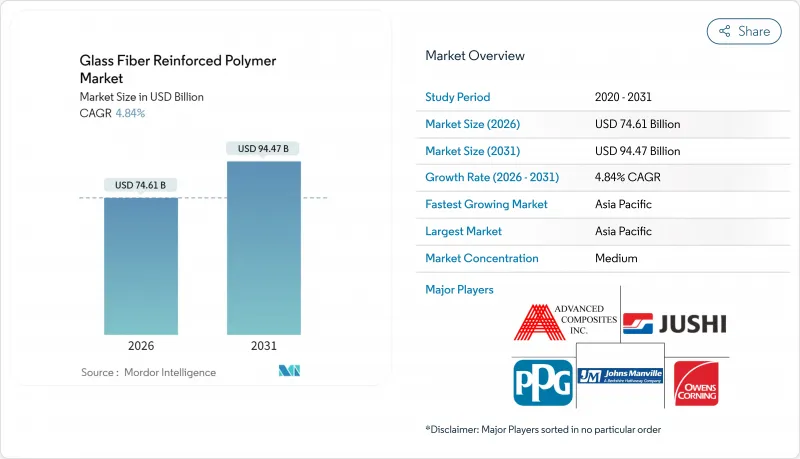

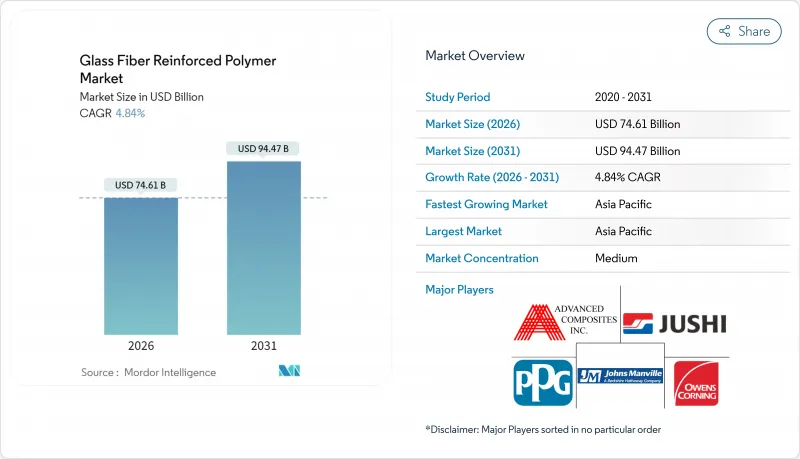

유리섬유 강화 폴리머 시장은 2025년 711억 7,000만 달러로 평가되었고, 2026년에는 746억 1,000만 달러로, 2026년부터 2031년에 걸쳐 CAGR 4.84%로 성장하고 2031년까지 944억 7,000만 달러에 달할 전망입니다.

운송, 신재생에너지, 항공우주, 건설분야의 OEM 제조업체가 중량감소, 내구성 향상, 보다 엄격한 지속가능성 목표 달성을 목적으로 부식이 없는 복합재료로 중금속을 대체하는 움직임이 수요 증가를 견인하고 있습니다. 특히 아시아태평양의 급속한 도시화는 철근, 교량 바닥판, 파이프라인 라이너를 위한 유리 섬유 강화 폴리머 솔루션을 지정하는 인프라 투자를 촉진하고 있습니다. 재료 혁신으로 성능 범위가 확대되고 있습니다. 바이오 베이스의 에폭시 수지가 양산 단계에 들어가, 사축 스티치 보강재나 하이브리드 탄소 및 유리 섬유 복합재가 새로운 구조 용도를 가능하게 하고 있습니다. 경쟁은 격렬한 것 분산화가 진행되고 있고, 다국적 기업은 저이익률의 제품 라인을 정리해 리사이클 업자와의 제휴를 진행하는 한편, 지역 제조업체는 물류 리스크나 통환율 변동성을 완화하기 위해 고객 인접 지역에서 생산 능력을 확대하고 있습니다. 제품 수명 종료시의 과제는 남아 있는 것, 열분해나 탄화규소의 업사이클링에 있어서의 기술 혁신에 의해 순환형 사회의 실현을 향한 대처가 전진해, 유럽이나 북미에 있어서의 규제 압력이 완화되고 있습니다.

전동 이동성 프로그램은 복합재료의 채택을 가속화하고 있습니다. 왜냐하면 1Kg의 경량화가 주행 거리를 연장하고 배터리 크기를 줄이기 때문입니다. 유리 섬유 강화 열가소성 플라스틱은 배터리 케이스에서 프레스 강판을 대체하고 질량을 40% 줄이면서 내화성과 단열성을 향상시키고 있습니다. 자동차 제조업체는 무게를 30% 줄이면서도 정밀한 기어 포지셔닝을 위한 강성을 유지하는 탄소와 유리의 하이브리드 변속기 하우징을 채택하고 있습니다. 유리 섬유 강화 폴리머 시장 진출기업은 금형 비용의 저감을 활용하여 상용차에서 최대 50kg의 중량을 삭감하는 텐션 리프 스프링 등의 틈새 부품의 현지 생산을 진행하고 있어 이로써 적재량 증가가 가능해지고 있습니다.

풍력 발전 분야는 가장 빠르게 성장하는 최종 사용자입니다. 고층 타워와 긴 블레이드에는 경량이면서도 강도가 높은 재료가 필수가 되기 때문입니다. 터빈 OEM 제조업체는 첨단 편향을 허용 범위 내로 억제하기 위해 탄소 유리 복합재의 하이브리드 스파와 루트 인서트를 통합하여 15MW 클래스의 플랫폼을 실현하고 있습니다. 리투아니아의 연구자들은 사용한 블레이드에서 섬유와 독성 스티렌을 회수하는 열분해 공정을 입증하여 매립처분에 비해 폐기물 처리의 영향을 최대 51% 줄였습니다. 이러한 진보는 국내 입찰에서 점점 더 요구되는 라이프 사이클 인증 향상에 기여하고 있습니다.

특수 섬유 사이징, 엄격한 공정 관리, 에너지 집약적인 용해 공정으로 범용 금속에 비해 비용이 높습니다. 2024년 가격 하락으로 이익률이 압박되어 오엔스 코닝사의 복합재료 부문 매출은 2024년 1분기에 11% 감소한 5억 2,300만 달러로 유리 강화재 부문의 전략적 재검토를 촉구했습니다. 자본 집약적인 용해로와 신흥 지역의 규모의 경제성 한계로 인해 단위 비용이 높아지고 있으며 비용 중심 부문에서의 채택이 지연되고 있습니다.

폴리에스테르 수지는 저가격 및 압축 성형 및 스프레이업 성형 공정과의 폭넓은 호환성으로 2025년의 유리 섬유 강화 폴리머 시장 규모의 61.47%를 차지해 수요를 견인했습니다. 에폭시 수지는 규모야말로 작은 것, 뛰어난 접착성, 내피로성, 저보이드 가공 특성에 의해 항공우주, 풍력, 자동차 분야의 엄격한 사양을 충족하기 위해 2031년까지 4.99%라는 최고 CAGR로 추이할 전망입니다. 비닐에스테르 수지는 폴리에스테르보다 뛰어난 내약품성과 에폭시보다 낮은 코스트를 겸비해, 중간 정도의 성능을 필요로 하는 틈새 시장(선박 및 화학약품 저장 프로젝트)에서 수요가 높아지고 있습니다. 재생가능한 글리콜을 23% 함유한 신개발 바이오기반 에폭시 수지는 기계적 강도를 손상시키지 않으면서 제조시 배출량을 21% 줄여 ESG 스코어카드 및 조달 가이드라인 달성을 지원합니다. 고체 고분자 전해질로서도 기능하는 나노 필러 개질 에폭시 수지는 구조용 전지나 슈퍼커패시터의 이용 사례를 개척하고 있습니다. 유리 섬유 강화 폴리머 시장에서는 다운스트림 고객이 저탄소 대체품을 요구하는 동안 기존 폴리에스테르 수지에 대한 비용 압력이 지속될 것으로 예측됩니다.

비닐 에스테르 수지 제조업체는 고속 수지 전송 라인에 대응하기 위해 경화 속도의 개선을 진행하고 있습니다. 한편, 폴리우레탄계 수지는 강성보다 인성이 중시되는 충격 흡수 패널에의 채택이 진행되고 있습니다. PEEK와 같은 틈새 열가소성 수지는 240 ° C의 내열성이 요구되는 석유 및 가스 갱내 공구에서 여전히 필수적입니다. 공급 과잉 우려는 제한적입니다. 중국의 대규모 폴리에스테르 플랜트는 자사 전용로 네트워크를 운영하고 있어 수요 변동 시 신속한 생산 조정이 가능하기 때문입니다. 에폭시 수지 공급업체는 비스페놀 A와 에피클로로히드린의 선도 계약에 따라 원료 가격 변동을 헤지하여 항공우주 프라임 제조업체를 위한 가격을 안정화시키고 있습니다. 60초 내에 이형 가능한 스냅 큐어 에폭시와 같은 연속 가공 기술의 혁신은 사이클 타임을 단축하고 유리 섬유 강화 폴리머 시장의 양산 확대를 지원할 것입니다.

시트 몰딩 컴파운드 및 유리 매트 열가소성 수지를 포함한 압축 성형은 높은 재현성과 중량 생산의 경제성으로 인해 2025년 수익의 30.56%를 차지했습니다. 고유동 및 장섬유 열가소성 컴파운드에 의해 2차 가공 불필요한 박육 복잡 부품이 제조 가능하게 됨으로써 사출 성형은 2031년까지 연평균 복합 성장률(CAGR)4.89%를 유지할 전망입니다. 진공 보조 수지 전사 성형은 진화를 이루고 있으며, 경화시의 가압에 의해 섬유 함유율을 62%로 높여, 인장 강도를 760MPa까지 향상시키는 것과 동시에, 두께를 4% 감소하는 효과가 나타납니다. 설계 자유도가 택트 타임을 웃도는 건축용 패널이나 요트 선체에서는 수동 적층이 여전히 채택되고 있습니다.

연속 인발 성형 라인에서는 인라인 연마·밑칠 공정을 통합해, 창틀이나 송전망용 크로스 암의 공정 후 공정에 있어서의 인건비를 삭감하고 있습니다. 열경화성 수지와 열가소성 수지의 매트릭스를 전환할 수 있는 하이브리드 생산 셀은 자산 활용률을 향상시켜 유리 섬유 강화 폴리머 시장에서 복합재료 모듈의 실현을 가능하게 합니다. 로봇에 의한 핸들링은 폐기물을 저감하고, 클로즈드 루프의 디지털 트윈 기술에 의해 수지 과잉 영역을 실시간으로 검지, 박리 발생의 위험 개소를 방지합니다. 자동차용 고량산 실빔에 있어서는 사이클 타임이 55초를 하회하면 알루미늄 압출 성형과의 비용 경쟁력이 달성 가능하고, 주요 Tier 1 공급자는 2027년까지 이 목표를 내걸고 있습니다. 신흥경제국에서는 기술이전을 지원하는 우대대출제도에 따라 지역 수요를 충족하는 현지생산의 압축프레스가 보급되고 있습니다.

아시아태평양은 2025년 매출액의 48.35%를 차지했으며 2031년까지 연평균 복합 성장률(CAGR) 4.93%로 확대될 것으로 전망됩니다. 중국에서는 BASF의 108억 달러 규모의 쇼에 복합공장 등 거대 플랜트에 의한 생산능력 확대가 가속화되고 있어 100% 재생가능 전력으로 가동하여 자동차·전자기기용 복합재를 공급합니다. 인도에서는 철도 및 도로 근대화 사업이 국내 수요를 환기하고 있어 BASF사는 하류 가공업자용 폴리아미드 및 PBT의 증산을 발표했습니다. ASEAN 국가에서는 공급망 다양화에 따라 유리 섬유 강화 폴리머 시장 진출기업이 최종 사용자에 가까운 입지를 선택하는 니어 쇼어링이 진전하고 있습니다.

북미에서는 미국이 터빈 블레이드, 항공우주, 인프라 분야에서 수요 증가를 주도하고 있습니다. 화화집단(Jushi Group)은 미국에서의 신규로 건설을 최종 단계로 하고 있으며, 지역공급 안정성과 수입 관세 회피를 약속하고 있습니다. 연방 정부의 바이 아메리카 조항은 국내 조달을 점점 우월하게 만들고 기존 생산자와 신규 진출기업 모두에게 이익을 가져다줍니다. 캐나다는 제로 방출 차량 규제에 대응하기 위해 경량 버스와 배터리 케이스에 주력하고 있습니다. 유럽에서는 순환형 경제 관련법이 시행되어 재생 수지와 블레이드간 유리 회수 기술에 대한 투자가 촉진되고 있습니다. 카본 리버스의 다단계 열분해 기술은 단열재나 시트 성형 컴파운드용 섬유를 회수해, 조성금이나 브랜드 오너와의 제휴를 획득하고 있습니다. 독일은 내식성 라이너를 필요로 하는 수소 파이프라인 개수를 지원하고, 북해의 해상 풍력 발전 확대는 고탄성률 로빙 수요를 지속하고 있습니다. 남미 및 중동, 아프리카은 여전히 틈새 시장이지만, 브라질이 항만을 근대화하고 사우디아라비아가 수송·재생에너지 분야의 대형 프로젝트에 자금을 투입하는 가운데 기세를 늘리고 있어 유리 섬유 강화 폴리머 시장에 새로운 활약의 장이 열리고 있습니다.

The Glass Fiber Reinforced Polymer market is expected to grow from USD 71.17 billion in 2025 to USD 74.61 billion in 2026 and is forecast to reach USD 94.47 billion by 2031 at 4.84% CAGR over 2026-2031.

Demand is rising as OEMs in transportation, renewable energy, aerospace, and construction replace heavier metals with corrosion-free composites to lower weight, boost durability, and meet stricter sustainability targets. Rapid urbanization, especially in Asia-Pacific, is stimulating infrastructure investments that specify glass fiber reinforced polymer solutions for rebar, bridge decks, and pipeline liners. Material innovation is widening the performance envelope: bio-based epoxy chemistries are entering series production, while quadaxial stitched reinforcements and hybrid carbon-glass fabrics are enabling new structural applications. Competition is intense but fragmented; multinationals are pruning low-margin lines and partnering with recyclers, whereas regional producers expand capacity close to customers to hedge logistics risk and currency volatility. End-of-life hurdles remain; nevertheless, breakthroughs in pyrolysis and silicon-carbide up-cycling are improving the circularity narrative and easing regulatory pressure in Europe and North America.

Electric-mobility programs are accelerating composite uptake because every kilogram saved extends driving range and shrinks battery size. Glass fiber reinforced thermoplastics now replace stamped steel in battery enclosures, trimming mass by 40% while improving fire resistance and thermal insulation. OEMs deploy hybrid carbon-glass transmission housings that cut 30% weight yet keep stiffness for precise gear alignment. Glass fiber reinforced polymer market participants also exploit lower tooling costs to localize niche parts such as tension leaf springs that remove up to 50 kg from commercial vehicles, thereby permitting higher payloads.

The wind sector is the fastest-growing end-user because taller towers and longer blades mandate lighter yet stronger materials. Turbine OEMs integrate carbon-glass hybrid spars and root inserts to keep tip deflection within limits, thereby enabling 15-MW platforms. Lithuanian researchers have validated pyrolysis routes that reclaim fibers and toxic styrene from end-of-life blades, reducing disposal impacts by up to 51% versus landfill. These advances improve the life-cycle credentials that national tenders increasingly require.

Specialized fiber sizing, tight process controls, and energy-intensive melting raise costs versus commodity metals. Price declines during 2024 squeezed margins; Owens Corning's Composites sales fell 11% to USD 523 million in Q1 2024, prompting a strategic review of its glass reinforcements unit. Capital-intensive furnaces and limited economies of scale in emerging regions keep unit costs elevated, delaying adoption in cost-driven segments.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Polyester resins dominated 2025 demand with a 61.47% share of the glass fiber reinforced polymer market size, thanks to low price and broad compatibility with compression and spray-up processes. Epoxy, though smaller, will register the highest 4.99% CAGR to 2031 because its superior adhesion, fatigue resistance, and low-void processing meet stringent aerospace, wind, and automotive specifications. Vinyl ester fills the mid-performance niche, combining better chemical resistance than polyester with lower cost than epoxy, and thus appeals to marine and chemical containment projects. Recent bio-based epoxies containing 23% renewable glycol cut manufacturing emissions by 21% without sacrificing mechanical strength, supporting ESG scorecards and procurement guidelines. Nanofiller-modified epoxies that double as solid polymer electrolytes open structural battery and supercapacitor use cases. The glass fiber reinforced polymer market expects continued cost pressure on conventional polyester as downstream customers seek lower embedded carbon alternatives.

Vinyl ester producers are enhancing cure kinetics to suit high-speed resin transfer lines, while polyurethane chemistries gain adoption in impact-absorption panels where toughness outweighs stiffness. Niche thermoplastics such as PEEK remain essential in oil-and-gas downhole tools requiring 240 °C service temperatures. Oversupply concerns are limited because large polyester plants in China run captive furnace networks, allowing quick output throttling during demand swings. Epoxy suppliers hedge raw-material volatility through forward contracts on bisphenol-A and epichlorohydrin, stabilizing pricing to aerospace primes. Innovations in continuous processing, such as snap-cure epoxies that reach demold in 60 seconds, will compress cycle time and support volume ramp-ups in the glass fiber reinforced polymer market.

Compression molding, including Sheet Molding Compound and Glass Mat Thermoplastic, accounted for 30.56% of 2025 revenue due to high repeatability and favorable economics at medium volumes. Injection molding will post a 4.89% CAGR through 2031 as high-flow, long-fiber thermoplastic compounds allow thin-wall complex parts without secondary finishing. Vacuum-assisted resin transfer molding has evolved; adding pressure during cure boosts fiber volume to 62% and lifts tensile strength to 760 MPa while trimming thickness by 4%. Manual lay-up persists for architectural panels and yacht hulls where design freedom overrules takt time.

Continuous pultrusion lines now integrate inline sanding and priming, reducing downstream labor for window frames and power-grid crossarms. Hybrid production cells that switch between thermoset and thermoplastic matrices extend asset utilization and enable multimaterial modules in the glass fiber reinforced polymer market. Robotic handling lowers scrap, and closed-loop digital twins detect resin-rich zones in real time, preventing delamination hot spots. Cost parity with aluminum extrusion is within reach for high-volume automotive sill beams once cycle times fall below 55 seconds, a benchmark that major Tier-1 suppliers target by 2027. In emerging economies, localized compression presses fill regional demand, aided by concessional financing that supports technology transfer.

The Glass Fiber Reinforced Polymer Market Report Segments the Industry by Resin Type (Polyester, Vinyl Ester, Epoxy, and More), Process (Manual Process, Compression Molding, and More), Fiber Form (Rovings, Chopped Strands Mats, and More), End-User Industry (Energy, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Asia-Pacific dominated with 48.35% revenue in 2025 and is projected to grow at a 4.93% CAGR through 2031. China accelerates capacity with mega-plants such as BASF's USD 10.8 billion Zhanjiang Verbund, which will operate on 100% renewable electricity and supply automotive and electronics composites. India's rail and road modernization campaigns stimulate local demand; BASF has announced additional polyamide and PBT expansions to serve downstream converters. ASEAN countries leverage near-shoring as supply-chain diversification pushes glass fiber reinforced polymer market participants to locate closer to end users.

In North America, the United States leads turbine blade, aerospace, and infrastructure uptake. Jushi Group is finalizing a greenfield furnace in the country, promising regional supply security and import duty avoidance. Federal Buy-America clauses increasingly favor domestic sourcing, benefitting incumbent producers and new entrants. Canada focuses on lightweight buses and battery enclosures to meet zero-emission vehicle mandates. Europe enforces circular-economy legislation that spurs investment in recyclable resins and blade-to-blade glass reclamation. Carbon Rivers' multi-stage pyrolysis recovers fiber for reuse in insulation and sheet molding compounds, attracting grants and brand-owner partnerships. Germany supports hydrogen pipeline retrofits that require corrosion-resistant liners, while offshore wind build-out in the North Sea sustains high-modulus roving demand. South America and Middle East & Africa remain niche but are gaining momentum as Brazil upgrades ports and Saudi Arabia funds mega-projects in transport and renewable energy, opening new arenas for the glass fiber reinforced polymer market.