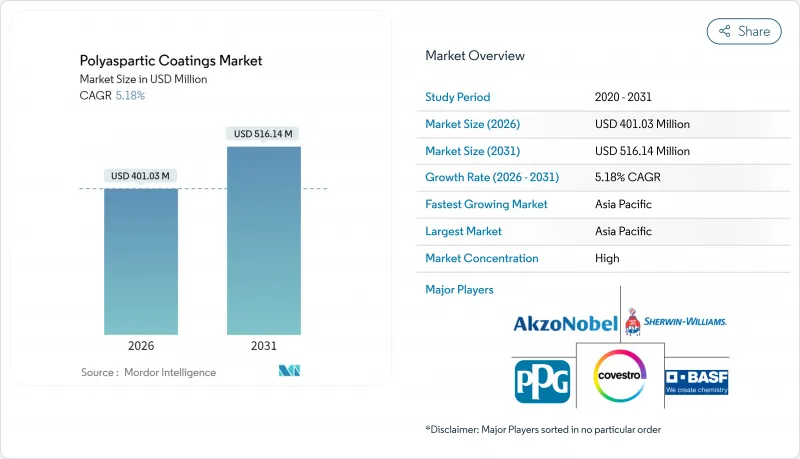

폴리아스파틱 코팅 시장은 2025년 3억 8,128만 달러로 평가되었으며, 2026년 4억 103만 달러에서 2031년까지 5억 1,614만 달러에 이를 것으로 예상됩니다.

예측 기간(2026-2031년)의 CAGR은 5.18%를 나타낼 것으로 전망됩니다.

건설업자, 제조업자, 자산 소유자가 다운타임의 삭감, 엄격화하는 대기질 규제에 대응, 수명의 연장을 실현하는 속경화·저VOC 시스템을 요구하는 움직임이 퍼지는 가운데 수요는 확대되고 있습니다. 바닥공업자는 숙련 노동자 부족을 완화하기 위해 이 기술에 의한 하루 사용 재개를 의지하고 있으며, 인프라 소유자는 갑판과 램프에서의 교통 규제를 최소화하기 위해 본 기술을 지정하고 있습니다. 수성화학제품은 용제계 시스템과의 성능차를 줄이고 있으며, 규제 준수를 간소화하기 위해 보다 신속하게 보급이 진행되고 있습니다. 아시아는 세계 소비량의 45%를 차지하며 중국과 인도의 대규모 건설과 빠른 프로젝트 리드 타임을 단축하는 지역 공급망에 견인되어 세계를 선도하고 있습니다.

유럽의 새로운 탈탄소화 규제에서는 건축자재의 VOC 함량에 상한이 설정되어 BREEAM, DGNB, EU 에코 라벨 제도에 있어서 저배출 도료가 우월합니다. ISO 준거의 배출량을 증명하는 폴리아스파틱계 도료 제조업체는 사양 선정상의 우위성을 확보할 수 있습니다. 개발자는 인증을 마케팅 자산으로 활용하여 임대료 프리미엄을 획득하기 때문입니다. 프라운호퍼 WKI와 같은 연구소가 제3자 시험을 제공하고 증명까지의 시간을 단축하고 있습니다. 그 결과 수요 증가로 수성 및 바이오 함유 등급의 수주가 증가하고, 배합 제조업체는 유럽 공장에서의 스케일 업을 가속화하고 있습니다. 다국적 기업은 점유율을 지키기 위해 기존의 용제계 제품 라인을 보다 친환경 화학 조성으로 재라벨화하고 있는 한편, 지역의 전문 제조업체는 수지 제조업체와 제휴해, 스프레이 가능한 키트를 발매하고 있습니다.

건설업자는 폴리아스파틱 수지 바닥재를 채용하고 있습니다. 이는 에폭시 수지에 비해 시공 기간을 1-2일 단축할 수 있기 때문에 고정 작업원으로 연간 시공 면적을 확대할 수 있기 때문입니다. 소유자는 고교통량의 소매·물류센터에서 15년 이상의 내용 연수를 획득할 수 있어 초기 재료비가 30-50% 높아도 평생 유지 비용을 삭감할 수 있습니다. 노동력 부족이 채용을 가속시키고 있습니다. 하루에 시공 가능한 시스템으로 귀중한 시공 요원을 조기에 다음 현장으로 돌릴 수 있기 때문입니다. 건축 설계 사무소에서는 장식 콘크리트 디자인에 폴리 아스파르트 산 탑 코트를 통합하여 미관과 내구성의 두 목표를 달성하고 있습니다. 이로 인해 창고에서 쇼핑몰, 경기장 콩코스까지 이용 사례가 확대되고 있습니다.

순수한 폴리아스파틱 코팅은 동등한 에폭시계 제품보다 30-50% 고가이며, 가격에 민감한 주택 분야에서의 보급을 제약하고 있습니다. 이 가격 차이는 비싼 아민 에스테르 원료와 엄격한 가공 공차를 반영한 것입니다. 라이프사이클 비용 모델이 없는 시공업체는 수명이 짧지만 보다 저렴한 시스템을 선택하기 쉽습니다. 이에 대해, 공급업체는 아크릴 수지나 폴리우레탄 수지를 배합한 하이브리드 제품 라인을 전개해, 속 경화성과 내자외선성을 유지하면서 정가를 15-20% 삭감합니다. 이를 통해 경험이 깊어짐에 따라 순수 등급으로의 전환 경로를 수립하고 있습니다.

2025년 시점에서 용제계 등급의 매출 점유율은 54.40%를 차지했지만, 규제 당국에 의한 VOC 상한치의 인하에 따라, 수성 제품은 기술 카테고리 중 최고의 5.78%의 연평균 복합 성장률(CAGR)을 나타냈습니다. 루브리졸의 Solsperse W60과 같은 수성 분산제는 안료 안정성을 향상시키고, 종래에는 용매계 캐리어로만 달성할 수 있었던 발색의 균일성을 실현합니다. 제조업체 각사는 탄소발자국 삭감을 위해, 바이오 유래 아민도 도입하고 있습니다. 아시아에서는 지자체의 그린 빌딩 기준이 유럽의 VOC 규제를 채용하고 있으며, 연방 규제가 없는 경제권에서도 사양 채용이 가속화되고 있습니다. 주요 건설업체는 수처리의 간편함과 낮은 악취성을 평가하고 있으며, 가동 현장에서의 봉쇄 비용 절감으로 이어져, 폴리아스파틱 코팅 시장은 병원이나 학교에서 선호되는 솔루션이 되고 있습니다.

수지 조사의 계속으로 수성계와 용제계 시스템의 기계적 특성차가 축소되고 있습니다. 코베스트로사의 INSQIN 폴리우레탄은 기존의 용매계 공정과 비교하여 공정용수 사용량을 95%, CO2 배출량을 45% 삭감합니다. 이러한 이점을 통해 페인트 공급업체는 경화 속도와 경도 외에도 환경 관련 주요 성능 지표를 호소할 수 있습니다. 그 결과, 폴리아스파틱 코팅 시장에서는 제품 계층화가 진행되고 있습니다. 비용에 중점을 둔 인테리어용으로는 엔트리 레벨 수성 하이브리드 제품, 상업용 바닥재용으로는 중위 등급의 범용 시스템, 외관 외장용으로는 프리미엄 수성 순수 등급이 전개되어 있습니다.

2025년 매출액의 69.20%는 순수계 배합이 차지했지만, 시공업자가 성능과 가격의 밸런스를 요구하기 때문에 하이브리드계 시스템은 CAGR 6.14%를 나타냈습니다. Advanced Polymer Coating의 TriFLEX DTM과 같은 제품은 폴리우레탄의 유연성과 폴리아스파라긴의 UV 내구성을 융합시켜 염수 분무와 퇴색에 견딜 수 있는 금속 직접 도장용 도료를 실현하고 있습니다. 하이브리드 제품은 온난한 기후 하에서의 대면적 시공을 용이하게 하기 때문에 개방 시간을 연장하는 경우가 많고, 순수 등급의 겔화가 빠르다는 일반적인 불만을 해소합니다.

두 번째 하이브리드 파는 폴리아스파라긴과 폴리실록산을 융합시켜 배기 가스 스택과 해양 구조물의 내열성을 향상시킵니다. 재료 과학자들은 올리고머 설계를 활용하고 경화 프로파일을 조정함으로써 다성분 장비가 아닌 표준 에어리스 펌프의 사용을 가능하게 하여 시공업체의 수용성을 확대하고 있습니다. 하이브리드 제품은 원료 비용을 갤런당 2자리 퍼센트 줄이기 때문에 폴리아스파틱 페인트 업계는 에폭시에서 스텝업 옵션으로 자리매김하여 구매자에게 가격 충격 없이 프리미엄 카테고리로의 전환을 용이하게 합니다.

폴리아스파틱 코팅 시장 보고서는 기술별(용제계, 수성계, 분체, UV경화), 유형별(순폴리아스파틱 코팅, 하이브리드 폴리아스파틱), 용도별(바닥재, 방수·방습층 등), 최종 사용자 산업별(건축 및 건설, 선박, 인프라 등), 지역별(아시아태평양, 동·아프리카·남미)

아시아태평양은 2025년 세계 수익의 44.70%를 차지했으며 2031년까지 연평균 복합 성장률(CAGR) 6.48%를 나타낼 것으로 예측됩니다. 이것은 메가 시티의 교통, 데이터센터 및 스마트 제조 클러스터에 대한 투자가 배경입니다. 중국에서는 신규 건설보다 개수로의 이행이 진행되고 급속 경화형 데크 개수 수요가 지속되고 있습니다. 한편 인도의 스마트시티 구상에서는 낮은 유지보수 도료를 지정한 보도교와 지하철역에 공적 자금이 투입되고 있습니다. 인도네시아와 베트남은 수입 의존도를 줄이는 혼합 하이브리드 페인트의 현지 공급 확대로 두 번째 성장 기지로 부상하고 있습니다.

북미 시장은 창고의 자동화, 냉장 저장 능력의 확장, 2022년에 성립된 1조 2,000억 달러 규모의 연방 인프라 계획에 의해 견인되었습니다. 교량 소유자는 이 도료의 야간 시공 후의 즉시 사용 재개 특성을 활용해, 차선 폐쇄를 최소한으로 억제하고 있습니다. 주 운수국은 이를 자산 관리 지침에 통합하고 있습니다. 상업 부동산 소유자는 영업 중단을 피하기 위해 야간 바닥 재도장을 계획하고 있으며, 이로 인해 신축 수요 감속기에도 애프터마켓 수요가 유지되고 있습니다. 계약자 인증 프로그램의 높은 채용률은 캐나다와 미국 전역에서 폴리아스파틱 코팅 시장의 확대를 가속화하고 있습니다.

유럽에서는 엄격한 대기질 규제와 성숙한 그린 빌딩 인증 제도가 수성 도료 도입의 안정된 기반을 형성하고 있습니다. 독일에서는 산업용 바닥의 개수가 지역 시장의 기반을 굳히고, 스칸디나비아에서는 엄격한 동결 융해기후하에서의 유지관리 사이클 연장을 목적으로, 목조 구조물에 폴리아스파틱막이 채용되고 있습니다. 남유럽에서는 건물의 에너지 소비 억제를 목적으로 폴리아스파틱계 바인더와 적외선 반사 안료를 조합한 쿨루프 배합이 시험 도입되고 있습니다. 동유럽 국가에서는 EU의 결속 기금의 뒷받침을 받아 엄격한 시공 기간을 단축하는 속 경화형 교량용 도료가 지정되어 시장 침투가 촉진되고 있습니다.

The Polyaspartic Coatings Market was valued at USD 381.28 million in 2025 and estimated to grow from USD 401.03 million in 2026 to reach USD 516.14 million by 2031, at a CAGR of 5.18% during the forecast period (2026-2031).

Demand is expanding as builders, manufacturers, and asset owners search for fast-curing, low-VOC systems that reduce downtime, meet tightening air-quality rules, and prolong service life. Flooring contractors rely on the technology's one-day return-to-service to mitigate skilled-labor shortages, while infrastructure owners specify it to limit traffic closures on decks and ramps. Water-borne chemistries are narrowing the performance gap with solvent-borne systems and are scaling faster because they simplify regulatory compliance. Asia leads global consumption with a 45% share, propelled by high-volume construction in China and India and by regional supply chains that shorten lead times for fast-moving projects.

Europe's new decarbonization rules cap VOC content in construction products and reward low-emission coatings within BREEAM, DGNB, and EU Ecolabel schemes. Polyaspartic suppliers that document ISO-compliant emissions secure specification advantages because developers use certifications as marketing assets to command rent premiums. Laboratories such as Fraunhofer WKI provide third-party testing, shortening time to proof. The resulting pull-through boosts orders for water-borne and bio-content grades, prompting formulators to accelerate scale-up at European plants. Multinationals re-label existing solvent-based lines with greener chemistries to defend share, while regional specialists partner with resin producers to launch ready-to-spray kits.

Builders embrace polyaspartic flooring because it cuts project schedules by one to two days over epoxy, enabling contractors to complete more square footage annually with fixed crews. Owners gain 15-plus-year service life in heavy-traffic retail and logistics centers, reducing lifetime maintenance costs even when initial material prices run 30-50% higher. Labor scarcity intensifies adoption: single-day systems free scarce applicators for the next job sooner. Architectural firms integrate polyaspartic topcoats into decorative concrete designs to meet both aesthetic and durability targets, expanding use cases from warehouses to shopping malls and stadium concourses.

Pure polyaspartic coatings cost 30-50% more than comparable epoxy, constraining penetration in price-sensitive housing segments. The premium reflects higher amine ester feedstock prices and tighter processing tolerances. Contractors without lifecycle-cost models default to cheaper systems despite shorter service life. Suppliers answer with hybrid lines that blend acrylic or polyurethane resins to shave 15-20% off list prices while retaining fast cure and UV resistance, planting a migration path toward pure grades as experience deepens.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Solvent-borne grades held a 54.40% revenue share in 2025; however, water-borne products are forecast to register a 5.78% CAGR, the highest among technology categories, as regulators impose lower VOC ceilings. Water-based dispersants such as Lubrizol's Solsperse W60 improve pigment stability, delivering color consistency once achievable only with solvent carriers. Producers also introduce bio-content amines to cut carbon footprints. In Asia, municipal green-building codes adopt European VOC limits, accelerating specification even in economies without federal mandates. Large contractors appreciate water clean-up and lower odor, which reduces containment costs on occupied sites, turning the polyaspartic coatings market into a preferred solution in hospitals and schools.

Continuous resin research has narrowed mechanical-property gaps between water-borne and solvent-borne systems. Covestro's INSQIN polyurethane reduces process-water use by 95% and CO2 emissions by 45% compared with legacy solvent routes. These gains enable coating suppliers to promote environmental key-performance indicators alongside cure speed and hardness. As a result, the polyaspartic coatings market sees tiered product ladders: entry water-borne hybrids for cost-sensitive interiors, mid-tier universal systems for commercial flooring, and premium exterior water-borne pure grades for facade cladding.

Pure formulations generated 69.20% of 2025 sales, yet hybrid systems are projected to grow at 6.14% CAGR as applicators seek balanced performance and price. Products such as Advanced Polymer Coatings' TriFLEX DTM merge polyurethane flexibility with polyaspartic UV durability to create a direct-to-metal coating that withstands salt spray and color fade. Hybrids often lengthen open time to ease large-area application in warm climates, resolving a common complaint about rapid pure-grade gel.

A second hybrid wave blends polyaspartic with polysiloxane to improve heat resistance in flue-gas stacks and offshore structures. Material scientists leverage oligomer design to tune cure profiles, enabling use of standard airless pumps instead of plural-component rigs, thus broadening contractor acceptance. Because hybrids cut raw-material cost per gallon by double-digit percentages, the polyaspartic coatings industry positions them as step-up options from epoxy, easing buyers into the premium category without sticker shock.

The Polyaspartic Coatings Market Report is Segmented by Technology (Solvent-Borne, Water-Borne, Powder, and UV-Cured), Type (Pure Polyaspartic Coatings and Hybrid Polyaspartic), Application (Flooring, Waterproofing and Moisture-Barrier, and More), End-User Industry (Building and Construction, Marine, Infrastructure, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Asia-Pacific generated 44.70% of global revenue in 2025 and is tracking a 6.48% CAGR through 2031 as megacities invest in transit, data centers, and smart manufacturing clusters. China's shift to renovation over greenfield builds sustains demand for rapid-cure deck refurbishment, while India's Smart Cities Mission channels public funds into pedestrian bridges and metro stations that specify low-maintenance coatings. Indonesia and Vietnam emerge as second-tier hotspots, aided by local suppliers scaling blended hybrids that lower import dependence.

North America's value is driven by warehouse automation, expansions in cold-storage capacity, and the USD 1.2 trillion federal infrastructure program enacted in 2022. Bridge owners exploit the chemistry's overnight return-to-service to minimize lane closures; state departments of transportation incorporate it into asset-management guidelines. Commercial real-estate owners schedule overnight floor recoats to sidestep business interruptions, which sustains aftermarket demand even during new-build slowdowns. High adoption of contractor certification programs accelerates the polyaspartic coatings market across Canada and the United States.

Europe's stringent air-quality statutes and mature green-building certification ecosystem create a stable platform for water-borne adoption. Germany anchors regional volume through industrial floor upgrades, while Scandinavia deploys polyaspartic membranes on timber structures to lengthen maintenance cycles in harsh freeze-thaw climates. Southern Europe experiments with cool-roof formulations that combine polyaspartic binders with infrared-reflective pigments to curb building energy use. Eastern European countries, encouraged by EU cohesion funds, specify rapid-cure bridge coatings to compress tight construction seasons, bolstering market penetration.