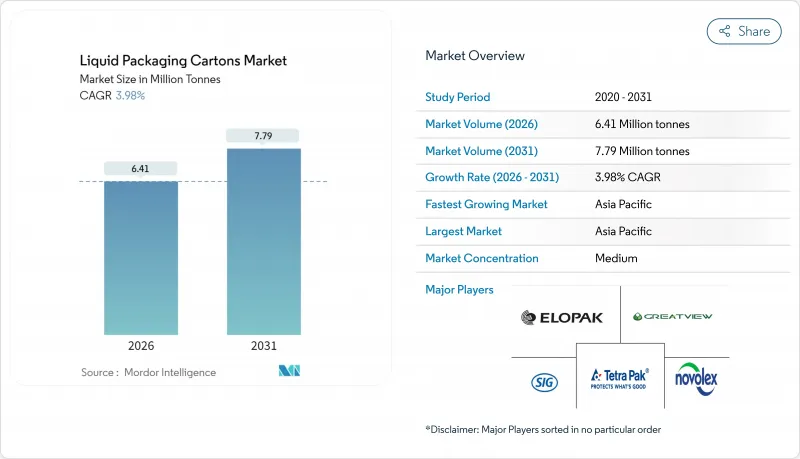

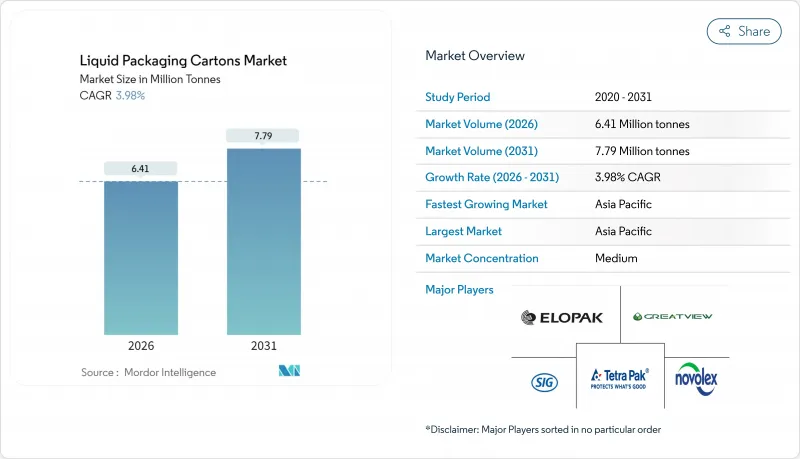

액체 포장용 카톤 시장은 2025년 616만 톤으로 평가되었고, 예측 기간(2026-2031년) CAGR 3.98%로 성장할 것으로 전망되며, 2026년 641만 톤에서 2031년까지 779만 톤에 이를 것으로 추정됩니다.

섬유계 소재를 권장하는 규제 기세, 보존 기간을 연장하는 장벽 기술의 혁신, 식료품 소매업의 급속한 디지털화가 성숙 경제권과 신흥 경제권 모두에서 액체 포장용 카톤 시장의 확대를 촉진하고 있습니다. 아시아태평양에서는 공공 영양 프로그램과 식품 접촉 규제의 진화로 상온 보존 가능한 포장에 대한 수요가 높아지고 가장 강한 성장이 예상됩니다. 동시에 유제품 및 식물성 음료에서 프리미엄화의 동향이 부가가치형 카톤 형식의 채용을 촉진하고 있습니다. 또한 지속가능성에 연동된 자금조달 채널이 섬유 소재의 혁신을 위한 자본을 이끌고 있습니다. 기존 기업은 탈탄소화 및 재활용 능력에 대한 대규모 투자로 점유율 방어를 도모하는 한편 지역 전문 기업이 현지 비용 우위성 및 민첩한 시장 진출 전략을 활용하고 있기 때문에 경쟁이 격화되고 있습니다.

인도네시아의 무료 영양식 프로그램을 통해 이 나라의 유제품 소비량은 2024년 420만 톤에서 2025년에는 530만 톤으로 증가하였고, 냉장이 불필요하고 열대 지역 물류에 견디는 무균 판지의 지속적인 수요 창출로 이어지고 있습니다. 중국의 GB 4,806 식품 접촉 규제는 적합 프리미엄을 높이고 인증받은 판지 공급자에게 액체 포장 판지 시장에서 가격 결정력을 부여합니다. 이러한 요인이 함께, 이 지역은 가치 및 수량의 성장에 있어서 주도적 입장을 강화해, 다국적 기업에 의한 현지 생산의 촉진이나 국내 가공업자와의 장기 공급 계약 체결을 뒷받침하고 있습니다. 중산 계급의 소득 증가는 상온 보존 가능한 유제품의 가정 보급을 더욱 가속화하고 있습니다. 이러한 요소가 종합적으로 작용하고 아시아태평양의 세계 액체 포장용 카톤 시장에 대한 기여도는 과거 평균을 크게 상회하는 수준에 도달했습니다.

온라인 식료품 시장은 2025년까지 세계 소매 시장의 61%를 차지한 것으로 평가되었고, 콜드체인의 복잡성을 없애고 배송 비용을 줄이는 상온 보존 제품에 대한 수요를 촉진하고 있습니다. 상온 보존 가능한 음료가 가장 혜택을 누리고 액체 포장용 카톤 시장은 전자상거래 효율화의 직접적인 추진역으로 자리매김하고 있습니다. 소매업체는 쌓을 수 있고 가볍고 재활용 가능한 섬유계 포장을 선호하고 있으며, 이러한 전환을 더욱 가속화하고 있습니다. 이러한 장점은 라스트마일의 배출량 및 정체가 포장 선택을 좌우하는 도시에서 특히 강력하게 지지되고 있습니다.

경량화가 진행되는 PET는 카톤의 라이프 사이클에 있어서의 탄소 우위성을 침식하고 있어, 음료 이용 사례에 따라서는 제조로부터 폐기까지의 차이가 1,000리터당 20kg CO2e 미만까지 축소하고 있습니다. PET에 재생 소재의 함유율이 높아짐에 따라, 코스트 퍼포먼스가 향상되어, 가격에 민감한 주스나 물 브랜드가 폴리머 병을 유지하는 유인이 되고 있습니다. 따라서, 특히 PET 생태계가 이미 잘 확립된 북미 및 EU 시장에서 카톤 공급업체는 대체품으로의 전환을 방지하기 위해 장벽 기술 혁신과 재활용률 향상을 가속화해야 합니다.

2025년 현재 액체 포장용 카톤 시장의 우유 점유율은 48.30%(약 300만 톤)를 유지했습니다. 그러나 비유제품 대체음료는 5.42%의 연평균 복합 성장률(CAGR)로 급성장하고 식습관 변화, 유당 불내증에 대한 배려, 윤리적 구매 행동 촉진으로 2031년까지 시장 점유율을 21.80%까지 확대될 전망입니다. 귀리, 아몬드, 간장 음료용 액체 포장용 카톤 시장 규모는 첨가물 없이 영양소를 보유하는 무균 가공 기술의 혜택을 누리고 있습니다. 전단 반응성 균질화 및 효소 보조 점도 제어와 같은 기술적 적응에는 산화에 의한 풍미 열화를 억제하는 견고한 배리어재가 요구됩니다. 이 때문에 컨버터는 필러와 협력하여 보존 기간 및 비용의 균형을 맞추는 커스터마이즈 사양을 개발하고 있습니다.

영양 강화 및 풍미 첨가를 실시한 프리미엄 처방은 제품 가치를 높이고 브랜드 소유자가 높은 비용의 종이 용기를 흡수 할 수 있습니다. 유제품은 소비 습관이 정착된 지역, 특히 정부 주도의 학생 영양 지원책이 실시되고 있는 지역에서는 여전히 중요합니다. 그러나 유제품 분야 내에서도 가치는 저지방 및 비타민 강화 제품으로 이행하고 있어 패키지 상의 스토리텔링을 가능하게 하는 고화질 인쇄 대응의 종이 용기가 선호되고 있습니다. 예측 기간 유제품 및 식물성 카테고리의 공존이 시장 규모를 서로 잠식하는 것이 아니라, 대상이 되는 액체 포장용 카톤 시장을 확대시킬 전망입니다.

액체 포장용 카톤 시장 보고서는 액체 유형별(유제품 베이스 우유, 비유제품 우유, 주스, 에너지 음료 및 기능성 음료 등), 포장 유형별(무균 카톤, 게이블 톱 카톤), 개구 형식별(스크류 캡, 스트로 홀, 풀 탭), 지역별(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)로 분류됩니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

아시아태평양은 2025년 출하량의 45.38%(약 280만 톤)를 차지했고, 5.92%의 연평균 복합 성장률(CAGR)로 2031년까지 395만 톤을 넘을 전망입니다. 확대의 배경은 인도네시아의 8,200만 명의 수혜자를 대상으로 한 학교급식 이니셔티브와 규제 기준의 강화에 따라 적합한 카톤 공급업체를 우대하는 중국의 동향을 들 수 있습니다. 동남아시아에서는 도시화가 진행되고, 외출처에서의 음료 수요가 가속되고 있어, 풀탭 및 소형 무균팩 수요를 뒷받침하고 있습니다.

북미는 성숙 시장이면서 고부가가치 분야에서 존재감을 나타내고 있습니다. 식물성 우유의 보급과 함께 점진적인 성장이 예상되는 반면, EPR 규제 강화는 국내 재활용 라인에 대한 투자를 촉진하고 있습니다. 유럽 수요는 안정적이며, 설탕세 개혁에 의한 제품 개량, PET보다 섬유 소재를 우선하는 ESG 대출이 지원하고 있습니다. 그러나, PET 용기의 경량화가 급속히 진행됨에 따라, 할인 프라이빗 브랜드 주스 시장에서의 액체 포장용 카톤의 점유율은 축소 경향에 있습니다.

라틴아메리카에서는 유제품 강화 프로그램과 확대되는 중산 계급의 구매력이 몰락하는 한편 통화 변동과 공급망 취약성이 최근 상승을 억제하고 있습니다. 중동 및 아프리카에서는 냉장 비용이 여전히 장벽이 되는 기후 하에서 상온 보존 가능한 포장이 유제품에 대한 접근을 지원하고, 완만하면서도 꾸준한 성장을 보이고 있습니다. 지역 분산화를 통해 세계의 액체 포장 판지 시장은 지역 충격의 영향을 완화하고 여러 대륙에 걸쳐 균형 잡힌 확장을 위한 기반을 구축하고 있습니다.

The liquid packaging cartons market was valued at 6.16 million tonnes in 2025 and estimated to grow from 6.41 million tonnes in 2026 to reach 7.79 million tonnes by 2031, at a CAGR of 3.98% during the forecast period (2026-2031).

Regulatory momentum favoring fiber-based materials, barrier-technology breakthroughs that prolong shelf life, and the rapid digitization of grocery retail are enlarging the liquid packaging cartons market footprint across both mature and emerging economies. Asia-Pacific delivers the strongest uplift as public nutrition programs and evolving food-contact rules deepen demand for ambient-stable packs. Simultaneously, premiumization trends in dairy and plant-based beverages advance the adoption of value-added carton formats, while sustainability-linked financing channels funnel capital toward fiber innovations. Competitive intensity is mounting as incumbents invest heavily in decarbonization and recycling capacity to defend share against regional specialists that exploit local cost advantages and agile market entry strategies.

Indonesia's Free Nutritious Meals Program pushes the nation's dairy intake from 4.2 million tonnes in 2024 to 5.3 million tonnes in 2025, generating sustained uptake of aseptic cartons that tolerate tropical logistics without refrigeration. China's GB 4806 food-contact rules elevate compliance premiums, granting certified carton suppliers pricing power within the liquid packaging cartons market. These forces reinforce the region's leadership in value and volume growth, encouraging multinationals to localize production and forge long-term supply contracts with domestic processors. Rising middle-class incomes further spur household penetration of shelf-stable dairy. Collectively, these factors lift Asia-Pacific's contribution to the global liquid packaging cartons market well above historic averages.

Online grocery is forecast to control 61% of global retail by 2025, channeling demand toward ambient products that remove cold-chain complexity and lessen fulfillment costs. Ambient-stable beverages benefit most, positioning the liquid packaging cartons market as a direct enabler of e-commerce efficiency. Retailers prioritize fiber-based packs that are stackable, lightweight, and recyclable, further reinforcing the shift. These advantages resonate strongly in urban zones where last-mile emissions and congestion drive packaging choices.

Lightweight PET advances erode cartons' life-cycle carbon lead, with cradle-to-grave differentials contracting under 20 kg CO2e per 1,000 litres in some beverage use cases.As PET incorporates higher recycled content, cost-performance ratios improve, tempting price-sensitive juice and water brands to retain polymer bottles. Carton suppliers must therefore accelerate barrier innovation and recycling rates to prevent substitution, especially in North American and EU markets where PET ecosystems are already well capitalized.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Dairy milk retained 48.30% share of the liquid packaging cartons market in 2025, translating to nearly 3 million tonnes. Non-dairy alternatives, however, outpaced with a 5.42% CAGR that will lift their contribution to 21.80% by 2031, propelled by dietary shifts, lactose-free preferences, and ethical purchasing drivers. The liquid packaging cartons market size for oat, almond, and soy beverages benefits from aseptic processing that preserves nutrients without additives. Technical adaptations, such as shear-sensitive homogenization and enzyme-assisted viscosity control, demand robust barrier materials to curb oxidative flavor degradation. Consequently, converters collaborate with fillers on customized specifications that balance shelf life and cost.

Premium formulations with fortification or added flavors increase product value, allowing brand owners to absorb higher carton costs. Dairy milk remains vital in regions with established consumption patterns, especially where government initiatives bolster student nutrition. Yet even within dairy, value migrates toward low-fat, vitamin-enriched products that favor cartons capable of high-graphic print for on-pack storytelling. Over the forecast horizon, the co-existence of dairy and plant-based categories broadens the addressable liquid packaging cartons market rather than cannibalizing volume.

The Liquid Packaging Cartons Market Report is Segmented by Liquid Type (Dairy-Based Milk, Non-Dairy Milk, Juices, Energy and Functional Drinks, and More), Packaging Type (Aseptic Cartons, and Gable Top Cartons), Opening Format (Screw Cap, Straw Hole, and Pull Tab), and Geography (North America, Europe, Asia Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Volume (Tonnes).

Asia-Pacific accounted for 45.38% of 2025 shipments, roughly 2.8 million tonnes, and its 5.92% CAGR positions the region to exceed 3.95 million tonnes by 2031. Expansion is driven by Indonesia's school meal initiative serving 82 million beneficiaries and China's elevated regulatory standards that reward compliant carton suppliers.Southeast Asian urbanization accelerates on-the-go beverage demand, boosting pull tab and small-format aseptic packs.

North America trails with a mature but high-value presence. Incremental growth aligns with plant-based milk adoption, while tightening EPR regulations spur investment in domestic recycling lines. European demand remains steady, underpinned by sugar-tax reformulation and ESG financing that favor fiber over PET. However, aggressive PET lightweighting erodes the liquid packaging cartons market share in discounted private-label juices.

Latin America benefits from dairy fortification programs and expanding middle-class purchasing power, yet currency volatility and supply-chain fragility curb immediate upside. The Middle East and Africa register modest but steady gains as ambient-stable packaging supports dairy access in climates where refrigeration costs remain prohibitive. Collectively, geography diversification cushions the global liquid packaging cartons market against regional shocks and positions the industry for balanced, multi-continent expansion.