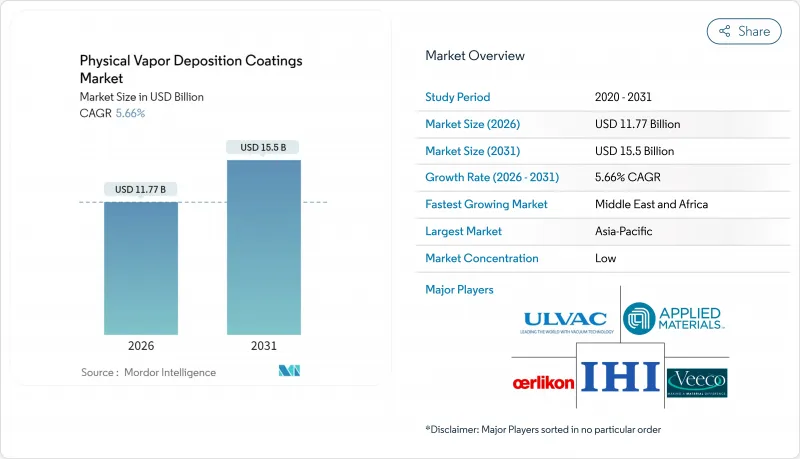

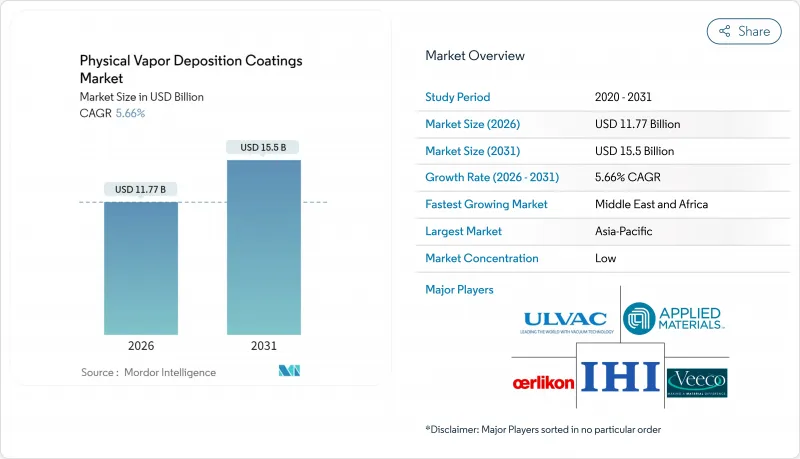

PVD(물리 증착) 코팅 시장 규모는 2026년에는 117억 7,000만 달러로 추정되고 있으며, 2025년 111억 4,000만 달러에서 성장을 계속하고 있습니다.

2031년까지는 155억 달러에 이르고, 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 5.66%로 확대될 것으로 전망됩니다.

이 성장 가속은 7nm 이하의 반도체 노드에 대한 수요 급증과 생체적합성 박막에 의존하는 저침습 의료기기의 보급 확대를 반영하고 있습니다. 6가 크롬 도금에 대한 규제 완화의 움직임과 3D 프린팅 부품의 마무리 처리의 필요성이 더하여 PVD(물리 증착)는 컴플라이언스 대응 수단인 동시에 프로세스 실현 기술로서의 지위를 확립하고 있습니다. 금속, 플라스틱, 유리 및 신흥 기판에 고밀도의 무결점 층을 형성하는 이 기술은 신규 코팅시설에 대한 견고한 설비 투자를 뒷받침합니다. 티타늄 타겟 가격의 상승과 고이온화 스퍼터링 소스의 상용화를 서두르는 장치 제조업체가 증가함에 따라 경쟁이 격화되고 있습니다.

7nm 이하의 로직 및 메모리 디바이스로의 이행이 가속하는 가운데, 서브 나노미터 정밀도로 성막되는 배리어층 및 시드층에 대한 수요가 급증하고 있습니다. 어플라이드 머티어리얼즈사가 공급하는 장치 플랫폼에서는 극단적인 종횡비에서 구리의 확산을 억제하는 몰리브덴계 인터커넥트 스택의 도입이 현저하게 증가하고 있습니다. 대만과 한국에서의 대량 도입은 초고진공 스퍼터 챔버, 첨단 티타늄 및 탄탈 타겟, in-situ 계측의 지역 공급망을 확립하고 있습니다. 미세화가 진행될수록 허용오차가 강화되어, 디바이스 제조업체는 보다 높은 이온화와 고밀도막을 실현하는 HiPIMS(고이온화 스퍼터) 소스의 통합을 요구받고 있습니다. 칩렛과 실리콘 관통 전극(TSV)을 포함한 고급 패키징 기술은 3D 집적을 위한 등각 PVD(물리 증착) 공정에 대한 지출을 더욱 밀어 올리고 있습니다.

카테터 기반 임플란트 및 정형외과용 고정기구에 대한 수요 가속화에 따라 코팅 요구 사항은 단순한 생체 적합성에서 항균성 및 뼈 결합 기능으로 고도화되고 있습니다. 마그네트론 스퍼터링법에 의한 550nm 두께의 탄탈막은 BMC 생명공학 시험에서 39.184N의 임계 접착 하중을 달성하여 코팅되지 않은 티타늄 구조를 능가하는 성능을 보였습니다. 미국 식품의약국(FDA)에 의한 규제 승인은 공정 검증 완료 후 지속적인 수익을 창출하고 미국, 독일, 아일랜드의 위탁 코팅 기업에 클린룸 격리 설비를 갖춘 전용 의료 라인의 추가를 촉구하고 있습니다. 비용 중심의 중국 및 말레이시아 의료기기 OEM 제조업체는 세계 공급망의 품질 감사를 수용하기 위해 물리 증착(PVD) 공정의 아웃소싱을 늘리고 있습니다.

12인치 클러스터 도구 1개의 가격은 클린룸 건설비와 시설 유틸리티를 제외하고 500만 달러에 달하는 것으로 나타났으며 이러한 자본 장벽에 의해 브라질, 인도네시아, 사하라 이남 아프리카에서는 신규 진입이 제한되고, 감가상각면에서 우위적인 자산을 보유한 기존 기업으로 발주가 집중되고 있습니다. 5-7년의 회수 기간과 노드 미세화에 따른 프로세스 진부화의 리스크가 자금 조달을 복잡화하고 있습니다. 인도와 베트남의 정부 인센티브 프로그램이 설비투자를 일부 상쇄하지만, 은행 계약에서는 여전히 우량 고객으로부터의 생산량 보장이 요구되고 있습니다.

HiPIMS는 70% 이상의 이온화율에 의해 절삭공구용 고밀착성 및 고밀도 코팅을 실현하여 예측 CAGR 6.92%와 가장 높은 성장률을 기록했습니다. 스퍼터링법은 2025년에 42.35%의 시장 점유율을 유지한 기반 기술이며, 마이크로일렉트로닉스에서 건축용 유리까지 대응 가능한 확장성이 높이 평가되고 있습니다. 열 증착 및 전자빔 증착은 광학 코팅의 틈새 시장을 차지하였으며, 아크 증착은 거대 입자 과제에도 불구하고 내마모성 장식 트림에 계속 사용되고 있습니다. 자동차 OEM 제조업체가 프레스 가공 공정의 공구 수명을 연장하는 질화물 레시피를 표준화함에 따라 HiPIMS은 PVD(물리 증착) 코팅 시장에서 규모를 꾸준히 확대할 것으로 예측됩니다.

장비 제조업체는 타겟의 온 더 플라이 교환을 가능하게 하는 멀티 캐소드 구성을 도입해, 레시피 전환 시간을 30% 단축하고 있습니다. 이온 주입과 이온 플레이팅은 표면 개질과 코팅 증착이 융합되는 의료용 임플란트 분야에서 인지도를 높이고 있습니다. 공정 유형의 다양화는 용도 주도의 로드맵을 따르고, 반도체 팹은 초청정 환경을, 공구 제조업체는 고에너지 이온 조사를, 가구 제조업체는 저온 장식 크롬을 각각 요구하고 있습니다.

플라스틱 기판은 현재 규모가 작지만, 저온 사이클과 플라즈마 전처리에 의한 폴리머 변형 회피에 의해 6.05%의 연평균 복합 성장률(CAGR)로 성장하고 있습니다. PVD(물리 증착) 코팅 시장에서 금속의 점유율은 60.78%로 여전히 압도적이며, 이는 확립된 공구 및 엔진 부품의 수요량을 반영하고 있습니다. 고급차용 폴리카보네이트 및 ABS 트림 부품은 전해 도금 크롬을 대체하는 스퍼터링 질화 지르코늄을 도입하여 미관과 재활용성 간의 균형을 실현하고 있습니다.

건축용 저방사(Low-E) 패널 유리의 금속화는 안정적인 수요를 유지하고 있습니다. Corning Eagle XG와 같은 특수 유리는 포토닉스 분야에서 수요가 증가하고 있습니다. 헬리콥터와 무인항공기용 복합 기판은 방위 지출에 힘입은 신흥 틈새 시장입니다. 기판의 다양화 압력은 서로 다른 열팽창 계수 하에서 코팅의 밀착성을 검증할 필요성을 야기하고 있으며, 이를 위해 현장 플라즈마 활성화 및 베이스 코트 전략에 대한 투자가 진행되고 있습니다.

아시아태평양은 2025년 대만, 한국 및 중국 본토의 반도체 투자를 원동력으로 47.40%의 점유율을 유지하였습니다. 현지 설비 보조금과 웨이퍼 제조 인센티브는 차세대 HiPIMS 및 이온화 PVD 라인에 자본을 유도하고 있습니다. 일본과 태국의 자동차 산업 거점에서는 REACH 규정에 따른 수출 요구 사항을 충족하기 위해 장식용 크롬 대체 기술이 도입되었습니다. 인도에서는 Ionbond사의 뭄바이 신규 라인이 가동되어 국내 절삭공구 제조업체의 리드 타임 단축에 기여하고 있습니다.

북미는 항공우주 및 의료기기 분야의 클러스터를 원동력으로 안정된 성장을 기록하고 있습니다. 미국의 터빈 엔진 OEM 제조업체는 1,500°C를 초과하는 연소 온도를 실현하는 다층 내열 배리어 코팅을 도입하고 있습니다. 한편 캘리포니아주의 크롬 금지침에 의해 배관금구용 저온 장식막의 도입이 가속하고 있습니다. 캐나다와 멕시코는 자동차 공구와 내식성이 요구되는 오일 샌드 채굴기 등 자동차 산업용 부품으로 공헌하고 있습니다.

유럽에서는 유해 도금을 금지하는 규제의 원동력에 의해 진전이 나타나고 있습니다. 독일은 정밀 공구 분야에서 주도적인 입장에 있으며, 스위스는 시계 부품 코팅을 전문으로 하고 북유럽 국가는 연료전지 스택 층의 선구적인 기술을 보유하고 있습니다. 2024년 11월에 가동을 시작한 Ionbond사의 스웨덴 대형센터는 스칸디나비아 지역의 생산능력을 두배로 높여 북미용 수출을 실시하는 OEM의 물류비용 절감에 기여합니다. 사우디아라비아, 아랍에미리트(UAE), 남아프리카공화국이 견인하는 신흥 지역에서는 코팅 가공된 드릴 비트, 밸브, 장식용 금속풍 마감 쇠장식이 필요한 인프라 확장을 배경으로 5.82%라는 가장 높은 CAGR을 기록하고 있습니다.

Physical Vapor Deposition Coatings market size in 2026 is estimated at USD 11.77 billion, growing from 2025 value of USD 11.14 billion with 2031 projections showing USD 15.5 billion, growing at 5.66% CAGR over 2026-2031.

This acceleration reflects demand spikes from sub-7 nm semiconductor nodes and the wider use of minimally invasive medical devices that rely on biocompatible thin films. Regulatory momentum away from hexavalent chromium electroplating, combined with the need to finish 3D-printed parts, positions physical vapor deposition as both a compliance route and a process enabler. The technology's ability to deliver dense, defect-free layers on metals, plastics, glass, and emerging substrates underpins robust capital spending on new coating centers. Competitive intensity rises as titanium target prices increase and equipment manufacturers rush to commercialize high-ionization sputter sources.

The current ramp toward sub-7 nm logic and memory devices multiplies demand for barrier and seed layers deposited with sub-nanometer precision. Equipment platforms supplied by Applied Materials reported strong uptake for molybdenum-based interconnect stacks that mitigate copper diffusion at extreme aspect ratios. Volume adoption in Taiwan and South Korea anchors regional supply chains for ultra-high-vacuum sputter chambers, advanced titanium and tantalum targets, and in-situ metrology. Each shrink node tightens tolerance bands, pushing tool makers to integrate HiPIMS sources that deliver higher ionization and denser films. Advanced packaging formats, including chiplets and through-silicon vias, further lift spending on conformal physical vapor deposition steps for 3D integration.

The accelerating demand for catheter-based implants and orthopedic fixation hardware elevates coating requirements from simple biocompatibility to antimicrobial and osteointegrative functions. Magnetron-sputtered tantalum films of 550 nm thickness achieved critical adhesion loads of 39.184 N, outperforming uncoated titanium constructs in BMC Biotechnology trials. Regulatory approvals under the US FDA (Food and Drug Administration) create durable revenue once process validation is complete, stimulating contract coaters in the United States, Germany, and Ireland to add dedicated medical lines with clean-room isolation. Cost-sensitive device OEMs (original equipment manufacturers) in China and Malaysia are increasingly outsourcing PVD (physical vapor deposition) steps to meet global supply-chain quality audits.

A single 12-inch cluster tool can cost USD 5 million, excluding clean-room build-out and facility utilities. Such capital thresholds deter new entrants in Brazil, Indonesia, and sub-Saharan Africa, consolidating orders among established players that possess depreciation-advantaged assets. Financing is complicated by five- to seven-year payback horizons and the risk of process obsolescence as node geometry evolves. Government incentive programs in India and Vietnam partially offset cap-ex, yet bank covenants still require volume guarantees from blue-chip customers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

HiPIMS recorded the highest 6.92% forecast CAGR, driven by ionization levels exceeding 70%, which yield dense coatings with superior adhesion for cutting tools. Sputter Deposition remains the bedrock, with a 42.35% market share in 2025, favored for its scalability from microelectronics to architectural glass. Thermal and e-beam evaporation occupy niche markets in optical coating, while Arc Vapor Deposition continues to be used in wear-resistant decorative trims, despite challenges from macro-particles. The physical vapor deposition coatings market size for HiPIMS is projected to climb steadily as automotive OEMs standardize on nitride recipes that extend tool life in press shops.

Equipment builders incorporate multi-cathode configurations that allow for on-the-fly target changes, reducing recipe switch-over by 30%. Ion Implantation and Ion Plating gain visibility in medical implants where surface modification and coating deposition converge. Process-type diversification aligns with an application-driven roadmap: semiconductor fabs demand ultra-clean environments, tool manufacturers prize high-energy ion bombardment, and furniture producers seek low-temperature decorative chrome.

Plastic substrates, though smaller today, are advancing at a 6.05% CAGR as low-temperature cycles and plasma pre-treatments avoid polymer deformation. The physical vapor deposition coatings market share for Metals stays dominant at 60.78%, reflecting entrenched tooling and engine component volumes. Polycarbonate and ABS trim pieces in premium cars utilize sputtered zirconium nitride to replace electroplated chrome, striking a balance between aesthetics and recyclability.

Metallization of glass for architectural low-E panels sustains steady volumes; specialty glass, such as Corning Eagle XG, sees an uptick in photonics applications. Composite substrates in helicopters and drones represent an emergent niche propelled by defense spending. Substrate diversification pressures coerce coatings to validate adhesion under disparate coefficients of thermal expansion, prompting investments in in-situ plasma activation and base-coat strategies.

The Physical Vapor Deposition Coatings Market Report is Segmented by Process Type (Sputter Deposition, E-Beam Evaporation, Hipims, and More), Substrate (Metals, Glass, and More), Material Type (Metals/Alloys, Ceramics and Oxides, and More), End User (Tools and Components), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

The Asia-Pacific region retained a 47.40% share in 2025, driven by semiconductor investments in Taiwan, South Korea, and mainland China. Local equipment subsidies and wafer-fab incentive packages channel capital into next-generation HiPIMS and ionized PVD lines. Automotive hubs in Japan and Thailand add decorative chrome alternatives to meet REACH-style export requirements. India benefits from Ionbond's new Mumbai line, which shortens lead times for domestic cutting-tool manufacturers.

North America records stable growth, driven by clusters in the aerospace and medical device sectors. US turbine-engine OEMs adopt multilayer thermal-barrier coatings that lift firing temperatures past 1,500 °C, while California's chrome ban accelerates the adoption of low-temperature decorative films on plumbing hardware. Canada and Mexico contribute to the automotive industry through components such as automotive tooling and oil-sand extraction, which demand erosion resistance.

Europe advances through regulatory tailwinds that outlaw toxic plating baths. Germany leads in precision tools, Switzerland specializes in watch component coatings, and the Nordics pioneer fuel cell stack layers. Ionbond's Swedish mega-center, opened November 2024, doubles Scandinavian capacity and reduces logistics costs for OEMs exporting to North America. Emerging regions led by Saudi Arabia, the United Arab Emirates and South Africa record the swiftest 5.82% CAGR, reflecting infrastructure expansions that rely on coated drill bits, valves and decorative metal-effect fittings.