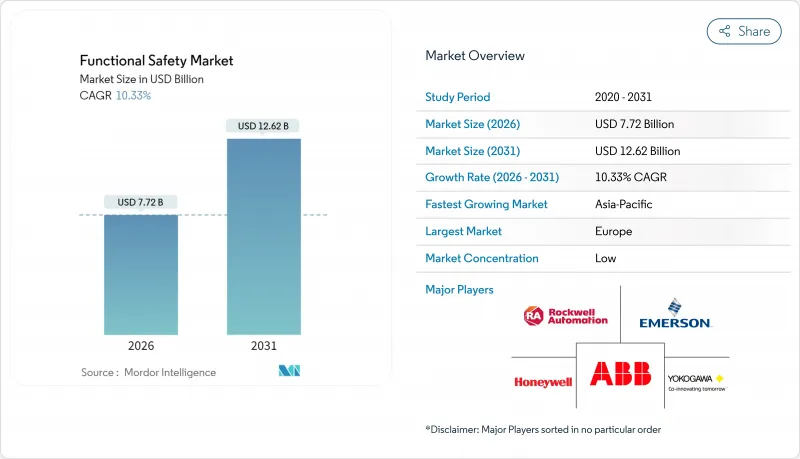

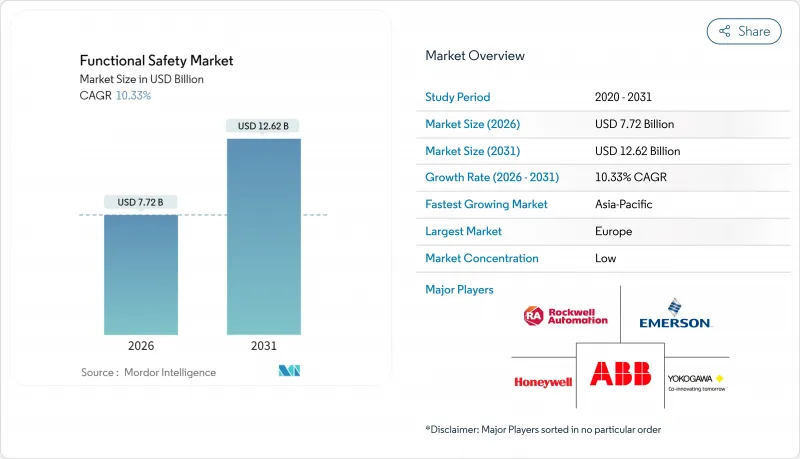

세계의 기능 안전 시장 규모는 2026년 77억 2,000만 달러로 추정되며, 2025년 70억 달러에서 성장할 전망입니다. 2031년에는 126억 2,000만 달러에 이르고, 2026년부터 2031년까지 CAGR 10.33%로 확대될 전망입니다.

견고한 수요는 보다 엄격한 세계 표준과 Industry 4.0의 도입이 교차하는 현상에 기인하고 있으며, 제조업체는 설계 단계부터 안전 기능을 핵심 자동화 플랫폼에 통합하는 것을 강요하고 있습니다. 석유, 가스 및 전력시설에서 사고 조사 후 규제 강화도 도입을 촉진하고 급속한 디지털화는 하드와이어드 릴레이보다 프로그램 가능한 안전 로직을 선호하는 이용 사례를 낳고 있습니다. 각 공급업체는 기능 안전과 기업 사이버 보안의 통합 요구사항에서도 혜택을 누리고 있습니다. 이 동향은 공정 안전과 사이버 레지리언스를 동일 분야의 두 가지 측면으로 취급하는 ISA/IEC 62443 가이드라인에 의해 강화되고 있습니다. 그 결과, SIL 준수 및 사이버 보안 설계를 단일 솔루션으로 검증할 수 있는 공급자가 명확한 경쟁 우위를 획득하고 있습니다.

IEC 61508은 현재 업계를 가로지르는 제품 승인의 기반이 되고 있으며, 2024년 ISO 26262 개정판에서는 AI와 머신러닝에 대한 명확한 지침이 추가되어 설계 단계에서의 안전성 통합이 의무화되고 있습니다. 따라서 세계 시장 진출을 목표로 하는 제조업체는 SIL 인증 구성요소와 시스템 레벨 검증을 필요로 하므로 인증 시험 기관에 대한 예측 가능한 수요가 지속됩니다. 동시에 EU 기계 지침, OSHA 지침 및 일본과 중국의 동등한 규정에 따라 시행의 엄격화가 진행되고 있습니다. 이와 더불어, 비준수에 대한 벌칙의 강화도 함께, 이러한 틀은 기업에게 감사의 간소화와 플랜트 승인의 신속화를 도모하기 위해 독립형 릴레이로부터 통합형으로 인증받은 안전 컨트롤러로의 교체를 촉구하고 있습니다.

디지털 변환이 운영 데이터를 클라우드화하는 동안 안전 기능은 이더넷 기반 네트워크와 네이티브와 연동하면서 확정적인 응답 시간을 유지해야 합니다. 스마트 팩토리에서는 디지털 트윈을 활용한 예지 보전이 이루어지며, AI 해석에 의해 SIL 목표를 위협하기 전에 센서 드리프트를 검지합니다. 이러한 이용 사례에서는 다중 프로토콜에 대응하고 진단 기능을 MES나 ERP층으로 밀어 올리는 프로그램 가능한 로직이 유리합니다. 따라서 인증 상태를 유지하면서 원격으로 패치를 적용할 수 있는 유연한 안전 PLC 및 소프트웨어 프레임워크에 대한 수요가 증가하고 있습니다.

SIL 3 인증을 취득하려면 엄격한 제3자 시험과 문서화가 요구되므로 프로젝트 총 예산의 15-25%가 추가 비용으로 발생합니다. 많은 중소기업들은 업그레이드를 연기하거나 낮은 SIL 목표를 선택하기 때문에 경공업과 개별 생산 분야에서의 보급이 늦어지고 있습니다. 구독 모델은 도움이 되지만, 자본 집약도는 여전히 단기 성장의 주요 억제요인이며, 특히 현지 규제가 아직 성숙 단계에 있는 지역에서는 두드러집니다.

안전 센서의 수익은 물리적 위험과 제어 시스템을 연결하는 주요 역할을 반영하여 2025년 기능 안전 시장 규모에서 최대 27.62%를 차지했습니다. 광학 해상도와 자체 진단 기능의 지속적인 개선으로 센서의 신뢰성이 향상되었으며 제조업체는 증명 테스트 간격을 연장하고 다운타임을 줄일 수 있습니다. 비접촉 감지가 오염 위험을 최소화하는 청정실 및 식품 등급 환경에서의 채택도 증가하고 있습니다.

프로그램 가능 안전 시스템에 대한 수요는 2031년까지 연평균 복합 성장률(CAGR) 11.05%로 예측되어 디바이스 카테고리에서 가장 높은 성장률을 나타냅니다. Industry 4.0의 보급에 따라, 유저는 빈번한 제품 전환에 대응 가능한 소프트웨어 설정형 로직을 선호하고 채용하고 있어, 이것에 의해 제어반의 배선 변경이 불필요하게 됩니다. OMRON의 'Sysmac Studio'와 같은 플랫폼은 프로그래밍 시간을 90% 줄이고 인증 엔지니어 부족이라는 병목 현상을 해결하는 데 기여하고 있습니다. 최종 제어 장비(밸브, 액추에이터, 드라이브)도 기세를 늘리고 있습니다. 공정 산업에서는 노후화된 기계식 거버너를 상태 모니터링을 지원하는 SIL 인증 디지털 기기로 대체하고 있기 때문입니다. 예측 기간 동안 검증을 효율화하는 통합형 센서 컨트롤러 패키지는 개별 부품에서 번들 솔루션으로의 지출 시프트가 진행되어 플랫폼 공급자에 대한 동향이 강화될 전망입니다.

긴급정지(ESD) 시스템은 공정 이상시 신속한 차단을 필요로 하는 석유, 가스, 화학 플랜트를 기반으로 2025년 기능 안전 시장 점유율의 23.55%를 차지했습니다. 시장 밀도는 고가치 자산과 엄격한 표준으로 다층 보호가 요구되는 해양 플랫폼 및 LNG 플랜트에서 가장 높습니다. 각 공급업체는 더 적은 I/O 지점에서 SIL 3을 달성하고 수명 주기 비용을 줄이기 위해 진단 기능과 투표 아키텍처를 지속적으로 강화하고 있습니다.

고신뢰성 압력보호시스템(HIPPS)은 심해 프로젝트에서 대형 플레어 스택의 회피와 배출량 감축을 목적으로 채용이 진행되어 10.95%의 연평균 복합 성장률(CAGR)로 성장이 전망되고 있습니다. 북해 자산 도입 성공으로 2,500만 달러의 설비투자(CAPEX) 삭감을 실현하여 견조한 투자이익률(ROI) 사례를 창출하였습니다. 버너 관리 및 터보 기계 제어는 전력 및 정제 분야에서 안정적인 수요를 유지합니다. 한편, 화재 및 가스 감지 시스템은 화염, 유독 가스, 열 감지를 단일 분석 대시보드에 통합하는 풀 커버리지 모델을 의무화하는 규제에 의해 수요가 밀려오고 있습니다.

유럽은 2025년 시점에서 기능 안전 시장 점유율 28.40%를 유지해 선두를 견지했습니다. EU 기계 지령과 독일, 이탈리아 및 북유럽 국가에서 고도 자동화 보급이 기반이 되고 있습니다. 신재생에너지 및 해상풍력 분야에서 도입이 가속되고 있으며, 고가치 자산과 원격지 특성으로부터 원격 진단 기능을 갖춘 SIL 3 준거 셧다운 장치가 요구되고 있습니다.

북미는 OSHA 주도의 노동자 안전 프로그램과 정제, 석유화학 및 제약분야의 광범위한 생산능력에 힘입어 작은 차이로 계속됩니다. 이 지역은 성숙한 IT-OT 통합 기술과 풍부한 인증 기술자를 배경으로 안전과 사이버 보안의 융합을 선도하고 있습니다. 반도체 공장을 위한 연방정부의 자극책은 IEC 61508과 ISA/IEC 62443의 두 요건을 충족하는 프로그래머블 안전 플랫폼의 신규 도입을 촉진하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 11.25%라는 가장 빠른 성장이 예상됩니다. 중국의 지속적인 제조업 고도화와 일본의 정밀 로봇 투자가 함께, 프로그래머블 안전 PLC나 스마트 라이트 커튼의 대량 구입을 촉진하고 있습니다. 동남아시아 국가에서는 엄청난 설비투자 없이 증가하는 직장안전에 대한 기대에 부응하기 위해 구독형 안전서비스를 채용하고 있습니다. 반면에 인도의 새로운 화학 공정 안전 지침을 통해 새로운 플랜트는 처음부터 SIL 2 이상의 사양 수준에서 설계됩니다. 중동 및 아프리카에서는 사우디아라비아, 카타르, UAE의 NOC(국영 석유회사) 및 IOC(국제 석유회사) 프로젝트가 신규 LNG 및 수소 시설에서 HIPPS(고신뢰성 프로세스 제어 시스템)와 고급 화재 및 가스 감지 시스템의 표준화를 추진해 점증적인 성장을 가져오고 있습니다.

Functional Safety market size in 2026 is estimated at USD 7.72 billion, growing from 2025 value of USD 7.00 billion with 2031 projections showing USD 12.62 billion, growing at 10.33% CAGR over 2026-2031.

Solid demand arises from the way stricter global standards now intersect with Industry 4.0 roll-outs, forcing manufacturers to embed safety functions into core automation platforms from the concept stage. Heightened regulatory enforcement following incident investigations in oil, gas, and power facilities further boosts adoption, while rapid digitalization creates use cases that favor programmable safety logic over hard-wired relays. Vendors also benefit from the need to merge functional safety with enterprise cybersecurity, a trend reinforced by ISA/IEC 62443 guidelines that treat process safety and cyber resilience as two halves of the same discipline. As a result, solution providers that can validate SIL compliance and cyber-secure design in one offering win a clear competitive edge.

IEC 61508 now anchors product approvals across sectors, and the 2024 ISO 26262 update adds explicit AI and machine-learning guidance, forcing design-stage safety integration. Manufacturers seeking global market entry therefore require SIL-rated components and system-level validation, which sustains predictable demand for accredited testing laboratories. At the same time, the EU Machinery Directive, OSHA directives, and comparable rules in Japan and China have raised enforcement intensity. Coupled with rising penalties for non-compliance, these frameworks motivate enterprises to replace standalone relays with integrated, certificate-backed safety controllers to simplify audits and speed plant approvals.

Digital transformation places operational data in the cloud, so safety functions must now talk natively to Ethernet-based networks while maintaining deterministic response times. Smart factories use digital twins for predictive shutdowns, and AI analytics spot sensor drift before it threatens SIL targets. Such use cases favor programmable logic that can accept multiple protocols and push diagnostics upstream to MES and ERP layers. Demand therefore tilts toward flexible safety PLCs and software frameworks that can be patched remotely without losing certification status.

Obtaining SIL 3 certification can add 15-25% to total project budgets because of rigorous third-party testing and documentation. Many SMEs defer upgrades or select lower SIL targets, slowing penetration in light industry and discrete manufacturing. While subscription models help, capital intensity remains the leading brake on near-term growth, especially where local enforcement is still maturing.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Revenue from safety sensors accounted for the largest 27.62% share of the functional safety market size in 2025, reflecting their role as the primary link between physical hazards and control systems. Continuous improvements in optical resolution and self-diagnostics increase sensor reliability, letting manufacturers raise proof-test intervals and cut downtime. Adoption also rises in clean-room and food-grade environments where non-contact sensing minimizes contamination risk.

Demand for programmable safety systems is forecast to post an 11.05% CAGR through 2031, the fastest rate among device categories. As Industry 4.0 spreads, users favor software-configurable logic that can adapt to frequent product changeovers without rewiring cabinets. Platforms such as Omron's Sysmac Studio cut programming time by 90%, easing the certified-engineer bottleneck. Final control elements, valves, actuators, and drives, also gain momentum because process industries are replacing aging mechanical governors with SIL-rated digital devices that support condition monitoring. Over the forecast horizon, integrated sensor-controller packages that streamline validation are likely to shift spend away from discrete components toward bundled solutions, reinforcing the trend toward platform providers.

Emergency shutdown (ESD) systems represented 23.55% of the functional safety market share in 2025, anchored in oil, gas, and chemical operations that need rapid isolation during process upsets. Market density is highest on offshore platforms and LNG trains where high-value assets and stricter codes compel multi-layered protection. Vendors continue to enhance diagnostics and voting architectures to meet SIL 3 with fewer I/O points, lowering lifecycle cost.

High-integrity pressure protection systems (HIPPS) are projected to grow at a 10.95% CAGR as deep-water projects adopt them to avoid oversized flare stacks and reduce emissions. Successful deployments on North Sea assets delivered USD 25 million in CAPEX savings, creating a robust ROI case. Burner management and turbomachinery controls maintain steady demand in power and refining, while fire-and-gas systems receive a boost from regulations mandating full coverage models that integrate flame, toxic gas, and heat detection into one analytics dashboard.

The Functional Safety Market Report is Segmented by Device Type (Safety Sensors, Safety Controllers/Modules/Relays, and More), Safety Systems (BMS, TMC, HIPPS, and More), Services (TIC, Design/Engineering/Maintenance, and More), End-User Industry (Oil and Gas, Power Generation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe retained the lead with 28.40% functional safety market share in 2025, underpinned by the EU Machinery Directive and widespread use of advanced automation in Germany, Italy, and the Nordic states. Adoption intensifies in renewable energy and offshore wind, where high-value assets and remote locations demand SIL 3-compliant shutdown devices capable of remote diagnostics.

North America follows closely, supported by OSHA-driven worker-safety programs and extensive refining, petrochemical, and pharmaceutical capacity. The region also pioneers safety-cybersecurity convergence, helped by mature IT-OT integration skills and a deep bench of certified engineers. Federal stimulus for semiconductor fabs reinforces new installations of programmable safety platforms that meet both IEC 61508 and ISA/IEC 62443 requirements.

Asia-Pacific is poised for the fastest 11.25% CAGR to 2031. China's ongoing manufacturing upgrade, alongside Japan's precision robotics investments, spurs heavy purchases of programmable safety PLCs and smart light curtains. Southeast Asian nations adopt subscription-based safety services to meet rising workplace safety expectations without heavy CAPEX, while India's new chemical-process safety guidelines bring green-field plants straight to SIL 2-plus specification levels. Middle East and Africa contribute incremental gains as NOC and IOC projects in Saudi Arabia, Qatar, and the UAE standardize HIPPS and advanced fire-and-gas detection on green-field LNG and hydrogen facilities.