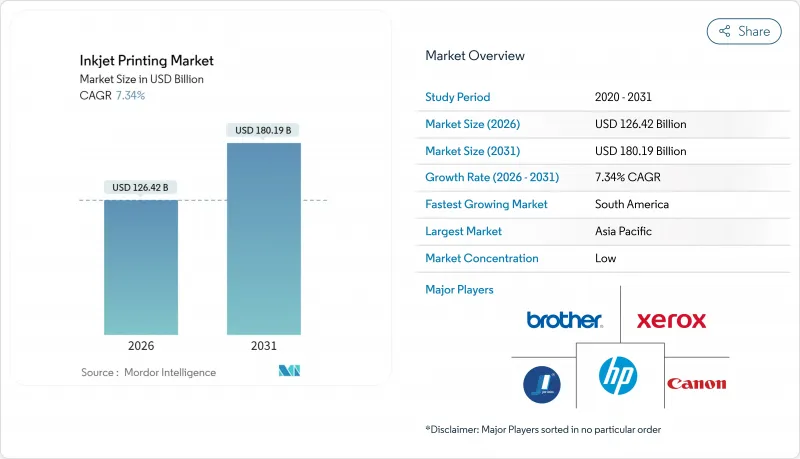

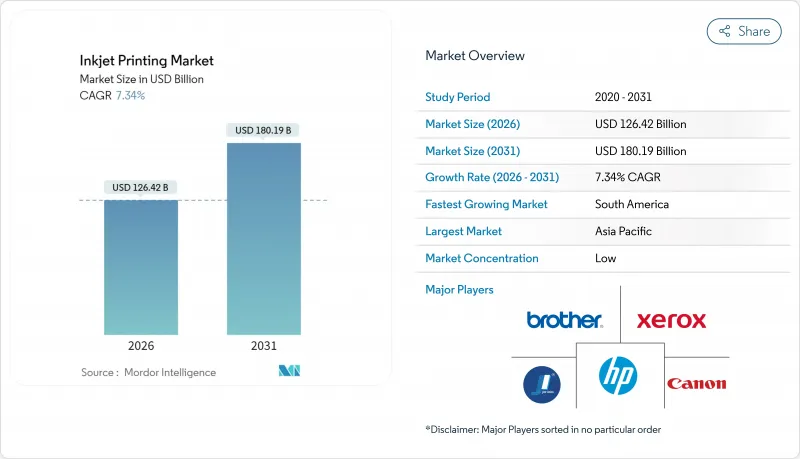

세계의 잉크젯 인쇄 시장은 2025년 1,177억 7,000만 달러로 평가되었으며, 2026년 1,264억 2,000만 달러에서 2031년까지 1,801억 9,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중(2026-2031년) CAGR은 7.34%로 예상됩니다.

현재의 성장세는 데이터가 풍부한 패키징에 대한 수요 증가, 패션 업계에서 온디맨드 섬유 생산으로 전환, 수성 화학물질을 추천하는 규제 압력 등 3개의 기둥에 지지되고 있습니다. 벤더 각사는 하드웨어 중심의 제안에서 총 소유 비용을 줄이고 대량 맞춤화를 지원하는 연결성이 높고 서비스 풍부한 에코시스템으로 이행하고 있습니다. 프린트헤드 기술 혁신 기업 간의 통합과 지역별 현지 생산 촉진책이 함께 경쟁 환경이 재구성되고 있습니다. 동시에 다이레? 투 셰이프, 기능성 일렉트로닉스, 장식 용도와 같은 미개척 영역의 기회도 열리고 있습니다. 잉크젯 인쇄 시장은 이러한 구조적 요인을 포장, 출판, 섬유 및 산업 분야에서 아날로그 시스템을 대체하는 확장 가능한 디지털 대응 워크플로우로 전환함으로써 계속 성장하고 있습니다.

엄격한 추적성 규제와 위조 방지 대책으로 브랜드 소유자는 실시간 가변 데이터 대응을 요구하고 있으며, 이를 효율적으로 스케일할 수 있는 것은 잉크젯 인쇄 시장 뿐입니다. Graphic Packaging International이 도입한 임프린팅 기술은 라인 속도를 유지하면서 배치 레벨 직렬화를 실현하여 고해상도 열 잉크젯이 높은 처리량 환경과 공존할 수 있음을 증명합니다. MapleJet의 모듈식 코딩 시스템은 인라인 통합이 가동 중지 시간을 최소화하고 재생 가능한 필름에서 규제 준수를 보장하는 방법을 추가로 보여줍니다. SUDPACK-LEIBINGER와 같은 협업은 이 접근법을 단일 소재 포장으로 확대하고, 준수 잉크와 재생 가능 기재의 조합이 미래의 EU 목표 하에서 미래를 기대하는 운영을 실현하는 방법을 입증합니다. 시장 전반에서 QR 코드와 동적 디자인 요소를 포함하는 능력은 포장을 수동 용기에서 대화식 브랜드 자산으로 전환하여 혁신적인 잉크젯 플랫폼에 대한 지속적인 수요를 확고히 합니다.

출판사가 재고를 불안정한 소비자 수요에 맞추는 중, 첫회 인쇄 부수는 축소 경향이 계속되고 있습니다. Nielsen BookScan의 데이터에 의하면, 최초 발주수는 2자리수의 감소를 나타내고 있어, 1,000부 미만의 인쇄 부수에서도 오프셋 인쇄 수준의 경제성을 실현하는 매엽 및 웹 잉크젯 장치의 도입을 촉구하고 있습니다. Canon의 신형 B2 디바이스는 시간당 8,700장의 인쇄가 가능해, 손익 분기점을 인하하는 것과 동시에, 소셜 미디어 주도의 판매 급증시에 공급을 보충하는 '갭' 인쇄 전략을 실현합니다. HP의 디지털 생산 플랫폼은 작업 순서 지정 및 마무리 공정 자동화, 인건비 절감, 클라우드 기반 분석의 통합으로 이러한 변화를 더욱 가속화하고 있습니다. 출판사가 마이크로 배치 보충 및 개인화 버전으로 전환하는 동안 잉크젯 인쇄 시장은 창고 비용을 늘리지 않고 이러한 새로운 워크플로우를 수익화 할 수 있는 유일한 기술로 두드러집니다.

마케팅 예산을 프로그래매틱 플랫폼으로 전환하는 과정에서 상업용 인쇄의 대응 가능한 양은 제한되어 있습니다. 광고 대행사는 클릭률 지표와 실시간 기여를 강조하기 때문에 전통적으로 많은 양의 전단지와 카탈로그에 의존했던 인쇄 서비스 공급자는 과제에 직면하고 있습니다. 이에 대응해 기업은 데이터 구동형 개인화를 활용한 고임팩트 직접 메일 및 트랜스프로모 인쇄물로 사업 전환을 진행하고 있습니다. 인쇄 회사는 고유 QR 코드와 로열티 프로그램을 결합하여 관련성을 유지하고 프리미엄 마진을 획득했습니다. 그러나 전반적인 인쇄량 감소는 잉크젯 인쇄 시장의 전통적인 상업 부문에 여전히 부담을 주고 있습니다.

드롭 온 디맨드(DoD) 플랫폼은 2025년 수익의 45.88%를 차지했으며, 다양한 기재에 대한 적응성과 고객이 요구하는 고화질성을 뒷받침하고 있습니다. 주도적 입장에 있지만, DoD의 성장은 감속 경향에 있어, 연속 잉크젯의 CAGR 9.10%가, 중단 없는 고속 코딩을 요구하는 포장 라인에 소구하고 있습니다. 연속 잉크젯으로 인한 잉크젯 인쇄 시장 규모는 2031년까지 336억 달러 이상에 달할 것으로 예상되며, 많은 컨버터에게 속도가 품질과 동등한 중요성을 갖고 있음을 보여줍니다. DoD 벤더는 이에 대응해, 재순환 헤드와 AI 지원형 액적 제어를 통합하는 것으로, 1,200 dpi의 해상도를 손상시키지 않고 80 m/min을 넘는 속도를 실현하고 있습니다.

투자 판단은 SKU의 복잡성과 다운타임 허용도를 중심으로 전개하는 경향이 강해지고 있습니다. 매일 수백 개의 배치 코드를 관리하는 식품 및 음료 라인은 연속식 기술로 이행하는 한편, 장식 인쇄나 사진 인쇄 분야에서는 그레이 스케일 변조의 우위성으로 드롭 온 디맨드가 여전히 주류입니다. 드롭 온 디맨드 프리코트와 연속 바니시 층을 융합한 하이브리드 구조는 잉크젯 인쇄 시장의 향후 수렴 경로를 보여줍니다.

수성 잉크는 2025년 34.22%의 점유율을 차지했으며, 낮은 VOC 특성과 광범위한 종이 대응성이 평가되었습니다. 규제 강화가 채용을 가속하는 한편, 수성 캐리어와 폴리머 입자를 조합한 라텍스 잉크의 옥외 내구성도 주목을 받고 있습니다. 라텍스 잉크가 예상되는 CAGR 10.78%는 2031년까지 잉크젯 인쇄 시장 점유율을 약 1/4로 늘릴 수 있습니다. 대용량 벌크 탱크와 무취 운전을 실현한 라텍스 잉크는 기존 용제 잉크가 담당해 온 점포내 사인이나 장식 분야에서의 채용이 진행되고 있습니다.

용제계 잉크는 극도의 밀착성이나 내약품성이 요구되는 분야에서는 여전히 사용되고 있지만, 자동차 부품의 고정구조차도 UV-LED나 라텍스 잉크의 대체품이 시험 도입되고 있습니다. Mimaki의 CMR 프리 UV 잉크와 HP의 Latex R 시리즈는 내구성을 손상시키지 않고 지속가능성에 초점을 맞춘 R&D 사이클이 가속되고 있음을 보여줍니다. 규제 당국이 기준을 엄격하게 하고 있는 동안, 잉크젯 인쇄 업계는 컴플라이언스를 개척 대책이 아니라 가치 제안에 통합하는 화학 기술로 중심을 옮기고 있습니다.

잉크젯 인쇄 시장 보고서는 인쇄 기술(드롭 온 디맨드, 연속 잉크젯 등), 잉크 유형(수성, 용제, UV 경화형 등), 구성 부품(프린터, 잉크 카트리지, 벌크 잉크 등), 용도(도서 및 출판, 광고 등), 기재(종이 및 판지, 플라스틱 필름 및 포일 등), 지역(북미 등)으로 분석했습니다. 시장 예측은 금액 기준(달러)으로 제시됩니다.

아시아태평양의 우위성은 양산 지향 중국 컨버터와 고정밀 일본 헤드 제조업체와 비교할 수 없는 시너지 효과를 반영합니다. 광동성에서 타밀 나두에 이르는 섬유산업 거점에서는 자동화 및 AI 대응 인쇄기에 대한 투자가 확대되어 지역의 주도적 입장을 강화하고 있습니다. 한국은 전자기기 산업의 에코시스템을 활용하여 OLED 및 PCB 제조용 기능성 잉크젯 라인의 시험 도입을 진행하고 잉크젯 인쇄 시장을 지원하는 기술 기반을 확충하고 있습니다.

남미의 성장 가속은 정책 주도의 현지화에 의존합니다. 이로 인해 컨버터는 수입 관세로부터 보호되는 동시에 고용 창출이 촉진됩니다. 재정적 우대 조치는 특히 식품 포장 분야에서 중소 공장의 디지털 라인으로의 갱신을 지원합니다. 이 분야에서는 추적성과 단납기에 대한 수요가 잉크젯 기술과 일치하고 있습니다. 2024년 공급망 혼란은 국내 인쇄 능력의 전략적 가치를 부각시키고 2031년까지 설비 투자를 촉진할 것입니다.

북미와 서유럽에서는 연구 개발 클러스터와 엄격한 환경 기준을 통해 기술 발전 방향이 계속 형성되고 있습니다. 독일의 인쇄 잉크 규제와 REACH 규제의 확대는 낮은 VOC 화학 물질로의 급속한 전환을 촉진하고 사실상 세계 표준을 수립하고 있습니다. 중동 및 아프리카에서는 전자상거래의 확대에 의해 라벨이나 연포장 수요가 높아지고 있지만, 인프라의 부족이 규모 확대를 억제하고 있습니다. 그러나 걸프 국가의 파일럿 프로젝트는 음료 코딩을 위한 고속 싱글 패스 라인을 입증하여 잉크젯 인쇄 시장의 향후 성장을 시사하고 있습니다.

The inkjet printing market was valued at USD 117.77 billion in 2025 and estimated to grow from USD 126.42 billion in 2026 to reach USD 180.19 billion by 2031, at a CAGR of 7.34% during the forecast period (2026-2031).

Current momentum rests on three pillars: rising demand for data-rich packaging, the fashion sector's pivot to on-demand textile output, and regulatory pressure that favors water-based chemistries. Vendors are shifting from hardware-centric propositions toward connected, service-rich ecosystems that lower the total cost of ownership and support mass customization. Consolidation among printhead innovators, coupled with region-specific incentives for localized production, is reshaping competitive dynamics while opening white-space opportunities in direct-to-shape, functional electronics, and decor applications. The inkjet printing market continues to thrive by translating these structural forces into scalable, digitally enabled workflows that replace analog systems across packaging, publishing, textile, and industrial verticals.

Stringent traceability mandates and anti-counterfeiting initiatives are pushing brand owners toward real-time, variable data capabilities that only the inkjet printing market can scale efficiently. Graphic Packaging International's deployment of imprinting technology embeds batch-level serialization while maintaining line speeds, proving that high-resolution thermal inkjet can coexist with high-throughput environments. MapleJet's modular coding systems further illustrate how inline integration minimizes downtime and ensures regulatory compliance on recyclable films. Collaborations such as SUDPACK-LEIBINGER extend this approach to mono-material packaging, demonstrating how compliant inks combined with recyclable substrates future-proof operations under forthcoming EU targets. Across markets, the ability to embed QR codes and dynamic design elements is transforming packaging from a passive container to an interactive brand asset, locking in sustained demand for innovative inkjet platforms.

Average first-print runs continue to contract as publishers align inventory with volatile consumer demand. Nielsen BookScan data show double-digit drops in initial orders, prompting adoption of sheetfed and web inkjet devices that deliver offset-like economics at runs below 1,000 copies. Canon's new B2 device prints 8,700 sheets per hour, reducing breakeven points and enabling "gap" printing strategies that bridge supply during social-media-driven sales spikes. HP's digital production platforms reinforce this shift by automating job sequencing and finishing, trimming labor costs, and integrating cloud-based analytics. As publishers pivot to micro-batch replenishment and personalized editions, the inkjet printing market stands out as the only technology able to monetize these emerging workflows without inflating warehousing costs.

The ongoing transition of marketing budgets to programmatic platforms limits addressable volumes for commercial print. Agencies favor click-through metrics and real-time attribution, challenging print service providers that were once reliant on high-volume flyers and catalogs. In response, firms reposition toward high-impact direct mail and transpromo pieces that leverage data-driven personalization. By coupling unique QR codes with loyalty programs, printers preserve relevance and capture premium margins, yet overall volume shrinkage remains a drag on the inkjet printing market's legacy commercial segment.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Drop-on-Demand (DoD) platforms delivered 45.88% of 2025 revenue, underscoring their versatility across substrates and the high image fidelity clients require. Despite leadership, DoD growth decelerates as Continuous Inkjet's 9.10% CAGR appeals to packaging lines seeking uninterrupted, high-velocity coding. The inkjet printing market size attributable to Continuous Inkjet is projected to surpass USD 33.6 billion by 2031, indicating that speed now carries equal weight with quality for many converters. DoD vendors respond by integrating recirculation heads and AI-assisted droplet control to push speeds past 80 m/min without sacrificing 1,200 dpi resolution.

Investment decisions increasingly revolve around SKU complexity and downtime tolerance. Food and beverage lines that manage hundreds of batch codes daily gravitate toward Continuous technology, while decor and photographic segments remain DoD strongholds due to grayscale modulation advantages. Hybrid architectures that blend DoD pre-coats with Continuous varnish layers illustrate the convergence path ahead for the inkjet printing market.

Aqueous formulations held 34.22% share in 2025, benefiting from low VOC profiles and broad paper compatibility. Regulatory headwinds expedite adoption, yet they also elevate Latex chemistries that combine water-based carriers with polymer particles to deliver exterior durability. Latex's 10.78% CAGR could lift its slice of the inkjet printing market to nearly one-quarter by 2031. High-capacity bulk tanks and odor-free operation position Latex for in-store signage and decor, segments historically served by solvent inks.

Solvent-based lines persist where extreme adhesion or chemical resistance prevails, but even automotive fixtures now pilot UV-LED and Latex alternatives. Mimaki's CMR-free UV inks and HP's Latex R-series underscore an accelerating R&D cycle focused on sustainability without durability trade-offs. As regulators harden thresholds, the inkjet printing industry is pivoting toward chemistries that embed compliance into their value proposition rather than treating it as a retrofit.

The Inkjet Printing Market Report is Segmented by Printing Technology (Drop-On-Demand, Continuous Inkjet, and More), Ink Type (Aqueous, Solvent, UV-Curable, and More), Component (Printers, Ink Cartridges and Bulk Inks, and More), Application (Books and Publishing, Advertising, and More), Substrate (Paper and Paperboard, Plastic Films and Foils, and More), and Geography (North America, and More). Market Forecasts in Value (USD).

Asia-Pacific's dominance reflects unparalleled synergy between volume-oriented Chinese converters and high-precision Japanese head manufacturers. Investments in automation and AI-enabled presses proliferate across textile hubs from Guangdong to Tamil Nadu, reinforcing regional leadership. South Korea leverages its electronics ecosystem to pilot functional inkjet lines for OLED and PCB fabrication, widening the technology pool that feeds the inkjet printing market.

South America's acceleration hinges on policy-driven localization that shields converters from import tariffs while fostering job creation. Fiscal incentives help smaller plants upgrade to digital lines, especially in food packaging, where demand for traceability and shorter lead times aligns with inkjet capabilities. Supply chain disruptions in 2024 illustrated the strategic value of domestic print capacity, spurring cap-ex through 2031.

North America and Western Europe continue to shape technological trajectories via R&D clusters and stringent environmental norms. The German Printing Ink Ordinance and REACH expansions catalyze rapid migration to low-VOC chemistries, setting de facto global benchmarks. In the Middle East and Africa, rising e-commerce elevates label and flexible-packaging demand, yet infrastructure gaps temper scale. Nonetheless, pilot projects in Gulf states demonstrate high-speed single-pass lines for beverage coding, hinting at future momentum in the inkjet printing market.