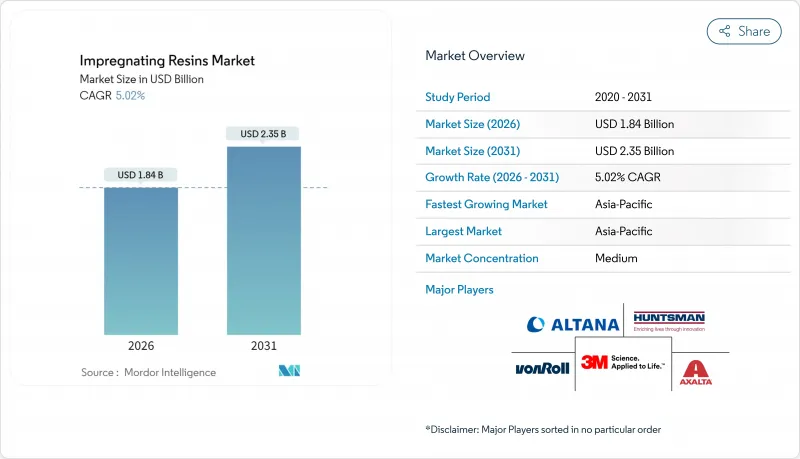

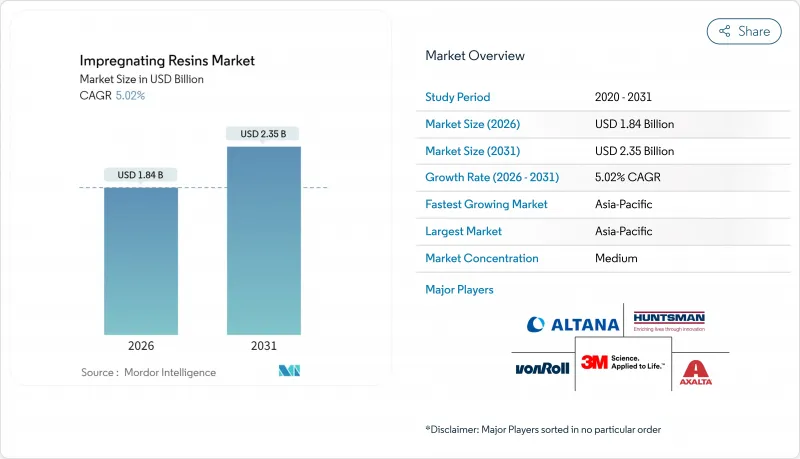

세계의 함침 수지 시장은 2025년 17억 5,000만 달러로 평가되었으며, 2026년 18억 4,000만 달러에서 2031년까지 23억 5,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중(2026-2031년) CAGR은 5.02%로 예상됩니다.

모터, 발전기, 변압기, 파워 일렉트로닉스 모듈에서 고효율 전기 절연재에 대한 견조한 수요가 이러한 확대를 지원합니다. 재생에너지 및 전동 이동성 플랫폼의 내구성 있는 성능을 지원하기 위해 절연 내력을 향상시키고 부분 방전 손실을 줄이는 진공 가압 함침(VPI) 시스템을 OEM 제조업체가 점점 지정하는 경향이 있습니다. 해상 풍력 터빈의 대형화, 고전압 전기자동차의 보급, 스마트 그리드의 고도화에 의해 고품질 액체 절연재의 다년간에 걸친 조달 파이프라인이 강화되고 있습니다. 첨단 VPI 설비에 대한 지속적인 자본 수요는 수지와 기계 설비를 수직으로 통합한 제품 라인을 보유한 기존 제조업체들에게 유리하게 작용하며, 함침 수지 시장의 집중화가 점차 진행되고 있습니다.

세계 규정에 따라 산업용 모터의 손실 제한이 더욱 엄격해지고 있습니다. 미국에서는 에너지부의 개정 규칙에 따라 마력 등급별로 최소 공칭 효율이 의무화되고 있습니다. 이러한 기준값은 핫스팟 온도 감소, 진동 억제, 리와인드 간격의 연장을 실현하는 VPI 처리된 권선의 리노베이션을 촉진합니다. 제조업체는 에너지 감사 기준을 충족하기 위해 180℃ 내열 등급에 해당하고 저손실 계수를 나타내는 함침 수지를 지정합니다. 공장이 운용 비용 절감을 추구하는 가운데, 함침 수지 시장에서는 리와인드 키트나 현장 서비스용 수지에 대한 안정된 애프터마켓 수요를 볼 수 있습니다. 동남아시아와 라틴아메리카의 중규모 산업 거점에서도 유사한 교환 사이클이 재현되어 중기적인 성장세를 강화하고 있습니다.

미국 환경보호청(EPA)의 2025년 에어로졸 코팅 반응성 개정 규제 및 유럽의 휘발성 유기 화합물(VOC) 배출 상한 강화로 규제 대상 용제를 전혀 방출하지 않는 100% 고형분 시스템으로의 이행이 가속화되고 있습니다. 무용제 수지는 진공 하에서 권선 스택에 효율적으로 침투하여 제어된 열 하에서 더 빠르게 중합하므로 작업자의 노출 위험을 없애고 ISO 14001 인증을 획득할 수 있습니다. Gehring의 IMFLEX와 같은 유도 가열식 트리클 라인은 기존의 침지 및 소성 라인에 비해 사이클 타임을 20% 단축하는 공정 유연성을 보여줍니다. 환기 부하를 줄이고 폐기물 처리 방식을 단순화하여 비용 절감 효과를 통해 신규 플랜트의 무용제 라인은 사실상 설비 투자 옵션이 되었습니다. 이러한 운용상의 이점은 선진국과 신흥국을 불문하고 함침 수지 시장의 성장 궤도를 강화하고 있습니다.

세계 각국의 규제 당국은 산업용 페인트의 VOC 허용치를 계속 낮추고 있습니다. 캐나다의 2024년 규정은 130개 품목의 농도 상한을 설정하고 재배합 또는 시장 철수를 요구합니다. 남부 캘리포니아의 자동차 페인트에 대한 개정 규칙 1151은 전기 절연 응용 분야에서도 유사한 규제 강화를 시사하며 규정 준수 문서 작성 및 테스트 비용을 증가시킵니다. 소규모 수지 제조 업체들은 사내 환경 담당 직원과 솔벤트 회수 설비가 부족한 경우가 많으며, 그린 케미스트리를 우선하는 OEM 계약 획득 경쟁력을 제약하고 있습니다. 2년 이하의 전환 기간에 따라 자본계획의 기간이 압축되어 업그레이드 비용을 흡수하는 것보다 함침 수지 시장에서 철수를 선택하는 지역 기업도 나오고 있습니다.

2025년 함침 수지 시장 점유율의 64.12%를 무용제계 배합이 차지해, 2031년까지 연평균 복합 성장률(CAGR) 5.10%로 전 대체품을 웃도는 성장이 전망됩니다. 이 우위성은 100% 고형분 화학 조성이 진공 중의 에어 포켓 발생 없이 고정자 적층체에 함침을 가능하게 해, 클래스 H 및 클래스 N의 내열 등급을 실현하는 특성에 유래합니다. 이것은 부분 방전 발생을 억제하고 견인용 및 풍력 발전용 고정자의 수명을 연장합니다. 플랜트 운영자는 용제 배제에 의해 방화 규제의 제약이 해소되어 배기 가스 세정 장치의 부하가 대폭 삭감되기 때문에 개수 후 2년 이내에 운용 비용이 축소되는 점을 중시하고 있습니다.

혁신 파이프라인은 자동 적하법 및 롤 침지법을 위한 무용제 레올로지를 지속적으로 개선하고 있습니다. 최근 RSC 문서화된 폴리에스테르 네트워크는 331℃에서 열화 개시 온도와 기준선비 38% 저감의 유전 손실을 달성하여 고주파 인버터에 대한 적용 범위를 확대하고 있습니다. IEEE 275-1992 및 1553-2002 평가 프로토콜은 OEM 인증을 이끌어 새로운 수지 등급이 기존 절연 시스템과 원활하게 통합되도록 합니다. 솔벤트 기반 등급은 가용 시간 연장에 중점을 둔 틈새 리와인드 공장에서 여전히 사용되고 있지만, 규제 및 보험 우대 조치가 고형분 기술에 유리하게 작용하기 때문에 점유율은 해마다 감소하고 있습니다. 그 결과, 조기에 무용제 설비에 투자한 제조업체는 가격 프리미엄과 충성 계약을 획득해, 세계의 함침 수지 시장에서 주도적 지위를 굳히고 있습니다.

함침 수지 보고서는 기술별(무용제 수지, 용제계 수지), 수지 유형별(에폭시, 폴리에스테르, 폴리에스테르이미드, 기타 수지 유형), 용도별(모터 및 발전기, 가전제품, 변압기, 전기 전자 부품 등), 지역별(아시아태평양, 북미, 유럽 등)으로 분류되어 있습니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

아시아태평양은 함침 수지 시장에서 2025년 매출의 41.20%를 차지했고 2031년까지 5.11%라는 가장 빠른 CAGR을 기록할 것으로 예상됩니다. 중국에서 전동기 생산의 우위성이 지역 수요를 활발하게 유지하는 한편, 복건성 및 광동성에서의 해상 풍력 발전 클러스터를 대상으로 한 인센티브가 수지 수요 증가를 보증하고 있습니다. 인도의 고효율 가전을 위한 성능 인센티브는 국내 업체들이 VPI 라인을 확대하는 중 하류 분야에서 큰 기회를 보여줍니다. 동남아시아 국가들은 경쟁력 있는 노동 비용과 증가하는 전자기기 수출을 활용하여 현지 함침 수지 생산 능력을 확보함으로써 세계 OEM 네트워크에 공급하는 지역 공급망의 기반을 구축하고 있습니다.

북미에서는 자동차의 전동화, 회복 기조에 있는 산업 설비 투자, 송전망 현대화 프로그램을 배경으로 성숙하면서도 견조한 수요를 볼 수 있습니다. 주요 수지 제조업체는 현재 미국 및 멕시코 공장을 재생 가능 전력으로 가동하고 있으며 제품의 탄소 발자국을 축소하고 OEM 제조업체에 스코프 3 배출량의 우위성을 가져오고 있습니다. 미국 에너지부의 모터 및 변압기 기준은 리노베이션을 촉진하고 규제 조치를 예측 가능한 수지 판매에 연결합니다. 2024년에 시행되는 캐나다의 VOC 규제는 더욱 무용제화를 추진하고 기술적으로 첨단 공급업체에게 시장 진출 기회를 제공합니다.

유럽에서는 에너지 가격 변동에 직면하면서도 2026년 시행의 REACH 규칙 부속서 XVII 포름알데히드 규제 등 저배출 수지를 우대하는 선견적인 정책이 지속되고 있습니다. 북해 및 발트해에서의 해상 풍력 발전 설비의 설치 페이스는 고성능 실리콘 수요를 고정화해, 가전 생산의 감속을 일부 상쇄하고 있습니다. 외국산 에폭시 수지에 대한 반덤핑 관세는 국내 수지 제조를 지원하지만 다운스트림 공정에 비용 압력도 가해집니다. 전체적으로 함침 수지 시장은 아시아태평양의 규모, 북미의 표준 주도형 업그레이드, 유럽의 환경 기술 리더십이 보완적인 성장의 기둥이 되어 균형 잡힌 지리적 기반을 유지하고 있습니다.

The Impregnating Resins Market was valued at USD 1.75 billion in 2025 and estimated to grow from USD 1.84 billion in 2026 to reach USD 2.35 billion by 2031, at a CAGR of 5.02% during the forecast period (2026-2031).

Robust demand for high-efficiency electrical insulation in motors, generators, transformers, and power-electronics modules underpins this expansion. Original-equipment manufacturers increasingly specify vacuum pressure impregnation (VPI) systems that elevate dielectric strength and cut partial-discharge losses, supporting durable performance in renewables and e-mobility platforms. Scale-up of offshore wind turbines, higher-voltage electric vehicles, and smart-grid upgrades reinforce multi-year procurement pipelines for premium liquid insulation. Persistent capital requirements for advanced VPI equipment favor established players with vertically integrated resin and machinery offerings, gradually concentrating the impregnating resins market.

Global regulations now mandate tighter loss limits for industrial motors; in the United States, updated Department of Energy rules require minimum nominal efficiencies across horsepower classes. These thresholds spur retrofits with VPI-treated windings that cut hot-spot temperatures, reduce vibration, and extend rewind intervals. Manufacturers consequently specify impregnating resins that tolerate 180 °C thermal classes and exhibit a low dissipation factor to meet energy audits. As plants chase operational expense reductions, the impregnating resins market sees stable aftermarket demand for rewind kits and field-service resins. Mid-size industrial hubs in Southeast Asia and Latin America replicate this replacement cycle, reinforcing the medium-term growth impulse.

The U.S. Environmental Protection Agency's 2025 amendments on aerosol-coating reactivity, plus Europe's evolving VOC caps, accelerate the transition to 100% solids systems that release no regulated solvents. Solventless resins penetrate winding stacks efficiently under vacuum, polymerize faster under controlled heat, and remove worker-exposure liabilities, enabling ISO 14001 certification. Induction-heated trickle lines such as Gehring's IMFLEX illustrate process agility, cutting cycle times by 20% versus conventional dip-and-bake lines. Cost savings accrue from lower ventilation loads and simpler waste-treatment schemes, making solventless lines the de-facto capex choice for greenfield plants. These operational gains reinforce the impregnating resins market trajectory in developed and emerging economies alike.

Authorities worldwide keep lowering permissible VOC thresholds for industrial coatings; Canada's 2024 rules cap concentrations across 130 product classes, requiring reformulation or market withdrawal. Southern California's revised Rule 1151 on automotive coatings signals similar tightening for electrical-insulation applications, adding compliance documentation and lab-testing expenses. Smaller resin formulators often lack in-house environmental staff and solvent-recovery infrastructure, constraining their ability to compete for OEM contracts prioritizing green chemistry. Transition timelines of two years or less compress capital-planning windows, prompting some regional players to exit the impregnating resins market rather than absorb upgrade costs.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solventless formulations account for 64.12% of the impregnating resins market share in 2025, outpacing all alternatives with a 5.10% CAGR to 2031. This dominance derives from the ability of 100% solids chemistries to impregnate stator stacks under high vacuum without entrapped air pockets, yielding class H and class N thermal ratings. The resulting reduction in partial-discharge inception bolsters service lives of traction and wind-generator stators. Plant operators emphasize solvent elimination because it removes fire-code constraints and slashes exhaust-scrubber loads, shrinking operating costs within two years of retrofit.

Innovation pipelines continue to refine solventless rheology for automated trickling and roll-dip methods. Recent RSC-documented polyester networks achieve 331 °C onset degradation and 38% lower dielectric loss versus baseline, expanding suitability for high-frequency inverters. IEEE 275-1992 and 1553-2002 evaluation protocols guide OEM qualifications, ensuring that new resin grades integrate seamlessly with existing insulation systems. Solvent-based grades persist in niche rewind shops that value extended pot life, yet their share erodes annually as regulatory and insurance incentives favor solids technology. Consequently, producers that invested early in solventless assets enjoy pricing premiums and loyalty contracts, solidifying leadership positions across the global impregnating resins market.

The Impregnating Resins Report is Segmented by Technology (Solventless Resins and Solvent-Based Resins), Resin Type (Epoxy, Polyester, Polyester-Imide, and Other Resin Types), Application (Motors and Generators, Home Appliances, Transformers, Electrical and Electronic Components, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific accounted for 41.20% of 2025 sales in the impregnating resins market and posts the quickest 5.11% CAGR to 2031. China's dominance in electric-motor production keeps regional demand vibrant, while targeted incentives for offshore wind clusters in Fujian and Guangdong provinces guarantee resin pull-through. India's performance incentives for high-efficiency appliances signal a sizable downstream opportunity as domestic manufacturers scale VPI lines. Southeast Asian nations leverage competitive labor costs and growing electronics exports to source localized impregnating capacity, anchoring regional supply chains that feed global OEM networks.

North America exhibits mature but resilient demand underpinned by automotive electrification, rebounding industrial capex, and grid modernization programs. Major resin suppliers now run U.S. and Mexican plants on renewable electricity, shrinking product carbon footprints and giving OEMs a Scope 3 emissions advantage. U.S. Department of Energy motor and transformer standards drive retrofits, translating regulatory action into predictable resin sales. Canada's VOC rules, effective 2024, further push solventless adoption, giving technologically advanced suppliers a market opening.

Europe navigates energy-price volatility yet sustains forward-looking policy drivers such as REACH Annex XVII formaldehyde limits effective 2026, which favor low-emission resins. Offshore-wind installation rates in the North Sea and Baltic Sea lock in high-performance silicone demand, partially offsetting weaker appliance production. Anti-dumping tariffs on foreign epoxy imports shore up domestic resin manufacturing, though they add cost pressure downstream. Overall, the impregnating resins market retains a balanced geographic footprint with Asia-Pacific's scale, North America's standards-driven upgrades, and Europe's environmental-technology leadership acting as complementary growth pillars.