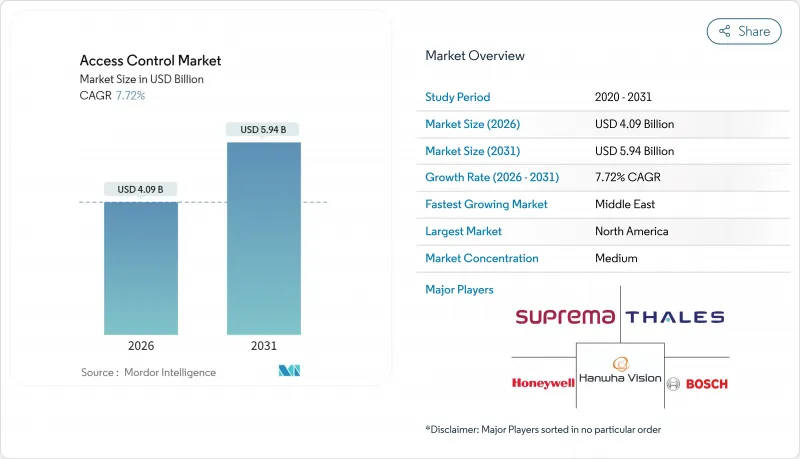

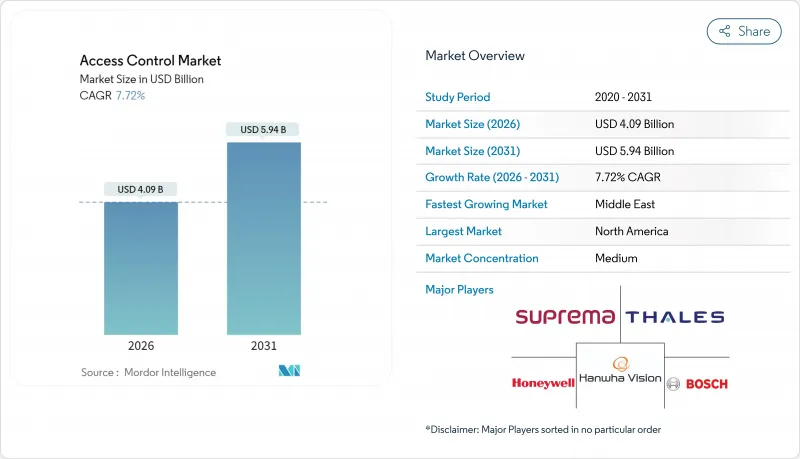

2026년 액세스 제어 시장 규모는 40억 9,000만 달러로 추정되며, 2025년 38억 달러에서 성장한 수치입니다. 2031년에는 59억 4,000만 달러에 달하고, 2026년부터 2031년에 걸쳐 CAGR 7.72%로 성장할 것으로 예측되고 있습니다.

클라우드 관리, 모바일 인증, 생체인증 기술이 기업, 공공 부문, 중요 인프라 시설에서 기존의 키와 카드를 대체함에 따라 수요가 증가하고 있습니다. 보다 엄격한 데이터 보호 규정, 비접촉식 사용자 경험에 중점을 두고 영상 감시 시스템과의 통합이 업그레이드 사이클을 가속화하고 있습니다. 반도체 부족으로 인한 가격 상승은 구매자를 소프트웨어 정의 아키텍처로 이끌고 있으며, 이를 통해 미래를 기대하는 설비 투자가 가능해지고 공급망 위험도 줄어듭니다.

2024년 10월에 발효되는 NIS2 지령에서는 모든 물리적 입구에서 다요소 인증과 변조 방지 기능이 있는 감사 추적이 의무화됩니다. 데이터센터 운영자는 암호화 및 지속적인 모니터링 조항을 충족하기 위해 기존 카드에서 생체 인증 및 모바일 인증으로의 전환을 가속화하고 있습니다. 공급업체공급망 검토를 통해 조달 기준을 인상하고 자동화된 컴플라이언스 보고 기능을 갖춘 플랫폼에 대한 수요가 증가하고 있습니다. NIS2와 GDPR(EU 개인정보보호규정)의 시너지 효과로 인해 개인 데이터를 보호하면서 물리적 보안을 강화하는 통합 솔루션에 대한 수요가 높아지고 있으며, 액세스 제어 시장 전체의 업데이트 예산이 증가하고 있습니다.

상업용 부동산 소유자는 물리적 접촉 없이 개찰기, 엘리베이터, 오피스 룸의 해제가 가능한 Apple Wallet 및 Google Pay 인증을 발행하고 있습니다. 원격 프로비저닝은 배지 발행 비용을 절감하고 유연한 좌석 정책을 실현할 수 있도록 지원합니다. 암호화된 무선 업데이트를 통해 시설 관리 팀은 분실된 단말기를 즉시 비활성화할 수 있으며 보안 강화와 임차인 경험을 향상시킬 수 있습니다. 기존의 스마트폰 인프라와의 호환성에 의해 카드 프린터 관련의 경비가 불필요하게 되어, 도입 메리트가 한층 더 높아지고 있습니다. 신속한 도입 사이클은 운영 효율성의 현저한 향상으로 이어져 액세스 제어 시장의 기세를 더욱 가속화하고 있습니다.

클라우드 호스팅 액세스 플랫폼은 NIS2를 충족하기 위해 지속적인 위협 모니터링, 보안 코드 서명 및 문서화된 개발 파이프라인을 추가해야 하며 공급업체의 운영 비용을 15-20% 증가시킵니다. 소규모 공급자는 감사 비용과 침투 테스트 비용의 흡수를 걱정하고 인증 인프라를 가진 세계 브랜드에 구매자가 집중하는 가운데 업계 재편이 일어나고 있습니다. 일부 EU 기업들은 업그레이드를 연기하고 갱신 사이클을 연장하고 있기 때문에 액세스 제어 시장의 성장 전망은 약간 둔화되고 있습니다.

2025년의 수익은 하드웨어가 61.45%의 점유율로 주도하고, 물리적 도입에 있어서의 전자정, 컨트롤러, 생체인증 리더의 필수성을 반영하고 있습니다. 대학 시설의 리뉴얼만으로, 캠퍼스가 모바일 대응 인프라로 이행하는 중에, 대폭적인 락 갱신 사이클이 촉진되었습니다. 전자정은 핸즈프리 입실을 가능하게 하는 초광대역 모듈로 가장 빠른 단위 성장을 기록했습니다. 생체인증 멀티센서 리더는 고신뢰성 인증을 요구하는 연구소나 약국에서 보급이 진행되고 있습니다.

이 소프트웨어는 2031년까지 연평균 복합 성장률(CAGR) 8.78%로 확대되어 관리 콘솔에 예측 분석 및 AI 구동형 이상 감지 기능을 추가합니다. 클라우드 제어 기반은 분산 사이트를 통합하여 실시간 정책 배포 및 자동 컴플라이언스 감사를 가능하게 합니다. 대시보드 내 영상 액세스 통합은 조사 능력을 강화하고 개방형 API는 생태계 개발을 촉진합니다. 통합 서비스와 지속적인 지원 계약은 파트너 수익을 확대하고 관리 서비스를 액세스 제어 업계에서 견고한 지속적인 수익원으로 자리매김하고 있습니다.

호스팅된 ACaaS는 2025년 도입 실적의 51.60%를 차지하며 서버 소유보다 예측 가능한 구독을 선호하는 중소기업이 견인하고 있습니다. On-Premise 솔루션과 동등한 기능 외에도 자동 업데이트를 통해 소규모 IT 부서의 기술적 부담을 줄일 수 있습니다. 상세한 임차인 포털은 코워킹 브랜드가 수천 명의 회원을 동적으로 관리할 수 있도록 지원하여 액세스 제어 시장에서 고객 충성도를 심화시킵니다.

하이브리드 ACaaS는 CAGR 8.35%에서 가장 빠르게 성장하는 모델로 규제 대상 기업을 위한 클라우드 오케스트레이션과 로컬 에지 스토리지 간의 균형을 실현합니다. 병원은 네트워크 장애 시 기밀 로그를 현장 어플라이언스로 라우팅하고 연결 복구 후 분석을 위해 클라우드와 동기화합니다. 매니지드 ACaaS는 복잡한 멀티 벤더 환경에서 맞춤형 통합이 필요한 틈새 시장을 유지하고 있지만 플랫폼은 보다 광범위한 액세스 제어 시장에서 업계를 가로질러 확장 가능한 셀프 서비스 패러다임으로 꾸준히 수렴하고 있습니다.

액세스 제어 시장은 구성요소별(하드웨어, 소프트웨어, 서비스), ACaaS 도입 형태별(호스팅, 매니지드, 하이브리드), 인증 방법별(싱글 팩터, 멀티 팩터, 모바일 인증), 접속 기술별(RFID/NFC, 스마트 카드, Bluetooth LE, UWB), 최종 사용자 업종별(상업, 산업, 정부 기관 등) 및 지역별 시장 예측은 금액(달러) 기준으로 제공됩니다.

북미는 기업 캠퍼스, 대학, 병원의 대규모 현대화를 배경으로 2025년 수익 점유율 38.30%를 유지했습니다. 켄튀르키예 대학교의 9,000 도어 전환 등 미국 고등 교육 기관의 리노베이션 사례는 액세스 제어와 출석 분석을 결합한 모바일 지원 플랫폼이 캠퍼스 전역에서 채택되었음을 보여줍니다. 캐나다의 스마트 빌딩 장려책과 멕시코의 월경 물류 시설이 수요를 끌어 올리고 있습니다. UWB(초광대역)와 생체인증 스타트업에 대한 벤처투자에 의해 이 지역은 액세스 제어 시장에서의 기술 혁신의 최전선에 위치하고 있습니다.

중동은 2031년까지 연평균 복합 성장률(CAGR) 9.22%로 가장 빠르게 성장하는 지역으로 국가 주도의 스마트 시티 구상과 보안 우선 규제 프레임워크이 견인하고 있습니다. 아랍에미리트(UAE)(UAE)과 사우디아라비아에서는 물리적 신분증을 대체하는 얼굴 인증, 홍채 인증, 지문 인증 시스템의 대규모 도입이 진행되고 있으며, 카타르와 오만에서는 전국 규모의 IoT 지령 센터에 액세스 제어 기능을 통합하고 있습니다. 현지 시스템 통합사업자는 세계 벤더의 SDK를 활용하고 지역 특화형 솔루션을 개발하여 시장 현지화를 가속화하고 있습니다.

유럽에서는 엄격한 프라이버시법 규정에도 불구하고 꾸준한 성장을 볼 수 있습니다. NIS2(네트워크 정보 보안 지령)나 EU AI법에서는 생체인증 이용시 명시적인 동의와 투명성이 요구되고 있습니다. 이에 대해, 조직은 하이브리드형 ACaaS를 채택해, 기밀성이 높은 생체 인증 템플릿을 유럽 영역 내에 유지하는 대응을 취하고 있습니다. 독일, 프랑스, 영국은 벤더 락인 회피를 위해 개방형 프로토콜 시스템을 선호하고 있으며, 북유럽 사업자는 지속 가능한 저전력 리더의 개발을 주도하고 있습니다. 동유럽의 교통 허브에서는 카드식 배리어를 모바일 인증이나 영상 인증에 의한 입퇴장 시스템으로 갱신하고 있어 이들 모두가 액세스 제어 시장의 수익 확대에 기여하고 있습니다.

The access control market size in 2026 is estimated at USD 4.09 billion, growing from 2025 value of USD 3.80 billion with 2031 projections showing USD 5.94 billion, growing at 7.72% CAGR over 2026-2031.

Demand is intensifying as cloud management, mobile credentials and biometrics replace legacy keys and cards across corporate, public-sector and critical-infrastructure facilities. Stricter data-protection regulations, the premium placed on contactless user experiences and convergence with video surveillance are reinforcing the upgrade cycle. Price escalations linked to semiconductor shortages are nudging buyers toward software-defined architectures that future-proof capital expenditure while mitigating supply-chain risk.

The NIS2 directive, effective October 2024, requires multi-factor authentication and tamper-resistant audit trails across every physical entry point. Data-center operators are accelerating migration from legacy cards to biometric or mobile credentials to meet encryption and continuous-monitoring clauses. Vendor supply-chain scrutiny raises procurement thresholds, steering demand toward platforms offering automated compliance reporting. Synergies between NIS2 and GDPR are creating a premium for unified solutions that protect personal data while enforcing physical security, lifting overall replacement budgets across the access control market.

Commercial landlords are issuing Apple Wallet and Google Pay credentials that unlock turnstiles, elevators and suites without physical interaction. Remote provisioning cuts badge issuance costs and supports flexible seating policies. Encrypted over-the-air updates let facility teams deactivate lost phones instantly, tightening security while enhancing tenant experience. The solution's compatibility with existing smartphone infrastructure eliminates card-printer overheads, strengthening its business case. Fast deployment cycles translate into visible gains in operational efficiency, reinforcing momentum for the access control market.

Cloud-hosted access platforms must add continuous threat-monitoring, secure code-signing and documented development pipelines to satisfy NIS2, lifting vendor operating costs by 15-20%. Small providers struggle to absorb audit fees and penetration-test expenses, triggering consolidation as buyers gravitate toward global brands with certified infrastructure. Some EU enterprises defer upgrades, stretching the replacement cycle, which marginally tempers the access control market growth outlook.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hardware led 2025 revenue with 61.45% share, reflecting the essential need for electronic locks, controllers and biometric readers in physical deployments. University retrofits alone drove substantial lock refresh cycles as campuses shifted to mobile-ready infrastructure. Electronic locks posted the fastest unit growth, powered by ultra-wideband modules that enable hands-free entry. Biometric multi-sensor readers gained traction in laboratories and pharmacies demanding high-assurance verification.

Software is growing at 8.78% CAGR to 2031, adding predictive analytics and AI-driven anomaly detection to management consoles. Cloud control planes unify disparate sites, allowing real-time policy pushes and automated compliance audits. Video-access convergence within dashboards strengthens investigative capabilities, while open APIs invite ecosystem development. Integration services and recurring support contracts widen partner revenue, positioning managed services as a resilient annuity layer within the access control industry.

Hosted ACaaS controlled 51.60% of 2025 deployments, driven by SMEs favoring predictable subscriptions over server ownership. Feature parity with on-prem solutions, plus automatic updates, reduces the skills burden for lean IT departments. Granular tenant portals help co-working brands manage thousands of members dynamically, deepening customer loyalty within the access control market.

Hybrid ACaaS is the fastest-growing model at 8.35% CAGR, balancing cloud orchestration with local edge storage for regulated entities. Hospitals route sensitive logs to on-site appliances during network outages, then synchronize to the cloud for analytics once connectivity returns. Managed ACaaS retains a niche for complex, multi-vendor estates needing bespoke integrations, but platforms are steadily converging toward self-service paradigms that scale across sectors in the wider access control market.

Access Control Market is Segmented by Component (Hardware, Software, Services), Acaas Deployment (Hosted, Managed, Hybrid), Authentication Method (Single-Factor, Multi-Factor, Mobile Credential), Connectivity Technology (RFID/NFC, Smart Cards, Bluetooth LE, UWB), End-User Vertical (Commercial, Industrial, Government, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America maintained 38.30% 2025 revenue share underpinned by large-scale modernizations in corporate campuses, universities and hospitals. US higher-education retrofits, such as the University of Kentucky's 9,000-door conversion, illustrate campus-wide embrace of mobile-ready platforms that blend access control with attendance analytics. Canada's smart-building incentives and Mexico's cross-border logistics facilities add incremental demand. Venture investment in UWB and biometric startups keeps the region at the forefront of technology innovation within the access control market.

The Middle East is the fastest-growing territory at 9.22% CAGR through 2031, lifted by sovereign smart-city agendas and security-first regulatory frameworks. UAE and Saudi Arabia demonstrate large-scale rollouts of facial, iris and fingerprint systems that replace physical IDs, while Qatar and Oman embed access control into nationwide IoT command centers. Local integrators build on global vendor SDKs, creating region-specific solutions that accelerate market localization.

Europe exhibits steady growth despite stringent privacy legislation. NIS2 and the EU AI Act require explicit consent and transparency for biometric use. Organizations respond by adopting hybrid ACaaS so that sensitive biometric templates remain on European soil. Germany, France and the UK prioritize open-protocol systems to avoid vendor lock-in, while Nordic operators pioneer sustainable, low-power readers. Eastern European transport hubs upgrade card-based barriers with mobile and video-verified entry, all contributing to incremental access control market revenue.