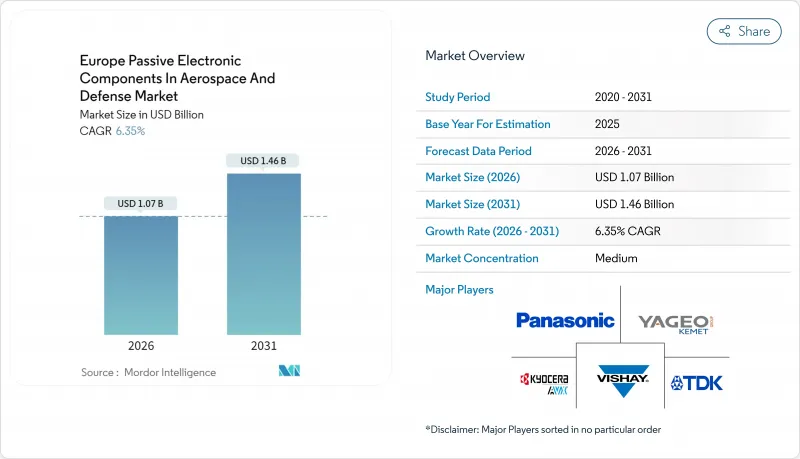

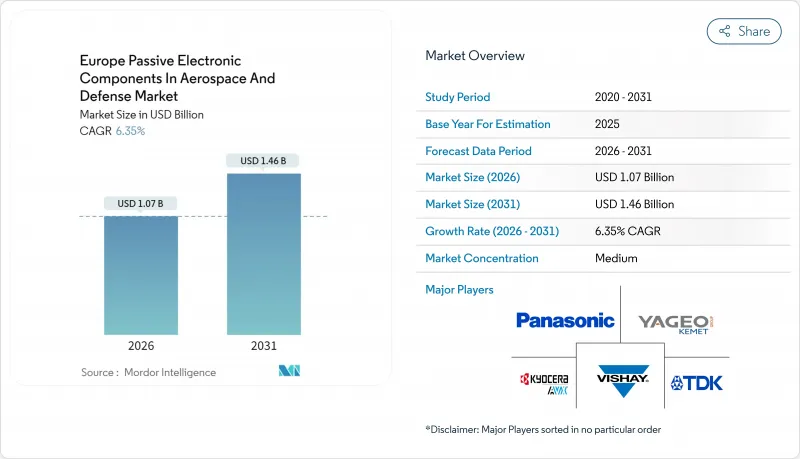

유럽의 항공우주 및 방위용 수동 전자부품 시장은 2025년에 10억 1,000만 달러로 평가되었으며, 2026년 10억 7,000만 달러에서 2031년까지 14억 6,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 6.35%로 예상됩니다.

방위 근대화 계획 증가, 소형 위성 별자리의 확대 및 전기항공기(MEA) 아키텍처로의 전환은 견고하고 신뢰성 있는 수동 부품에 대한 수요를 증가시키고 있습니다. 공급측의 기세는 유럽위원회의 'ReArm Europe' 이니셔티브에도 기인하고 있으며, 방위능력 강화를 위해 최대 8,000억 유로를 동원할 계획입니다. 이를 통해 엄격한 EU 현지 조달 규정을 충족하는 부품 공급업체에게 보다 광범위한 기회가 열릴 전망입니다. 플랫폼 수준에서는 상용 고정익 항공기가 여전히 지출의 대부분을 차지하고 있지만, 유럽 각국 정부 및 민간 사업자가 관측, 통신, 군사 감시를 위한 궤도 자산을 확대하는 가운데 위성 및 우주선이 현재 가장 빠른 단위 성장률을 나타내고 있습니다. 한편, 정책 주도의 현지화, GaN 파워 조사 및 드론 대비 요건이 경쟁의 틀을 재구축하고 있으며, 벤더는 지역적인 제조 거점을 강화하고 재료 혁신을 가속화할 수밖에 없는 상황이 되고 있습니다.

2024년에 3,260억 유로라는 역대 최고의 방위 예산이 계상되면서 고밀도 커패시터, 인덕터, 필터를 많이 사용하는 최첨단 아비오닉스, 레이더, 전자전(EW) 시스템의 조달을 가속화했습니다. 신규 무기 지출은 2021년 590억 유로에서 2024년에는 1,020억 유로로 급증했으며, 전술 라디오, 능동형 전자주사식 위상배열 레이더 및 디지털 비행 컴퓨터용으로 더 많은 인증 수동 부품이 공급되고 있습니다. 유럽 방위기금의 2025년도 사업계획(10억 6,500만 유로)에서는 공동센서 및 전자전(EW) 연구개발에 거액의 보조금을 할당하였으며, 유럽 벤더는 조기 설계 도입 기회를 선행하여 획득할 수 있습니다. 이와 더불어 2030년까지 방위조달 예산의 50%를 EU 공급업체에 유용한다는 정책 지침으로 프라임 기업은 지역의 수동 부품 전문기업과의 제휴를 강화하는 인센티브를 획득하여 유럽의 항공우주 및 방위용 수동 전자부품 시장의 구조적인 성장 경로가 강화되고 있습니다.

유럽이 마이크로위성 및 나노위성 별자리에 주력하는 움직임에 의해 매 발사마다 필요로 하는 내방사선성 수동 부품의 수가 배로 증가하고 있습니다. 유럽우주기구(ESA)는 2024년 뉴아테나 계획에 850만 유로, M7 미션 후보에 130만 유로를 계상했으며 이는 과학 및 안보 페이로드의 안정적인 공급 라인을 강조하고 있습니다. 부품 제조업체는 Exxelia사의 LEO 위성군 전용으로 특화한 MML 필름 커패시터의 상표 등록 등 소형화 및 밀폐 설계로 대응하고 있습니다. 소비자용과 방위용 촬영을 결합한 이중용도 위성은 이용 가능한 시장 규모를 더욱 확대하고 정부와 민간사업자 모두가 내장해성이 높은 우주 인프라를 추구하는 가운데 유럽의 항공우주 및 방위용 수동 전자부품 시장의 지속적인 성장을 뒷받침하고 있습니다.

탄탈광석은 정치적으로 불안정한 지역이 원산지인 경우가 많으며, 페라이트 원료는 중국의 가공 능력에 크게 의존하고 있습니다. 수출 규제를 둘러싼 긴장 증가는 스팟 가격 상승과 리드 타임의 장기화를 초래하고 있습니다. 유럽 기업은 안전 재고로의 자본 전환이나 대체 화학 물질의 모색을 요구받고 있으며, 유럽의 항공우주 및 방위용 수동 전자부품의 이익률은 압박되고 있습니다. EU의 중요 원재료법은 2030년까지 채굴의 10%, 가공의 40%를 지역 내에서 실시할 것을 목표로 하고 있지만, 당분간 불안정한 공급이 성장의 걸림돌이 되고 있습니다.

유럽의 항공우주 및 방위용 수동 전자부품 시장의 규모는 2025년에 커패시터가 4억 8,000만 달러에 달하면서 47.15%라는 압도적인 점유율을 차지했습니다. 세라믹 MLCC는 비행 제어 시스템, 레이더, 미사일 시커의 전력 무결성 및 디커플링 기능을 지원합니다. 체적 효율과 내방사선성에 따라 가격 변동에도 불구하고 확고한 지위를 유지하고 있습니다. 한편, 인덕터는 중동 및 아프리카(MEA)의 하위 부문에서 고밀도 파워 컨버터와 EMI 필터의 보급에 따라 7.05%의 연평균 복합 성장률(CAGR)로 보다 급속히 확대되고 있습니다. 박막 인덕터와 성형 파워 인덕터는 GaN 기반 컨버터 내에서 도입이 진행되고, 원환체 초크는 아비오닉스의 신호 라인을 간섭으로부터 보호하고 있습니다.

집적 수동 소자(IPD)는 저항 소자와 용량 소자를 알루미나 기판 상에 공배치함으로써 부문 간의 경계를 모호하게 하고 소형화와 신뢰성 향상을 실현하고 있습니다. AESA 레이더를 위한 신흥 RF 필터 어셈블리는 모놀리식 모듈 내에 공진기와 커패시터를 통합하여 인증 프로세스를 가속화합니다. 저항기, 변압기 및 RF 필터는 특히 정밀한 임피던스 매칭이 필수적인 전자전 포드용 틈새 시장에서 중요한 역할을 유지합니다. 부문 횡단적인 역동성은 유럽의 항공우주 및 방위용 수동 전자부품 시장에서 광범위한 기반을 지원하는 꾸준한 다양화의 길을 뒷받침합니다.

세라믹 기술은 MLCC, 공진기, 기판 등의 폭넓은 용도로 2025년 유럽의 항공우주 및 방위용 수동 전자부품 시장 점유율의 53.10%를 차지했습니다. 첨단 티타네이트 바륨 배합 기술은 군용 온도 범위 전체에서 안정된 유전율을 실현하고, 고온 공소성 세라믹은 임베디드 수동 부품을 지원합니다. 탄탈은 뛰어난 체적 용량에 의해 6.56%의 연평균 복합 성장률(CAGR)로 가장 빠른 성장이 예상되며, 특히 위성이나 미사일의 포인트 오브 로드 변환기에서 체적 효율과 서지 내성이 비용 증가를 상회하는 상황에서 우위성을 발휘합니다.

알루미늄 전해 커패시터는 항공기 탑재 레이더 프로세서 내의 대용량 에너지 저장에 필수적으로 사용되고 있지만, 125°C를 넘는 온도 영역에서의 수명 단축에 의해 엔진 베이에서의 사용은 제한되고 있습니다. PPS 및 PTFE 필름을 도입한 필름 커패시터는 지향성 에너지 연구나 우주 추진 장치에서의 펄스 전원 코일에 활용되고 있습니다. 페라이트 재료는 전자전 수신기의 원환체 인덕터와 광대역 트랜스포머를 뒷받침하고 있지만 공급 리스크에 의해 벤더는 망간 아연 대체품을 고려하고 있습니다. 그 결과, 재료의 다양성은 지정학적 변동에 대한 헤지 역할을 하며 유럽의 항공우주 및 방위용 수동 전자부품 시장의 성장세를 유지하고 있습니다.

The Europe passive electronic components in aerospace and defense market was valued at USD 1.01 billion in 2025 and estimated to grow from USD 1.07 billion in 2026 to reach USD 1.46 billion by 2031, at a CAGR of 6.35% during the forecast period (2026-2031).

Rising defense modernization programmes, expanding small-satellite constellations, and the transition toward More-Electric-Aircraft architectures are intensifying demand for rugged, high-reliability passive parts. Supply-side momentum also stems from the European Commission's ReArm Europe initiative, which will mobilize up to EUR 800 billion for defense capability enhancement, opening wider opportunities for component suppliers that can meet stringent EU localization rules. At platform level, commercial fixed-wing aircraft still dominate spend, yet satellites and spacecraft now post the fastest unit growth as European governments and private operators scale orbital assets for observation, connectivity, and military surveillance. Meanwhile, policy-driven localization, GaN power research, and anti-drone requirements are reshaping the competitive playbook, compelling vendors to deepen regional manufacturing footprints and accelerate material innovation.

Record defense allocations of EUR 326 billion in 2024 accelerated procurement of cutting-edge avionics, radars, and EW suites that consume dense arrays of capacitors, inductors, and filters. New armaments spending jumped from EUR 59 billion in 2021 to EUR 102 billion in 2024, channeling larger volumes of qualified passives into tactical radios, active-electronically-scanned-array radars, and digital flight computers. The European Defence Fund's EUR 1.065 billion 2025 Work Programme earmarks sizable grants for collaborative sensor and EW R&D, giving European vendors a head-start on early design-in opportunities. In parallel, a policy mandate that 50% of defense procurement budgets flow to EU suppliers by 2030 incentivizes primes to deepen ties with regional passive specialists, reinforcing the Europe passive electronic components in aerospace and defense market's structural growth path.

Europe's pivot toward constellations of micro and nano-satellites multiplies the number of radiation-tolerant passives required per launch. The European Space Agency set aside EUR 8.5 million for NewAthena and EUR 1.3 million for M7 mission candidates in 2024, underscoring a steady pipeline of science and security payloads. Component makers are responding with miniaturized, hermetic designs such as Exxelia's Trademarked MML film capacitors tailored to LEO constellations. Dual-use satellites that combine civil and defense imagery further expand total available market, positioning the Europe passive electronic components in aerospace and defense market for sustained upside as both governments and commercial operators pursue resilient space infrastructures.

Tantalum ore often originates from politically unstable regions, while ferrite raw materials depend heavily on Chinese processing capacity. Heightened tension around export controls raises spot prices and lengthens lead times. European firms must divert capital toward safety stock and explore alternate chemistries, squeezing margins within the Europe passive electronic components in aerospace and defense market. The EU's Critical Raw Materials Act aims to localize 10% of extraction and 40% of processing by 2030, yet interim volatility remains a drag on growth.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The Europe passive electronic components in aerospace and defense market size for capacitors reached USD 0.48 billion in 2025, translating to a dominant 47.15% share. Ceramic MLCCs underpin power-integrity and decoupling functions across flight controls, radar, and missile seekers. Their volumetric efficiency and radiation tolerance keep them entrenched despite price swings. Inductors, however, are scaling faster at a 7.05% CAGR as high-density power converters and EMI filters proliferate in MEA subsystems. Thin-film and molded power inductors gain traction inside GaN-based converters, while toroidal chokes secure avionics signal lines against interference.

Integrated Passive Devices (IPDs) are blurring categorical lines by co-locating resistive and capacitive elements onto alumina substrates, shrinking size and boosting reliability. Emerging RF filter assemblies for AESA radar merge resonators and capacitors within monolithic modules to expedite qualification. Resistors, transformers, and RF filters sustain niche but critical roles, particularly in electronic warfare pods where precision impedance matching is essential. The aggregate dynamism across categories confirms a steady diversification path underpinning the broader Europe passive electronic components in aerospace and defense market.

Ceramic technology captured 53.10% of the Europe passive electronic components in aerospace and defense market share in 2025 thanks to its wide utility across MLCCs, resonators, and substrates. Advanced barium-titanate formulations deliver stable dielectric constants across military-temperature ranges, while high-temperature cofired ceramics support embedded passives. Tantalum's superior volumetric capacitance positions it for fastest growth at 6.56% CAGR, particularly within point-of-load converters on satellites and missiles where volumetric efficiency and surge reliability outweigh cost premiums.

Aluminum electrolytics remain indispensable for bulk energy storage inside airborne radar processors, though life-time derating above 125 °C limits their use in engine bays. Film capacitors leveraging PPS and PTFE films cater to pulse-power coils in directed-energy research and space propulsion. Ferrite materials underpin toroidal inductors and broadband transformers in EW receivers, yet supply risk forces vendors to qualify manganese-zinc substitutes. Consequently, material diversity acts as a hedge against geopolitical volatility, sustaining momentum for the Europe passive electronic components in aerospace and defense market.

The Europe Passive Electronic Components in Aerospace and Defense Market Report is Segmented by Type (Capacitors, Resistors, Inductors, and More), Material (Ceramic, Tantalum, Aluminum Electrolytic, Film, Ferrite, and More), Platform (Commercial Fixed-Wing Aircraft, Military Fixed-Wing Aircraft, Rotorcraft and More), End-User (OEM Production Lines, and MRO), and Geography. The Market Forecasts are Provided in Terms of Value (USD).