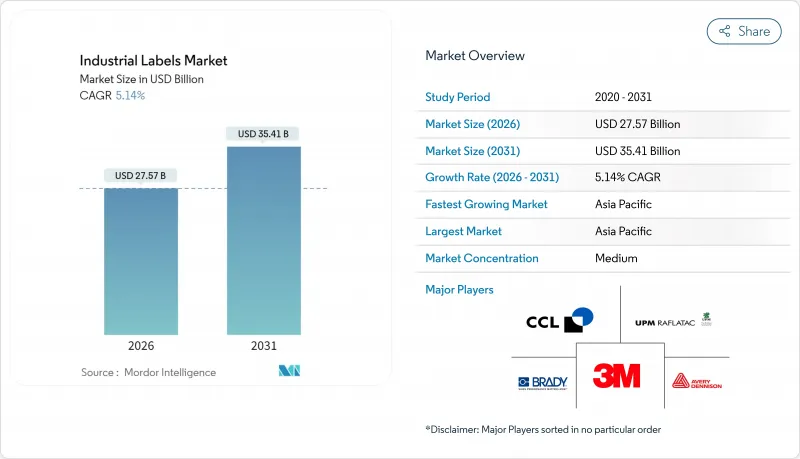

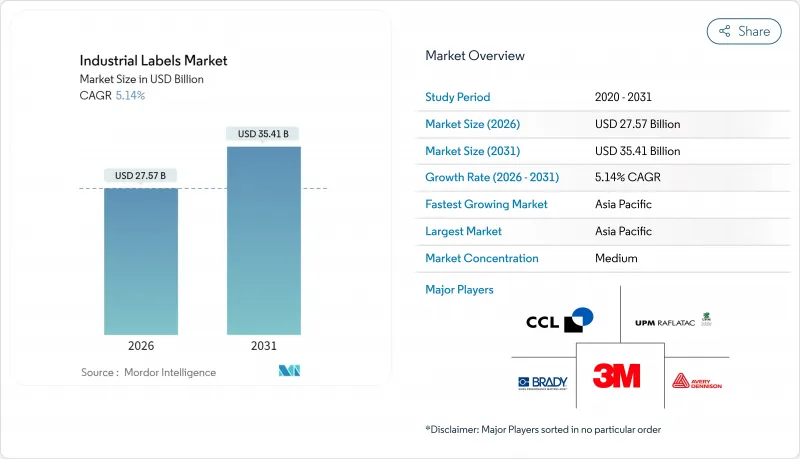

세계의 산업용 라벨 시장은 2025년 262억 2,000만 달러로 평가되었으며, 2026년 275억 7,000만 달러에서 2031년까지 354억 1,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중 (2026-2031년) CAGR은 5.14%로 전망되고 있습니다.

이러한 성장세는 규제 강화와 디지털 제조의 확대에 따라 신뢰할 수 있는 제품 식별, 추적성, 안전 정보 전달에 대한 지속적인 수요를 뒷받침하고 있습니다. 새로운 컴플라이언스 요건, 신속한 전자상거래 이행, 디지털 및 스마트 인쇄 기술의 채택 가속화는 컨버터, 원료 공급업체 및 장비 제조업체 전체에서 비용 구조와 경쟁 전략을 재구성합니다. 산업용 라벨 시장은 공장 자동화 및 물류 가시화에 대한 투자 증가의 이점을 얻고 있지만, 폴리머와 접착제의 가격 변동성과 엄격한 VOC 규제가 이익률에 대한 압박 요인으로 계속되고 있습니다. 전체적으로, 이 분야는 성숙한 최종 용도 수요와 신흥의 혁신 영역이 균형있게 혼합되어 있으며, 이들 전체가 향후 5년간 한 자릿수 중반의 성장을 지원할 전망입니다.

제조업자는 2026년 1월 시행이 다가오는 FDA 식품 추적 가능성 규칙에 대응하기 위해 2차원 코드와 직렬화된 추적 가능성 로트 코드를 기재 가능한 라벨의 도입이 시급합니다. 2028년에 설정된 새로운 식품 표시 규칙의 통일 준수 기한에 따라, 변화하는 데이터 항목에 대응 가능한 인쇄 시스템의 필요성이 높아지고 있습니다. 콜드체인 전체에서 판독성을 유지하는 내구성 및 내후성이 있는 기재에 대한 수요가 높아지고 있습니다. 2차원 바코드로의 전환으로 인해 프린터의 해상도 요구사항이 증가하고 있으며, RFID를 포함한 베이커리 라벨을 이용한 소매업의 초기 파일럿 사업은 컴플라이언스와 공급망 최적화의 교차점을 나타냅니다. 브랜드가 라인을 리노베이션하는 동안 산업용 라벨 시장에서 고사양의 식품 등급 제품이 급증하고 있습니다.

자동화 완성 센터에서는 ERP 시스템에서 생성되어 로봇 구동 창고를 이동하는 가변 데이터 라벨의 규모 확대가 진행되어 물류 라벨 시장은 CAGR 9.98%로 추이하고 있습니다. Walmart의 RFID 도입 확대 정책에 따라 업스트림 공급업체는 상품 단위로 인코딩된 인레이 임베딩을 의무화하고 있습니다. 실시간 위치 감지 기능이 있는 BLE 라벨의 보급은 AI를 활용한 재고 관리 알고리즘에 대응하기 위해 수동형 바코드에서 IoT 대응 태그로 전환이 진행되고 있음을 나타냅니다. 아시아태평양의 급성장 중인 크로스 보더 전자상거래는 기계 판독이 가능하고 오류 없는 식별을 가능하게 하는 산업용 라벨 시장 수요를 더욱 가속화하고 있습니다.

폴리비닐알코올 가격의 하락과 운임 할증의 교차 발생이 아시아태평양의 가공거점에서 이익 계획을 저해하고 있습니다. 접착제 원료나 실리콘 라이너가 석유 및 에너지 시장에 연동해 급격하게 변동하기 때문에 계약 재협상이 빈발하고 있습니다. 2024년 4분기 조달 보고서는 특수 코팅 공급 불안정을 지적하며, 가공업자는 운전자금을 압박하는 버퍼 재고를 보유해야 합니다. 이러한 요인이 결합되어 견조한 수요에도 불구하고 산업용 라벨 시장 전체의 확대는 약간 둔화되고 있습니다.

폴리머 라벨은 우수한 내약품성에 의해 2025년 시점에서 산업용 라벨 시장의 51.98%의 점유율을 유지했지만, 종이 기반 에코 기재는 CAGR 9.38%로 확대되어, 2031년까지 산업용 라벨 시장에서 점유율을 확대할 전망입니다. 자동차, 농약, 윤활유 용도에서는 여전히 내마모성으로 PP 및 PET 필름이 채용되고 있지만, 가혹한 환경용으로는 금속층과 폴리머층을 조합한 하이브리드 라미네이트가 이용되고 있습니다.

지속가능성에 대한 요청이 재료 교체를 빠르게 촉진하고 있습니다. 탄소 행동 종이 제품 라인과 대마 섬유 라벨 용지는 측정 가능한 환경 부하 저감을 실현하고 있습니다. 과일 폐기물이나 견과류 껍질을 원료로 한 종이 제품은 농업 제품을 재이용해, 고급 식품 브랜드에 지지되고 있습니다. 조기 도입 기업은 공업용 라벨 시장에서는 처음으로 '제조 공정 개시 시점까지의 배출량'을 견적서에 기재해 것으로 차별화를 도모하고 있습니다.

감압 접착 구조는 FMCG 및 제약 공장에서 신속하고 유연한 부착 라인의 강점을 배경으로 2025년에는 산업용 라벨 시장의 43.05%를 차지했습니다. 동시에 인몰드 및 열전사 라벨은 블로우 성형기와 사출 성형기가 1차 성형시 장식을 통합하는 움직임에 따라 8.78%의 연평균 복합 성장률(CAGR)을 나타냅니다.

라이너리스 기술은 생산성과 지속가능성 양면에서 효과를 발휘하여 롤당 라벨 매수를 80% 증가시키고 다운타임을 삭감합니다. OptiCut WashOff 라이너리스 라벨은 재활용 탱크에서 완전히 벗겨지므로 폐쇄 루프 PET 시스템의 실현에 기여합니다. 로봇 대응형 부착장치는 이러한 기구를 Industry 4.0 라인에 한층 더 통합해, 산업용 라벨 시장의 보급을 촉진합니다.

산업용 라벨 시장 보고서는 원재료(폴리머 및 플라스틱, 금속 등), 메커니즘(감압식, 접착제 도포식 등), 제품 유형(경고 및 보안, 자산 태그 등), 인쇄 기술(아날로그, 디지털, 하이브리드, 스크린), 식별 기술(바코드, RFID 등), 최종 사용 산업(식품 및 음료, 전자 기기 등), 지역별로 분류되어 있습니다. 시장 예측은 금액 기준(달러)으로 제시됩니다.

아시아태평양은 2025년에 산업용 라벨 시장의 38.10%를 차지했고, 전자기기, 자동차, 전자상거래 허브의 확대에 의해 2031년까지 연평균 복합 성장률(CAGR) 8.52%를 보일 것으로 예측됩니다. 중국과 인도가 생산능력 강화를 주도하는 한편, ASEAN 국가의 우대 정책이 인근 조달을 촉진하고 있습니다. 정부 주도 Industry 4.0 프로그램은 신규 그린필드 공장에서의 스마트 라벨 도입을 가속화하고, 이 지역이 세계의 산업용 라벨 시장 성장에 핵심적인 역할을 담당할 것을 확고히 하고 있습니다.

북미는 확립된 규제 체제와 대형 소매업의 의무화로부터 혜택을 받고 있습니다. Avery Dennison의 케레타로 RFID 공장은 멕시코가 미국 컨버터를 위한 저비용 공급 파트너로 부상하고 있음을 보여줍니다. 캐나다의 VOC 규제와 미국 공급망 보안에 중점을 두어 소비재 및 전략 산업에서의 라벨 수요는 견조하게 추진되어 지역 산업용 라벨 시장의 안정성을 강화하고 있습니다.

유럽에서는 엄격한 에코 디자인 지령과 폐기물 지령에 의해 성숙한 수요가 억제되고 있습니다. 브랜드 소유자가 유럽 그린딜의 목표에 부합하는 동안 재활용 가능한 라벨 기술 혁신이 조기에 도입되었습니다. 독일의 자동화 분야 리더십은 고기능 생산 설비를 지원하고, 한편 영국의 브렉시트 후의 규제 차이는 다국어 및 다포맷 대응 라벨 전략을 촉진하고 있습니다. 중동, 아프리카 및 남미의 신흥 클러스터는 성장 궤도에 변동을 보이지만, 개발 도상 산업용 라벨 시장에서 선구자 이익을 요구하는 컨버터에게 매력적인 시장으로 계속되고 있습니다.

The industrial labels market was valued at USD 26.22 billion in 2025 and estimated to grow from USD 27.57 billion in 2026 to reach USD 35.41 billion by 2031, at a CAGR of 5.14% during the forecast period (2026-2031).

This growth momentum underscores sustained demand for reliable product identification, traceability, and safety communication as regulations tighten and digital manufacturing expands. New compliance mandates, rapid e-commerce fulfillment, and accelerating adoption of digital and smart printing technologies are reshaping cost structures and competitive strategies across converters, raw-material suppliers, and equipment manufacturers. The industrial labels market benefits from rising investment in factory automation and logistics visibility, yet pricing volatility for polymers and adhesives and stricter VOC limits continue to pressure margins. Overall, the sector demonstrates a balanced mix of mature end-use demand and emerging innovation pockets that collectively support mid-single-digit growth over the next five years.

Manufacturers face imminent January 2026 enforcement of the FDA Food Traceability Rule, forcing adoption of labels capable of carrying 2D codes and serialized Traceability Lot Codes.Uniform compliance dates set for new food labeling rules in 2028 heighten the need for print systems that flex with evolving data fields. Demand is rising for durable, weather-resistant substrates that stay legible across cold chains. The push toward 2D barcodes is increasing printer resolution requirements, and early retail pilots with RFID-embedded bakery labels illustrate how compliance intersects with supply-chain optimization. As brands retrofit lines, the industrial labels market records a surge in high-specification food-grade products.

Automated fulfillment centers are scaling variable-data labels that originate in ERP systems and travel through robotics-driven warehouses, aligning with a 9.98% CAGR in logistics labeling. Walmart's expanded RFID directive compels upstream suppliers to embed encoded inlays at item level. Real-time location sensing printed BLE labels show how IoT-ready tags are replacing passive barcodes to meet AI-powered inventory algorithms. APAC's booming cross-border e-commerce further accelerates industrial labels market demand for machine-readable, error-free identification.

Downward swings in polyvinyl alcohol costs, interspersed with freight surcharges, hamper profit planning in Asia-Pacific converting hubs. Contract renegotiations become frequent as adhesive feedstocks and silicone liners move sharply with oil and energy markets. Q4 2024 sourcing reports flag erratic availability of specialty coatings, prompting converters to hold buffer inventories that erode working capital. Combined, these shocks slightly temper overall industrial labels market expansion despite healthy demand.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Polymer labels retained 51.98% industrial labels market share in 2025 due to superior chemical resistance, yet paper-based eco substrates are set to outpace with a 9.38% CAGR, lifting their slice of industrial labels market size through 2031. Automotive, agrochemical, and lubricants applications still rely on PP and PET films for abrasion resistance, while hybrid laminates combine metal and polymer layers for extreme environments.

Sustainability imperatives are catalyzing rapid material substitution. Carbon-action paper lines and hemp-fiber label stocks demonstrate measurable footprint reductions. Fruit-waste and nut-shell papers repurpose agricultural by-products, appealing to premium food brands. Early adopters differentiate by reporting cradle-to-gate emissions in quotations, a first in the industrial labels market.

Pressure-sensitive constructions led with 43.05% industrial labels market share in 2025 on the strength of fast, flexible application lines across FMCG and pharma plants. Concurrently, in-mold and heat-transfer labels present an 8.78% CAGR as blow-molders and injection molders integrate decoration into primary forming.

Linerless technology illustrates dual gains in productivity and sustainability, providing 80% more labels per roll and reducing downtime. OptiCut WashOff linerless labels detach cleanly in recycling baths, aiding closed-loop PET systems. Robotics-ready applicators further integrate these mechanisms into Industry 4.0 lines, enhancing industrial labels market adoption.

The Industrial Labels Market Report is Segmented by Raw Material (Polymer/Plastic, Metal, and More), Mechanism (Pressure-Sensitive, Glue-Applied, and More), Product Type (Warning/Security, Asset Tags, and More), Printing Technology (Analog, Digital, Hybrid, Screen), Identification Technology (Barcode, RFID, and More), End-User Industry (Food/Beverage, Electronics, and More), and Geography. Market Forecasts in Value (USD).

Asia-Pacific dominated with 38.10% industrial labels market share in 2025 and is projected to compound at 8.52% through 2031 thanks to expanding electronics, automotive, and e-commerce hubs. China and India spearhead capacity additions, while ASEAN incentives attract near-shoring. Government Industry 4.0 programs accelerate smart-label adoption inside new greenfield plants, cementing the region's pivotal role in global industrial labels market growth.

North America benefits from entrenched regulatory frameworks and big-box retail mandates. Avery Dennison's Queretaro RFID plant underscores Mexico's ascent as a low-cost supply partner for U.S. converters Averydennison. Canadian VOC controls and the U.S. emphasis on supply-chain security keep label demand resilient across consumer and strategic industries, reinforcing regional industrial labels market stability.

Europe exhibits mature demand moderated by strict eco-design and waste directives. Recyclable label innovations enjoy early adoption as brand owners align with European Green Deal goals. Germany's automation leadership sustains high-spec production tools, while UK regulatory divergence post-Brexit prompts multi-language, multi-format label strategies. Emerging clusters in the Middle East & Africa and South America show variable trajectories but remain attractive for converters seeking first-mover gains in developing industrial labels markets.