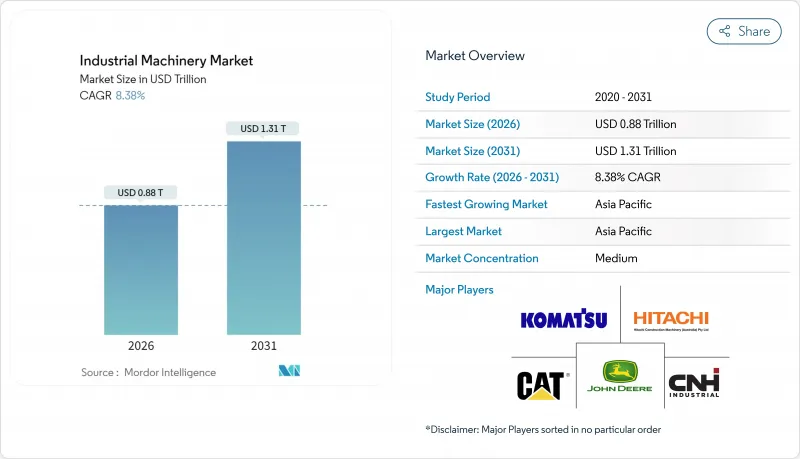

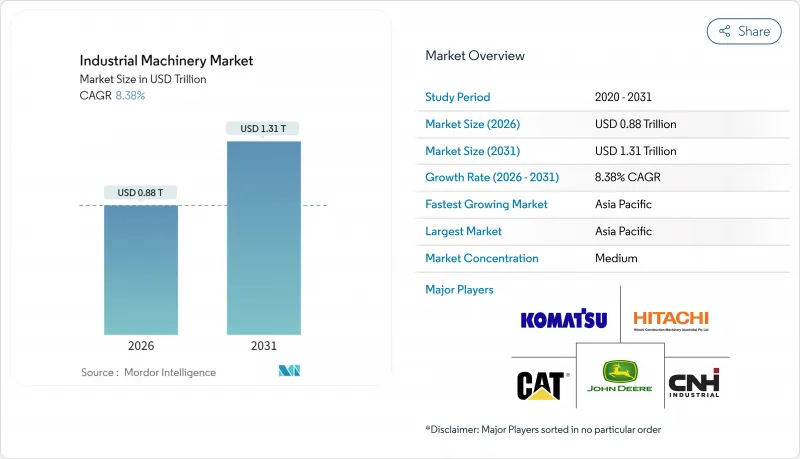

산업기계 시장은 2025년 8,100억 달러에서 2026년 8,800억 달러로 성장할 것으로 예측되고, 2026년에서 2031년까지 연평균 복합 성장률(CAGR) 8.38%로 성장을 지속하여 2031년까지 1조 3,100억 달러에 달할 것으로 예측되고 있습니다.

이 확장은 지속적인 인프라 투자, 가속화된 공장 자동화, 그리고 무공해 장비의 점진적 보급을 반영했습니다. 최종 사용자들은 계획되지 않은 가동 중단을 억제하기 위해 인공지능 기반 예측 유지보수 플랫폼에 대한 지출을 늘렸으며, 제조업체들은 납기 단축을 위해 모듈식 기계 설계를 추구했습니다. 아시아태평양 지역은 2024년 중국과 인도의 급속한 생산능력 확대로 압도적인 선두를 유지했습니다. 북미 및 유럽 구매자들은 제품 라인 간 신속한 전환이 가능한 리쇼어링 대응형 다중 공정 기계에 집중하여 국내 공급망 회복탄력성을 지원했습니다. CNC 및 로봇공학 분야 숙련된 인력 부족은 자동화 수요를 높게 유지했으며 초기 자본 투자를 낮추는 서비스형 장비(EaaS) 모델을 촉진했습니다.

세계의 제조업체들은 가동 중단 시간을 줄이고 처리량을 향상시키기 위해 센서, 클라우드 분석, 디지털 트윈을 도입했습니다. 지멘스의 센세이(Senseye) 플랫폼은 분당 100만 개 이상의 기계 데이터 포인트를 처리하여 예측 정확도를 85% 향상시키고 유지보수 비용을 최대 40% 절감했습니다. 장비 제조사들은 새로운 구독 수익을 창출하고 Equipment-as-a-Service 계약을 가능하게 하는 엣지 분석 모듈을 내장했습니다. 디지털 트윈은 운영자가 생산 중단 없이 사이클 타임 변경을 테스트할 수 있게 하여 자본 업그레이드의 정당성을 입증하는 데 도움을 줍니다. 이러한 기능들은 더 빠른 투자 회수를 이끌어냈으며, 예산이 부족한 중형 공장들도 자동화를 도입하도록 장려했습니다. 사이버 보안 인식의 증가는 공급업체들이 기기 내 암호화와 네트워크 분할을 통해 기계 제어기를 강화하도록 촉발했습니다.

아시아태평양 및 중동 지역의 다년간 공공사업 예산은 토공 기계, 크레인, 콘크리트 장비 주문 증가를 지속해서 견인했습니다. 배터리 구동 소형 로더는 진화하는 저배출 및 소음 규제를 충족하여 도시 작업 현장에서 주목받았습니다. CASE 건설 장비의 12EV 전기 소형 휠 로더는 23kWh 배터리로 1.15톤 적재량을 제공하면서 배기 가스를 완전히 제거했습니다. 건설사들은 대형 굴삭기에 하이브리드 구동계를 도입해 공회전 시 연료 소비를 줄였다. OEM 연계 리스 업체의 유연한 금융 패키지와 잔존 가치 보증은 건설사들이 높은 초기 구매 비용을 상쇄하는 데 도움을 주며 수요를 더욱 강화했습니다.

고정밀 다기능 선반과 자동 용접 셀의 초기 구매 가격은 많은 중소 규모 공장의 구매를 주저하게 했습니다. 캐터필러는 경제 불확실성 속에서 일부 고객이 장비 교체를 연기하면서 2025년 1분기 매출이 전년 동기 대비 10% 감소한 142억 달러를 기록했습니다. 계획되지 않은 가동 중단 시간은 여전히 생산 비용의 평균 24%를 차지하여 노후 자산의 재정적 위험을 부각시켰습니다. OEM 업체들은 구매자가 기계 가동 시간당 비용을 지불하고 유지보수, 소프트웨어, 소모품을 묶어 제공하는 구독 모델을 도입했습니다. SKF의 ‘Everything-as-a-Service’ 서비스는 공장이 베어링 소유권이 아닌 성능에 대해 비용을 지불하도록 하여 재무제표 부담을 완화했습니다.

2025년 토목 건설기계는 세계의 고속도로 및 주택 및 에너지 프로젝트의 진전에 따라 산업기계 시장 점유율의 30.85%를 차지했습니다. 고출력 불도저와 굴삭기는 대량의 토공 작업에 필수적이었지만, 함대 갱신이 완료된 성숙 시장에서는 수요가 두드러졌습니다. 산업용 로봇과 자동화 셀은 가장 성장이 빠른 제품군으로 2031년까지 연평균 복합 성장률(CAGR) 12.57%로 확대하고 있습니다. 제조업체가 작업원과 안전하게 협동하는 협동 로봇을 채택함으로써 설치 기반는 165억 달러에 달했습니다. 서비스로서의 로봇(RoA) 계약의 보급에 의해 초기 비용이 삭감되고, 소규모의 작업장에서도 시각 유도 암을 이용한 픽 앤 플레이스 작업이 가능하게 되었습니다. 컴프레서와 펌프는 에너지 비용을 줄이는 가변 속도 구동 장치로 업그레이드함으로써 혜택을 받았으며 판매 증가를 지원했습니다.

장비 제조사들은 모션 컨트롤러에 인공지능을 통합해 사이클 시간을 단축하고 픽킹 정확도를 개선했습니다. 테슬라의 기가팩토리 자동화 모델은 자동차 제조사들에게 고정형 로봇과 자율 이동 로봇을 결합해 수요에 따라 부품을 공급함으로써 작업 중 재고량을 줄이는 방식을 고무했습니다. 물류 처리 장비는 고처리량 컨베이어와 분류기가 필요한 전자상거래 물류센터로부터 꾸준한 수요를 유지했습니다. 농업 기계도 정밀 살포 시스템과 농촌 노동력 부족 문제를 해결하는 자율 주행 트랙터의 도움으로 발전했습니다. 제품 부문은 실내 물류를 위한 전동 텔레핸들러, 도시 고층 건설용 하이브리드 크롤러 크레인 등 특수 기계가 출시되며 다각화를 지속했습니다.

건설 분야는 2025년 산업기계 시장 규모에서 29.12%로 최대 응용 분야 점유율을 유지했으며, 이는 교통망 현대화와 공공시설 확장이 지속되고 있음을 반영합니다. 시공사는 도시 프로젝트에 저소음·무공해 기계를 우선적으로 도입하며 단순 출력을 넘어선 새로운 사양 기준을 창출했습니다. 농업 분야는 연평균 10.71%의 가장 빠른 성장률을 기록했습니다. 자동 조향 트랙터, 드론 유도 살포기, 스마트 수확기는 수확량 증대와 동시에 화학 투입량을 감소시켰습니다. 디어 앤 컴퍼니는 농업 인력 부족 완화를 위한 자율주행 기술 도입을 위해 미국 공장 투자에 200억 달러를 배정했습니다. 식품 가공 시설은 인공 시각 기술을 활용해 폐기물을 줄이며 팔레타이징과 품질 검사를 자동화했습니다.

자동차 제조업체들은 전기차 생산 능력을 확대하고 배터리 케이스용 고정밀 레이저 절단 시스템을 설치했습니다. 화학 및 제약 공장들은 원격 모니터링이 가능한 현장 세척식 스키드 패키지를 도입해 강화된 안전 및 추적성 규정을 충족했습니다. 섬유 생산 업체들은 소형 로봇을 도입해 봉제 라인을 자동화하며 해외 생산 이전 추세를 역전시켰습니다. 발전 프로젝트, 특히 풍력 터빈 설치 및 그리드 규모 배터리 조립에는 특수 제작된 자재 취급 장비가 필요했습니다. 인쇄 업체들은 인쇄기 활용도를 최적화하기 위해 인더스트리 4.0 워크플로우 소프트웨어를 도입하며 모듈식 후가공 장비 시장을 확대했습니다. 각 응용 분야는 맞춤형 자동화를 요구했으며, 이는 광범위한 장비 판매의 기반이 되었습니다.

아시아태평양 지역은 2025년 매출 점유율 42.35%를 유지하며 8.42%의 연평균 성장률(CAGR)을 기록, 산업기계 시장에서의 지배력을 강화했습니다. 중국 자동화 공급업체들은 경쟁력 있는 서보 드라이브와 PLC를 도입하여 현지화된 가격 경쟁력을 확보, 수입 브랜드에 도전장을 내밀었습니다. 인도의 생산 연계 인센티브 제도는 기계 수입을 지원하고 국내 생산을 위한 합작 투자를 장려했습니다. 일본과 한국은 초정밀 로봇 및 반도체 장비에 집중하여 높은 단가를 유지했습니다. 대만의 계약 전자 제조는 표면 실장 및 검사 장비에 대한 지속적인 투자를 필요로 하여 특수 피더 및 카메라에 대한 수요를 유지했습니다.

유럽은 에너지 비용 상승에 맞서 경쟁력을 유지하기 위해 다중 공정 기계에 투자하는 기업들로 꾸준한 수요를 보였다. 독일 건설사들은 동유럽 자동차 및 가전 공장에 고정밀 성형 프레스를 공급했습니다. 스칸디나비아 목재 가공 공장들은 통나무당 수율을 최적화하는 지능형 톱 라인을 설치했습니다. 영국은 무공해 건설 기계에 대한 보조금을 도입해 도시 재개발 현장에서 소형 전기 굴삭기 채택을 촉진했습니다. 유럽의 수리·유지보수·정비 부문은 운영사들이 예측 분석을 통해 기계 수명을 연장하면서 성장했습니다.

남미, 중동, 아프리카는 새로운 성장 분야가 되었습니다. 브라질 인프라 개선 사업에는 대규모 토공 장비와 콘크리트 펌프가 필요했으나 환율 변동성으로 수입이 제한되었습니다. 히타치 건설기계와 마루베니는 브라질에 광산 장비 서비스 합작사를 설립해 현지화 지원과 가동 중단 시간 단축을 도모했습니다. 걸프협력회의(GCC) 국가들은 담수화 및 재생에너지 프로젝트에 투자하며 부식 방지 펌프와 대용량 크레인을 필요로 했습니다. 아프리카 정부들은 트랙터 구매 보조금을 통해 농업 기계화를 우선시하여 저출력 기계 판매를 지원했습니다.

The industrial machinery market is expected to grow from USD 0.81 trillion in 2025 to USD 0.88 trillion in 2026 and is forecast to reach USD 1.31 trillion by 2031 at 8.38% CAGR over 2026-2031.

Expansion reflected sustained infrastructure investment, accelerated factory automation, and the growing availability of zero-emission equipment. End-users increased spending on artificial-intelligence-enabled predictive maintenance platforms to curb unplanned downtime, while manufacturers pursued modular machine designs to shorten delivery cycles. Asia-Pacific held a commanding lead in 2024, helped by rapid capacity additions in China and India. North American and European buyers focused on reshoring-ready, multi-process machines that can switch quickly between product lines, supporting domestic supply-chain resilience. Tight skilled-labor pools for CNC and robotics roles kept automation demand elevated and encouraged Equipment-as-a-Service models that lower initial capital needs.

Manufacturers worldwide adopted sensors, cloud analytics, and digital twins to curb downtime and enhance throughput. Siemens' Senseye platform processed more than 1 million machine data points per minute and lifted forecast accuracy by 85%, cutting maintenance costs by as much as 40%. Equipment builders embedded edge analytics modules that unlock new subscription revenue and enable Equipment-as-a-Service contracts. Digital twins let operators test cycle-time changes without stopping production, helping to justify capital upgrades. These capabilities drove faster paybacks and encouraged mid-sized plants to adopt automation despite tight budgets. Rising cybersecurity awareness prompted vendors to harden machine controllers with on-device encryption and network segmentation.

Multi-year public-works budgets in Asia-Pacific and the Middle East continued to boost orders for earth-moving machines, cranes, and concrete equipment. Battery-powered compact loaders gained traction on urban job sites because they meet evolving low-emission and noise regulations. CASE Construction Equipment's 12EV electric compact wheel loader delivered a 1.15-ton payload using a 23 kWh battery while eliminating exhaust emissions . Contractors also adopted hybrid drivetrains in large excavators to cut fuel consumption during idling. Flexible finance packages and residual-value guarantees from OEM-linked leasing units helped contractors offset high upfront prices, further strengthening demand.

Initial purchase prices for high-precision multitasking lathes and automated welding cells deterred many small plants. Caterpillar recorded a 10% year-over-year sales decline to USD 14.2 billion in Q1 2025 as some customers delayed fleet renewals amid economic uncertainty. Unplanned downtime still averaged 24% of production costs, underscoring the financial risk of older assets. OEMs introduced subscription models where buyers pay per machine-hour, bundling maintenance, software, and consumables. SKF's Everything-as-a-Service offering let factories pay for bearing performance instead of ownership, easing balance-sheet pressure.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Earth-moving equipment captured 30.85% of industrial machinery market share in 2025 as global highway, housing, and energy projects progressed. High-horsepower dozers and excavators remained essential for bulk earthworks, but demand plateaued in mature markets where fleets had been refreshed. Industrial robots and automation cells were the fastest-growing product, advancing at a 12.57% CAGR toward 2031. The installed base reached USD 16.5 billion as manufacturers adopted collaborative robots that work safely next to operators. Wider use of Robot-as-a-Service contracts reduced upfront costs, permitting small job-shops to deploy vision-guided arms for pick-and-place tasks. Compressors and pumps benefited from upgrades to variable-speed drives that lower energy bills, supporting incremental sales.

Equipment builders integrated artificial intelligence into motion controllers to cut cycle times and improve pick accuracy. Tesla's gigafactory automation model inspired automakers to blend fixed robots with autonomous mobile robots that deliver parts on demand, trimming work-in-progress inventory. Material-handling equipment held steady demand from e-commerce fulfillment centers that required high-throughput conveyors and sorters. Agricultural machinery also advanced, helped by precision spraying systems and autonomous tractors that address rural labor shortages. The products segment continued to diversify as vendors introduced specialty machines, including electric-drive telehandlers for indoor logistics and hybrid-powered crawler cranes for urban high-rise construction.

Construction retained the largest application share at 29.12% of the industrial machinery market size in 2025, reflecting ongoing transport-network upgrades and utility expansions. Contractors prioritized low-noise, zero-emission machines for city projects, creating new specification points beyond raw horsepower. Agricultural applications recorded the fastest growth at a 10.71% CAGR. Autosteering tractors, drone-guided sprayers, and smart harvesters supported yield gains while reducing chemical inputs. Deere and Company earmarked USD 20 billion for United States factory investments that will roll out autonomous technologies to mitigate farm labor gaps. Food-processing facilities automated palletizing and quality inspection, leveraging artificial-vision to cut waste.

Automotive manufacturers expanded electric-vehicle capacity and installed high-tolerance laser-cutting systems for battery enclosures. Chemical and pharmaceutical plants adopted clean-in-place skid packages with remote monitoring, meeting stricter safety and traceability rules. Textile producers deployed compact robots to automate sewing lines, reversing offshoring trends. Power-generation projects, especially wind-turbine installation and grid-scale battery assembly, required purpose-built material-handling rigs. Printing firms embraced Industry 4.0 workflow software to optimize press utilization, extending the market for modular finishing machines. Each application segment demanded tailored automation, underpinning broad-based equipment sales.

The Global Industrial Machinery Market Report is Segmented by Product Type (Earth-Moving Equipment, Material-Handling and More), Application Industry (Printing, Food, Textile, Construction, and More), End-User Ownership (OEMs, Contract Manufacturers, and More), Automation Level (Conventional Manually Operated, Semi-Automated/CNC, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific maintained a 42.35% revenue share in 2025 and recorded an 8.42% CAGR, strengthening its dominance in the industrial machinery market. Chinese automation suppliers introduced competitive servo drives and PLCs, enabling localized price points that challenged imported brands. India's Production-Linked Incentive schemes supported machinery imports and encouraged joint ventures for domestic manufacture. Japan and South Korea focused on ultraprecise robotics and semiconductor equipment, sustaining high unit values. Taiwan's contract electronics manufacturing required continuous investment in surface-mount and inspection machines, preserving demand for specialty feeders and cameras.

North America benefited from federal infrastructure funding and private-sector reshoring initiatives. Manufacturers expanded brownfield sites with modular machining cells that switch quickly between parts, supporting just-in-time delivery. Autonomous haul trucks deployed in Canadian mining underscored the region's appetite for high-technology heavy equipment. Currency stability and access to low-cost energy attracted further investment in petrochemical and battery production lines, bolstering orders for compressors, pumps, and web-handling systems. Education partnerships addressed skilled-labor shortages by promoting robotics technician programs.

Europe saw steady demand as firms invested in multi-process machinery to defend competitiveness against rising energy costs. German builders supplied high-tolerance forming presses to Eastern European automotive and appliance plants. Scandinavian wood-processing mills installed intelligent saw lines that optimise yield from every log. The United Kingdom launched grants for zero-emission construction machinery, promoting adoption of compact electric excavators in urban redevelopment. The European repair-maintenance-overhaul sector grew as operators extended machine lifespans with predictive analytics.

South America and the Middle East and Africa represented emerging growth pockets. Brazilian infrastructure upgrades needed large earth-moving fleets and concrete pumps, but exchange-rate volatility constrained imports. Hitachi Construction Machinery and Marubeni set up a mining-equipment service venture in Brazil to localise support and shorten downtime. Gulf Cooperation Council nations invested in desalination and renewable-energy projects, requiring corrosion-resistant pumps and high-capacity cranes. African governments prioritised agricultural mechanisation by subsidising tractor purchases, aiding sales of low-horsepower machines.