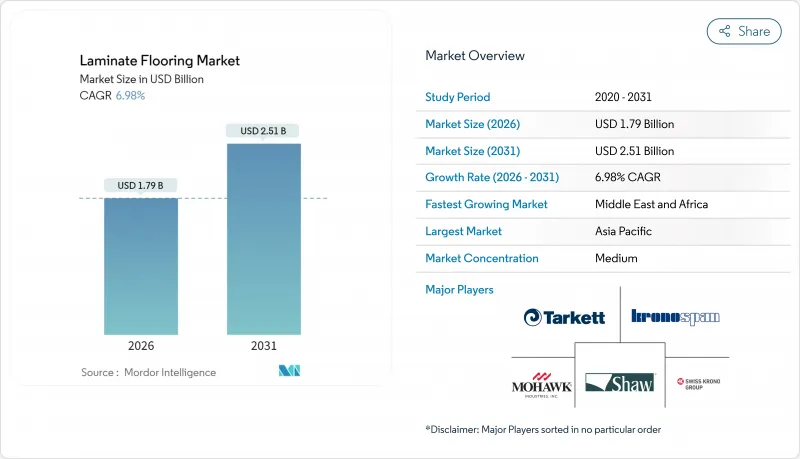

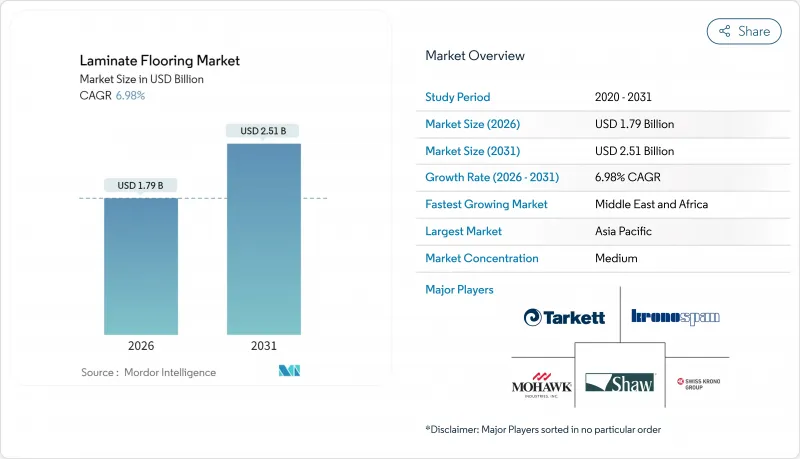

세계의 라미네이트 바닥재 시장은 2025년 16억 7,000만 달러로 평가되었으며, 2026년 17억 9,000만 달러에서 2031년까지 25억 1,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중(2026-2031년) CAGR은 6.98%로 전망됩니다.

이 성장세는 팬데믹 후 주택 리노베이션 수요, 아시아태평양의 도시 주택 착공 건수 증가, 보다 안전한 배합을 촉진하는 포름알데히드 규제의 강화에 기인하고 있습니다. 기술 혁신은 내수성 코어재와 시공 노력을 삭감하는 클릭-락 시스템 등, 용도의 가능성이 넓어지고, 이것이 하드우드나 세라믹 타일과의 비교에 있어서 주요한 우위성이 되고 있습니다. 고급 비닐 바닥재 제조업체가 생산능력 확대에 투자하는 가운데 경쟁이 치열해지고 있습니다. 그러나 라미네이트 바닥재는 여전히 매력적인 비용 구조를 유지하면서 이전보다 자연 소재의 질감을 더 설득력을 가지고 재현하고 있습니다. 이익률은 HDF(고밀도 섬유판)나 MDF(중밀도 섬유판) 원재료 가격의 영향을 받기 쉬운 상황입니다만, 주요 제조업체에 의한 수직 통합이 가격 변동의 영향을 일부 상쇄하고 있습니다.

세계의 락다운에 의해 소비자의 지출이 주택 개수로 이동해, 경제 재개 후에도 계속되는 바닥재 교환 수요의 급증을 가져왔습니다. Houzz의 2024년 조사에서는 주택 소유자의 67%가 대규모 바닥재 프로젝트를 실시했으며, 라미네이트는 저비용 시공과 현실적인 목조를 양립시켜 점유율을 확대했습니다. 성숙 시장에서는 노후화된 주택스톡이 신축보다 빈번한 개수를 필요로 하기 때문에 개수 프로젝트가 주류가 되어, 미국, 캐나다, 독일, 일본에 있어서 수요량 증가를 견인하고 있습니다. 원격 근무 동향에 의해 홈 오피스 수요가 지속되어, 카펫보다 의자의 흠집이나 커피를 쏟는 경우에 강한 내구성이 있는 바닥재가 요구되고 있습니다. DIY 체인점에서는 2024년을 통해 바닥재 판매가 호조로, Home Depot도 2025년 초까지 이 동향이 계속된다고 확인했습니다. 제조업체는 전문업자 없이 주말에 시공 가능한 간이 클릭식 시스템을 개발하여 라미네이트 바닥재의 리폼 수요를 더욱 강화하고 있습니다.

라미네이트의 시공 비용은 하드우드와 비교해 약 50% 낮고, 목재 가격이 급등하는 시기에 그 차이가 더욱 확대됩니다. 이로 인해 변동기에는 절약 지향 구매자가 소재 변경을 검토하는 경향이 있습니다. 엔지니어드 오버레이는 재마감의 필요성을 제거하고 평생 비용을 절감합니다. 임대 부동산과 최초의 주택 구매자에게 비용 효율적인 솔루션으로 자리를 잡고 있습니다. 최근의 텍스처 기술의 진보에 의해 손깎은 오크나 히코리의 감촉을 놀라울 정도로 충실하게 재현합니다. 일찌기 고급 지향의 구매층이 주저하고 있던 심미적인 타협점을 해소했습니다. 건설 회사는 모델 하우스에 라미네이트를 채용하는 경우가 증가하고 있습니다. 외관의 매력을 손상시키지 않고 예산 관리가 가능해지고 프로젝트가 확대됨에 따라 이 기술은 구매자의 업그레이드 수요로 파급되고 있습니다. 소매업체는 마케팅 메시지에서 가격 차이를 강조하고 소비자의 가격 우위에 대한 인식을 높이고 있습니다. 이 경제적 매력은 구매력이 여전히 제약을 받고 있는 신흥 시장에도 확산되어 인도, 인도네시아, 브라질 채용을 촉진하고 있습니다.

섬유판은 라미네이트 생산 비용의 약 65%를 차지하기 때문에 공급 충격 시에는 목재 칩이나 수지 원료의 가격 변동이 즉시 이익률을 압박합니다. 독일의 지표에서는 2024년 HDF 가격이 15-20% 상승했고, 제조업체는 여러 차례 인상을 강요받아 유통업체와의 관계에 긴장이 생겼습니다. 자사 패널 공장이 없는 중소 컨버터는 보다 큰 압력을 받아 불채산 계약에서 철수하는 경우도 보였습니다. 에너지 가격의 변동은 위험을 증폭시킵니다. 왜냐하면 섬유판 생산은 열을 대량으로 소비하기 때문에 비용이 천연가스나 전력요금에 연동하기 때문입니다. CARB 2단계 및 EU의 포름알데히드 함량 규제에 대한 대응은 수지의 복잡성과 비용을 증가시키지만, 이를 항상 전가할 수 있는 것은 아닙니다. 제조업체는 다년간의 섬유 계약이나 자사 수지 제조 시설에 의한 헤지를 실시하고 있지만, 이러한 전략에는 많은 지역 기업이 부족한 자본이 필요합니다.

2025년 HDF 기반 판자는 뛰어난 밀도로 일상적인 보행 시의 눌림에 강하고 라미네이트 바닥재 시장 점유율의 63.61%를 차지했습니다. 한편, MDF 대체품은 경량화에 의해 DIY 시공자의 취급이 용이하다는 점을 살려 CAGR 7.11%로 증가하고 있습니다. MDF 기재를 이용한 라미네이트 바닥재 시장 규모는 엠보싱 인레지스터 기술의 향상으로 매우 사실적인 질감을 실현함으로써 2026년 6억 5,000만 달러에서 2031년까지 9억 2,000만 달러로 확대될 것으로 전망됩니다. 공급업체는 HDF 제품을 프리미엄 가격대에 위치시키고, MDF 라인은 가치 채널을 타겟으로 함으로써, 자사 제품군의 세분화를 카니발리제이션 없이 실현하고 있습니다. 내습성 첨가제의 혁신에 의해 기존 성능 격차가 해소되고 있어, 설계자가 중간 정도의 부하가 걸리는 상업시설에서 MDF 채용을 검토하는 움직임이 확산되고 있습니다. 패널 제조업체는 탄소 목표 달성을 위해 재생 목재 섬유를 배합하고 있지만 기계적 특성은 EN 13329 마모 등급 기준을 충족합니다. 아시아 공장이 MDF 생산량을 늘리고 단위 비용을 낮추면 세계 가격 경쟁이 치열해지고 업계 경쟁은 더욱 격화될 것으로 예측됩니다.

수요 동향은 지역에 따라 다르며, 북미에서는 계절적인 습도 변동에 대한 내성으로부터 고밀도 코어재가 계속 선호되는 한편, 유럽에서는 MDF의 지속가능성이 중시되고 있습니다. 마케팅 캠페인에서는 저밀도 보드와 베이스 소재의 조합에 의한 차음성 향상이 강조되어 소음 대책을 요구하는 집합 주택 개발업체의 관심을 모으고 있습니다. 중국산 HDF에 대한 관세조치에 의해 수입업체는 베트남과 브라질로부터의 조달 다양화를 강요받아, 결과적으로 공급이 안정된 MDF의 수용이 촉진되고 있습니다. Kronospan과 Swiss Krono와 같은 브랜드는 판재 전체에서 밀도를 단계적으로 변화시키는 하이브리드 구조를 제안하여 HDF의 표면 내구성과 MDF의 비용 성능을 융합시키고 있습니다. 향후 기술 혁신에서는 성능을 저하시키지 않고 배출량을 더욱 삭감하는 바이오 베이스 수지의 활용이 모색될 것입니다. 구매자는 궁극적으로 가격, 안정성 및 품질 인식의 균형을 고려하여 기재 유형을 선택하게 됩니다.

아시아태평양은 중국과 인도의 대규모 주택 건설을 배경으로 2025년 세계 수익의 37.95%를 차지했습니다. 이 지역은 2031년까지 연평균 복합 성장률(CAGR) 6.55%를 유지할 것으로 예측됩니다. 중국의 도시 재개발은 계속되고 있으며, 현 수준의 도시에서는 진부화한 주택 단지의 재개발이 진행되어 라미네이트와 같은 비용 효율적인 내장재가 요구되고 있습니다. 인도의 PMAY-Urban 체계는 예산과 소비자 목재의 미관에 대한 기대의 균형을 맞추기 위해 라미네이트를 지정한 저소득자 주택을 조성합니다. 베트남과 필리핀을 포함한 동남아시아 시장에서는 중산 계급 소비가 확대되고 있으며 바닥재 제품의 조직적 소매 판매를 촉진하고 브랜드 인지도를 높이고 있습니다. 이 지역은 규제가 다양하기 때문에 배출 기준에 적합한 제품이 필요하며, 세계 제조업체는 현지에 시험소를 설치하고 있습니다.

중동 및 아프리카는 현재 규모가 작고 사우디아라비아, 이집트, 걸프 협력 회의(GCC) 국가에서 메가 프로젝트가 급증하고 있으며 CAGR 6.82%로 가장 급성장하고 있는 지역입니다. 개발자는 속도와 비용의 확실성을 우선시하고 있으며, 라미네이트는 현대 건축 테마에 적합한 외관과 함께이 두 가지 특성을 결합합니다. 수입 의존도가 여전히 높기 때문에 유통업체는 운송 불안정으로 인한 리드타임 위험을 제한하기 위해 보다 광범위한 SKU를 보유하고 있습니다. 통화 변동은 착륙 비용을 불안정하게 만들 수 있으므로 지역에서의 생산이 촉진되고 있습니다. Kronospan의 중동 패널 공장 실현 가능성 조사는 이러한 전환점을 보여줍니다. 소매업체가 현지 노동력에 적합한 클릭 락 기술에 대해 계약자에게 이해를 깊게 하기 위한 설치 워크숍을 개최하는 등 소비자 교육도 진행 중입니다. 북미 시장은 5.05%의 안정된 CAGR을 유지합니다. 지속적인 주택 개수 수요와 하이브리드 근무 형태에 의한 오피스 개축 수요의 축적이 견인합니다. 미국이 중국제 패널에 부과한 관세는 국내 생산량 증가를 촉구하고 Mohawk가 노스캐롤라이나주에서 실시한 8,700만 달러 규모의 확장 계획은 리쇼어링 동향을 상징하고 있습니다.

유럽에서는 프랑스와 독일의 건설 부진에도 불구하고 수요가 확대되고 있습니다. DIY 문화의 뿌리와 에너지 리노베이션 인센티브가 바닥재 업그레이드를 뒷받침하기 때문입니다. EU의 순환형 경제 지령에 의해 재활용성이 확인된 제품에 대한 관심이 높아지고, 공장에서는 바이오 베이스의 바인더 채용이나 회수 프로그램의 도입이 진행되고 있습니다. 중국산 합판에 대한 안티 덤핑 관세는 대체 목재 패널과의 가격 경쟁을 완화함으로써 간접적으로 지역의 라미네이트 공장을 보호하고 있습니다. 동유럽 국가, 특히 폴란드와 루마니아는 경쟁력 있는 인건비와 중앙 물류 거점으로 수출 거점으로 부상하고 있습니다. 남미는 경제변동 가운데 3.95%의 연평균 복합 성장률(CAGR)로 지연을 겪고 있지만, 브라질의 사회주택계획인 'Minha Casa Minha Vida'가 비용 효율적인 라미네이트 바닥재의 기반 수요를 창출하고 있습니다. 환율로 인한 수입 비용 상승은 Duratex와 같은 기업의 현지 생산을 촉진하고 있습니다.

The Laminate Flooring Market was valued at USD 1.67 billion in 2025 and estimated to grow from USD 1.79 billion in 2026 to reach USD 2.51 billion by 2031, at a CAGR of 6.98% during the forecast period (2026-2031).

Momentum stems from post-pandemic home renovation, accelerating urban housing starts in Asia-Pacific, and stricter formaldehyde regulations that spur safer formulations. Technology is widening end-use possibilities through water-resistant cores and click-lock systems that cut installation labor, a key advantage over hardwood and ceramic tile alternatives. Competition is intensifying as luxury vinyl players invest in capacity, yet laminate retains a compelling cost profile while replicating natural textures more convincingly than before. Margins remain sensitive to HDF and MDF input prices, but vertical integration among leading mills partially offsets volatility.

Global lockdowns reoriented consumer spending toward home upgrades, causing a sharp rise in flooring replacements that persists even as economies reopen. Houzz's 2024 survey showed 67% of homeowners undertook major flooring projects, and laminate won share by combining low install cost with realistic wood visuals. Renovation projects dominate mature markets because aging housing stock requires refreshes more frequently than new builds, boosting volumes in the United States, Canada, Germany, and Japan. Remote work trends keep the spotlight on home offices, directing demand toward durable surfaces that resist chair scuffs and coffee spills better than carpet. DIY chains reported elevated flooring sales throughout 2024, and Home Depot confirmed continuing strength into early 2025. Manufacturers responded with simplified click-systems that allow weekend installation without professional crews, reinforcing laminate's renovation appeal.

Laminate's installed cost runs roughly 50% below hardwood, a spread that widens when lumber prices spike, prompting thrifty buyers to switch materials during volatile periods. Engineered overlays eliminate the need for refinishing, lowering lifetime expense and positioning laminate as a value-engineered solution for rental properties and first-time homeowners. Recent texturing advances replicate hand-scraped oak or hickory finishes convincingly, reducing the aesthetic compromise that once deterred premium buyers. Builders increasingly use laminate in model homes to control budgets without sacrificing curb appeal, and this practice cascades to buyer upgrades once a project scales. Retailers highlight the value gap in marketing messages, amplifying consumer awareness of price advantages. The economic appeal extends to emerging markets where purchasing power remains constrained, fuelling adoption in India, Indonesia, and Brazil.

Fibreboard accounts for roughly 65% of laminate production cost, so swings in woodchip and resin inputs quickly erode margins during supply shocks. German indices showed 15-20% HDF inflation during 2024, compelling mills to execute multiple price hikes that strained distributor relationships. Smaller converters lacking captive panel mills faced greater pressure, occasionally exiting unprofitable contracts. Energy price fluctuations magnify the risk because fiberboard production is heat-intensive, tying costs to natural gas and electricity tariffs. Compliance with CARB Phase 2 and EU limits on formaldehyde content adds resin complexity and cost that cannot always be passed downstream. Manufacturers hedge through multi-year fiber contracts and in-house resin facilities, but such strategies require capital that many regional players lack.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

HDF-based planks commanded 63.61% of laminate flooring market share in 2025 due to superior density that resists indentation during daily traffic. MDF alternatives, however, are increasing at a 7.11% CAGR, capitalizing on lighter weight that eases handling for DIY installers. The laminate flooring market size for MDF substrates is projected to expand from USD 0.65 billion in 2026 to USD 0.92 billion by 2031 as improved emboss-in-register technology delivers highly realistic textures. Suppliers position HDF products at premium price points while MDF lines target value channels, enabling portfolio segmentation without cannibalization. Innovations in moisture-resistant additives blur the historical performance gap, encouraging specifiers to accept MDF in moderate-duty commercial jobs. Panel producers integrate recycled wood fibers to meet carbon goals, yet mechanical properties still meet EN 13329 wear ratings. Sector rivalry is expected to intensify as Asian mills scale MDF output, lowering unit cost and amplifying price competition globally.

Demand dynamics vary regionally, with North America continuing to favor high-density cores for resilience against seasonal humidity swings, while Europe leans toward MDF's sustainability narrative. Marketing campaigns highlight acoustic improvements possible through lower-density boards paired with underlay, a feature attracting multifamily developers seeking noise mitigation. Trade tariffs on Chinese HDF push importers to diversify sourcing from Vietnam and Brazil, inadvertently boosting MDF acceptance where availability proves steadier. Brands such as Kronospan and Swiss Krono showcase hybrid constructions that gradient density across the plank, merging HDF surface durability with MDF affordability. Future innovation may explore bio-based resins to further cut emissions without sacrificing performance. Buyers will ultimately balance price, stability, and perceived quality when selecting substrate types.

The Laminate Flooring Market Report is Segmented by Product Type (High-Density Fiberboard, Medium-Density Fiberboard), Application (Residential, Commercial), Construction (New Construction, Renovation/Replacement), and Geography (North America, South America, Europe, Asia-Pacific, Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commanded 37.95% of global revenue in 2025 on the back of large-scale residential construction in China and India, and the region is projected to post a 6.55% CAGR through 2031. Chinese urban renewal continues, with county-level cities redeveloping obsolete housing blocks that require cost-effective interiors like laminate. India's PMAY-Urban scheme subsidizes low-income flats that specify laminate to balance the budget with consumer expectations for wood aesthetics. Southeast Asian markets, including Vietnam and the Philippines, witness rising middle-class consumption, driving organized retail of flooring products and increasing brand awareness. Regulatory diversity across the region necessitates tailored emission compliance, prompting global manufacturers to set up localized testing labs.

Middle East & Africa, though smaller today, is the fastest-growing territory at 6.82% CAGR as megaprojects proliferate in Saudi Arabia, Egypt, and the Gulf Cooperation Council. Developers prioritize speed and cost certainty; laminate delivers both attributes alongside visuals suited to modern architectural themes. Import dependency remains high, so distributors stock broader SKU assortments to limit lead-time risk amid shipping volatility. Currency swings can destabilize landed cost, encouraging regional production; Kronospan's feasibility study for a Middle East panel plant illustrates this pivot. Consumer education is underway as retailers host installation workshops to familiarize contractors with click-lock techniques suitable for local labor pools. North America grows at a steady 5.05% CAGR, propelled by persistent home improvement and a backlog of office conversions sparked by hybrid work arrangements. U.S. tariffs on Chinese panels raise domestic production volumes, and Mohawk's USD 87 million expansion in North Carolina exemplifies reshoring trends.

European demand advances despite construction downturns in France and Germany, as robust DIY cultures and energy-retrofit incentives fuel flooring upgrades. EU circular-economy directives elevate interest in products with verified recyclability, encouraging mills to adopt bio-based binders and take-back programs. Anti-dumping duties on Chinese plywood indirectly shield regional laminate mills by reducing price competition from alternative wood panels. Eastern European countries, notably Poland and Romania, emerge as export hubs due to competitive labor costs and central logistics. South America trails with 3.95% CAGR amid economic volatility, yet Brazil's Minha Casa Minha Vida social-housing initiative adds baseline volume for cost-efficient laminate. Currency depreciation elevates import costs, stimulating local production by firms such as Duratex.