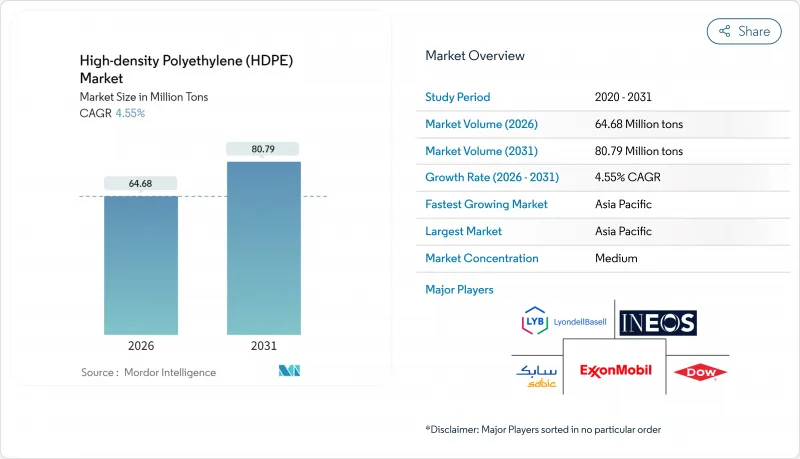

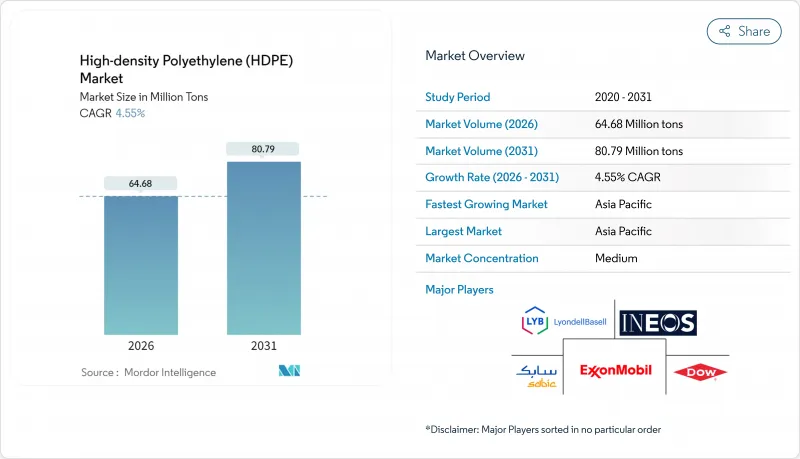

고밀도 폴리에틸렌(HDPE) 시장은 2025년 6,187만 톤에서 2026년에는 6,468만 톤으로 성장할 것으로 보입니다. 2026-2031년에 걸쳐 연평균 복합 성장률(CAGR) 4.55%로 성장할 것으로 예상되며, 2031년까지 8,079만 톤에 이를 것으로 예측됩니다.

강력한 인프라 지출, 확대되는 화학 재활용 공급망, 수소 대응 파이프 시스템의 채택 증가가 이러한 성장세를 뒷받침하는 한편, 소재의 본질적인 내구성, 내화학성 및 재활용성은 최종 사용자들이 고밀도 폴리에틸렌 솔루션에 계속해서 의존하도록 합니다. 인도 및 아세안(ASEAN) 전역의 공공 주택 프로그램 가속화, 전자상거래 유통 분야의 식품 등급 블로우 성형 확대, 저탄소 가스 그리드를 위한 PE-100-RC 파이프 네트워크 구축이 종합적으로 HDPE 시장의 잠재 수요를 확대하고 있습니다. 혼합 폐기물 흐름을 버진 등급 rHDPE로 전환하는 화학 재활용업체들은 공급 안정성을 강화하고 원료 변동성을 완화하며 순환 경제 의무를 강화합니다. 경쟁은 다소 분산된 상태가 지속되지만, 크래커 설비와 첨단 재활용 기술을 결합한 수직 통합 생산자들은 비용 및 지속가능성 측면에서 우위를 유지합니다.

수자원 네트워크 현대화 프로젝트는 100년 수명과 토목 공사 비용을 30-40% 절감하는 무굴착 설치 능력을 겸비한 HDPE 파이프를 우선적으로 채택합니다. 미국 토목공학회(ASCE)는 노후 배수관로의 부식 저항성 측면에서 HDPE의 우수성을 강조합니다. 인도의 2024년 신규 폴리에틸렌 품질 기준 의무화는 핵심 수자원 응용 분야의 재료 무결성을 강화합니다. 프로젝트 설계자들은 지반 변동에 대응하는 유연성으로 누수 위험을 줄이는 HDPE를 선호합니다. 다수의 5개년 계획을 아우르는 공공 부문 자금 조달 주기는 안정적인 파이프 수요를 보장하여 HDPE 시장의 예측 가능한 성장을 뒷받침합니다. 무굴착 공법 통합은 총 설치 비용을 낮춤으로써 HDPE를 콘크리트 및 연성 주철 대안과 차별화합니다.

급속한 전자상거래 확산은 복잡한 물류 과정을 견디면서도 식품 품질을 보호하는 포장을 요구합니다. 식품 등급 HDPE 용기는 엄격한 이행 시험을 통과하고 FDA 승인을 획득하여 유제품, 조미료, 상온 보관 음료의 기본 선택지가 됩니다. 2025년 3월 발효 예정인 유럽연합 규정은 식품 접촉 플라스틱에 대한 광범위한 추적성을 요구하며, 이는 HDPE 생산자들이 이미 충족하는 기준입니다. 얇은 벽 두께 블로우 성형을 통한 중량 경감은 수지 사용량을 줄이고, 기업의 배출 목표와 부합하며, 수요를 유지하여 HDPE 시장의 회복력을 강화합니다.

포장 규제가 강화되면서 유럽 및 북미 일부 지역에서 일회용 HDPE 제품 수요가 감소하고 있습니다. 그러나 HDPE의 재활용성은 다회용 응용 분야에서 정책 리스크를 완화하며, 기계적 재활용 경로가 부족한 다층 필름 대비 확립된 수거 체계가 경쟁력을 유지합니다. 가산업체들은 무게 기준을 준수하기 위해 캡 및 디스펜싱 시스템을 재설계하여 용량 손실을 제한하고 있습니다. 결과적으로 규제는 HDPE 시장 성장을 억제하지만 역전시키지는 못합니다.

시트 및 필름 부문은 2025년 HDPE 시장 점유율의 40.65%를 차지했으며, 이는 꾸준한 포장 수요와 다운스트림 변환업체의 블로운 필름 공정 숙련도에 기반합니다. 지속가능한 포장 목표는 혼합 폴리머보다 HDPE를 선호하는 단일 소재 필름 설계를 촉진합니다.

파이프 및 튜브는 HDPE 시장 규모에서 차지하는 비중은 작지만, 상수도 인프라 개조, 수소 대비 가스 그리드, 무굴착식 재생 공사로 인해 2026-2031년 기간 동안 가장 높은 6.07%의 연평균 성장률(CAGR)을 기록했습니다. 누수 손실 벌금이 증가함에 따라, 균일한 융착 접합부와 100년 수명을 가진 HDPE 배관으로 유틸리티 업체들이 전환하고 있습니다. 산업용 필름, 지오멤브레인, 운반용 백이 포트폴리오를 완성하며, 건설 지출이 위축될 때 기준 레진 수요를 유지합니다.

고밀도 폴리에틸렌(HDPE) 시장 보고서는 용도별(파이프, 튜브, 시트, 필름, 경질 제품, 기타 용도), 수지 등급별(PE-80, PE-100, PE-100-RC, 기타), 최종 사용자 산업(포장, 건축 및 건설, 농업, 운송, 전기 및 전자 등), 지역(아시아태평양, 북미, 유럽, 남미)별로 분류됩니다.

아시아태평양 지역은 2025년 HDPE 시장 점유율의 42.30%를 차지했으며, 중국의 다운스트림 필름 수출과 인도의 인프라 붐에 힘입어 2031년까지 연평균 5.55%의 성장률을 기록할 것으로 전망됩니다. 이 지역의 통합 생산 업체들은 석탄-올레핀 및 나프타 크래커의 유연성으로 에틸렌 가격 변동성을 완화하는 이점을 누리고 있습니다. 그러나 공급 과잉 기간으로 지역 마진이 압박되면서 재고 균형을 위한 정기 점검이 촉발되었습니다.

북미의 HDPE 시장은 에탄 기반 원료의 이점과 화학 재활용 투자 붐으로 순환형 수지 공급이 확대되는 혜택을 누리고 있습니다. 성장률은 아시아태평양보다 낮지만, 고부가가치 파이프, 필름 및 의료용 등급 수요가 수익 기반을 유지합니다.

유럽은 여전히 정책 주도적이며, 수소 네트워크 확장으로 HDPE가 PE-100-RC 파이프 프로젝트와 재생 원료 확보를 위한 화학 재활용 제휴로 유입됩니다. 일회용 플라스틱 금지 정책으로 얇은 벽체 경질 포장재 물량은 감소했으나, 높은 재활용성 덕분에 HDPE는 다회용 반환형 크레이트 및 화학 드럼 분야에서 확고한 위치를 유지합니다.

The High-density Polyethylene (HDPE) market is expected to grow from 61.87 Million tons in 2025 to 64.68 Million tons in 2026 and is forecast to reach 80.79 Million tons by 2031 at 4.55% CAGR over 2026-2031.

Strong infrastructure spending, widening chemical-recycling supply chains, and rising adoption of hydrogen-ready pipe systems anchor this trajectory, while the material's intrinsic durability, chemical resistance, and recyclability keep end-users committed to high-density polyethylene solutions. Accelerated public-housing programs across India and ASEAN, expanding food-grade blow-molding in e-commerce distribution, and the rollout of PE-100-RC pipe networks for low-carbon gas grids collectively widen the HDPE market's addressable demand. Chemical recyclers diverting mixed-waste streams into virgin-grade rHDPE strengthen supply security, temper feedstock volatility, and reinforce circular-economy mandates. Moderately fragmented competition persists, yet vertically integrated producers that pair cracker capacity with advanced recycling retain cost and sustainability advantages.

Water-network modernisation projects prioritise HDPE pipes because they combine a 100-year service life with trenchless installation capability that cuts civil works costs by 30-40%. The American Society of Civil Engineers underscores HDPE's corrosion resistance for ageing distribution lines. India's 2024 quality-standard mandate for virgin polyethylene reinforces material integrity in critical water applications. Project designers favour HDPE because its flexibility accommodates ground movement, reducing leakage risk. Public-sector funding cycles spanning multiple five-year plans guarantee steady pipe volumes, ensuring predictable growth for the HDPE market. Integration of trenchless methods further differentiates HDPE from concrete and ductile-iron alternatives by lowering total installed costs.

Rapid e-commerce penetration demands packaging that survives complex logistics while protecting food quality. Food-grade HDPE containers pass stringent migration tests and hold FDA clearance, making them default choices for dairy, condiments, and shelf-stable beverages. European Union regulations, effective March 2025, require extensive traceability for food-contact plastics, a standard that HDPE producers already meet. Weight-reduction via thin-wall blow-molding lowers resin usage, aligns with corporate emission targets, and sustains demand, reinforcing the HDPE market's resilience.

Tighter packaging rules compress demand for disposable HDPE articles in Europe and parts of North America. However, HDPE's recyclability mitigates policy risk in multi-use applications, and well-established collection streams preserve its appeal versus multi-layer films that lack mechanical-recycling pathways. Converters are redesigning closures and dispensing systems to remain within weight thresholds, limiting volume loss. Consequently, regulation restrains but does not reverse HDPE market growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Sheets and Films held 40.65% of the 2025 HDPE market share, underpinned by steady packaging demand and downstream converter familiarity with blown-film processes. Sustainable packaging targets stimulate mono-material film designs that favour HDPE over mixed polymers.

Pipes and Tubes, although a smaller slice of the HDPE market size, posted the sharpest 6.07% CAGR for 2026-2031 on the back of water-infrastructure retrofits, hydrogen-ready gas grids, and trenchless renewals. Rising leak-loss penalties push utilities toward HDPE piping thanks to its homogenous fusion joints and 100-year service life. Industrial films, geomembranes, and carrier bags round out the portfolio, sustaining baseline resin offtake when construction spending softens.

The High-Density Polyethylene (HDPE) Market Report is Segmented by Application (Pipes and Tubes, Sheets and Films, Rigid Articles, and Other Applications), Resin Grade (PE-80, PE-100, PE-100-RC, and More), End-User Industry (Packaging, Building and Construction, Agriculture, Transportation, Electrical and Electronics, and More), and Geography ( Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Asia-Pacific controlled 42.30% of the 2025 HDPE market share and is forecast to record a 5.55% CAGR to 2031, propelled by Chinese downstream film exports and India's infrastructure boom. Integrated producers in the region benefit from coal-to-olefins and naphtha-cracker flexibility, buffering ethylene volatility. However, oversupply periods have compressed regional margins, prompting scheduled maintenance to balance inventories.

North America's HDPE market benefits from ethane-advantaged feedstock and a wave of chemical-recycling investments that elevate circular-resin availability. While growth rates are lower than Asia-Pacific, value-added pipe, film, and medical-grade demand sustains profit pools.

Europe remains policy-driven; its hydrogen-network build-out channels HDPE into PE-100-RC pipe projects and chemical-recycling alliances that secure recycled feedstock. Anti-single-use-plastic mandates depress thin-wall rigid packaging volumes, yet high recyclability keeps HDPE firmly in multi-use, returnable crates and chemical drums.