있습니다. 지역별 탄소계획이 성숙함에 따라 중기적으로는 북미와 EU에서 도입이 가속화된 후 아시아태평양으로 확대될 전망입니다.

재생 농업 시스템은 미생물 활성, 영구적인 지피, 다양한 윤작을 중시합니다. 이들은 모두 부식질이 양이온 교환 용량을 높이고 근권 미생물총을 키우는 것으로 효과를 발휘하는 수법입니다. 인도에서는 제도적 추진력이 현저합니다. 이 나라의 '자연농법추진국가미션'은 1만 곳의 바이오투입자원센터를 지원하여 75만 헥타르에서의 바이오투입 도입을 목표로 하며, 이로써 지역의 부식질 생산자에 대한 안정적인 인수를 보장합니다. 북미에서는 식품기업이 재생농업의 제작면적 목표를 내걸고 적합농가에게 가격 프리미엄을 제공하는 공급체인 계약에 후민질 투입을 포함하고 있습니다. 재생 유기 인증 프로그램이 토양 유기물 지표에 휴민산의 기여를 입증함에 따라 장기적인 수요가 구조화되고 있습니다. 기술 기업은 농장 관리 소프트웨어에 토양 건강 대시보드를 통합하고 실험실의 유기 탄소 데이터를 실용적인 적용 가이드로 변환하여 반복 구매를 촉진합니다.

비색시험과 추출 프로토콜의 차이로 인해 후민산 측정치에 최대 40%의 편차가 생겨 구매자의 신뢰를 해치는 사태가 발생하고 있습니다. 생산자가 브랜드 간의 표시 내용을 비교할 수 없는 경우 가격이 유일한 차별화 요인이 되어 진정한 생산자의 이익률이 저하될 우려가 있습니다. AOAC(공정분석법협회) 라머법이나 HPTA(후민제품무역협회) 가이드라인은 확고한 기준을 제공하고 있습니다만, 검사비용이나 EU역외에서의 규제집행 부족으로 도입이 진행되고 있지 않습니다. 규제 당국이 표시 감시 자원이 부족한 지역에서는 후민산 농축물과 위장한 합성 요소 혼합물이 유통 경로에 범람하여 단기적인 시장 침체가 심화되고 있습니다. 프리미엄 브랜드는 QR 코드에 의한 추적성과 제3자 기관의 검사 증명서로 대응하고 있지만, 이러한 안전 대책의 확대는 여전히 불균일하며, 후민산 시장의 단기적인 수량 증가를 제한하고 있습니다.

액체 농축물은 시비 관개 및 엽면 살포 플랫폼과의 통합에 의해 견인되어 2031년까지 연평균 복합 성장률(CAGR) 6.68%로 가장 빠른 성장 궤도를 기록할 전망입니다. 액체 후민산 시장은 수직 농장과 정밀 농업에서의 채용 확대에 따라 상승이 예상됩니다. 미립자 및 분말 형태는 광범위한 곡물 재배의 핵심 제품이지만, 가격 중심의 포지셔닝은 이익률 상승을 제한합니다. 액체 부문의 경쟁적 차별화는 고농도(후민산 12% 이상)에서의 안정성과 칼슘이 풍부한 수질의 적합성에 의존합니다. 제조업체는 침전 억제를 위한 킬레이트화 기술에 투자하고 1,000리터 토트에서의 출하를 실현함으로써, 헥타르당의 물류 비용을 대폭 삭감하고 있습니다.

분말 제제는 2025년 시점에서 후민산 시장의 33.75%의 점유율을 유지했고 대규모 원예 분야에서 액체 제품이 지지를 모으면서 점유율의 감소에 직면했습니다. 적하관개시스템이 정비되지 않은 신흥경제국의 협동조합에서는 수작업에 의한 살포가 주류이기 때문에 분말제품은 여전히 비용효과가 우수합니다. 미국의 혼합 제조업체는 우레아 기반 NPK 비료에 미분화된 후민산 분말을 첨가하여 유통 효율을 높임으로써 이 부문의 지속성을 유지하고 있습니다. 그러나 수명주기 분석에 따르면 액체 비료는 분말 비료보다 Kg 당 효능이 우수하며 범위 3 배출량 보고에서 중요시되는 지표인 탄소 실적가 낮음을 보여줍니다. 생산자는 이에 대응하고 태양광 발전에 의한 건조 라인을 도입하여 탄소 중립 분말 비료를 시장에 투입하고 지속가능성에 대한 인식의 격차를 메우고 있습니다.

후민산 시장 보고서는 형태(분말, 미립자, 액체), 용도(유기 비료, 동물사료, 기타 용도), 지역(아시아태평양, 북미, 유럽, 남미, 중동, 아프리카)별로 분류되어 있습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

아시아태평양의 후민산 시장은 공공 부문에 의한 바이오 투입 자재 도입의 제도화 프로그램을 원동력으로 CAGR 7.18%로 가속하고 있습니다. 인도의 1,974억 4,000만 루피 규모의 PM-PRANAM계획에서는 합성비료 보조금의 삭감액에 따라 주정부에 상환이 이루어지기 때문에 농업부문은 협동조합을 통해 후민산과립을 배포하고 있습니다. 중국의 14차 5개년 계획에서는 토양건강연구개발(R&D) 자금이 확보되고 지방정부는 액체 후민농축액과 세트의 점적관개 키트를 보조하고 있습니다. 카르나타카의 데이터 플랫폼 시험 운영은 토양 검사 결과와 QR 코드가 포함된 후민 제품 추천 정보를 통합하여 보급 서비스의 병목 현상을 제거합니다. 이 지역의 광범위한 소규모 농가층은 베트남에서 선구적으로 도입된 마이크로팩 포장 모델을 통해 후민산 자재를 채용하고 있습니다. 이러한 구조적 개입에 의해 안정된 수요 기반이 확립되어 규모 생산과 지역 밀착형 배합 플랜트가 추진되어 수입 의존도의 저감을 도모하고 있습니다.

유럽은 CE 마킹의 조화와 2024년 기준에서 1,600만 헥타르를 넘는 정착한 유기농지 면적에 의해 후민산 시장의 32.10%를 차지했습니다. 소매업체의 프라이빗 브랜드 프로그램에서는 바이오 자극제의 사용이 「플래닛 스코어」선반 표시의 취득 조건이 되어, 과일·야채 부문에서 수요를 확대하고 있습니다. EU(유럽연합) 혁신기금을 이용한 카본파밍의 파일럿 사업에서는 후민산에 의한 유기탄소 증가를 수익화하고 있으며, 후민산 공급업체는 원격센싱 플랫폼과 함께 검증기관으로서의 지위를 확립하고 있습니다. 저탄소 식품의 브랜딩이 수익원을 확대해, 고가격대의 과일 카테고리에서는 후민산엽면 살포에 의해 당도(Brix)와 색도 지수를 향상시켜, 품질 연동형 가격 설정을 실현하고 있습니다. 그러나 유럽 유통업체는 2024년 이후 해상 수송 혼란으로 인한 수입 비용 상승에 직면하여 공급 안정화를 위해 지역 내 이탄지 채굴과 갈탄 처리 시설에 대한 투자를 촉진했습니다.

북미 수요는 꾸준히 증가하는 반면, 시장 분단화가 진행되고 있습니다. 미국에서는 보전 혁신 보조금을 활용하여 탄소 효율형 공급망에서 푸민 질 배합 자재를 평가하는 주 차원의 파일럿 사업을 지원하고 있습니다. 아이오와주와 일리노이주 대규모 협동조합에서는 후민산 투여 모듈을 자체 가변 시비 플랫폼에 통합하여 서비스 패키지를 구축하고 있습니다. 캐나다 온실 재배 사업자는 CFIA(캐나다 식품 검사청) 기준을 준수하기 때문에 중금속 함량이 100ppm 미만인 순도 보증 액체 제품에 대한 집중적인 수요를 견인하고 있습니다. 브라질 남미 수출 대두 복합시설에서는 재생농업인증 수출계약을 지원하기 위해 후민산 강화를 시용하고 있습니다. 한편 중동 및 아프리카의 생산자는 특히 이집트의 백만 페단(약 666만 헥타르)의 토지 개량 프로젝트에 있어서 염해 토양 과제의 완화에 부식 제품을 채용하여 가뭄 내성의 강화를 도모하고 있습니다. 각 지역의 고유한 농학적 과제가 독자적인 가치 제안을 낳고 있으며, 세계의 후민산 시장에서는 적응적인 마케팅이 요구되고 있습니다.

The Humic Acid market is expected to grow from 0.78 million tons in 2025 to 0.82 million tons in 2026 and is forecast to reach 1.09 million tons by 2031 at 5.72% CAGR over 2026-2031.

This trajectory reflects broadening acceptance of biologically derived soil-health solutions as governments tighten fertilizer regulations and carbon markets monetize soil organic carbon gains. Expansion of regenerative farming, coupled with demand from controlled-environment agriculture, reshapes procurement strategies across the agricultural value chain. Manufacturers that prove quality consistency and integrate with precision-application technology capture early-mover advantages in high-value crop segments. Meanwhile, climate-linked finance mechanisms fuel farmers' willingness to invest in inputs that boost soil carbon, elevating humic products from discretionary soil conditioners to revenue-generating climate assets.

Government agencies now quantify soil organic carbon as a tradable metric, shifting humic inputs from cost centers to revenue drivers. The USDA introduced Practice Code 336 in 2024, reimbursing growers who apply compost or biochar that lifts soil organic matter. European carbon programs similarly assign credits to measurable gains in soil carbon stocks, turning humic products into tools that meet compliance while earning farmers additional income streams. Financial institutions bundle these credits into green-finance products, broadening access to capital for input purchases. As verification protocols sharpen, audited traceability becomes a product differentiator in the Humic Acid market, favoring firms with standardized testing and digital reporting platforms. Medium-term uptake accelerates in North America and the EU before spreading to APAC as regional carbon schemes mature.

Regenerative systems emphasize microbial activity, permanent ground cover, and diversified rotations-all practices that thrive when humic substances elevate cation-exchange capacity and foster root-zone microbiomes. India illustrates institutional momentum: its National Mission on Natural Farming backs 10,000 Bio-Input Resource Centers targeting 750,000 ha for bio-input adoption, ensuring stable offtake for local humic producers. In North America, food companies commit to regenerative acreage targets, embedding humic inputs in supply-chain contracts that offer price premiums to compliant growers. Long-term demand becomes structural as certification programs such as Regenerative Organic validate humic acid's contribution to soil-organic-matter metrics. Technology firms integrate soil-health dashboards into farm-management software, translating laboratory organic-carbon data into actionable dosing guides that drive repeat purchases.

Colorimetric tests and divergent extraction protocols yield humic readings that can vary by 40%, undermining buyer confidence. When growers cannot compare label claims across brands, price becomes the sole differentiator, eroding margins for authentic producers. The AOAC (Association of Official Analytical Communities) Lamar method and HPTA (Humic Products Trade Association) guidelines offer robust baselines, yet adoption lags due to testing fees and a lack of enforcement outside the EU. Short-term market drag intensifies in regions where regulators lack resources to police labeling, allowing synthetic urea blends masquerading as humic concentrates to flood distribution channels. Premium brands respond with QR-code traceability and third-party lab certificates, but scale-up of these safeguards remains uneven, limiting near-term volume gains for the Humic Acid market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Liquid concentrates logged the fastest trajectory at 6.68% CAGR through 2031, propelled by integration with fertigation and foliar-spray platforms. The Humic Acid market for liquids is projected to rise amid rising adoption by vertical farms and precision-ag operations. Granular and powdered forms remain staples for extensive cereal cropping, but their price-led positioning limits upside on margins. Competitive differentiation in the liquid tier hinges on stability at high concentrations (>= 12% humic fraction) and compatibility with calcium-rich waters. Manufacturers invest in chelation technology to suppress sedimentation, allowing 1,000-L tote shipments that slash per-hectare logistics costs.

Powdered formulations, while retaining 33.75% Humic Acid market share in 2025, face incremental erosion as liquids gain favor with large-scale horticulture. Powder remains cost-effective for cooperatives in emerging economies that lack drip-system infrastructure, where manual broadcasting prevails. Blending houses in the United States add micronized humic powder to urea-based NPK, achieving distribution efficiencies that keep this segment resilient. However, lifecycle analyses illustrate lower carbon footprints for liquids, as their efficacy per kilogram surpasses powders, a metric increasingly scrutinized under scope-3 emissions reporting. Producers counter by deploying solar-powered drying lines to market carbon-neutral powder, bridging the sustainability narrative gap.

The Humic Acid Market Report is Segmented by Form (Powdered, Granular, and Liquid), Application (Organic Fertilizer, Animal Feed, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific's Humic Acid market accelerates at 7.18% CAGR, fueled by public-sector programs institutionalizing bio-input adoption. India's Rs 19,744 crore PM-PRANAM scheme reimburses states based on reductions in synthetic-fertilizer subsidies, prompting agriculture departments to distribute humic granules via cooperatives. China's 14th Five-Year Plan earmarks soil-health R&D (research and development) funding, and provincial governments subsidize drip-fertigation kits bundled with liquid humic concentrates. Data-platform pilots in Karnataka integrate soil-test results with QR-coded humic product recommendations, lowering extension-service bottlenecks. The region's vast smallholder base adopts humic inputs through micro-pack sachets, a packaging model pioneered in Vietnam. These structural interventions establish reliable offtake, driving scale production and localized formulation plants that reduce import dependency.

Europe commands 32.10% Humic Acid market share owing to harmonized CE marking and entrenched organic-farming acreage exceeding 16 million ha in 2024. Retailer private-label programs stipulate biostimulant usage to earn "Planet Score" shelf labels, amplifying demand in the fruit and vegetable sectors. Carbon-farming pilots under the EU (European Union) Innovation Fund monetize humic-induced organic-carbon gains, positioning humic suppliers as verifiers alongside remote-sensing platforms. Low-carbon food branding expands revenue pools, and premium-priced fruit categories use humic foliar sprays to enhance Brix and color indices, forging quality-linked pricing. European distributors, however, face rising import costs after 2024 maritime freight disruptions, prompting investment in regional peat-bog extraction and lignite-processing facilities to secure supply resilience.

North American demand grows steadily but faces fragmentation. The United States deploys Conservation Innovation Grants to fund state-level pilots that evaluate humic blends in carbon-smart supply chains. Large cooperatives in Iowa and Illinois integrate humic dosing modules into in-house variable-rate platforms, creating bundled service packages. Canadian greenhouse operators drive concentrated demand for liquids with purity guarantees below 100 ppm heavy metals to comply with CFIA (Canadian Food Inspection Agency) standards. South America's export soybean complexes in Brazil incorporate humic enrichments to support regenerative-certified export contracts. Meanwhile, Middle East & African growers adopt humic products to mitigate saline-soil challenges, especially in Egypt's million-feddan reclamation project, reinforcing drought-resilience positioning. Each region's specific agronomic pressures carve distinct value propositions, requiring adaptive marketing in the global Humic Acid market.