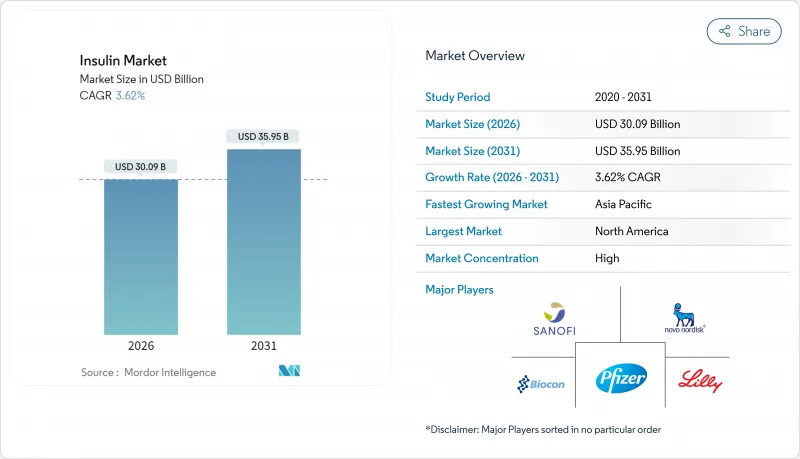

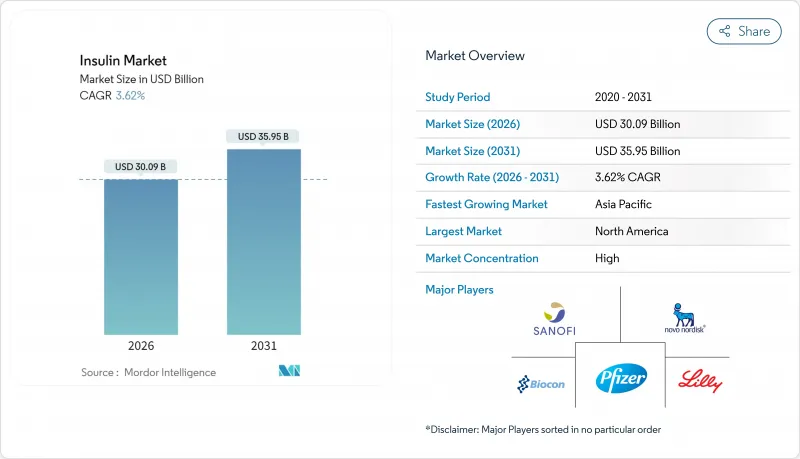

인슐린 시장은 2025년 290억 4,000만 달러로 평가되었고, 2026년에는 300억 9,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 3.62%로, 2031년까지 359억 5,000만 달러에 달할 전망입니다.

수요는 당뇨병 유병률의 꾸준한 상승, 상환 범위의 확대 및 장시간 지속적이고 비침습적인 제제에 있어서의 지속적인 혁신에 의해 지원되고 있습니다. 동시에, 바이오시밀러에 대한 접근 확대가 가격 상승을 억제하는 반면, 차세대 투여 시스템은 처방 의사와 환자 선택을 확대하고 있습니다. 인크레틴계 치료제와의 경쟁에 의해 수요는 약간 감소 경향에 있습니다만, 제조업체 각 사는 주 1회 투여의 기저 인슐린 제제, 혈당 반응형 플랫폼, 대규모 생산 능력 확장에 의해 이것을 상쇄하고 있습니다. 이러한 요인이 함께 인슐린 시장은 성숙하면서도 견고함을 유지하고 있으며, 판매량의 점증, 제품 구성의 다양화, 기술 내용의 고도화가 특징이 되고 있습니다.

세계 당뇨병 유병률은 2021년 5억 3,660만 명에서 2045년까지 7억 8,320만 명으로 46% 증가할 것으로 예측되고 있으며, 인슐린 요법의 기초 수요를 지속할 전망입니다. 중국 단독으로도 2023년에 2억 3,300만명의 사례가 보고되어 유병률은 15.9%에 육박해, 암멧 니즈의 규모를 부각하고 있습니다. 도시화, 고령화, BMI의 상승이 함께, 특히 신흥 시장에서 인슐린 의존 인구를 확대하고 있습니다. 이 시장에서 질병 진행은 고소득 국가와 유사한 경향을 보이고 있습니다. 이미 높은 BMI는 2형 당뇨병 관련 장애조정 생존년(DALY)의 절반 이상을 차지하고 있으며, 약물에 의한 혈당조절에 대한 의존이 계속되는 것을 시사하고 있습니다. 경구 당뇨병 치료제에서 기초 및 추가 요법(베이스 및 볼루스 요법)으로의 임상 전환은 대체 요법이 초기 단계의 환자를 얻는 동안 인슐린 사용량 증가를 보장합니다.

각국에서 전개되는 캠페인으로 진단과 치료 개시가 가속화되고 있습니다. 중국의 '전국 수량 집중 조달'에 의한 인슐린 일괄 입찰은 가격을 낮추면서 공립 병원 전체에서의 치료 보급을 촉진했습니다. 인도의 바이오시밀러 인슐린 도입 시책은 입증된 동등성을 가진 대체가능한 제품을 우선시함으로써 정책이 경제적 장벽을 해소할 수 있음을 보여줍니다. WHO의 사전 인증 과정은 품질 보증된 인슐린 선택의 폭을 넓히고 저소득 및 중소득국에 검증된 조달 경로를 제공합니다. 이러한 프로그램은 선순환을 생성합니다. 조기 발견은 처방량을 증가시키고, 그것이 규모의 경제와 추가 가격 하락을 촉진하고, 환자의 접근 확대로 이어집니다.

복잡하고 비용이 많이 드는 승인 프로세스는 새로운 인슐린 및 바이오시밀러 시장 진입을 지연시킵니다. 미국 FDA가 2024년에 발행한 인슐린 이코덱에 대한 완전한 답변은 제조 공정의 검증 부족을 지적하고, 후기 개발 단계의 제품조차도 정체될 가능성을 나타냈습니다. 바이오시밀러 개발 기업은 여전히 분자당 미화 1억 달러를 넘는 엄청난 비용을 요구하는 비교 임상시험 프로그램을 시행해야 하며, 이는 중소기업에게 과도한 장벽이 되고 있습니다. WHO의 세계 사전 인증은 다양한 집단에서 추가적인 생물학적 동등성 데이터를 요구하고, 또한 타임라인을 연장합니다. 그 결과, 여러 관할 구역에 걸친 품질 요건을 탐색할 수 있는 기존 기업에 시장 지배력이 집중된 채로 단기적으로는 가격 경쟁과 환자의 선택이 제한되게 됩니다.

2025년 시점에서 장시간 작용형 아날로그 제제는 인슐린 시장 점유율의 45.92%를 차지하며, 모든 당뇨병 유형에 있어서의 기초요법의 기반이 되고 있습니다. 주 1회 투여 제형의 지속적인 보급으로 이 범주의 환자 편의성은 더욱 높아질 전망입니다. 속효형 및 프리믹스 부문은 FDA 최초의 승인 바이오시밀러인 메리로그(Merilog)와 커스티(Kirsty)에 의한 온화한 경쟁이 발생하고 있으며, 미국 840만명의 인슐린 사용자에 대한 액세스 확대를 도모하고 있습니다. 한편, 초속효형 흡입제제는 바늘을 사용하지 않는 투여법에 대한 사용자의 취향에 힘입어 2031년까지 연평균 복합 성장률(CAGR) 5.18%로 성장을 견인할 것으로 예측되고 있습니다. 이중 지속성 화학을 모색하는 파이프라인 프로그램은 향후 주사 빈도를 월1회로 줄이고 복약 준수율을 향상시키고 경쟁 압력에도 불구하고 기초 요법 제품의 지속적인 중요성을 포착할 수 있습니다.

이와 병행하여, 혈당에 반응하는 조사는 생체활성을 실시간으로 조절하는 「스마트」인슐린의 개발로 진전하고 있어 저혈당증의 발생을 거의 근절할 가능성을 지니고 있습니다. 바이오시밀러의 활동은 여전히 유럽에서 가장 활발하며, 합리화된 입찰 시스템이 제조 효율을 높이는 공급업체에게 보상하는 구조가 되고 있습니다. 이러한 경쟁과 장치 업그레이드가 결합되어 가치 창출은 분자 차별화에서 제제와 장치의 통합 생태계로 꾸준히 전환하고 있습니다.

북미는 2025년 견고한 보험 적용 범위와 프리미엄 아날로그의 조기 채택으로 세계 수익의 41.78%를 차지했습니다. 그러나 메디케어의 자기부담 상한액 35달러는 제조업자의 가격 설정 폭을 좁히고 있으며, 업무 효율화와 차별화된 가치 제안이 요구되고 있습니다. 미국의 생산 능력 확장(노보놀디스크사의 41억 달러 규모 노스캐롤라이나 공장, 엘라이 릴리사의 90억 달러 규모 인디애나 복합시설)은 단기적인 바이오시밀러와 GLP-1 경쟁의 존재에도 불구하고 장기적인 시장에 대한 확신을 보여주고 있습니다. 한편 캐나다에서는 동물 유래 제품의 단계적 폐지와 현대적인 아날로그 제품의 채택이 진행되어, 북미가 고순도 재조합 공급원으로 전환하고 있는 것을 뒷받침하고 있습니다.

유럽은 성숙하면서도 활기찬 시장이며, 바이오시밀러의 침투와 가치 기반의 구매가 가격 억제를 촉진하고 있습니다. 바이오시밀러 진입 후 28개국에서 인슐린 글라긴의 평균 가격이 20% 이상 하락하여 지급자의 협상력을 보였습니다. 주 단위 기저 인슐린 "아위크리(이코덱)"의 승인과 AID 시스템의 CE 마크 확대는 차세대 치료법의 조기 실증의 장소로서 같은 지역의 위치를 명확히 하고 있습니다. 그러나 2025년 피어스프 펌프 카트 부족으로 대표되는 공급망의 혼란은 특수 카트리지 형식의 취약성을 드러내고 제조 거점의 다양화의 필요성을 돋보이게 하고 있습니다. 바이오시밀러의 규제 간소화가 실현되면 개발 사이클의 단축과 2026년 이후의 경쟁 격화가 예상됩니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 4.43%로 가장 빠르게 성장할 지역으로, 당뇨병 이환율 상승, 도시형 라이프스타일로의 이행, 정책 주도의 가격 억제책이 이를 견인하고 있습니다. 중국의 수량 기준 조달 시스템은 전국 입찰에서 인슐린 가격을 최대 48% 낮추고 수백만 명의 신규 사용자에 대한 액세스를 확대했습니다. 인도는 국내 바이오시밀러 생산 능력을 활용하여 기존 아날로그 제품으로 충분한 공급을 얻을 수 없었던 지방 지역을 커버하고 있습니다. 다국적기업은 사노피의 베이징복합시설과 노보놀디스크의 천진확장계획에서 볼 수 있듯이 현지에서의 충전 및 포장 제휴와 신규 공장 건설을 조합하여 성장 클러스터에 가까운 공급 거점을 확립하고 있습니다. 콜드체인 인프라의 부족과 지역 간의 상환 격차는 과제로 남는 것, 물류 전문 기업이나 원격 의료 플랫폼에 있어서의 기회도 낳고 있습니다.

The insulin market is expected to grow from USD 29.04 billion in 2025 to USD 30.09 billion in 2026 and is forecast to reach USD 35.95 billion by 2031 at 3.62% CAGR over 2026-2031.

Demand is anchored by the steady rise in diabetes prevalence, expanding reimbursement coverage, and continuous innovation in long-acting and non-invasive formulations. At the same time, widening access to biosimilars is tempering price growth, while next-generation delivery systems are expanding prescriber and patient options. Competition from incretin-based therapies is siphoning demand at the margin, yet manufacturers are counter-balancing through weekly basal products, glucose-responsive platforms, and large-scale capacity expansions. Collectively, these forces point to a maturing yet resilient insulin market characterized by incremental volume gains, richer product mix, and heightened technology content.

Global diabetes prevalence is projected to rise from 536.6 million in 2021 to 783.2 million by 2045, a 46% surge that sustains baseline demand for insulin therapies. China alone reported 233 million cases in 2023 with prevalence approaching 15.9%, underscoring the scale of unmet need. Urbanization, aging, and rising BMI collectively widen the insulin-dependent population, especially in emerging markets where disease progression increasingly mirrors that of high-income countries. High BMI already accounts for over half of Type 2 diabetes-related disability-adjusted life years, signaling continued reliance on pharmacologic glucose control. The clinical transition from oral antidiabetics to basal-bolus regimens ensures insulin volume growth even as alternative therapies capture early-stage patients.

National campaigns are accelerating diagnosis and therapy initiation. China's National Volume-Based Procurement centralized insulin bidding, cutting prices while boosting treatment uptake across public hospitals. India's biosimilar insulin adoption initiatives similarly demonstrate how policy can close affordability gaps by favoring interchangeable products with proven equivalence. The WHO pre-qualification pathway is widening the pool of quality-assured insulin options, giving low- and middle-income countries a validated procurement channel. Such programs create virtuous cycles: earlier detection raises prescribing volumes, which then reinforce economies of scale and further price erosion, broadening patient access.

Complex, high-cost approval pathways delay market entry for novel and biosimilar insulins. The U.S. FDA's 2024 complete response letter on insulin icodec highlighted manufacturing validation gaps that can stall even late-stage assets. Biosimilar developers must still undertake extensive comparative clinical programs costing over USD 100 million per molecule, a hurdle disproportionate to smaller firms. The WHO's global pre-qualification demands additional bioequivalence data across diverse populations, further stretching timelines. As a result, market power remains concentrated among incumbents able to navigate multi-jurisdictional quality requirements, limiting price competition and patient choice in the near term.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Long-acting analogs held 45.92% of insulin market share in 2025, serving as the backbone of basal therapy across diabetes types. Continued penetration of once-weekly options promises to strengthen the category's patient convenience appeal. Rapid-acting and premix segments face modest price competition from the first FDA-approved biosimilars Merilog and Kirsty, broadening access for the 8.4 million U.S. insulin users. Meanwhile, ultra-rapid inhalable formulations are projected to lead growth at a 5.18% CAGR through 2031, driven by user preference for needle-free dosing. Pipeline programs exploring dual-protraction chemistry could eventually trim injection frequency to monthly intervals, enhancing adherence and positioning basal products for sustained relevance despite competitive pressures.

In tandem, glucose-responsive research is advancing towards "smart" insulin that modulates bioactivity in real time, holding the potential to all but eliminate hypoglycemia events. Biosimilar activity remains most intense in Europe, where streamlined tender systems reward suppliers that raise manufacturing efficiency. Such competition, coupled with device upgrades, is steadily shifting value creation from molecule differentiation toward combined formulation-device ecosystems.

The Insulin Market Report is Segmented by Product Type (Rapid-Acting, Long-Acting, Combination/Premix, Biosimilar, Other), Application (Type 1 Diabetes, Type 2 Diabetes), Delivery Device (Pens, Pump Reservoirs, Vials & Syringes, Jet/Patch/Inhalers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America sustained a 41.78% share of global revenue in 2025, benefiting from robust insurance coverage and early adoption of premium analogs. The USD 35 Medicare copay ceiling, however, is narrowing manufacturers' pricing latitude, compelling operational efficiencies and differentiated value propositions. U.S. capacity expansions-Novo Nordisk's USD 4.1 billion North Carolina plant and Eli Lilly's USD 9 billion Indiana complex-underline long-term confidence despite nearer-term biosimilar and GLP-1 competition. Canada, meanwhile, is phasing out animal-sourced products in favor of modern analogs, underscoring North America's pivot to high-purity recombinant supply.

Europe remains a mature yet dynamic market where biosimilar penetration and value-based purchasing foster disciplined price trajectories. After biosimilar entry, average insulin glargine prices declined more than 20% across 28 countries, illustrating payers' negotiation leverage. Weekly basal approvals such as Awiqli (icodec) and expanded CE markings for AID systems position the region as an early proving ground for next-generation therapies. Still, supply chain hiccups-Fiasp PumpCart shortages in 2025-expose vulnerabilities in specialized cartridge formats and highlight the need for diversified manufacturing nodes. Prospective regulatory streamlining for biosimilars could shorten development cycles and raise competitive intensity post-2026.

Asia-Pacific is the fastest-growing geography at a 4.43% CAGR through 2031, propelled by escalating diabetes incidence, urban lifestyle shifts, and policy-driven affordability gains. China's Volume-Based Procurement has cut insulin prices by as much as 48% in nationwide tenders, expanding access to millions of new users. India is leveraging domestic biosimilar capacity to cover rural districts previously underserved by analog products. Multinational firms are pairing local fill-finish alliances with greenfield builds, as evidenced by Sanofi's Beijing complex and Novo Nordisk's Tianjin expansion, to anchor supply close to growth clusters. Cold-chain infrastructure gaps and regional reimbursement disparity remain challenges, yet they also create openings for logistics specialists and telehealth platforms.