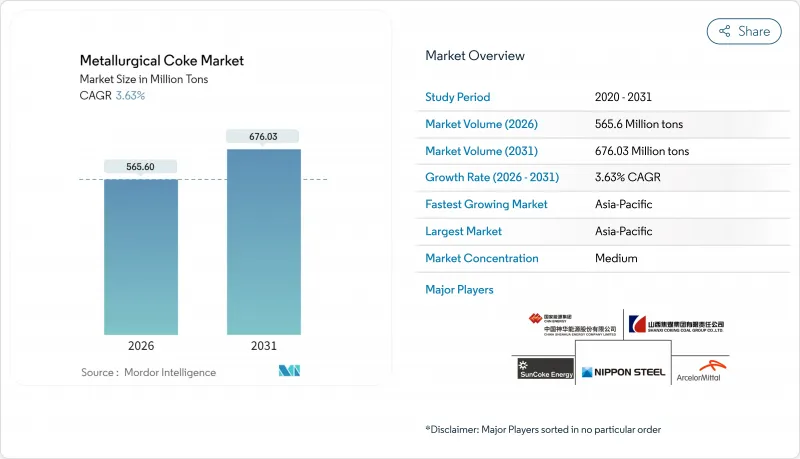

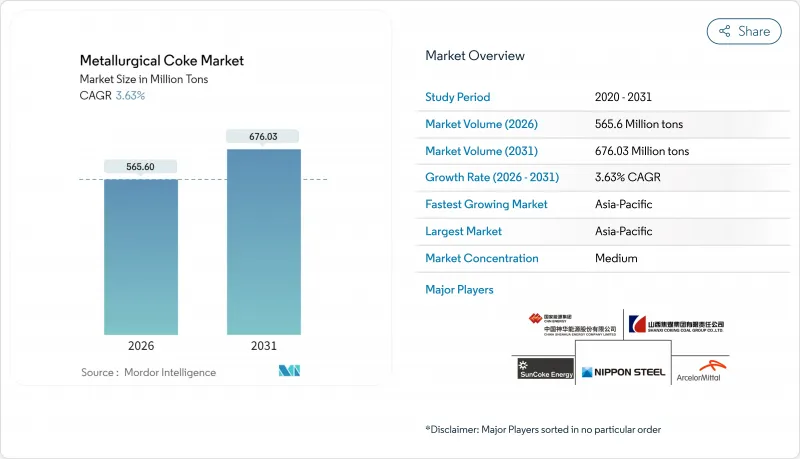

세계의 야금 코크스 시장은 2025년 5억 4,578만 톤으로 평가되었으며, 2026년 5억 6,560만 톤에서 2031년까지 6억 7,603만 톤에 이를 것으로 예측됩니다. 예측 기간 중(2026-2031년) CAGR은 3.63%로 전망됩니다.

아시아태평양에서의 철강 생산 확대, 북미의 공공 인프라 투자 안정, 통합 제철소를 단기적인 가격 변동으로부터 보호하는 장기 계약이 확대를 지원하고 있습니다. 용광로 조업은 대체제철 공정에 경제적 우위를 유지하고 있기 때문에 탈탄소화의 역풍에도 불구하고 고품질의 저회분 코크스에 대한 수요는 견조합니다. 미국 및 유럽 연합(EU)에서는 환경 규제가 강화되고 있지만, 열회수식 코크스로는 대기업이 컴플라이언스 비용을 억제하고 이익률을 확보하는 데 도움이 됩니다. 공급망의 탄력성(회복력)이 전략적으로 중요성을 늘리고 있으며, 수직 통합형 철강 제조업체는 자사 전용 코크스 생산 능력 확보를 추진하고 지리적으로 분산된 자산을 가진 공급업체를 우선하는 경향이 있습니다.

대규모 유틸리티 프로그램은 여러 해에 걸친 철강 인수 계약을 확정하고 있으며, 이는 야금 코크스 시장의 안정적인 수요에 직결됩니다. 정부 계약은 예측 가능한 주문을 보장하고 코크스 생산자가 노 가동률과 물류 계획을 최적화하는 데 도움이 됩니다. 유틸리티 기업은 경기 후퇴기에도 계속되는 경우가 많기 때문에 수요의 변동을 완화하고 공급자의 장기수익을 보호합니다. 미국과 인도와 같이 인프라 정비와 국내 철강 정책이 연동하는 지역에서는 우수한 공급망의 회복력을 누리고 있습니다. 이 협력을 통해 제철소는 프리미엄 저회분 코크스 공급을 보장하는 장기 구매 계약의 갱신을 촉진하고 있습니다.

중국, 인도, 멕시코, 동남아시아를 중심으로 자동차 생산 대수 증가는 정밀 주조용 코크스 수요를 밀어 올려 첨단 고강도 강종의 고온 처리를 촉진합니다. 전기자동차 플랫폼은 가볍고 강성이 높은 배터리 하우징이 요구되며 코크스 원료의 탄소 함량 안정성에 대한 품질 요구가 엄격해지고 있습니다. 자동차 공장의 지리적 집적은 지역 밀착형 코크스 공급 거점의 형성을 촉진하고 복합 운송망을 보유한 지역 생산자에게 비용 우위성을 가져옵니다. 자동차 제조업체가 공급망 리스크 경감을 위해 부품의 현지 생산을 진행하는 가운데, 인근의 코크스 공장에 있어서 수요 패턴은 보다 예측 가능하게 되어 있습니다. 그러나 자동차 수요의 주기성은 여전히 코크스 공급업체에게 월별 계약 할당과 스팟 시장 간에 유연하게 전환 가능한 생산 능력을 유지해야 합니다.

미국에서는 유해 대기오염물질 국가배출기준(NEPS)에 근거하여 누설 허용치의 인하가 확정되었고, 펜스라인에서의 벤젠 연속 감시와 고급 누설 감지 프로토콜이 의무화되었습니다. 유럽 연합(EU)에서는 석탄 밸류체인 전반에서 메탄 측정 및 보고를 의무화하였으며, 코크스 시설에 새로운 규정 준수 요건이 추가되었습니다. 탈황 장치, 벤젠 추출 장치 및 집진 장치에 대한 설비 투자는 생산 능력 톤당 100달러를 초과할 수 있으며 소규모 독립 생산자에게는 자금 조달이 어려운 비용입니다. 그 결과 규제 부담이 업계 재편을 가속화하고 진입 장벽을 높여 야금 코크스 시장의 성장을 억제하고 있습니다.

용광로용 코크스는 야금 코크스 시장의 63.74%를 차지하고 있습니다. 안정된 선철 생산 목표에 의해 연간 발주량은 안정되고, 프로세스 제어의 고도화에 의해 제철소가 요구하는 냉간 강도와 CSR(탄소 함유율) 사양이 향상하고 있습니다. 너트 코크스는 생산량은 적지만, 10-25mm의 정밀한 사이즈가 요구되는 주조 및 비철 금속의 이용 사례에 의해 CAGR 4.05%로 시장 전체의 성장률을 웃도는 성장을 보이고 있습니다.

통합 생산자는 노 효율을 확보하기 위해 다년간 계약으로 조달량을 확보하고 있으며, 열회수로를 가동하는 공급업체는 예측 가능한 품질로 프리미엄 가격을 획득하고 있습니다. 이 부문의 점진적인 성장은 야금 코크스 시장 전체의 기반이 되고 있으며, 환경 규제의 강화에도 불구하고 생산 능력 확대가 여전히 기존의 드럼 스탬프식 노를 중심으로 전개되는 것을 보증하고 있습니다.

저회분(회분 8-12%) 제품은 2025년 야금 코크스 시장의 70.25%를 차지했고, 노 슬래그 규제와 배출량 상한 강화를 반영하며, 2031년까지 연평균 복합 성장률(CAGR) 4.38%로 추이할 것으로 예측됩니다.

인도의 수입 제한(반기당 140만 톤을 상한으로 하는 저회분 코크스화물)은 공급 안정성에서 이 등급의 전략적 중요성을 돋보이게 합니다. 고도의 석탄 세정 및 혼합 기술에 대한 투자를 추진하는 생산자는 이 프리미엄 부문을 장악해, 대기업 제철소와의 장기 공급 계약을 확보하는데 있어 우위의 입장에 있어, 이것에 의해 야금 코크스 업계내에서의 침투를 심화시키고 있습니다.

야금 코크스 보고서는 코크스 유형(용광로 코크스, 주물 코크스 등), 등급(저회분 8-12%, 고회분 15% 이상), 용도(제철 및 제강, 주조, 제당 가공 등), 최종 사용 산업(통합제철 제조업체, 미니밀/전기로(EAF) 사업자 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다.

아시아태평양은 2025년 세계 시장의 69.10%를 차지하며 인도의 활발한 생산 능력 확대와 동남아시아 인프라 프로젝트의 지속적인 수요로 2031년까지 연평균 복합 성장률(CAGR) 3.98%를 유지할 전망입니다. 중국의 신규 석탄 기반 제철소 허가의 일시 정지는 신규 프로젝트를 억제하고 있지만 기존 제철소에서는 유지 보수 정지 및 효율화 개수 때문에 여전히 고품질 코크스의 소비가 계속되고 있습니다.

북미에서는 긴 수명 인프라 투자가 철강 주문을 안정화시키고 있습니다. 멕시코 자동차 산업 클러스터와 캐나다 천연 자원 파이프라인은 수요를 증가시키고 대륙 내 코크스 유통을 지원합니다.

유럽은 여전히 중요한 시장이며 수소 DRI 설비가 보급될 때까지 스웨덴, 독일, 프랑스에서 고품질 코크스가 필수적입니다. EU 메탄 규제 2024/1787은 새로운 감시 비용을 발생시켜 채산성이 낮은 코크스로의 폐쇄를 초래할 수 있습니다. 이로 인해 역내 공급이 핍박하고 수입 의존이 지속될 전망입니다. 브라질의 통합 제철소를 기반으로 하는 남미 신흥 그린강 허브에 지지된 중동 및 아프리카는 전통적인 고로 중심지역 이외의 사업 전개를 목표로 하는 생산자에게 다양화의 새로운 프론티어를 형성하고 있습니다.

The Metallurgical Coke Market was valued at 545.78 Million tons in 2025 and estimated to grow from 565.6 Million tons in 2026 to reach 676.03 Million tons by 2031, at a CAGR of 3.63% during the forecast period (2026-2031).

Escalating steel production in Asia Pacific, steady public-infrastructure investment in North America, and long-term contracts that shield integrated mills from short-term price swings underpin this expansion. Blast-furnace operations retain economic advantages over alternative ironmaking routes, so demand for premium low-ash coke remains firm despite decarbonization headwinds. Environmental regulation is tightening across the United States and the European Union, yet heat-recovery coke ovens help large operators contain compliance costs and safeguard margins. Supply-chain resilience is rising in strategic importance, pushing vertically integrated steel producers to secure captive coke capacity and favor suppliers with geographically diversified assets.

Large public-works programs have locked in multi-year steel offtake commitments that translate directly into steady metallurgical coke market demand. Government contracts provide predictable order books, helping coke producers optimize oven utilization rates and logistics planning. Because public projects often proceed even in downturns, they soften demand volatility and protect long-term supplier revenues. Regions with synchronized infrastructure and domestic steel policy, such as the United States and India, enjoy superior supply-chain resilience. This alignment encourages mills to renew long-term offtake agreements that secure premium low-ash coke supplies.

Vehicle output growth, particularly in China, India, Mexico, and Southeast Asia, lifts foundry coke requirements for precision castings and heats advanced high-strength steel grades. Electric-vehicle platforms demand lightweight yet rigid battery housings that intensify quality requirements for consistent carbon levels in coke feedstock. Geographic clustering of automotive plants fosters localized coke-supply hubs, giving regional producers with multimodal transport access a cost edge. As automakers localize components to mitigate supply-chain risk, demand patterns become more predictable for nearby coke plants. Nevertheless, cyclical vehicle demand still obliges coke suppliers to keep flexible capacity that can swing between monthly contract allocations and spot markets.

The United States finalized lower leak limits under the National Emission Standards for Hazardous Air Pollutants, mandating continuous benzene monitoring at fencelines and advanced leak-detection protocols. The European Union now requires methane measurement and reporting across the coal value chain, adding compliance layers for coke facilities. Capital expenditure for desulfurization, benzene extraction, and dust-capture equipment can exceed USD 100 per-ton of capacity, costs that smaller independent producers struggle to finance. Consequently, the regulatory burden accelerates industry consolidation and raises barriers to entry, moderating metallurgical coke market growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Blast-furnace varieties hold a 63.74% slice of the metallurgical coke market. Stable hot-metal production targets keep annual call-offs steady, while process-control upgrades raise the cold-strength and CSR specifications mills expect. Nut coke, though a lower-volume grade, is eclipsing aggregate growth at a 4.05% CAGR due to foundry and non-ferrous use cases that require precise 10-25 mm sizing.

Integrated producers contract multi-year volumes to safeguard furnace efficiency, so suppliers running heat-recovery ovens capture premiums for predictable quality. The segment's incremental growth continues to anchor the broader metallurgical coke market, ensuring that capacity expansions still centre on traditional drum-stamp batteries despite mounting environmental scrutiny.

Low-ash (8-12% ash) product occupied 70.25% of the metallurgical coke market in 2025 and is forecast to record a 4.38% CAGR through 2031, reflecting tighter furnace slag limits and emission caps.

Import restrictions in India that cap low-ash cargoes at 1.4 million tons per half-year underscore the grade's strategic importance for supply security. Producers investing in advanced coal washing and blending technology are best positioned to seize this premium segment and secure long-term supply agreements with large mills, thereby deepening penetration within the metallurgical coke industry.

The Metallurgical Coke Report is Segmented by Coke Type (Blast-Furnace Coke, Foundry Coke, and More), Grade (Low Ash 8 To 12% Ash and High Ash More Than 15% Ash), Application (Iron and Steel Making, Foundry Castings, Sugar Processing, and More), End-User Industry (Integrated Steel Producers, Mini-mills/EAF Operators, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Asia Pacific delivered 69.10% of global volume in 2025 and will maintain a 3.98% CAGR through 2031 owing to India's vigorous capacity build-out and ongoing demand from Southeast Asian infrastructure projects. China's moratorium on new coal-based steel permits curbs greenfield projects, yet existing furnaces still consume high-quality coke for maintenance outages and efficiency upgrades.

North America is driven by long-life infrastructure spending that stabilized steel orders. Mexico's automotive clusters and Canada's natural-resource pipelines add incremental volume and sustain intracontinental coke flows.

Europe remains significant because high-grade coke is indispensable for Sweden, Germany, and France until hydrogen DRI facilities scale. The EU Methane Regulation 2024/1787 ushers in new monitoring costs that could shutter sub-economic batteries, tightening internal supply and sustaining import dependence. South America, underpinned by Brazilian integrated mills, and the Middle-East and Africa, buoyed by emerging green-steel hubs, collectively form a diversification frontier for producers seeking exposure beyond traditional blast-furnace heartlands.