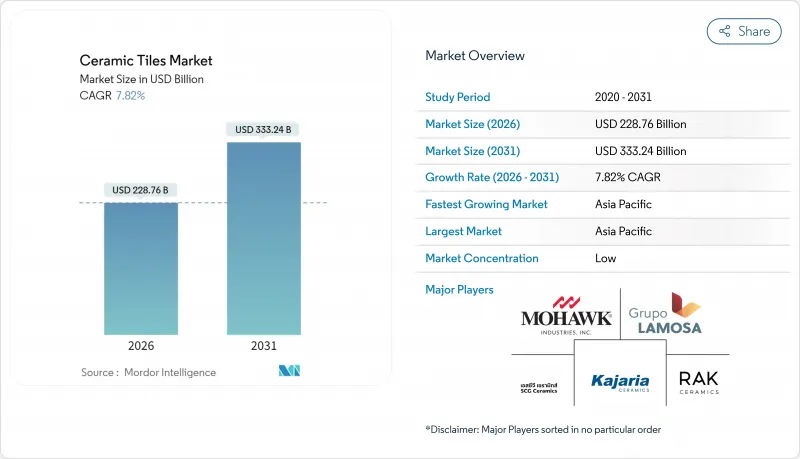

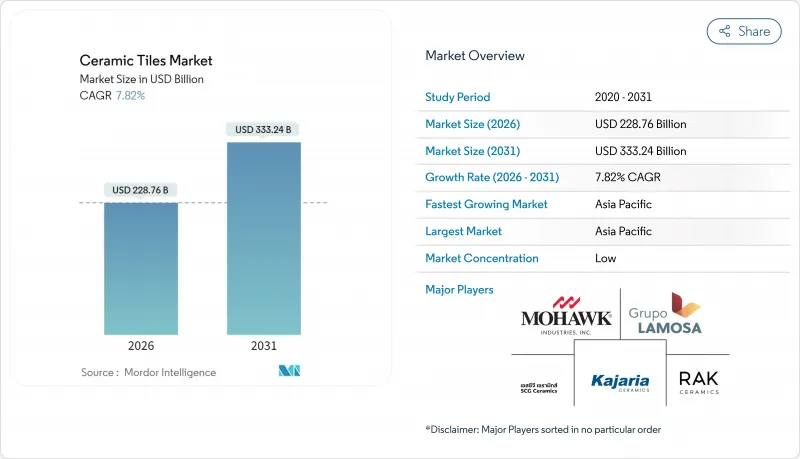

세계의 세라믹 타일 시장은 2025년 2,121억 7,000만 달러로 평가되었으며, 2026년 2,287억 6,000만 달러에서 2031년까지 3,332억 4,000만 달러에 이를 것으로 예측됩니다. 예측 기간 중(2026-2031년) CAGR은 7.82%로 예상됩니다.

공공 부문의 꾸준한 인프라 지출, 아시아태평양의 급속한 도시로의 인구 이동, 내구성이 높고 청소하기 쉬운 표면재를 선호하는 소비자의 기호가 이 확대를 지지하고 있습니다. 미국의 새로운 정부 지출 패키지뿐만 아니라 인도 및 동남아시아의 지하철, 공항, 스마트 시티 개발의 지속은 바닥재 및 외장재 제품의 잠재적 수요 기반을 확대하고 있습니다. 또, 도자기에 매우 현실적인 석재, 목재 및 금속 효과를 프린트하는 기술이 수요를 뒷받침하고 있어 천연 소재와 같은 가격 변동 리스크 없이 고급화를 실현하고 있습니다. 유럽의 환경 규제는 저탄소 가마와 폐기물 유래 원료 혼합물의 도입을 가속화하고 온라인 소매 채널은 세계의 제품 가용성과 가격 투명성을 높입니다.

교통 회랑, 에너지 플랜트 및 복합 시설에 대한 세계 자본 지출은 세라믹 타일 시장에 대량 주문을 촉진하고 있습니다. 미국에서는 다년간 연방 프로그램이 도로, 교량, 반도체 공장, 청정 에너지 시설에 총 1조 2,000억 달러를 배분하여 공장 및 데이터센터에 지정된 중부하 세라믹 타일의 지속적인 수요를 창출하고 있습니다. 중국의 '일대일로' 구상은 협력 경제권에서 타일을 많이 사용하는 철도역과 주택건설을 추진하고 있으며, 아세안 정부도 30년의 수명을 가진 바닥재 제품을 우선하는 토목공사 예산을 증가시키고 있습니다. 골재 및 시멘트 공급업체는 두 자리 수익 성장을 보고하고 세라믹 표면재의 견조한 하류 소비를 보여줍니다.

디자이너는 시각적 임팩트와 성능을 양립시키는 경향을 강화하고 있어 대형 판재나 대리석 스타일 슬래브의 채용을 촉진하고 있습니다. 잉크젯 프린터는 채석장의 석재에 필적하는 줄무늬와 금속 광택을 재현하면서 경량화와 색조의 재현성을 실현합니다. 최대 1.8m×3.6m의 대형 도자기판은 줄눈을 줄여 오픈 플랜 오피스나 고급 주택에서 중시되는 매끄러운 연속성을 표현합니다. 단납기 유약에 의해 생산 사이클이 단축되어 패션 동향을 반영한 빈번한 신스타일 도입이 가능하게 되었습니다. 내습성이 중요한 주방과 지하실에서는 세라믹 타일 시장이 하드우드재에 대해 점유율을 확대하고 있습니다. 건축가는 전자기기 조립층을 위한 정전기 방지 마감을 지정하여 장식성을 넘어 기능적인 매력을 넓히고 있습니다.

많은 선진국 시장에서는 숙련된 타일 장인이 부족하여 인건비 상승과 프로젝트 공기 연장을 초래하고 있습니다. 대형 도자기 슬래브는 전용의 리프팅 장치와 에폭시계 그라우트를 필요로 하며, 표준적인 60cm 제품에 비해 시공 예산을 15-25% 증가시킵니다. 주택 소유자가 주말에 플로팅 비닐판을 스스로 시공할 수 있는 반면, 세라믹의 리노베이션에는 전문적인 방수 처리와 기초 준비가 요구됩니다. 업계 단체는 인정 제도를 강화하고 있지만, 인정 작업원 공급은 수요에 따라 잡히지 않고, 특히 개수 공사에서의 단기적인 수량 성장을 억제하고 있습니다.

세라믹 타일은 흡수율 0.5% 미만, 동결 내성을 갖추고 옥외 광장이나 교통 거점에 적합하기 때문에 2025년에는 세라믹 타일 시장 점유율의 50.78%를 차지했습니다. 잉크젯 장식 기술에 의해 강화된 유약 도자기는 2031년까지 연평균 복합 성장률(CAGR) 8.34%를 기록해 유약 세라믹과 모자이크 형식을 웃도는 전망입니다. 소비자는 전체 착색과 내마모성 클래스(PEI IV 이상)를 내구성의 증거로 파악해, 호텔 로비나 공항에 대리석의 대체재로서 채용이 진행되고 있습니다.

이 부문의 기세는 제조업체가 연속 가마를 활용하여 외관용 대형 박판을 대량 생산하고, 구조 부하를 경감하면서 내충격성을 유지함으로써 세라믹 타일 시장 전체를 견인하고 있습니다. 모자이크 타일은 틈새 시장이면서 장인 기술의 미학이 가격 프리미엄을 낳는 고급 스파에서 점유율을 획득했습니다. 항균 작용을 갖춘 구리 유약의 혁신에 의해 식품 취급 구역이나 병원에서의 용도가 넓어져 제품 다양화가 지속적인 수익 성장을 지원하는 좋은 예가 되고 있습니다.

바닥재 설치는 습기 있는 지역과 고교통량 복도의 필수 사양에 따라 2025년 세라믹 타일 시장 규모의 48.10%를 차지했습니다. 미끄럼 방지 가공의 세라믹 타일과 공업용 쿼리 타일이 상업용 주방, 창고, 교통기관의 역을 지배하고, 기초가 되는 수량의 안정성을 확보하고 있습니다.

벽면 용도는 2031년까지 연평균 복합 성장률(CAGR) 8.17%로 확대되어 건축가가 특징 벽, 호텔 접수, 소매점의 배경에 텍스처 가공이나 3D 표면을 채용하는 움직임이 뒷받침하고 있습니다. 디자인 옵션 확장으로 평균 판매 가격이 상승하고 세척이 용이한 유약은 접객 산업의 위생 기준을 충족합니다. 지붕 및 외벽 용도는 세라믹의 축열성과 우박 내성이 평가되는 지중해 지역 및 안데스 지역에 집중하는 한편, 카운터탑, 풀 및 틈새 용도가 종합적으로 잠재 수요를 확대합니다.

세라믹 타일 시장은 제품 유형별(자기 타일, 유약 세라믹 타일 등), 용도별(바닥재, 벽재 등), 최종 사용자별(주택, 상업시설, 공업 시설), 건설 단계별(신축, 개수 및 리노베이션), 유통 채널별(독립 소매점, 대형 홈 센터 등), 지역별로 구분됩니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

아시아태평양은 2025년 세계 수익의 47.35%를 차지했으며 2031년까지 연률 8.31%를 보일 것으로 예측됩니다. 이것은 대규모 도시 주택 건설, 지하철 연장, 수출 지향형 생산 클러스터에 의해 지원됩니다. 중국 내륙에서는 점토광에 가까운 지역에서 생산 능력이 확대되고, 인도에서는 유리질 바닥재의 사용을 규정하는 스마트 시티 계획과 저가격 주택 계획이 추진되고 있습니다. 베트남에서는 100개 이상의 제조업체가 북부 지역에 집중되어 있으며, 유약용 화학약품을 수입에 의존하고 있지만, 2024년에는 유약 타일 80%, 세라믹 타일 20%의 생산 구성을 달성했습니다. ASEAN 무역협정에 의한 무관세 유통이 실현되고, 지역 통합형 공급 체인이 촉진되고 있습니다.

북미는 성숙한 시장이지만 전략적으로 중요한 지역이며, 국내 제조업체는 미래의 안티 덤핑 관세에 대비하고 있습니다. 미국에서는 모기지 금리 상승으로 2024년 타일 소비량은 2억 6,450만 평방미터로 감소했지만, 반도체 및 배터리 공장에 대한 연방 정부 지출이 장기적인 수요를 지지하고 있습니다. Mohawk Industries는 테네시와 텍사스의 수직 통합 가마를 사용하여 리드 타임 단축과 공공 프로젝트 사양을 확보하고 있습니다. 캐나다에서는 병원 및 교통수단 개조 사업에 자금이 투입되어 저탄소 재료의 사용이 점점 의무화되고 있습니다. 한편, 멕시코의 Grupo Lamosa는 라틴아메리카 전역에 공장을 전개해 통화 리스크의 분산을 도모하고 있습니다. 유럽에서는 에너지 가격 상승으로 2023년 생산량이 18% 감소했지만, 세계 타일 기계 수출의 50%를 차지하고 있습니다(assopiastrelle.it). 이탈리아의 폐쇄 루프 공장에서는 소성 전 스크랩을 100% 재활용하여 환경면에서 리더십을 발휘하고 있습니다. 스페인에서는 EU의 넷 제로 목표 달성을 위한 수소 가마의 파일럿 사업이 추진되는 한편, 폴란드에서는 점토 부족으로 수입 증가와 스팟 가격의 변동이 발생하고 있습니다. 중동 및 아프리카에서는 이집트가 저비용의 셰일 자원을 활용하여 연간 2억 평방미터를 생산합니다. 아랍에미리트(UAE)의 라스 알하이마 지역에는 40,000개의 산업 등록 기업이 집적되어 관련 표면 마감 수요를 견인하고 있습니다.

The ceramic tiles market was valued at USD 212.17 billion in 2025 and estimated to grow from USD 228.76 billion in 2026 to reach USD 333.24 billion by 2031, at a CAGR of 7.82% during the forecast period (2026-2031).

Steady public-sector infrastructure outlays, rapid urban migration in Asia-Pacific, and consumers' preference for durable, easy-to-clean surfaces anchor this expansion. New government spending packages in the United States and ongoing metro, airport, and smart-city developments in India and Southeast Asia are enlarging the addressable base for flooring and cladding products. Demand also benefits from technology that prints hyper-realistic stone, wood, and metallic effects on porcelain bodies, enabling premiumization without the price volatility of natural materials. Environmental regulations in Europe accelerate the rollout of low-carbon kilns and waste-based raw mixes, while online retail channels broaden product availability and price transparency worldwide.

Global capital spending on transport corridors, energy plants, and mixed-use complexes is stimulating large-volume orders for the ceramic tiles market. In the United States, multiyear federal programmed collectively allocate USD 1.2 trillion to roads, bridges, semiconductor fabs, and clean-energy facilities, generating sustained demand for heavy-duty porcelain specified in factories and data centers. China's Belt and Road Initiative drives tile-intensive rail stations and housing in partner economies, while ASEAN governments raise civil works budgets that favor flooring products with 30-year service lives. Suppliers of aggregates and cement report double-digit revenue growth, signaling robust downstream consumption of ceramic surfacing.

Designers increasingly combine visual impact with performance, fuelling the uptake of large-format planks and marble-look slabs. Inkjet printers replicate veining and metallic highlights that rival quarried stone, but at lower weight and in repeatable colourways. Format growth-porcelain boards up to 1.8 m by 3.6 m-reduces grout lines and conveys seamless continuity valued in open-plan offices and luxury residences. Quick-fire glazes cut production cycles, enabling frequent style introductions that mirror fashion trends. The ceramic tiles market also gains share versus hardwood in kitchens and basements where moisture resistance is critical. Architects specify anti-static finishes for electronics assembly floors, widening functional appeal beyond decor.

Skilled tile setters remain scarce in many developed markets, lifting labour rates and extending project timelines. Large-format porcelain slabs need specialised lifting rigs and epoxy grouts, adding 15-25% to installation budgets versus standard 60 cm products. Where homeowners can install floating vinyl planks themselves over a weekend, ceramic renovations require professional waterproofing and sub-floor preparation. Industry associations have stepped up certification schemes, yet supply of certified crews lags demand, tempering short-run volume growth, especially in refurbishments.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Porcelain tiles secured 50.78% of the ceramic tiles market share in 2025 owing to water-absorption rates below 0.5% and frost resistance that suits outdoor plazas and transit hubs. Glazed porcelain, aided by inkjet decoration, is projected to register an 8.34% CAGR through 2031, outpacing glazed ceramic and mosaic formats. Consumers perceive its colour-through body and abrasion class >= PEI IV as proof of longevity, encouraging substitution for marble in hotel lobbies and airports.

The segment's momentum lifts the overall ceramic tiles market as manufacturers leverage continuous kilns to mass-produce large thin slabs for facades, reducing structural load yet retaining impact strength. Mosaic tiles, though niche, capture share in luxury spas were artisanal aesthetics command price premiums. Copper-glaze innovations offering antimicrobial action broaden use in food-handling zones and hospitals, illustrating how product diversification underpins sustained revenue growth.

Floor installations represented 48.10% of the ceramic tiles market size in 2025 driven by mandatory specification in wet areas and heavy-traffic corridors. Slip-resistant porcelain and industrial-grade quarry tiles dominate commercial kitchens, warehouses, and transit stations, ensuring baseline volume stability.

Wall applications, posting an 8.17% CAGR to 2031, flourish as architects deploy textured and 3D surfaces for feature walls, hotel receptions, and retail backdrops. Expanded design palettes increase average selling prices, and easy-clean glazes meet hospitality hygiene codes. Roof and facade uses remain concentrated in Mediterranean and Andean regions where ceramic's thermal mass and hail resistance are valued, while countertop, pool, and niche applications collectively extend total addressable demand.

The Ceramic Tiles Market Segments Into by Product Type (Porcelain Tiles, Glazed Ceramic Tiles, and More), by Application (Floor, Wall, and More), by End-User (Residential, Commercial, Industrial), by Construction (New Construction, Replacement and Renovation), by Distribution Channel (Independent Retailers, Large Home Centers and More), by Geography. The Market Forecasts are Provided in Terms of Value (USD)

Asia-Pacific accounted for 47.35% of global revenue in 2025 and is forecast to compound to 8.31% annually through 2031, anchored by mass urban housing, metro extensions, and export-oriented production clusters. China's inland provinces add capacity close to clay deposits, while India scales smart-city and affordable-housing schemes that stipulate vitrified flooring. Vietnam's 100-plus manufacturers, concentrated in the north, rely on imported chemicals for glazes but still achieved a combined output mix of 80% glazed and 20% porcelain tiles in 2024. ASEAN trade agreements allow duty-free flows, favouring regionally integrated supply chains.

North America presents a mature but strategically important arena where domestic producers hedge against future antidumping duties. US tile consumption eased to 264.5 million m2 in 2024 amid high mortgage rates, yet federal outlays on semiconductor and battery plants underpin long-term volume. Mohawk Industries leverages vertically integrated Tennessee and Texas kilns to shorten lead times and secure public-project specifications. Canada funds hospital and transit refurbishments that increasingly stipulate low-carbon materials, while Mexico's Grupo Lamosa operates plants across Latin America to diversify currency exposure. Europe, while posting an 18% output drop in 2023 due to energy spikes, still accounts for 50% of global tile-machinery exports assopiastrelle.it. Italy's closed-loop plants recycle 100% of unfired scrap, showcasing environmental leadership. Spain advances hydrogen-kiln pilots to meet EU Net-Zero targets, while Poland's clay shortages force higher imports and spot-price volatility. In the Middle East and Africa, Egypt produces 200 million m2 annually using low-cost shale resources, and the UAE's Ras Al Khaimah cluster hosts 40,000 industrial registrants, fuelling related surface-finishing demand.