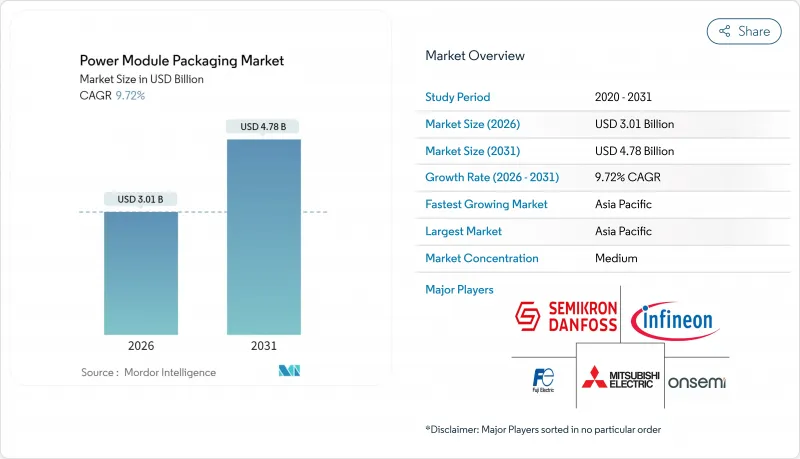

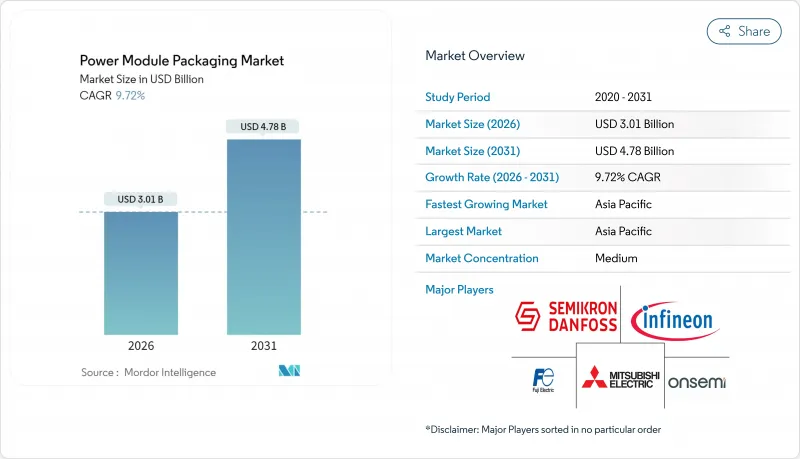

세계의 파워 모듈 패키징 시장 규모는 2026년에는 30억 1,000만 달러로 추정되고 있으며, 2025년 27억 4,000만 달러에서 성장이 예상됩니다. 2031년에는 47억 8,000만 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 9.72%로 성장할 것으로 전망됩니다.

와이드 밴드갭 반도체가 틈새 시장에서 주류 시장으로 전환되고 전기자동차가 800V 아키텍처를 채택하고 산업용 모터 구동 장치가 에너지 효율 향상을 우선시함에 따라 수요가 가속화되고 있습니다. 특히 자동차 제조업체가 수명 신뢰성을 손상시키지 않고 소형화를 요구하는 가운데, 200℃를 넘는 환경에서도 저열 저항, 고전류 밀도 및 신뢰성이 높은 동작을 실현하는 패키징 기술 혁신이 결정적인 경쟁 우위성이 되고 있습니다. 말레이시아, 인도, 인도네시아를 중심으로 한 지역 분산화는 제조 거점의 확대와 지정학적 리스크의 저감에 의해 더욱 추진력을 더하고 있습니다. SiC(탄화규소) 및 GaN(질화갈륨) 디바이스가 기존의 실리콘 솔루션에 마진 압력을 가하는 한편, 질화알루미늄 등의 첨단 세라믹 기판이 양면 냉각 설계를 가능하게 함으로써 시장 점유율을 획득해 경쟁 환경은 변화하고 있습니다.

배터리 전기자동차(BEV)에서 SiC의 침투가 진행되고 있습니다. 이는 자동차 제조업체가 항속거리 연장과 급속충전 기능을 선호하기 때문입니다. Tesla의 초기 입증 데이터는 실리콘 IGBT 대체품에 비해 약 7%의 항속거리 향상이 확인되었으며, SiC의 디바이스 비용이 높음에도 불구하고 이 벤치마크는 업계 전체의 채용 확대를 촉구했습니다. Fraunhofer의 강화형 직접 냉각 인버터 구조는 베이스 플레이트를 배제함으로써 효율을 99.5%까지 향상시키고, 패키징 기술의 진보가 구동계 성능의 향상에 직결되는 것을 실증하고 있습니다. 800V 차량 탑재 시스템으로의 전환이 확산되는 동안 절연 및 부분 방전 문제가 발생하고 있으며, 이들은 첨단 기판과 낮은 인덕턴스 연결 기술로만 해결할 수 있습니다. 이로 인해 프리미엄 모듈에 대한 수요가 증가하고 있습니다. 900V 배터리 팩을 발표하는 OEM이 증가함에 따라 SiC 다이와 양면 냉각 패키징을 결합한 공급업체는 장기적인 설계 채택을 보장하는 입장에 있습니다.

전동 모터는 세계 산업용 전력 소비량의 약 70%를 차지하고 있으며 전문가에 따르면 가변속 드라이브의 보편적 도입으로 여러 중규모 발전소 상당의 출력을 상쇄할 수 있을 것으로 추정되고 있습니다. 그러나 선진국의 3상 모터 전자속도 제어 채용률은 불과 15%로 미개척의 잠재능력이 방대하게 남아 있습니다. SiC 기반 드라이브 모듈은 컴프레서가 전체 부하에서 가동할 기회가 적은 HVAC(냉난방 공조) 등의 가변 부하 용도에 있어서 15-40%의 에너지 절약 효과를 가져옵니다. 7세대 자동차용 등급 IGBT 기술은 허용 접합 온도를 향상시켜 소형 방열판과 소형 캐비닛 설계를 가능하게 합니다. 이렇게 하면 설치 비용을 줄일 수 있습니다. 정부의 효율화 규제와 전기요금의 상승은 20년에 걸친 산업용 가동 사이클에서 신뢰성을 보장할 수 있는 고성능 패키징에 있어서 지속적인 순풍이 되고 있습니다.

SEMI의 예측에 따르면 300mm 팹 장비는 증가하는 경향이 있으며, 그 일부는 레이저 다이싱 및 하이브리드 본딩 라인과 같은 고급 패키징 장비에 할당됩니다. 와이드 밴드갭 디바이스는 250℃ 이상 프로파일에 대응할 수 있는 소결로와 ±3μm 이내의 픽 앤 플레이스 정밀도가 요구되어 신규 진입 장벽을 높이고 있습니다. EV 배터리 공장은 유사한 설비 투자 부담에 직면하고 있으며 자본 집약성이 전동화 밸류체인 전반의 체계적인 장벽임을 보여줍니다. 자금 조달 장벽은 성숙한 반도체 클러스터가 부족한 지역에서 가장 심각하게 느껴지고 남아시아와 라틴아메리카에서 다양화 목표 달성을 늦추고 단기 생산 능력 확대를 억제하고 있습니다.

기판은 2025년 수익의 27.85%를 차지했으며, 열 제어와 전기적 절연에 있어서 핵심적인 역할을 뒷받침하고 있습니다. 다이 어태치는 은 소결이나 과도적 액상 접합 기술에 의해 납계 합금을 이용하지 않는 200℃ 초과 상황에서 동작을 가능하게 해, 10.96%의 연평균 복합 성장률(CAGR)로 가장 급속한 성장이 전망되는 부품입니다. 베이스 플레이트는 열 경로를 단축하는 기판 직접 냉각 방식으로 서서히 대체됩니다. 한편, 접합부 온도를 12K 저하시키는 세라믹 봉지재는 특히 고출력 풍력 발전 컨버터에 있어서 채용 범위를 확대하고 있습니다.

구리 클립을 이용한 첨단 평면 배선 기술은 와이어 본딩의 신뢰성 약점을 없애고 전류 밀도를 향상시켜 EV 구동용 인버터의 패키지 면적을 줄입니다. 열 계면 재료는 나노구조 탄소 네트워크로 진화하여 이론저항값 0.1mm2K/W에 가까워짐으로써, 고 사이클 스트레스 하에서의 수명을 연장합니다. 기판 압착, 금속화 및 소결 부착 서비스를 수직으로 통합하는 공급업체는 OEM이 서멀 스택업 성능에 대한 단일 소스 책임을 요구하는 동안 계약을 획득했습니다. 이 종합적인 접근 방식은 저전력 소비자 분야에서 상품화 압력이 증가함에 따라 공급업체의 이익률을 보호합니다.

파워 모듈 패키지 시장에서 IGBT 모듈은 2025년 현재 36.88%의 점유율을 유지했습니다. 이것은 1200V 이하의 용도에 대해 확립된 제조 라인과 유리한 비용 곡선에 의해 지원되는 결과입니다. 그러나, SiC 모듈은 2031년까지 연평균 복합 성장률(CAGR) 10.52%로 확대되어 EV 구동계와 급속 충전기에서 뛰어난 스위칭 속도를 실현하여 전도 손실을 대폭 삭감합니다. GaN 모듈은 고주파 통신 정류기 수요 증가에 따라 성장하고 있으며, Infineon의 GaN Systems 인수가 경쟁력을 더욱 강화하고 있습니다.

Si-MOSFET 모듈은 비용에 중점을 둔 가전 및 소비자용 전원에 있어서 여전히 매력적이며, 사이리스터는 스위칭 속도보다 견고성이 우선되는 HVDC 링크나 유도 가열 분야에서 존재감을 유지하고 있습니다. 200mm SiC 웨이퍼로의 전환으로 10년 이내에 실리콘과 동등한 비용 경쟁력이 실현될 전망입니다. 그러나 자동차 등급 SiC의 수율은 대량 생산 확대의 장벽 요인으로 계속되고 있습니다. 그러므로 첨단 검사 능력과 제로 ppm 결함 목표를 제공하는 패키징 기업은 광대역 갭 반도체 팹 소유자에게 필수적인 협력자가 됩니다.

아시아태평양은 2025년 지출의 48.35%를 차지했으며 중국의 OSAT 생태계가 AI 서버와 EV의 기세로부터 혜택을 받아 CAGR 11.37%로 확대될 것으로 예측됩니다. 인도의 100억 달러 규모의 장려책과 Micron이 구자라트 주에서 8억 2,500만 달러 규모 공장 건설은 2027년까지 백엔드 생산 능력을 대폭 강화하는 정책 추진력을 보여줍니다. 말레이시아는 Intel의 70억 달러 규모 패키징 확장 계획과 Micron의 페낭 주 투자에 의해 강화되어 대만 해협 리스크를 경감할 수 있는 보완적 거점으로서의 지위를 확립하고 있습니다.

북미의 CHIPS법은 527억 달러를 계상해, 국내 공급 기반 강화를 위해 첨단 패키징을 우선합니다. Amkor의 20억 달러 규모 애리조나 공장은 2026년 가동 개시 후 AI 가속기 모듈을 생산할 예정입니다. 팹이 중요 설비용으로 현지 OSAT를 인정하는 움직임에서 지역 점유율은 완만하게 상승할 전망입니다. 유럽은 자동차용 SiC 공급망의 자립화에 주력하고 있으며, Wolfspeed는 독일에 30억 달러를 투자해 OEM의 전동화 목표에 따른 에피웨이퍼 모듈 생산 라인을 계획 중입니다. 유럽판 Chip법은 각국 지원책의 조화를 목표로 하지만, 미국 자금 규모에는 아직 미치지 못하고, 기업간의 크로스 보더 제휴 강화가 촉구되고 있습니다.

중동 및 아프리카에서는 기가와트 규모의 태양광 및 풍력발전 프로젝트를 기반으로 한 신규 사업 기회가 확대 중입니다. 이를 위해서는 그리드포밍 인버터가 필수적이며, 걸프 국가의 정부계 펀드는 경험이 풍부한 모듈 제조업체와의 합작사업을 통해 현지조립체제 구축을 추진하고 있습니다. 풍부한 재생에너지를 활용하여 미래의 수소 수출을 지원하는 기반 정비가 도모되고 있습니다.

Power Module Packaging market size in 2026 is estimated at USD 3.01 billion, growing from 2025 value of USD 2.74 billion with 2031 projections showing USD 4.78 billion, growing at 9.72% CAGR over 2026-2031.

Demand is accelerating as wide-bandgap semiconductors transition from a niche to a mainstream market, electric vehicles adopt 800V architectures, and industrial motor drives prioritize energy efficiency improvements. Packaging innovation that delivers lower thermal resistance, higher current density, and reliable operation beyond 200°C has become a decisive competitive advantage, especially as automotive OEMs demand smaller footprints without compromising lifetime reliability. Regional diversification, most notably in Malaysia, India, and Indonesia, adds further impetus by expanding the manufacturing footprint and reducing geopolitical risk. Competitive dynamics are shifting as SiC and GaN devices place legacy silicon solutions under margin pressure, while advanced ceramic substrates, such as aluminum nitride, capture market share by enabling double-sided cooling designs.

SiC penetration in battery electric vehicles is increasing as OEMs prioritize range extension and fast-charge capability. Early field data from Tesla demonstrated roughly 7% range gain over silicon IGBT alternatives, a benchmark that triggered broad industry replication despite SiC's higher device cost. Fraunhofer's Enhanced Direct-cooling Inverter architecture increased efficiency to 99.5% by eliminating baseplates, demonstrating how packaging advances directly translate into drivetrain gains. Widespread migration to 800V vehicle systems raises insulation and partial discharge challenges that only advanced substrates and low-inductance interconnects can address, thereby boosting premium module demand. As more OEMs unveil 900-V battery packs, suppliers that marry SiC dies with double-sided-cooling packaging are positioned to secure long-term design wins.

Electric motors account for approximately 70% of global industrial power consumption, and experts estimate that the universal deployment of variable-speed drives could offset the equivalent output of several mid-sized power stations. Yet only 15% of three-phase motors in developed economies employ electronic speed control, leaving vast untapped potential. SiC-based drive modules deliver 15-40% energy savings across variable-load applications such as HVAC, where compressors seldom operate at full load. Generation 7 automotive-grade IGBT technology increases the permissible junction temperature, enabling smaller heatsinks and more compact cabinet designs, which in turn lower installation costs. Governments' efficiency mandates and rising electricity prices provide a durable tailwind for high-performance packaging that can guarantee reliability over 20-year industrial duty cycles.

SEMI forecasts that 300 mm fab equipment will increase with a rising slice earmarked for advanced packaging gear such as laser dicing and hybrid-bonding lines. Wide-bandgap devices require sintering ovens capable of profiles exceeding 250 °C and pick-and-place accuracy within +-3 µm, which raises the barrier to entry for newcomers. EV battery plants face parallel capex burdens, illustrating how capital intensity is a systemic hurdle across electrification value chains. Financing obstacles are felt most acutely in regions that lack mature semiconductor clusters, slowing diversification goals and tempering near-term capacity additions in South Asia and Latin America.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Substrates captured 27.85% of 2025 revenue, underscoring their pivotal role in controlling heat and electrical isolation. Die attach is projected to post an 10.96% CAGR, the fastest component trajectory, as silver sintering and transient-liquid-phase bonding enable operation beyond 200 °C without the use of lead-based alloys. Baseplates are steadily displaced by direct-substrate-cooling schemes that collapse thermal paths, while ceramic encapsulants that pare junction temperature by 12 K widen their footprint, especially in high-power wind converters.

Advanced planar interconnects using copper clips eliminate wire-bond reliability weak points and enhance current density, thereby reducing package footprints within EV traction inverters. Thermal interface materials are evolving toward nano-structured carbon networks, nearing the theoretical resistance of 0.1 mm2K/W, which extends mission life under high-cycle stress. Suppliers that vertically integrate substrate pressing, metallization, and sintered attach services are winning contracts as OEMs demand single-source responsibility for thermal stack-up performance. The holistic approach safeguards supplier margins even as commoditization pressures intensify in lower-power consumer segments.

IGBT modules retained 36.88% of the 2025 value within the power module packaging market, buoyed by entrenched manufacturing lines and favorable cost curves for <=1200 V applications. Yet SiC modules will grow at a 10.52% CAGR through 2031, unlocking superior switching speeds and slashing conduction losses in EV drivetrains and fast chargers. GaN modules are witnessing growth in high-frequency telecom rectifier demand, with Infineon's acquisition of GaN Systems amplifying its competitive firepower.

Si-MOSFET modules remain attractive for cost-sensitive appliance and consumer power supplies, while thyristors retain relevance in HVDC links and induction heating, where ruggedness takes precedence over switching speed. The transition to 200 mm SiC wafers promises cost parity with silicon within the decade; however, automotive-grade SiC yields remain the gating factor for volume ramp. Packaging houses offering deep inspection competence and zero-ppm defect targets are, therefore, essential allies to wide-bandgap fab owners.

The Power Module Packaging Market Report is Segmented by Components (Substrate, Baseplate, Die Attach, and More), Power Device Type (IGBT Modules, Si-MOSFET Modules, and More), Power Range (< 600 V, 600 - 1200 V, 1200 - 1700 V, and More), End-User (Automotive, Industrial, and More), and Geography (North America, South America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

The Asia-Pacific region led with 48.35% of 2025 spending and is expected to compound at a 11.37% CAGR as China's OSAT ecosystem benefits from AI server and EV momentum. India's USD 10 billion incentive scheme and Micron's USD 825 million Gujarat plant underscore a policy drive that will add meaningful backend capacity by 2027. Malaysia is bolstered by Intel's USD 7 billion packaging expansion and Micron's investment in Penang, positioning the country as a complementary hub that can mitigate Taiwan Strait risk.

North America's CHIPS Act earmarks USD 52.7 billion and prioritizes advanced packaging to shore up domestic supply; Amkor's USD 2 billion Arizona site will handle AI accelerator modules when it comes online in 2026. Regional share is poised to rise modestly as fabs qualify local OSATs for critical installations. Europe focuses on automotive SiC supply-chain sovereignty, with Wolfspeed planning USD 3 billion for a German epi-wafer and module line that dovetails with OEM electrification targets. The European Chips Act aims to harmonize national incentives, yet it still lags behind U.S. funding levels, prompting companies to enhance cross-border collaboration.

The Middle East and Africa present emerging greenfield opportunities anchored in gigawatt-scale solar and wind projects that require grid-forming inverters. Gulf sovereign funds are exploring joint ventures with experienced module makers to establish local assembly, leveraging abundant renewable energy to power future hydrogen exports.