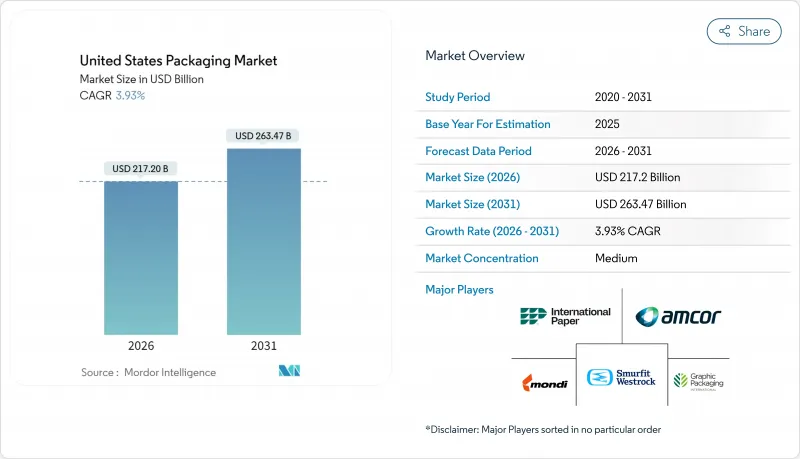

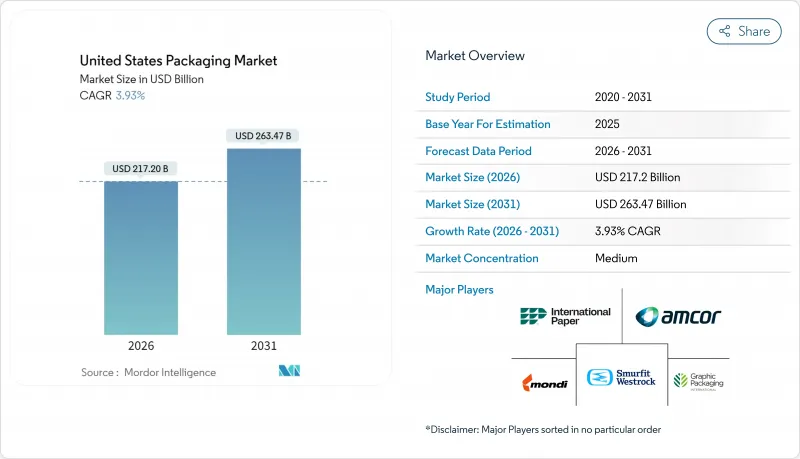

미국의 포장 시장은 2025년 2,089억 8,000만 달러에서 2026년에는 2,172억 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 3.93%를 나타낼 것으로 예상됩니다. 2031년까지 2,634억 7,000만 달러에 달할 전망입니다.

9,408억 달러 규모의 트럭 운송 업계와의 견고한 연계가 미국의 포장 시장의 회복력을 지원하고 있습니다. 포장의 디자인과 무게가 직접화물 수송 비용에 영향을 미치기 때문입니다. 전자상거래 확대, 주레벨 확대 생산자 책임법(EPR) 등의 규제 변화, 의약품 생산 능력의 국내 회귀 가속이 자동화 대응 라인과 고배리어성 소재에 대한 투자를 촉진하고 있습니다. 미국 시장은 식품 및 음료 분야에서 프리미엄화의 혜택을 계속 받고 있습니다만, PFAS 프리 규제나 폴리머 생산 능력 증강에 의한 코스트 압력에 의해 컨버터 기업의 이익률은 압박되고 있습니다. 대규모 통합 공급업체는 규모와 연구 개발의 깊이를 활용하여 규제 준수 비용을 흡수하고 가격 결정력을 유지하고 있습니다. 한편, 중소기업은 틈새 시장에서 차별화를 도모하고 있습니다.

자동화 대응의 2차 라인에 투자함으로써 소비재 제조업체는 노동력 부족과 SKU 증가를 효율적으로 관리할 수 있습니다. 메리 케이는 200만 달러의 설비 갱신 후 라인 노동력을 85% 삭감하면서 분당 50-60유닛의 생산을 유지했습니다. 주요 운송 회사의 체중 중량 과금 제도는 소형 경량 소포를 우월하고 적절한 크기의 골판지 인서트와 완충재 수요를 자극하고 있습니다. 미국의 포장 시장이 옴니 채널 대응으로 이행하는 동안 보호 기능, 브랜드화, 데이터 풍부한 통합 솔루션을 제공하는 컨버터는 마지막 마일 비용 절감을 목표로 소매업체로부터 수주를 획득하고 있습니다. 자동화는 유통업체의 피킹·패킹 미스 삭감과 다음날 배송의 실현을 지원해, 신뢰성이 높은 2차 포장이 경쟁상의 필수 요건이 되고 있습니다. 공급망 리스크 경감을 위해서 기재의 복수 조달이 진행되어, 다양한 소재 포트폴리오를 가지는 컨버터가 혜택을 받고 있습니다.

프리미엄 브랜드는 보존 기간을 연장하고 클린 라벨 처방에 대응하는 다층 고 배리어 필름으로 이행하고 있으며, 이 움직임이 미국의 포장 시장에서 단가 상승을 견인하고 있습니다. 첨단 코팅 기술은 산소, 빛, 습기를 차단하고 첨가물이없는 천연 풍미를 보호하고 식품 폐기를 줄입니다. 소비자는 재봉 가능한 주둥이와 투명한 창문 파우치를 선호하기 때문에 컨버터는 장벽 성능과 매장에서의 소구력의 균형이 요구됩니다. FDA의 식품 접촉 승인은 컴플라이언스의 복잡성을 늘리고 저설비 투자 경쟁 업체의 진입을 제한합니다. 브랜드 소유자는 소비자가 인식하는 품질에 대해 지불하려는 의도를 중심으로 한 마진 확장 전략을 통해 높은 포장 비용을 정당화하고 있습니다. 오가닉 스낵과 레이디 투 드링크 커피의 매출 증가에 따라 프리미엄 연포장에 대한 수요가 높아지고, 필름 압출 제조업체의 장기 수주가 강화되고 있습니다.

뉴섬 주지사는 사업 부담을 이유로 초기 규제 실시를 연기했지만, 2032년까지 플라스틱을 25% 삭감할 의무와 50억 달러의 폐기물 기금은 유효합니다. 생산자는 재활용 인프라에 자금을 제공하고 포장을 재설계하거나 단계적 요금을 지불해야합니다. 미국의 포장 시장의 대기업은 비용을 폭넓은 제품군에 분산할 수 있는 한편, 중소 컨버터는 이익률의 저하와 설비 투자 능력의 축소에 직면하고 있습니다. 불확실성으로 신제품 투입이 정체되고, 캘리포니아주 한정 SKU와 전국통일규격의 선택을 둘러싼 논의가 주간 물류를 복잡화시키고 있습니다. 브랜드 소유자에 대한 비용 전가는 매장 가격에 압력을 가하여 선택적 소비재 카테고리의 판매 수량 성장을 둔화시킬 수 있습니다.

플라스틱은 범용성과 비용 효율성이 높기 때문에 2025년 시점에서 미국의 포장 시장 점유율의 35.88%를 유지했습니다. 그러나 종이 및 판지는 CAGR 5.33%로 확대하고 있어 소매업체가 섬유계 대체품의 도입을 약속하는 가운데, 2031년까지 플라스틱의 점유율을 일부 침식할 것으로 예측됩니다. 에너지부가 셀룰로오스계 필름에 5,200만 달러를 기여하는 움직임은 차세대 기재에 대한 공공 부문의 지원을 나타냅니다. 천연 HDPE 부족으로 인해 2025년 3월에는 재활용 수지 가격이 파운드당 96센트에 이르렀으며 병에서 병으로 재활용하는 프로젝트에 과제가 발생했습니다.

미국 포장 시장의 플라스틱 가공업자는 탄소 회계 요구와 수지 공급 과잉 위험의 이중 압력에 직면하고 있습니다. 투자는 재활용성을 고려한 단일 소재 PE 필름으로 이행하는 한편, 다층 나일론 구조는 높은 배리어지로 이행하고 있습니다. 음료 제조업체가 무한 재활용을 요구하는 합금 캔을 채택하는 동안 금속 포장 수요는 유지됩니다. 전체적으로 소재 선정에서는 기본 성능 이상으로 비용, 순환성 지표, 규제 리스크의 밸런스가 중시되게 되었습니다.

2025년 종이 및 판지 제품은 골판지의 대량 소비로 미국 포장 시장 점유율의 28.70%를 차지했습니다. 금속품은 탄산음료나 하드셀처가 경량화와 리사이클 이점을 요구하여 알루미늄캔을 선택했기 때문에 CAGR 6.64%를 나타낼 것으로 예측됩니다. 크라운 홀딩스의 식수 수입은 2024년에 17% 증가하여 지속적인 수요를 뒷받침했습니다. 실간이 금속 식품 캔 시장에서 50%의 점유율을 유지하고 있다는 사실은 상온 저장 가능 제품의 강인성을 보여줍니다.

디지털 인쇄의 도입으로 가공업자는 계절적인 SKU 급증에 대응할 수 있게 되는 반면, HDPE 저그 등의 경질 플라스틱은 밸류 팩에서 식료품 업계의 지지를 유지하고 있습니다. 그러나 금속의 무한한 재활용이라는 특성은 기후 변화를 걱정하는 소비자에게 공감을 불러 일으키고, 프로모션 예산이 캔 중심의 형식으로 이동하고 있습니다. LME 알루미늄 가격의 변동이 수량 증가를 억제할 수 있지만, 브랜드 소유자는 다년간의 테이크 오어 페이 계약으로 헤지하여 캔 제조업체로의 주문을 안정시키고 있습니다.

The United States Packaging market is expected to grow from USD 208.98 billion in 2025 to USD 217.2 billion in 2026 and is forecast to reach USD 263.47 billion by 2031 at 3.93% CAGR over 2026-2031.

Strong links to the country's USD 940.8 billion trucking sector keep the US packaging market resilient, because packaging design and weight directly shape freight costs. E-commerce proliferation, regulatory shifts such as state-level Extended Producer Responsibility statutes, and accelerated on-shoring of pharmaceutical capacity are steering capital toward automation-ready lines and higher-barrier materials. The US market continues to benefit from premiumization in food and beverage segments, while cost pressures from PFAS-free mandates and polymer capacity additions squeeze margins for converters. Large, integrated suppliers leverage scale and R&D depth to absorb regulatory compliance costs and preserve pricing power as smaller firms seek niche differentiation.

Investments in automation-ready secondary lines allow consumer packaged goods firms to manage labor shortages and SKU proliferation efficiently, with Mary Kay trimming line labor by 85% after a USD 2 million upgrade while maintaining 50-60 units per minute. Dimensional-weight pricing by major carriers rewards smaller, lighter parcel formats, stimulating demand for right-sized corrugated inserts and cushioning. As the US packaging market aligns with omnichannel fulfillment, converters that offer integrated protective, branded, and data-rich solutions capture volume from retailers seeking to cut last-mile costs. Automation helps distributors minimize pick-pack errors and meet one-day delivery promises, making reliable secondary packaging a competitive necessity. Supply chain risk mitigation encourages multisourcing of substrates, benefiting converters with diversified material portfolios.

Premium brands are shifting to multilayer high-barrier films that extend shelf life and support clean-label formulas, a move that lifts average price per unit in the US packaging market. Advanced coatings block oxygen, light, and moisture, safeguarding natural flavors without additives and reducing food waste. Consumers favor pouches with resealable spouts and transparent windows, pushing converters to balance barrier performance with shelf appeal. FDA food contact clearances add compliance complexity, limiting the entry of low-capex competitors. Brand owners justify higher pack costs through margin-expansion strategies centered on consumer willingness to pay for perceived quality. As sales of organic snacks and ready-to-drink coffees climb, demand for premium flexible formats strengthens long-term order books for film extruders.

Governor Newsom delayed initial regulations, citing business burden, yet the 25% plastic reduction mandate by 2032 and the USD 5 billion waste fund remain in force. Producers must finance recycling infrastructure and redesign packages or pay modulated fees. Larger players in the US packaging market spread costs across wider portfolios, whereas small converters face margin erosion and reduced capex capacity. Uncertainty stalls new-product launches and complicates interstate logistics as companies debate California-only SKUs versus national harmonization. Cost pass-through to brand owners pressures shelf pricing, potentially dampening volume growth in discretionary categories.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastic retained 35.88% of the US packaging market share in 2025, thanks to versatility and cost efficiency. Paper and paperboard, however, grew at a 5.33% CAGR and are expected to erode some plastic volume by 2031 as retailers pledge fiber-based alternatives. The Department of Energy's USD 52 million fund toward cellulose-based films signals public-sector backing for next-gen substrates. Natural HDPE scarcity pushed recycled resin to 96 cents per pound in March 2025, challenging bottle-to-bottle projects.

Plastic converters in the US packaging market face dual pressure from carbon accounting demands and resin oversupply risks. Investments shift to mono-material PE films engineered for recyclability, while multi-layer nylon structures migrate to high-barrier paper. Metal packaging maintains demand as beverage makers lock in alloy cans to meet infinitely recyclable claims. Overall, material selection now balances cost, circularity metrics, and regulatory exposure more than basic performance.

Paper and paperboard products commanded 28.70% of the US packaging market share in 2025 due to high corrugated volumes. Metal products are forecast to grow at a 6.64% CAGR as carbonated soft drinks and hard seltzers choose aluminum cans for lightweighting and recycling benefits. Crown Holdings' beverage can income rose 17% in 2024, underscoring secular demand. Silgan's 50% hold on metal food cans shows the resilience of shelf-stable products.

Digital print adoption empowers converters to serve seasonal SKU spikes, while rigid plastics such as HDPE jugs retain grocery loyalty for value packs. Yet metal's infinite-recycle narrative resonates with climate-conscious shoppers, shifting promotional budgets toward can-centric formats. Price swings in LME aluminum could temper volume gains, but brand owners hedge through multiyear take-or-pay deals, stabilizing orders for can-makers.

The United States Packaging Market Report is Segmented by Material Type (Paper and Paperboard, Plastic, Metal, and Container Glass), Product Type (Paper and Paperboard Product Type, Plastic Product Type, and More), Packaging Format (Rigid Packaging Format, and Flexible Packaging Format), and End-User (Food, Beverage, Personal Care and Cosmetics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).