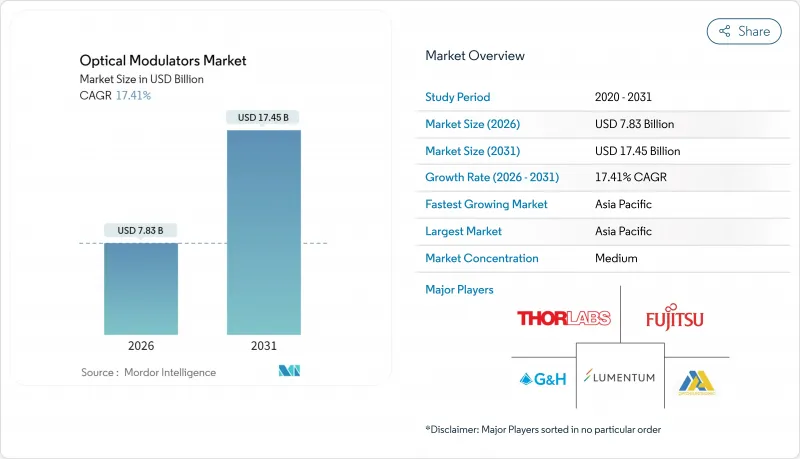

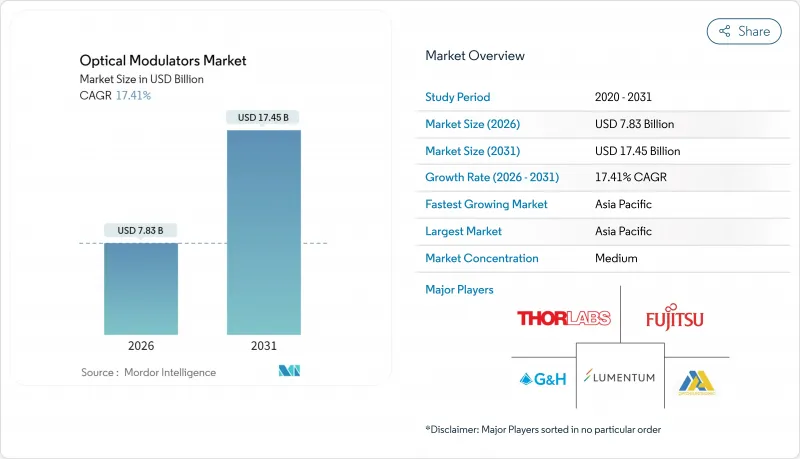

세계의 광변조기 시장은 2025년 66억 7,000만 달러에서 2026년까지 78억 3,000만 달러로 성장하고, 2026년부터 2031년까지 CAGR 17.41%로 성장을 지속하여 174억 5,000만 달러에 달할 것으로 예측됩니다.

이 성장 궤적은 800G 및 1.6T 광통신, 하이퍼스케일 데이터센터 배포, 초기 단계 양자 컴퓨팅 네트워크 등 모두 고속화를 계속하는 전기 광학 부품에 의존하는 분야에서 대역폭 수요의 가속을 반영합니다. 각 공급업체는 코패키지드 광학 부품의 열 설계 요구 사항을 충족하므로 위상 안정성과 낮은 구동 전압 설계를 선호합니다. 한편, 박막 니오브산리튬이나 실리콘 포토닉스에서의 재료 혁신이 비용 구조를 변혁중입니다. 스위치 ASIC 벤더가 100 기가보드 이상을 지원하는 광 엔진을 요구하는 동안 집적 변조기 칩은 틈새 시장에서 주류로 전환하고 있습니다. 한편 신흥 경제국의 정책 입안자는 5G 백홀 및 FTTH(Fiber-to-the-Home)에 주파수 대역과 보조금을 지속적으로 할당하고 있으며, 50-100Gbps 클래스의 대규모 도입이 지속되고 있습니다.

클라우드 공급자가 비트 단가를 줄이기 위해 2024년에는 800G 트랜시버 출하량이 2,000만 대를 돌파했습니다. 400G에서 800G로의 전환과 Ciena의 224G SerDes를 이용한 1.6T 코히런트 라이트 실증 등 초기 1.6T 기술 실증은 모듈레이터가 전력 예산을 파괴하지 않고 100G 보드의 심볼 레이트를 달성할 것을 요구하고 있습니다. 선형 플러그 가능 광 모듈 시장 규모는 2024년 50억 달러에서 2026년까지 100억 달러 이상으로 두 배로 늘어나 컴팩트하고 낮은 Vπ 아키텍처에 대한 단기적인 수요를 가속화하고 있습니다. 코패키지드 광 모듈 내부의 열 설계 마진은 축소 경향이 있어, 동일 기판상에서 드라이버 IC와 변조기의 도파로를 공동 최적화할 수 있는 통합 공급자가 우위성을 발휘합니다. 스위치 ASIC의 로드맵이 51T 및 102T 패브릭을 확정함에 따라 광 엔진의 탑재율이 가속되어 단기 CAGR에 대한 드라이버의 호영향이 더욱 강해집니다.

인도에서는 5G 서비스 개시 후 월간 광섬유 부설량이 101,550km로 급증해 5G 도입 전의 6배에 달했습니다. 이것은 기지국의 70% 광섬유화라는 정책 목표가, 실제의 광부품 수요에 직결하는 실례입니다. 각 스몰셀에는 최소 1개의 25G 또는 50G 광 프론트 홀 링크가 필요하므로 비용 및 내열성에 최적화된 변조기는 대량 주문이 예상됩니다. 중국의 클라우드 사업자는 2024년에 20-30억 달러 규모의 국내 트랜시버 시장을 창출해, 변조기 제조 공장에 파급하는 지역 조달 사이클을 강화했습니다. 광범위한 환경 조건 하에서 기기 인증을 받을 수 있는 공급업체는 공공 통신 입찰에서 우선 공급업체의 지위를 획득하여 중기 성장 전망을 높이고 있습니다.

심볼 레이트를 100G 보드 이상으로 밀어 올리는 것은 열 부하를 증가시키고 마이크로파 신호와 광 신호의 속도 매칭에 어려움을 줍니다. MIT 링컨 연구소의 인덕턴스 조정 전극은 50옴의 임피던스를 유지하면서 100GHz 이상의 대역폭을 제공하지만, 이러한 혁신 기술을 양산 가능한 모듈에 통합하는 것은 여전히 어렵습니다. 특수기판과 액체금속 서멀 비아는 부품 비용을 끌어올려 인증주기를 장기화시켜 단기적인 공급 다양성을 제한하고 CAGR을 억제하는 요인이 됩니다.

위상 변조기는 코히런트 검출의 기반 기술로서 2025년 광변조기 시장 점유율의 37.65%를 차지했습니다. 그러나 집적 모듈레이터 칩은 18.05%라는 가장 높은 CAGR로 추이할 전망입니다. 이는 코패키지드 광학 소자가 단일 기판 설계에 의존하고 전력 및 지연을 줄이기 때문입니다. 타워 세미컨덕터와 같은 파운드리가 레인당 400G 단위를 인증함에 따라 집적 칩과 관련된 광변조기 시장 규모가 확대되고 있습니다.

확립된 진폭 및 편광 디바이스는 직접 검출 및 감지 용도에서 계속 활용됩니다. 아날로그 변조기는 속도보다 선형성을 강조하는 틈새 무선 광전송(ROF) 영역에서의 위치를 유지합니다. 웨이퍼 레벨 테스트로의 전환은 평균 판매 가격(ASP)의 하락을 촉구하고, 포토닉 일렉트로닉스의 공동 설계를 습득한 신규 참가자를 초대하고 있습니다.

우수한 전기 광학 계수와 온도 안정성으로 인해 니오브산리튬은 43.55%의 점유율을 유지하고 있습니다. 그러나 CMOS 팹에 의한 대량 생산 및 저비용화가 실현된 실리콘 포토닉스는 18.25%의 연평균 복합 성장률(CAGR)로 급성장 중입니다. 대규모 클라우드 구매자가 엔드 투 엔드 단일 공급업체 포토닉 IC를 요구하는 동안 실리콘 포토닉스로 인한 광변조기 시장 규모가 확대되고 있습니다. 집적 레이저가 필수적인 분야에서는 인화인듐이 비계를 유지하고, 전기광학 폴리머는 100GHz를 넘는 마이크로파 포토닉스에 대응하고 있지만, 신뢰성의 과제는 여전히 남아 있습니다.

2025년 시점에서 아시아태평양은 광변조기 시장 점유율의 38.35%를 차지했습니다. 이것은 중국의 수직 통합 트랜시버 에코시스템과 인도의 기지국의 광섬유화 추진이 견인하고 있습니다. 지역 제조거점의 두께는 부품 비용(BOM)을 줄이고 5G 및 FTTH 네트워크에 신속하게 배치할 수 있습니다. 정부 보조금 프로그램과 현지 조달 의무가 생산 기반을 더욱 강화하고 있습니다. 북미에서는 성숙한 시장이면서 혁신 주도 수요를 볼 수 있어 하이퍼스케일 사업자나 방위 주요 기업이 최첨단의 박막 LiNbO3 및 실리콘 포토닉스를 채용해, AI 패브릭이나 양자 연구를 지지하고 있습니다. 유럽에서는 메트로 네트워크의 꾸준한 업그레이드가 계속되고 있는 한편, 자동차용 LiDAR나 산업용 센싱이 아날로그 및 편광 변조기의 인접 시장을 개척하고 있습니다. 이러한 성숙 지역의 광변조기 시장 규모는 기술 갱신에 의해 확대되고, 신흥 경제권의 수량 주도형 확대와는 대조적입니다.

The optical modulators market is expected to grow from USD 6.67 billion in 2025 to USD 7.83 billion in 2026 and is forecast to reach USD 17.45 billion by 2031 at 17.41% CAGR over 2026-2031.

This trajectory reflects accelerating bandwidth demand from 800 G and 1.6 T optics, hyperscale data-center rollouts, and early quantum-computing networks that all rely on ever-faster electro-optic components. Vendors are prioritizing phase-stable, low-drive-voltage designs to meet thermal budgets inside co-packaged optics, while material innovation in thin-film lithium niobate and silicon photonics is reshaping cost structures. Integrated modulator chips are moving from niche to mainstream as switch ASIC vendors mandate optical engines optimized for 100 Gbaud and above. Meanwhile, policymakers in emerging economies keep allocating spectrum and subsidies for 5G backhaul and fiber-to-the-home, sustaining large-volume deployments in the 50-100 Gbps class.

Record AI cluster build-outs lifted 800 G transceiver shipments past 20 million units in 2024 as cloud providers chased lower cost-per-bit metrics. The pivot from 400 G to 800 G, and early 1.6 T proof-points such as Ciena's 1.6 T coherent-lite demo using 224 G SerDes, compel modulators to hit 100 Gbaud symbol rates without breaking power budgets. Linear pluggable optics are doubling from USD 5 billion in 2024 to more than USD 10 billion by 2026, amplifying short-term demand for compact, low-Vπ architectures. Thermal design margins tighten inside co-packaged optics, rewarding integrated suppliers that can co-optimize driver ICs and modulator waveguides on the same substrate. As switch ASIC roadmaps lock in 51 T and 102 T fabrics, optical-engine attach rates accelerate, reinforcing the driver's positive impact on near-term CAGR.

India's monthly fiber deployment spiked to 101,550 km after 5G launch, six times the pre-5G run-rate, underlining how policy targets such as 70% tower fiberization translate into real optical component pull-through. Each small cell needs at least one 25 G or 50 G optical fronthaul link, so modulators tuned for cost and temperature resilience see large-volume orders. Chinese cloud operators generated a USD 2-3 billion domestic transceiver market in 2024, reinforcing regional procurement cycles that ripple through modulator fabs. Vendors able to qualify devices under wide environmental ranges win preferred-supplier status in public-telecom tenders, elevating medium-term growth prospects.

Pushing symbol rates past 100 Gbaud inflates thermal load and challenges velocity matching between microwave and optical signals. MIT Lincoln Laboratory's inductance-tuned electrodes stretch bandwidth beyond 100 GHz while holding 50-ohm impedance, but packaging such innovations into manufacturable modules remains difficult. Exotic substrates and liquid-metal thermal vias raise BOM and lengthen qualification cycles, limiting short-term supply diversity and depressing CAGR.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Phase modulators owned 37.65% of the optical modulators market share in 2025 as they remain fundamental for coherent detection. Integrated modulator chips, however, will post the strongest 18.05% CAGR because co-packaged optics depends on single-substrate designs that trim power and latency. The optical modulators market size tied to integrated chips expands as foundries like Tower Semiconductor qualify 400 G-per-lane units.

Established amplitude and polarization devices continue serving direct-detection and sensing. Analog modulators keep niche radio-over-fiber footholds where linearity trumps speed. The shift toward wafer-level test drives ASP reduction, inviting new entrants that master photonic-electronic co-design.

Lithium niobate held a 43.55% share thanks to its superior electro-optic coefficient and temperature stability. Yet silicon photonics is accelerating at 18.25% CAGR because CMOS fabs unlock high-volume, low-cost runs. The optical modulators market size attributable to silicon photonics rises as large cloud buyers demand single-supplier photonic ICs end-to-end. Indium phosphide retains a foothold where integrated lasers are mandatory, while electro-optic polymers address >100 GHz microwave photonics, though reliability hurdles persist.

The Optical Modulators Market Report is Segmented by Product Type (Amplitude Modulators, Polarization Modulators, and More), Material Platform (Lithium Niobate, Indium Phosphide, and More), Data-Rate Class (Less Than or Equal To 25 Gbps, 25 - 50 Gbps, and More), Application (Optical Communication, Fiber-Optic Sensors, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific accounted for 38.35% of the optical modulators market share in 2025, fueled by China's vertically integrated transceiver ecosystem and India's sprint to fiberize towers. Regional manufacturing depth keeps BOM low, allowing rapid deployment across 5G and FTTH footprints. Government subsidy programs and local sourcing mandates further anchor production. North America shows mature but innovation-led demand, with hyperscale operators and defense primes adopting cutting-edge thin-film LiNbO3 and silicon photonics to support AI fabrics and quantum research. Europe maintains steady upgrades in metro networks while automotive LiDAR and industrial sensing open adjacencies for analog and polarization modulators. The optical modulators market size in these mature regions grows via technology refresh, contrasting with volume-driven expansion in emerging economies.