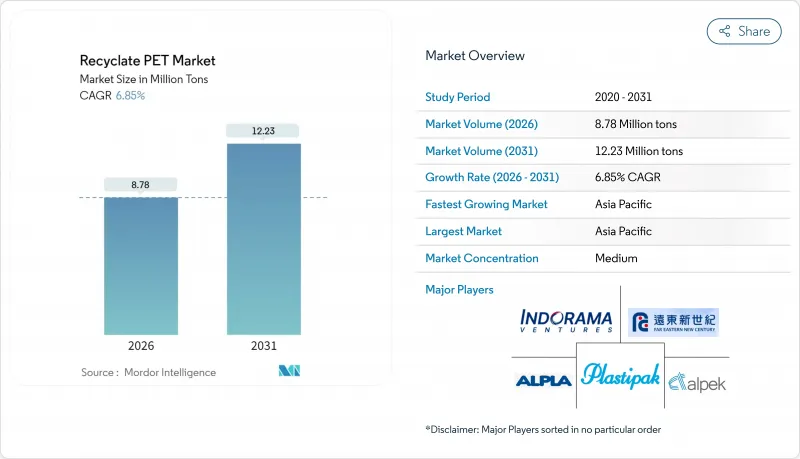

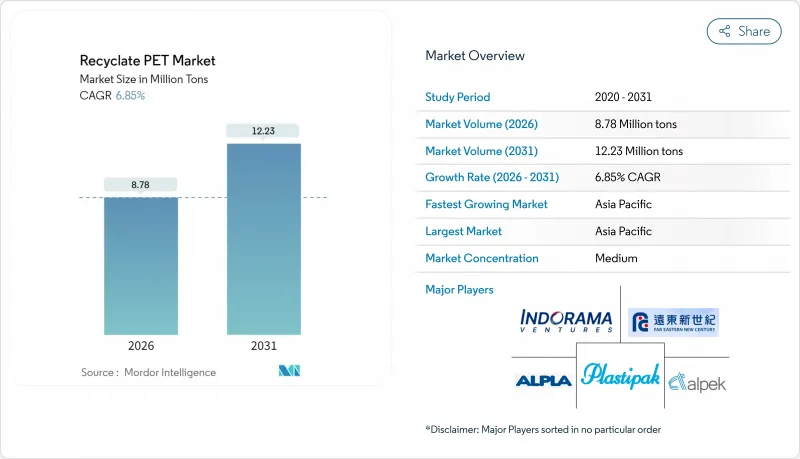

PET 재활용 시장은 2025년 822만 톤에서 2026년에 878만 톤으로 성장하고 2026년에서 2031년에 걸쳐 CAGR 6.85%로 성장하여 2031년까지 1,223만 톤에 달할 것으로 예측되고 있습니다.

규제 요건, 브랜드 소유자의 조달 목표 상승, 버진 수지와 재생 수지의 비용 수렴이 결합되어 PET 재활용 시장에서 구조적인 수요 변화를 추진하고 있습니다. 유럽에서는 병에서 병으로의 순환성이 법적으로 의무화되고 있으며, 미국에서는 2024년부터 2025년 초에 걸쳐 12개 주가 확대 생산자 책임(EPR)법을 도입하여 회수 및 재생재 사용 의무를 강화하고 있습니다. 아시아태평양의 성장은 중국의 2025년을 위한 재생재 35% 의무화와 인도의 2024년 플라스틱 폐기물 관리 개정 규칙에 근거한 단계적 EPR 도입을 배경으로 가속하고 있습니다. 효소분해 및 용제분해 기술의 발전에 의해 다운사이클되고 있던 유색 및 불투명 원료로부터 식품 그레이드 제품을 생산 가능하게 되어, 소비 후 자원의 적용 범위가 확대되고 있습니다. 경쟁 환경은 변화하고 있습니다. 통합형 석유화학 대기업은 기계적 처리 능력과 화학적 처리 능력 모두에서 사업 리스크를 헤지하는 한편, 폐기물 관리 사업자는 선별 및 세정 라인을 추가해, 밸류 체인 전체에서의 이익 획득을 도모하고 있습니다.

유럽연합(EU)의 포장 및 포장 폐기물 규제에서는 PET음료병에 대해 2025년까지 25%, 2030년까지 30%라는 구속력이 있는 재생재 함유율 기준을 설정하여 자발적인 서약을 법적 요건으로 전환하였습니다. 미국에서는 현재 12개 주가 EPR(확대생산자책임)법을 실시하고 최저재생재 함유율을 의무화하고 있으며, 캘리포니아주 SB54법이 선도역으로서 2030년까지 50%로 인상을 정하고 있습니다. 중국 국가발전개혁위원회는 2025년 1월 시행의 35% 재생재 사용 의무를 발표하여 기존 수출 루트로 흐르고 있던 국내 플레이크의 목적지를 변경시켰습니다. 인도의 개정 플라스틱 폐기물 관리 규칙에서는 브랜드 소유자가 연간 플라스틱 사용량과 동등한 회수 및 리사이클 활동을 의무화해 회수 자산의 수익화를 도모하고 있습니다. 이러한 규제는 종합적으로 법적 보증을 받은 오프테이크를 창출하고, PET 재활용 시장에서 기계 및 화학적 처리 능력에 대한 자본 투입을 지원하고 있습니다.

코카콜라, 펩시코, 유니레버, 네슬레, 다논 등 세계의 음료 및 소비재 대기업은 2030년까지 PET 원료의 25-50%를 재생재로 조달하는 것을 공약하고 있으며, 현행 포장량으로는 연간 약 200만톤의 추가 수요가 전망됩니다. 코카콜라의 2024년 지속가능성 보고서에 따르면, 회사의 병에는 23%의 재활용 소재가 사용되고 있으며, 인드라마 벤처스사 및 루프 인더스트리즈사와의 여러 해에 걸친 오프 테이크 계약에 의해 2028년까지 식품 등급의 플레이크를 확보하고 있습니다. 펩시코사와 카본라이트사의 합작사업에서는 2026년부터 텍사스주에서 연간 6만 톤의 병투병 수지를 공급 개시하여 안정공급과 스팟 시장의 변동 리스크 경감을 도모합니다. 유니레버는 지속가능한 포장에 10억 파운드를 할당하고 브랜드 목표 달성을 위해 화학 PET 재활용에 상당액을 충당했습니다. 이러한 구속력 있는 계약은 수익의 확실성을 제공하고 신공장의 자금 조달 위험을 줄이고 PET 재활용 시장 전반에 걸쳐 확장 계획을 가속화합니다.

인도, 인도네시아, 나이지리아, 브라질의 회수율은 20%에서 40%의 범위이며, 독일의 보증금 반환 제도에서 달성된 90%를 크게 밑돌고 있습니다. 비공식 폐기물 수집 네트워크가 주류이지만 픽업 및 품질 관리 프로세스가 부족하기 때문에 15% 이상의 오염을 포함한 베일이 생겨 식품 등급 기준을 충족하지 못합니다. 인도네시아에서는 도시의 폐기물 처리 커버율이 40%에 머물기 때문에 재활용 업자는 재선별에 추가 비용을 필요로 하고 기계 가동률이 저하하고 있습니다. 나이지리아에서는 새로운 EPR 제도가 시행되지 않기 때문에 예금제도의 기반 정비가 자금 부족에 빠져 원료가 수출로 흐르고 있습니다. 브라질에서는 역물류의 자원 부족으로 인해 2024년 병 회수율은 25%에 그쳐 포장 가공업자로부터의 강한 수요에도 불구하고 국내 공급이 제한되고 있습니다.

PET 재활용 시장에서 2025년 생산량 중 PET 단섬유가 41.20%를 차지했습니다. 이 부문은 의류 산업의 스코프 3 배출 감소 목표를 배경으로 2031년까지 연평균 복합 성장률(CAGR)7.05%로 확대될 것으로 예측됩니다. H&M, Inditex, Nike 등 브랜드로부터의 조달 확약을 배경으로, 단섬유용 PET 재활용 시장 규모는 동기간에 한층 더 140만 톤의 확대가 전망됩니다. 이 브랜드는 퍼 이스트 뉴 센추리 사 및 강소 중원사와 공급 계약을 체결하고 있으며 포장재 부족이 심화되는 환경에서도 섬유의 안정 조달을 확보하고 있습니다. 기계적 재활용업체는 병 용도보다 점도 요건이 엄격하지 않기 때문에 저품질 원료의 혼입이 가능한 단섬유를 선호합니다.

2025년 시점에서 식품용 및 비식품용을 포함한 PET병이 총량의 35.00%를 차지했습니다. 식품용 병 수지의 신장이 보다 현저한 것은 유럽 및 북미에서 2030년까지 재생재 25-30% 사용이 의무지어져, 프리미엄 가격과 장기 계약이 촉진되고 있기 때문입니다. PET 시트 및 필름 수요는 재생재 함유를 중시하는 의약품 및 전자 기기 열성형 포장이 견인하고 있습니다. PET 스트랩은 버진 폴리프로필렌과의 경쟁에 직면하고 있으며, 예금제도가 도입된 유럽 시장 이외의 이익률이 압박되고 있습니다. 엔지니어링 수지를 포함한 기타 특수 제품 유형은 자동차 제조업체가 비하중 부품에 대한 PET 재활용 채택을 시험적으로 진행하고 있기 때문에 꾸준히 성장하고 있습니다.

본 리사이클 PET 시장 보고서는 제품 유형(PET 단섬유, PET 스트랩, PET 시트 또는 필름, 식품용 PET 병, 비식품용 PET 병, 기타 제품 유형), 용도(포장, 공업용 실, 건축자재, 기타 용도), 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분석했습니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

아시아태평양은 2025년 수량의 42.85%를 차지하며, 2031년까지 8.05%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예측되며, PET 재활용 시장에서 가장 빠른 지역 성장 궤도를 나타냅니다. 중국에서는 2025년 시행의 재생재 35% 함유 의무로 수출용 생산능력이 국내 보틀러용으로 전환되어 베일 경쟁이 격화되고 플레이크 가격이 상승하고 있습니다. 인도의 EPR 제도에서는 2024년에 1,200개의 재활용업체 인증이 공식화되어 비식품 등급에서 식품 등급으로의 생산 능력 향상이 촉진되었습니다. 일본은 플라스틱 자원 순환법을 연장하여 2030년까지 50%의 재활용 소재 사용을 규정했습니다. 이에 따라 산토리와 아사히는 10년에 걸친 오프테이크 계약을 체결했습니다. 베트남, 인도네시아 등 동남아시아 시장에서는 수집 인프라 정비를 위한 다자간 대출이 유치되고 있지만, 발생원분별이 한정적이기 때문에 베일의 품질은 여전히 불안정합니다.

유럽은 보증금 반환 제도로 90% 이상의 회수율을 달성하는 확립된 거점으로 고품질 원료의 안정 공급을 확보하고 있습니다. 독일의 보증금 제도는 2024년 병의 98%를 회수하여 62만 톤의 기계 처리 능력을 지원했습니다. 스페인과 이탈리아는 각각 2025년, 2026년에 보증금 반환 제도를 도입하고 EU 지역 내의 재생재 함량 요건을 통일함으로써 국가 간 투자를 촉진합니다. 프랑스와 네덜란드의 화학적 재활용 설비가 확대됨에 따라 식품 등급의 고품질 제품이 150,000톤 증가하여 기계 처리량이 아닌 고도의 재활용 분야로의 성장 변화가 진행되고 있습니다.

북미는 주마다의 규제에 의해 진척 상황에 편차가 있습니다만, 꾸준히 발전하고 있습니다. 캘리포니아주, 오레곤주, 메인주, 콜로라도주, 뉴저지주에서는 음료 용기에 15-50%의 재활용 소재 사용을 의무화하는 법률이 제정되어 펩시코와 카본라이트, 인드라마와 루프 등의 합작사업이 추진되고 있습니다. 캐나다의 연방 플라스틱 등록 제도는 전국적인 투명성을 가져오고, 멕시코의 2024년 법은 PET병에 EPR을 도입했습니다. 이로 인해 알펙은 토르카 공장을 식품 등급 생산을 위해 개조했습니다. 미국에서는 연방 수준의 불통일이 컴플라이언스의 복잡화를 초래하는 반면, 여러 주를 중앙 집중식 시설에서 서비스하는 지역 허브의 형성을 촉진하고 있습니다.

The recyclate PET market is expected to grow from 8.22 million tons in 2025 to 8.78 million tons in 2026 and is forecast to reach 12.23 million tons by 2031 at 6.85% CAGR over 2026-2031.

Regulatory mandates, rising brand-owner procurement targets, and cost convergence between virgin and recycled resin are jointly propelling structural demand shifts in the recyclate PET market. In Europe, bottle-to-bottle circularity is now embedded in law, while 12 U.S. states adopted Extended Producer Responsibility (EPR) statutes between 2024 and early 2025, reinforcing collection and recycled-content obligations. Asia-Pacific growth is accelerating on the back of China's 35% recycled-content mandate for 2025 and India's staged EPR roll-out under the 2024 Plastic Waste Management Amendment Rules. Parallel advances in enzymatic and solvent-based depolymerization enable food-grade output from formerly downcycled colored and opaque feedstock, thereby widening the addressable pool of post-consumer materials. Competitive dynamics are shifting as integrated petrochemical majors hedge their operations with both mechanical and chemical capacity, while waste-management operators add sorting and washing lines to capture margins across the value chain.

The European Union's Packaging and Packaging Waste Regulation sets binding recycled-content thresholds of 25% in 2025 and 30% in 2030 for PET beverage bottles, effectively turning voluntary pledges into legal requirements. Twelve U.S. states now enforce EPR statutes that impose minimum recycled content, with California's SB 54 leading the way, which increases to 50% by 2030. China's National Development and Reform Commission issued a 35% recycled-content mandate effective January 2025, redirecting domestic flake that formerly entered export channels. India's amended Plastic Waste Management Rules require brand owners to match their annual plastic footprints with equivalent collection and recycling efforts, thereby monetizing their collection assets. Collectively, these mandates create a legally guaranteed offtake, underpinning capital deployment in both mechanical and chemical capacity across the recyclate PET market.

Global beverage and consumer-goods majors, including Coca-Cola, PepsiCo, Unilever, Nestle, and Danone, have pledged to source 25-50% of their PET from recycled materials by 2030, resulting in approximately 2 million tons of incremental demand annually at current packaging volumes. Coca-Cola's 2024 sustainability report shows 23% recycled content in its bottles and details multi-year offtake with Indorama Ventures and Loop Industries to secure food-grade flake through 2028. PepsiCo's joint venture with CarbonLite will deliver 60,000 tons per year of bottle-to-bottle resin in Texas starting in 2026, securing supply and mitigating spot-market volatility. Unilever earmarked GBP 1 billion for sustainable packaging, with a sizable allocation for chemical-recycled PET to meet branding goals. These binding contracts provide revenue certainty, derisking new plant financing, and accelerating expansion plans across the recyclate PET market.

Collection rates in India, Indonesia, Nigeria, and Brazil range from 20% to 40%, far below the 90% achieved in German deposit-return systems. Informal waste-picker networks dominate, yet they lack aggregation and quality control processes, resulting in bales with more than 15% contamination that fail to meet food-grade standards. Indonesia's municipal waste coverage spans only 40% of urban zones, forcing recyclers to spend more on re-sorting and thus curbing machine utilization. Nigeria's nascent EPR scheme remains unenforced, leaving deposit infrastructure unfunded and feedstock redirected to export. Brazil's under-resourced reverse logistics collected only 25% of bottles in 2024, limiting local supply despite strong demand from packaging converters.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

PET staple fiber accounted for 41.20% of the 2025 volume in the recyclate PET market. The segment is expected to grow at a 7.05% CAGR through 2031, driven by apparel-sector Scope 3 reduction goals. The recyclate PET market size for staple fiber is forecast to expand by an additional 1.4 million tons over the period, underpinned by sourcing commitments from H&M, Inditex, and Nike. These brands have locked supply contracts with Far Eastern New Century and Jiangsu Zhongyuan, ensuring fiber offtake in a tightening bale environment. Mechanical recyclers prefer staple fiber because the viscosity requirements are less stringent than those in bottle applications, allowing the inclusion of lower-grade feedstock.

PET bottles, encompassing both food-grade and non-food-grade formats, accounted for 35.00% of the volume in 2025. Food-grade bottle resin is expanding faster because European and North American laws mandate 25-30% recycled content by 2030, driving premium pricing and long-term contracts. PET sheets or films demand is driven by thermoformed packaging for pharmaceuticals and electronics that value recycled content. PET straps witness pricing competition from virgin polypropylene, which constrains margins outside deposit-driven European markets. Other specialty product types, including engineering resins, are growing steadily as automakers test recycled PET in non-load-bearing parts.

The Recyclate PET Market Report is Segmented by Product Type (PET Staple Fiber, PET Straps, PET Sheets or Films, PET Bottles Food Grade, PET Bottles Non-Food Grade, and Other Product Types), Application (Packaging, Industrial Yarn, Building Materials, and Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific contributed 42.85% of 2025 volume and is forecast to post an 8.05% CAGR to 2031, the fastest regional trajectory for the recyclate PET market. China's 35% recycled-content rule, effective 2025, has redirected export-oriented capacity toward domestic bottlers, tightening bale competition and lifting flake pricing. India's EPR program formalized 1,200 recycler certificates in 2024, catalyzing capacity upgrades from sub-food to food grade. Japan extended its Plastic Resource Circulation Act, stipulating 50% recycled content by 2030, prompting Suntory and Asahi to sign decade-long offtake agreements. Southeast Asian markets such as Vietnam and Indonesia attract multilateral financing for collection infrastructure, yet bale quality remains inconsistent due to limited source segregation.

Europe remains an established hub with deposit-return systems that deliver >90% collection, ensuring a steady supply of high-quality feedstock. Germany's Pfandsystem recovered 98% of bottles in 2024, feeding 620,000 tons of mechanical capacity. Spain and Italy will adopt deposit-return in 2025 and 2026, respectively, harmonizing recycled-content requirements across the bloc and encouraging cross-border investments. Chemical-recycling build-outs in France and the Netherlands add 150,000 tons of premium food-grade output, shifting incremental growth toward advanced recycling rather than mechanical throughput.

North America is fragmented but advancing due to state-level mandates. California, Oregon, Maine, Colorado, and New Jersey now legislate 15-50% recycled content in beverage containers, compelling joint ventures like PepsiCo-CarbonLite and Indorama-Loop. Canada's federal Plastics Registry brings national transparency, while Mexico's 2024 law introduces EPR for PET bottles, spurring Alpek to retrofit its Toluca plant for food-grade production. Federal-level inconsistency in the United States creates compliance complexity, yet also incentivizes regional hubs that service multiple states from centralized facilities.