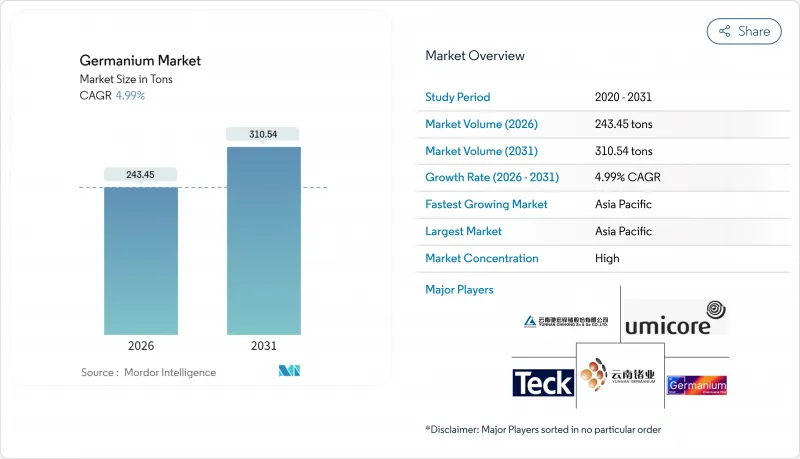

2026년 게르마늄 시장 규모는 243.45톤으로 추정되며, 2025년 231.88톤에서 성장할 전망입니다. 2031년 예측치는 310.54톤으로 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 4.99%로 성장할 전망입니다.

가격 상승세는 이러한 성장 경로를 뒷받침한다 : 중국이 수출 규제를 확대함에 따라 현물 가격은 2025년 3월 kg당 4,150달러로 치솟았으며, 이는 2023년 1월 대비 75% 급등한 수치다. 수요는 게르마늄의 광학적·전기적 특성이 높은 비용을 상쇄하는 고성능 용도에 집중됩니다. 광섬유 인프라 구축, 항공우주용 태양광 패널, 양자 연구 분야 모두 소비량이 증가하는 가운데, 국방 기관들은 공급 리스크를 억제하기 위해 국내 웨이퍼 생산 능력 확충에 투자하고 있습니다. 아연 제련의 부산물이라는 게르마늄의 특성으로 인해 생산이 가격 급등에 신속히 대응하기 어려운 점도 지속적인 공급 부족을 부각시킵니다. 이러한 요인들이 복합적으로 작용하여 세계의 게르마늄 시장은 수요 주도적이지만 지정학적 민감성을 지닌 확장 국면을 맞이하고 있습니다.

5G 백홀을 확장하고 6G 프로토타입을 시험 중인 통신 사업자들은 대륙 간 거리에서 신호 강도를 유지하기 위해 게르마늄 도핑 실리카에 의존합니다. 이 소재의 높은 굴절률 대비는 초저손실 광섬유에 있어 타의 추종을 불허하며, 장거리 회선에서의 대체를 불가능하게 합니다. 따라서 네트워크 고밀도화는 킬로미터당 도핑 부하량이 감소함에도 불구하고 총 사용량을 증가시킵니다. 2023년 이후 중국의 전략적 비축량 증가와 허가 강화는 서구 통신사들의 안보 우려를 증폭시켜, 비중국 정제 경로 확보를 위한 병행 노력을 촉발했습니다. 일본과 미국의 대형 프리폼 시설 투자 확대는 데이터 트래픽 증가 속에서 게르마늄 시장의 지속적인 상승세를 시사합니다.

게르마늄의 8-12μm 투과성은 운전자 보조 카메라부터 공장 검사 렌즈까지 열화상 활용 사례를 열어줍니다. 2024년부터 신차에 운전자 모니터링 기능을 의무화하는 EU 규정이 채택을 가속화합니다. 칼코겐화물 유리가 더 저렴한 대안이지만, 투과 효율과 환경 안정성에서 게르마늄에 뒤쳐져 OEM들은 프리미엄 안전 시스템에 게르마늄 광학 제품을 계속 사용합니다. 산업 유지보수 분야에서도 적외선 창이 부식성 환경을 견디는 데 활용되며 수요가 발생합니다.

중국은 2024년 1차 게르마늄의 65% 이상을 채굴 또는 정제했으며, 2024년 12월 미국으로의 직접 수출 금지는 이러한 집중도가 부여하는 영향력을 보여주었습니다. 미국 지질조사국(USGS)은 전면 금수조치가 미국 GDP를 34억 달러 감소시킬 것으로 전망하며, 이 중 40%가 반도체 제조에 영향을 미칠 것이라고 분석해 핵심 공급망의 취약성을 부각시켰습니다. 벨기에의 우미코어(Umicore)와 콩고민주공화국(DRC)의 STL이 연간 30톤 규모의 공장을 확장 중이지만, 생산량이 여전히 부족해 장기적인 공급 중단을 상쇄하기에는 역부족입니다.

이산화게르마늄이 차지하는 게르마늄 시장 규모는 전체 물량의 30.08%를 기록하며 광섬유 프리폼 및 촉매 생산의 핵심 중간재로서의 입지를 공고히 했습니다. 수요는 통신 케이블 배치 패턴을 따라가며 이 부문에 안정적이면서도 완만한 성장 경로를 제공합니다. 중국 및 벨기에 공장의 용매 추출 회로 개선으로 회수율이 상승하면서 연소 먼지로부터 확보 가능한 원료 공급량이 소폭 확대되고 있습니다.

양자 등급 결정 성장업체들이 화학기상증착(CVD) 반응기에 사용되는 초저습·초순도 전구체를 조달함에 따라, 사염화게르마늄은 2031년까지 연평균 5.54% 성장할 것으로 전망됩니다. 클로라이드 공정 화학이 높은 화학량론적 제어력을 제공하는 레이저 광학 코팅 분야에서도 틈새 시장 규모를 형성합니다. 일반적으로 11N 순도로 구역 정제된 잉곳은 적외선 렌즈 블랭크 및 고주파 트랜지스터 기판에 사용됩니다. 연간 10톤 미만의 수요로 인해 이 등급 시장은 공급이 제한적이며, 가격 프리미엄이 통합 생산업체를 원자재 가격 변동으로부터 보호합니다. 사불화게르마늄 및 요오드화게르마늄과 같은 기타 게르마늄 화합물은 여전히 실험실 규모에 머물며, 더 넓은 상업적 검증을 기다리고 있습니다.

게르마늄 시장 보고서는 유형별(이산화게르마늄, 사염화게르마늄, 게르마늄 잉곳 등), 용도별(광섬유 시스템, 적외선 광학, 중합 촉매, 전자기기, 태양전지, 기타 용도), 지역별(아시아태평양, 북미, 유럽, 세계 기타 지역)으로 분류됩니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

아시아태평양 지역은 2025년 기준 58.80%의 점유율로 게르마늄 시장을 주도했으며, 이는 아연 제련소 침출 잔여물을 6N 등급 이상의 금속으로 전환하는 수직 통합형 중국 생산업체들의 지원에 힘입은 결과입니다. 통신사들의 5G 구축 완료와 반도체 팹의 고대역폭 메모리 생산 확대에 힘입어 2031년까지 지역 소비량은 연평균 5.53% 성장할 전망입니다. 중국의 ‘전략적 소재 2035’ 프로그램 하의 정부 인센티브는 13N 결정 인발 라인 업그레이드를 지원하여 현지 생산 역량 우위를 강화하고 있습니다.

북미는 초순도 웨이퍼 확보를 최우선으로 하는 방위 및 우주 계약 덕분에 시장 내 입지를 크게 강화했습니다. 5N 플러스와 텍 리소스가 국내 원료를 공급하지만, 공급망 리스크를 완전히 해소하기에는 물량이 여전히 부족합니다. 2024년 워싱턴의 국방생산법 할당으로 추가 정제로 건설 타당성 조사가 촉진되며, 정책 주도형 지역 게르마늄 시장 확대 신호가 켜졌습니다.

유럽은 벨기에, 독일, 폴란드 공장에서 소량 생산하며 나머지는 주로 중국에서 수입합니다. 2024년 6월 채택된 EU 핵심 원자재법은 2030년까지 수입 의존도를 65%로 제한하고 재활용 시범 사업에 자금을 배정합니다. 우미코어의 콩고민주공화국 합작사는 2024년 10월 첫 5톤 분량을 출하하며 초기 진전을 보였다. 나미비아, 카자흐스탄 등 기타 지역에도 자원 잠재력이 있으나 환경 및 순도 기준 충족을 위해 상당한 자본이 필요합니다.

Germanium market size in 2026 is estimated at 243.45 tons, growing from 2025 value of 231.88 tons with 2031 projections showing 310.54 tons, growing at 4.99% CAGR over 2026-2031.

Price momentum underscores this growth path: spot quotations climbed to USD 4,150 per kg in March 2025, a 75% jump from January 2023, after China widened its export curbs. Demand concentrates in high-performance uses where germanium's optical and electrical properties outweigh elevated costs. Fiber-optic infrastructure roll-outs, aerospace solar arrays, and quantum research all consume rising volumes, while defense agencies fund new domestic wafer capacity to contain supply risk. Ongoing tightness is accentuated by germanium's status as a by-product of zinc smelting, which limits the speed with which production can respond to price spikes. Together these forces anchor a demand-driven but geopolitically sensitive expansion for the global germanium market.

Telecom operators expanding 5G backhaul and trialing 6G prototypes rely on germanium-doped silica to preserve signal strength over transcontinental distances. The material's high refractive-index contrast is unmatched for ultra-low-loss fibers, keeping substitution infeasible for long-haul lines. Network densification, therefore, lifts tonnage even as dopant loadings per kilometer fall. China's strategic stock build and tighter licensing since 2023 amplified security concerns among Western carriers, prompting parallel efforts to qualify non-Chinese refining routes. Investments in larger preform facilities in Japan and the United States indicate sustained upside for the germanium market amid data-traffic growth.

Germanium's 8-12 μm transparency opens thermal-imaging use cases from driver-assist cameras to factory inspection lenses. EU regulations that require driver-monitoring features in new models from 2024 accelerate adoption. While chalcogenide glasses offer a cheaper alternative, they lag germanium in transmission efficiency and environmental stability, keeping OEMs anchored to germanium optics for premium safety systems. Parallel demand comes from industrial maintenance, where infrared windows withstand corrosive conditions.

China mined or refined more than 65% of primary germanium in 2024, and its December 2024 ban on direct shipments to the United States showcased the leverage that concentration confers. The USGS projects that a full embargo would cut U.S. GDP by USD 3.4 billion, 40% of which would fall on semiconductor fabrication, underlining exposure along critical supply chains. Belgium's Umicore and DRC-based STL are scaling a 30 tpy plant but volumes remain too small to offset a prolonged suspension.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The germanium market size attributed to germanium dioxide accounted for 30.08% of total volume, cementing its role as the workhorse intermediate for optical-fiber preforms and catalyst production. Demand tracks telecom cable deployment patterns, giving this segment a stable yet moderate growth path. Improving solvent-extraction circuits in Chinese and Belgian plants are lifting recovery yields, marginally expanding accessible feedstock from flue dusts.

Germanium tetrachloride is projected to grow at 5.54% CAGR through 2031 as quantum-grade crystal growers source ultra-dry, ultrapure precursor for chemical-vapor-deposition reactors. Niche volumes also serve laser-optic coatings where chloride-route chemistry delivers high stoichiometric control. Ingots, typically zone-refined to 11N purity, fulfill infrared lens blanks and high-frequency transistor substrates. Their sub-10 ton annual requirements keep this tier tight, with pricing premiums shielding integrated producers from commodity swings. Other germanium chemicals such as tetrafluoride and iodide remain laboratory-scale, awaiting broader commercial validation.

The Germanium Market Report is Segmented by Type (Germanium Dioxide, Germanium Tetrachloride, Germanium Ingots, Other Types), Application (Fiber Optics System, Infrared Optics, Polymerisation Catalysts, Electronics, Solar Cells, Other Applications), and Geography (Asia-Pacific, North America, Europe, Rest of the World). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific dominated the germanium market with a 58.80% share in 2025, supported by vertically integrated Chinese producers that convert zinc-smelter leach residues into 6N metal and higher. Regional consumption will climb at a 5.53% CAGR through 2031 as telecom carriers complete 5G roll-outs and semiconductor fabs ramp high-bandwidth memory production. Government incentives under China's "Strategic Materials 2035" program subsidize upgrades to 13N crystal pulling lines, reinforcing local capacity advantages.

North America has significantly strengthened its position in the market due to defense and space contracts, which prioritize guaranteed access to ultra-pure wafers. 5N Plus and Teck Resources furnish domestic feed, but volumes remain insufficient to fully de-risk the supply chain. Washington's Defense Production Act allocations in 2024 spurred feasibility studies for additional refining furnaces, signaling a policy-driven uptick in the region's germanium market.

Europe relies on Belgian, German, and Polish plants for modest production, importing the remainder mainly from China. The EU Critical Raw Materials Act, adopted in June 2024, sets a 65% import-dependency ceiling by 2030 and earmarks funding for recycling pilots. Early progress is visible in Umicore's DRC joint venture, which shipped its first 5-ton batch in October 2024. Rest-of-World locations such as Namibia and Kazakhstan host resource prospects but require significant capital to meet environmental and purity benchmarks.