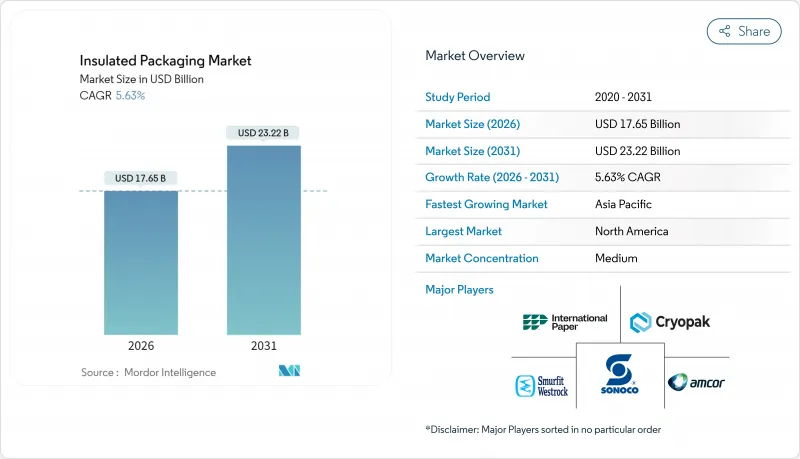

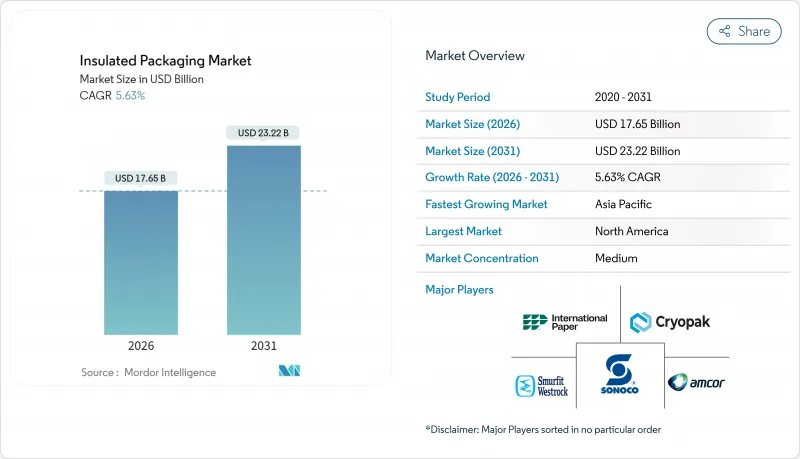

단열 포장 시장은 2025년 167억 1,000만 달러로 평가되었고, 2026년에는 176억 5,000만 달러로 성장할 것으로 예측되며, 2026-2031년 CAGR 5.63%로 성장을 지속하여 2031년까지 232억 2,000만 달러에 달할 것으로 예측했습니다.

콜드체인의 근대화, 전자상거래의 풀필먼트 수요, 지속가능한 소재에 대한 규제당국의 주목이 함께 이 확대를 견인하고 있습니다. 첨단 상변화물질(PCM)와 진공 단열 패널(VIP)은 온도 관리가 필요한 제품의 허용 운송 시간을 연장하고 부패 위험을 줄이고 세계 의료 물류를 지원합니다. 지역 격차는 여전히 존재합니다. 아시아태평양에서는 의약품 제조의 지속적인 성장을 보이며 콜드체인 거점에 많은 투자가 이루어지고 있는 반면 북미는 성숙한 전자상거래 네트워크를 활용하여 40.1%의 수익 리드를 유지하고 있습니다. 플라스틱은 여전히 가장 일반적인 기판이지만 바이오 에어로겔은 모든 경쟁 제품을 능가하는 성장을 보이고 있으며 최종 사용자가 성능 지표 외에도 폐기 비용 및 컴플라이언스 위험을 강조했다는 것을 보여줍니다. 고분자 비용 변동이 계속되는 가운데, 단열 포장 제조업체는 원료 다양화와 폐쇄 루프 모델을 채택하여 이익률을 안정화하고 있습니다.

소비자 직접 판매 배송은 물류 구조를 변혁하고, 복수 거점 배송망, 현관 선 체류 시간, 기후 변동하에서도 제품 품질을 유지하는 포장 설계를 공급자에게 요구하고 있습니다. 아마존의 온도 관리형 풀필먼트 센터 투자는 브랜드 가치 보호 및 부패 클레임 삭감을 위해 플랫폼이 콜드체인 기능을 내제화하는 사례입니다. 밀 키트 브랜드의 주간 출하량 증가는 단열 포장에 대한 예측 가능한 고주파수 주문을 의미합니다. 그 결과, 단열 포장 시장은 분류 자동화에 대응하면서 운임 할증을 삭감하는 경량으로 모듈식 포맷으로 전환하고 있습니다. 수요 분석에 의해 생산자는 QR코드 부착 센서를 임베디드하는 것도 촉구되고 있으며, 온도 이상이 발생했을 경우 배송업자에게 경고를 발하고, 설정 임계값을 넘은 패키지만 환불 대상으로 하는 구조를 지지하고 있습니다. 2025년에 선도적인 EC 소매업체는 공급업체 계약을 입증된 운송 경로 데이터와 연동시키는 성능 평가표를 발행하는 경향이 강해져 고성능 단열재에 대한 지속적인 투자를 확립하고 있습니다.

세포 및 유전자 치료, 백신, 단일클론항체에는 -80℃까지의 온도 관리가 필수이며, 제약 기업은 리던던트 전원, 현지 PCM 충전 설비, 검증이 끝난 포장 자재를 포함한 유통 거점에 대한 투자를 강요되고 있습니다. 동시에 밀키트 사업자는 냉장 단백질과 신선 식품을 다용한 메뉴 확충을 진행하고 있습니다. 이러한 분야가 함께 냉장 창고의 연간 가동률이 향상되어 주말 서비스 갭을 보완하는 운송업체에 대한 지속적인 수요를 지지하고 있습니다. 성공적인 포장 공급업체는 이제 PCM 블록을 교체하기만 하면 -20°C 생체의약품과 0-4°C 신선한 식품 모두를 지원할 수 있는 유니버설 시스템을 판매하고 있으며 물류 파트너의 SKU 증가를 억제하고 있습니다. FDA와 유럽 기관의 규제 감사는 컴플라이언스 프리미엄을 더욱 강화하고 추적 기능이 있는 단열 라인에 대한 투자를 가속화하고 있습니다.

발포 폴리스티렌과 폴리 우레탄은 스티렌과 이소시아네이트의 원료에 따라 달라지며, 그 가격은 원유 가격의 벤치 마크와 관련하여 변동합니다. 이로 인해 컨버터는 급격한 비용 상승에 노출되는 반면, 고객 계약에서는 가격이 6-12개월간 고정되는 경우가 많습니다. 헤지 전략은 부분적인 완화책이지만, 중견기업에게는 부담이 되는 유동성 지출이 필요합니다. 마진 압축은 새로운 금형 및 검증 연구를 위한 자본 예산을 방해하고 단열 포장 형식의 갱신 주기를 늦추고 있습니다. 일부 가공업체는 비용 흡수 방법으로 버진 폴리머를 재생재로 대체하고 있지만, 공급원의 불안정성에서 의약품 등급 포장에 사용하는 것은 제한적입니다. 지속적인 가격 변동으로 최종 사용자는 섬유 및 바이오폴리머 대체품의 시험 도입을 추진하고 있으며, 단열 포장 시장에서 기존의 발포재 솔루션에 대한 수요는 억제 경향이 있습니다.

플라스틱 재료는 확립된 공급망과 우수한 기계적 특성으로 인해 2025년 단열 포장 시장 규모의 41.85%를 차지했습니다. 그러나 바이오베이스 에어로겔은 7.74%의 연평균 복합 성장률(CAGR)을 나타내며 의약품 분야에서 발포제의 점유율을 분명히 침식하고 있습니다. 조달 담당자가 폐기물 처리세와 사용료를 산정할 때, 퇴비화 가능하고 재활용 가능한 라이너는 컴플라이언스 관련 비용 전체를 삭감하기 때문에 단열 포장 시장은 혜택을 받습니다. 목재섬유 복합재 제조업체는 결로 방지를 위해 수성 배리어 코트를 추가해 냉동 식품 분야에서의 적용 범위를 확대하고 있습니다. 업스트림 공정에서 기계적 재활용에 대한 병행 투자는 팔레트 운송에 적합한 성형 블록으로 변환 가능한 재생 PET 펠릿을 생산합니다. PET 외피와 섬유 코어를 결합한 하이브리드 복합재는 보다 낮은 평량으로 동등한 단열 성능(R값)을 달성하여 단열 성능을 유지하면서 포장 중량을 최대 18% 삭감합니다. 따라서 재료 선택은 단열 효율, 라인 자동화와의 적합성 및 진화하는 매립세의 균형을 맞추는 행위를 반영합니다.

하류에서는 원료 구매자가 바이오폴리머를 포함한 수지 계약을 다양화하고 스티렌 가격의 변동 위험을 헤지하고 있습니다. 중합 공정을 수직 통합하는 공급업체는 가격 결정력을 유지하는 반면, 제3자 컴파운더는 성형 사이클 단축을 가능하게 하는 급속 경화 화학물질의 인증 획득을 경쟁하고 있습니다. 2025년 실시의 라이프 사이클 어세스먼트는 입찰 서류에 표준적으로 기재되어 생산자에게 제조 공정(크래들 투 게이트)의 탄소발자국 공표를 촉구하고 있습니다. 단열 포장 업계에서는 주요 소매업체가 바이오 에어로겔 원료의 농업 잔류물 조달을 증명하는 증명서를 요구하는 움직임도 확산되어 삼림 관리 프로그램에 영향을 미치고 있습니다.

2025년 박스 컨테이너는 단열 포장 시장 점유율의 37.95%를 유지했습니다. 이것은 여러 업종에 있어서의 수작업 및 자동 피킹 라인에 대한 적합성이 요인입니다. 그러나 팔레트 운송은 CAGR 7.62%로 확대되었으며 완충재 폐기물 및 작업 공정을 줄이는 재사용 가능한 대형 포장재로의 전환을 반영하고 있습니다. 지역 배송 센터는 재고를 중앙 집중화하고 통합된 소형 화물 운송에 의존하기 때문에 48시간 보관 기간이 사전에 검증된 팔레트 수준 컨테이너를 선호합니다. 단열 포장 시장에서 항공사는 하층 갑판 위치에 탑재 가능한 풀 팔레트 VIP 크레이트를 승인하고 엄격한 시간 프레임 하에서 세포 요법 수출의 수송 능력을 확대하고 있습니다. 또한 전자기기 제조업체는 리튬 이온 배터리를 IATA 승인 온도 범위 내에 유지하기 위해 PCM 타일이 내장된 팔레트식 수송 용기를 채용하고 있습니다.

라이너 랩과 쿠션재는 여전히 틈새 EC 소포용이지만, 퀵 커머스 식품 소매업에서는 단열 로커와 직접 연계하는 모듈식 토트 인서트에 대체가 진행되고 있습니다. 경량의 파우치 형식은 리사이클 가능성의 검증에 직면하고 있어 가스 배리어 코팅을 실시한 단층 폴리에틸렌 구조의 시험 도입을 제조업체에 촉구하고 있습니다. 향후 성장은 완성 거점에 배치되는 자율 이동 로봇과의 사이즈 매트릭스의 조화에 달려 있습니다. 시뮬레이션 데이터를 설계 팀에 피드백할 수 있는 기업은 적재물을 보호하면서 선적 화물비를 줄이는 형상을 최적화하고 있습니다.

북미는 2025년에 39.60%의 수익을 차지했으며, 성숙한 EC 워크플로우, 광범위한 의약품 제조, 통일된 유통 가이드라인에 의해 최대의 지역 거점으로 계속되고 있습니다. 완성 센터는 마일리지 거리를 단축하기 위해 마이크로 허브와의 연계를 강화하여 포장 설계자는 6-12시간의 도시 지역 루프에 맞게 솔루션을 최적화해야 합니다. 약국 체인이 생물학적 제제의 당일 배송을 전개하는 가운데, 콜드체인에 대한 설비 투자는 견조하게 추이하고 있어 단열 포장의 국내 조달을 더욱 지지하고 있습니다.

아시아태평양은 8.85%의 연평균 복합 성장률(CAGR)을 기록했으며, 백신 생산 클러스터의 급속한 확대, 중간층 식단 서비스 수요 증가, 현대적인 냉장 저장 인프라에 대한 정부 보조금으로 세계 단열 포장 시장에서 가장 높은 성장률을 보였습니다. 다국적 컨버터 기업은 수지 공급을 확보하면서 수입 관세를 회피하기 위해 화학 원료 공급 거점 근처에 합작 회사를 설립하고 있습니다. 한국이나 싱가포르 등 지역 수출업체는 유럽 및 북미용 장거리편에서 안정적인 수송 성능을 실현하기 위해 VIP-PCM 하이브리드 기술을 채용하고 있습니다.

유럽에서는 지속가능성 규제 및 첨단 의료 요구의 균형을 맞추어 안정적인 한 자리 성장을 기록하고 있습니다. 순환형 경제지령에 의해 비재생 가능 발포재의 폐기 비용이 상승했기 때문에 대기업 식품 소매업체는 회수 기준을 충족시키는 섬유계 라이너로의 전환을 추진하고 있습니다. 동유럽 회원국은 EU 지역 기금을 활용하여 냉장실 용량을 확충, 농장에서 약국까지의 온도 관리의 통일을 확보하고 있습니다. 다른 지역에서는 남미가 해산물과 과일 수출을 확대하고 있으며 항공화물을 위해 합리적인 가격이지만 견고한 EPS 상자가 필요합니다. 반면 중동 및 아프리카는 기본 백신 배포에 주력하고 있으며 소득 향상과 공급망의 현대화에 따라 성장의 여지가 있습니다.

The insulated packaging market is expected to grow from USD 16.71 billion in 2025 to USD 17.65 billion in 2026 and is forecast to reach USD 23.22 billion by 2031 at 5.63% CAGR over 2026-2031.

Cold-chain modern-ization, e-commerce fulfillment demands, and regulatory attention on sustainable materials jointly steer this expansion. Advanced phase-change materials (PCM) and vacuum insulated panels (VIP) lengthen allowable transit windows for temperature-sensitive goods, lowering spoilage risk and supporting global health logistics. Regional disparities persist: Asia-Pacific experiences sustained pharmaceutical manufacturing growth and invests heavily in cold-chain nodes, whereas North America leverages mature e-commerce networks to protect a 40.1% revenue lead. Plastic remains the most common substrate, yet bio-based aerogels outpace all rivals, showing that end-users now weigh disposal costs and compliance risks alongside performance metrics. As polymer cost volatility lingers, insulated packaging producers diversify feedstocks and adopt closed-loop models to stabilize margins.

Direct-to-consumer delivery has re-shaped logistics, forcing suppliers to design packaging that safeguards product integrity through multi-stop carrier networks, porch dwell times, and variable climates. Amazon's investment in temperature-controlled fulfillment centers illustrates how platforms internalize cold-chain functions to protect brand equity and reduce spoilage claims. Meal-kit brands further amplify weekly volume, translating to predictable, high-frequency orders for insulated shippers. As a result, the insulated packaging market pivots toward lighter, modular formats that fit sorting automation while cutting freight surcharges. Demand analytics also prompt producers to embed QR-coded sensors that warn shippers if thermal abuse occurs, supporting refunds only when packages breach set thresholds. Across 2025, large e-commerce retailers increasingly issue performance scorecards that link supplier contracts to proven lane data, anchoring sustained investment in higher-performing insulators.

Cell and gene therapies, vaccines, and monoclonal antibodies require temperature windows down to -80 °C, compelling drug sponsors to fund distribution nodes that include redundant power, on-site PCM charging, and validated packaging fleets. Concurrently, meal-kit operators broaden menu offerings that rely on chilled proteins and fresh produce. Together these sectors elevate year-round utilization rates of cold-room space, which in turn sustains recurring demand for shippers that can endure weekend service gaps. Successful packaging suppliers now market universal systems adaptable to both -20 °C biologics and 0-4 °C perishables by swapping PCM bricks, reducing SKU proliferation for logistics partners. Regulatory audits by the FDA and European agencies further cement a compliance premium, accelerating spend on track-and-trace enabled insulation lines

Expanded polystyrene and polyurethane rely on styrene and isocyanate feedstocks whose prices swing with crude benchmarks, exposing converters to sudden cost spikes while customer contracts often lock prices for six to twelve months. Hedging strategies offer partial relief but require liquidity outlays that strain mid-tier firms. Margin compression hinders capital budgets for new tooling or validation studies, slowing the refresh cycle of insulated formats. Some converters replace virgin polymer with recycled content to buffer costs, yet inconsistent supply streams limit usage in pharmaceutical-grade packs. Persistent volatility encourages end-users to test fiber or bio-polymer substitutes, moderating demand for conventional foam-based solutions within the insulated packaging market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastic materials commanded 41.85% of the insulated packaging market size in 2025 owing to entrenched supply chains and robust mechanical properties. Yet, bio-based aerogels post an 7.74% CAGR that visibly erodes foam share in pharmaceutical corridors. The insulated packaging market benefits when procurement officers calculate disposal levies and user fees, because compostable and recyclable liners cut overall compliance spend. Manufacturers of wood-fiber composites add water-borne barrier coats to repel condensation, expanding addressable segments in frozen meals. Parallel investment in mechanical recycling upstream yields r-PET pellets that convert into molded bricks suited for pallet shippers. Hybrid composites combining PET skin with fiber core reach equivalent R-values at lower grammage, preserving thermal performance while dropping pack weight by up to 18%. Material choice therefore reflects a balancing act among insulation efficiency, line automation compatibility, and evolving landfill taxes.

Downstream, raw material buyers diversify resin contracts to include biopolymers, thus hedging against styrene volatility. Suppliers that vertically integrate polymerization steps maintain pricing power, while third-party compounders race to qualify rapid-cure chemistries enabling shorter molding cycles. Lifecycle assessments carried out in 2025 commonly form part of bid documents, nudging producers to publish cradle-to-gate carbon footprints. The insulated packaging industry also sees major retailers demand certificates verifying agricultural residue sourcing for bio-aerogels, influencing forest stewardship programs.

Boxes and containers preserved 37.95% of the insulated packaging market share in 2025 because they fit manual and automated picking lines across multiple sectors. Nonetheless, pallet shippers accelerate at 7.62% CAGR, reflecting a shift toward reusable macro-packs that cut dunnage waste and labor touches. Regional distribution centers pool inventory and rely on consolidated LTL moves, which favor pallet-level containers pre-validated for 48-hour hold times. The insulated packaging market sees airlines approve full-pallet VIP crates that ride in lower-deck positions, expanding capacity for cell therapy exports under stringent time windows. Furthermore, electronics manufacturers employ pallet shippers with PCM tiles to keep lithium-ion batteries within IATA approved temperature limits.

Liner wraps and cushions still serve niche e-commerce parcels, yet quick-commerce grocers substitute modular tote inserts that integrate directly with insulated lockers. Pouch formats, while lightweight, face recyclability scrutiny, pushing producers to trial mono-PE structures with gas-barrier coatings. Future growth hinges on harmonizing size matrices with autonomous mobile robots deployed in fulfillment hubs. Firms able to feed simulation data back to design teams optimize form factors that reduce outbound freight spend while safeguarding payloads.

The Insulated Packaging Market Report is Segmented by Material (Plastic, Paper and Wood-Fiber, Glass, Metal Foils, and More), Product Type (Pouches and Bags, Boxes and Containers, and More), Insulation Technology (Expanded Polystyrene, Vacuum Insulated Panels, and More), End-User Industry (Food and Beverage, Pharmaceutical and Biotechnology, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America represented 39.60% revenue in 2025 and remains the largest regional node thanks to mature e-commerce workflows, broad pharmaceutical manufacturing, and harmonized distribution guidelines. Fulfillment centers increasingly pair with micro-hubs to trim last-mile distance, thereby pushing pack designers to tailor solutions for six to 12-hour urban loops. Cold-chain capital spending remains robust as pharmacy chains roll out same-day biologics delivery, further sustaining domestic procurement of insulated packaging.

Asia-Pacific records a 8.85% CAGR, the fastest in the global insulated packaging market, driven by rapid expansion of vaccine production clusters, growing middle-class demand for meal services, and government subsidies for modern cold storage infrastructure. Multinational converters open joint-ventures near chemical feedstock hubs to secure resin supply while avoiding import tariffs. Regional exporters, especially in South Korea and Singapore, adopt VIP-PCM hybrids to achieve consistent lane performance on long-haul flights to Europe and North America.

Europe balances sustainability regulation with advanced healthcare needs, registering steady single-digit growth. The circular economy directive raises disposal fees on non-recyclable foams, spurring large grocers to adopt fiber-based liners that pass curbside collection tests. Eastern member states upgrade cold-room capacity via EU regional funds, ensuring harmonized temperature control from farm to pharmacy. Elsewhere, South America scales fish and fruit exports that necessitate affordable yet robust EPS boxes for airfreight, while Middle East and Africa focus on baseline vaccine distributionboth offering upside as incomes rise and supply chains modernize.