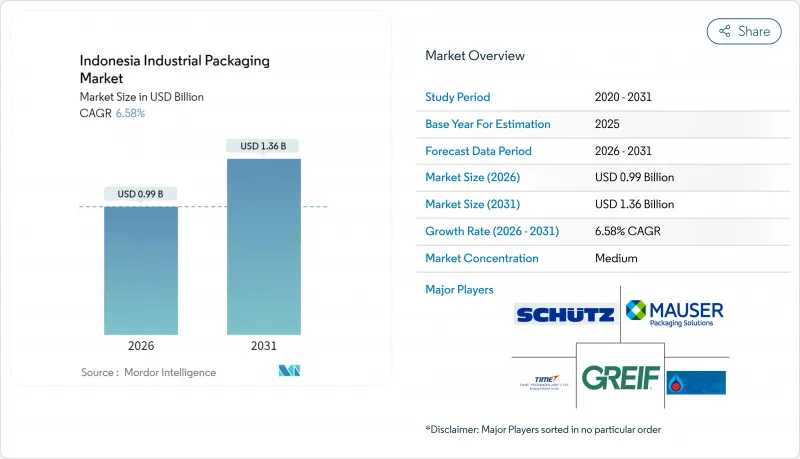

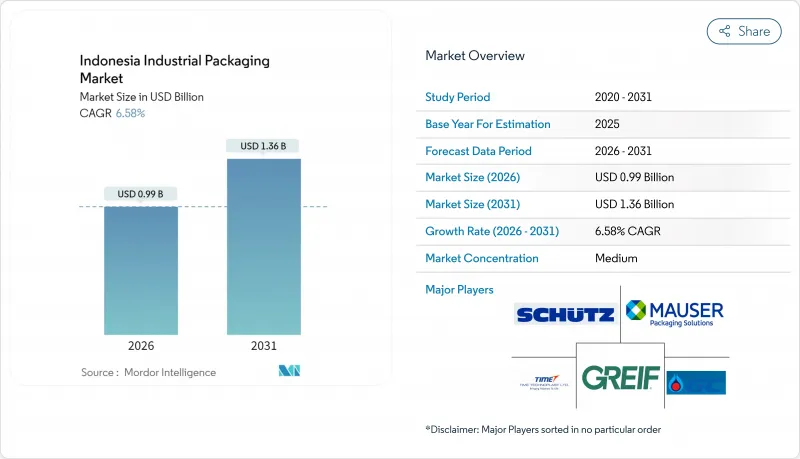

인도네시아의 산업용 포장 시장은 2025년 9억 3,000만 달러로 평가되었고, 2026년 9억 9,000만 달러에서 2031년까지 13억 6,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년) 동안의 CAGR은 6.58%로 전망되고 있습니다.

이 전망은 동남아시아 최대의 경제대국으로서의 동국의 입장을 반영하고 있으며, 석유화학제품의 생산능력 증가, 정부 주도의 영양 프로그램, 전자상거래의 급성장에 의해 벌크 포장 및 운송용 포장 솔루션에 대한 최종 사용자 수요가 계속 확대되고 있습니다. 찬드라 아스리사의 연간 420만 톤 규모 통합 석유화학단지와 2024년 재무부가 증설한 422조 7,000억 루피아(258억 달러)의 인프라 예산 등의 투자는 국내 공급망을 강화하고 화학제품, 식품, 건설 분야에서 포장재의 소비를 촉진합니다. 한편, 파우치 폐기물 대책 규제, 새로운 식품 접촉 기준, 확대 생산자 책임(EPR) 규정의 진화에 의해 재료 선택이 재검토되어 식품 직접 접촉 용도용 종이 및 섬유계 대체재의 도입이 가속하고 있습니다.

인도네시아의 무료 영양식 프로그램에는 2025년부터 매일 1억 9,000만 개의 식품의 포장이 필요하며, 분량이 관리되는 식품용기에 대한 안정적인 수요가 탄생하고 있습니다. 펩시코사가 2억 달러를 투입한 치카랑 공장은 2025년 동국 최대의 단일 식품 및 음료 투자 사례로, 배리어 드럼, 레토르트 파우치, 내열성 카톤을 기반으로 하는 고속 무균 라인을 갖추고 있습니다. 국내 대기업인 인도푸드사와 마요라사는 2024년 생산능력을 확대했으며 마요라사는 2조 5,260억 루피아(1억 5,400만 달러)를 투입해 신규 시설을 건설했습니다. 이 시설에는 가스 치환 포장 및 다층 종이 솔루션이 필요합니다. 확대되는 중산층 소비와 2억 7,000만 명에 달하는 인구가 간식, 음료, 간편식품에서 생산량의 지속적인 성장을 뒷받침하고 있습니다. 이러한 요인들이 결합되어 가공업자가 휴대성, 보존기간, 지속가능성 요건을 충족하기 위해 포장 형태를 다양화하는 가운데 인도네시아의 산업용 포장 시장은 꾸준한 성장을 계속하고 있습니다.

엑손모빌사의 150억 달러 규모 통합 석유화학단지와 롯데케미칼사의 에틸렌 크래커 확장 사례는 인도네시아의 화학 가치 체인에 대한 최대 규모의 외자 유입을 나타냅니다. 찬드라 아스리사의 신규 420만톤/년 플랜트에 의한 국내 수지 공급은 원료 가격을 안정화시켜 대용량 드럼캔, IBC 컨테이너, 내식성 복합 용기의 도입 확대를 촉진하고 있습니다. 의약품, 농약, 특수 중간체 등 다운스트림 산업의 성장에 따라 유엔 규격에 적합한 포장 및 부정 개봉 방지 캡에 대한 2차 수요가 증가하고 있습니다. 원재료 수출을 제한하는 국내 다운스트림화 정책은 더 많은 화학물질이 현지에서 가공되도록 하여 고부가가치 용기 시스템을 위한 인도네시아의 산업용 포장 시장의 잠재 규모를 확대하고 있습니다. 장기적으로, 찔레곤과 그레식에서의 화학 클러스터 정비는 벌크 수지 및 용매 출하량에서 두 자릿수 성장의 지속을 뒷받침합니다.

환경부는 2030년까지 다층 포장 봉투의 전국적인 단계적 폐지를 의무화하고 전환 기업에 포장 재설계와 대규모 재활용 가능한 단일 소재 라미네이트의 도입을 촉진하고 있습니다. EPR(확대 생산자 책임) 규정에서는 브랜드 소유자와 포장 제조업체가 회수 및 재활용 비용을 부담하기 때문에 단위 생산 비용이 15-20% 증가합니다. 2024년 11월 BPOM이 WTO에 통보한 식품 접촉 규제는 상업화 전에 광범위한 전환 시험과 공장 감사를 의무화합니다. 2025년 1월에 도입된 인도네시아의 탄소 거래 플랫폼 하에서 새로운 플라스틱 신용 시장이 컴플라이언스 부담을 더욱 증가시키는 반면, 회수율이 높은 사업자에게는 수익 기회를 제공합니다. 이러한 중복 정책은 인도네시아의 산업용 포장 시장에서 특히 자본력이 제한된 중소기업 컨버터에서 이익률을 줄이고 인증 주기를 장기화하고 있습니다.

플라스틱 부문은 풍부한 국내 수지 자원과 확립된 압출 성형 및 블로우 성형 인프라에 뒷받침되어 2025년 인도네시아의 산업용 포장 시장 점유율의 47.12%를 차지했습니다. 서자바주와 반텐주에서의 석유화학산업 확대가 원료 공급 안정성을 보장하기 때문에 일회용품 규제 강화에도 불구하고 인도네시아의 산업용 포장 시장 내 플라스틱 솔루션 부문은 2030년까지 큰 규모를 유지할 것으로 예측됩니다. 고밀도 폴리에틸렌 드럼, 폴리프로필렌 직물 백, 다층 필름은 화학, 농산물 및 전자상거래 분야에서 벌크 수송의 기반을 담당합니다.

종이 및 섬유계 소재는 7.62%라는 가장 높은 CAGR을 기록할 전망이며 이는 식품 접촉용 포장재에 있어서 폴리스티렌보다 판지를 권장하는 BPOM의 신규격 SNI 8218:2024가 촉진요인이 되고 있습니다. 고속 EC 라인용 골판지 등급, 성형 섬유 인서트, 라미네이트 크래프트 가방은 브랜드 소유자가 재활용 용이화 전략을 채택하면서 수요가 확대되고 있습니다. 금속, 복합재료 및 바이오베이스 폴리머는 부식성 화학 물질의 캡슐화, 고온 충전 및 퇴비화 가능한 푸드 서비스 용품과 같은 틈새 요구사항을 충족합니다. 코카콜라의 병입회사인 PT Amandina Bumi Nusantara사의 월 3,000톤 규모 재생 PET(rPET) 라인은 음료의 2차 포장에서 재생 소재로의 이행을 상징하고 있습니다. 지속적인 소재 대체 및 수지 순환성 향상은 인도네시아의 산업용 포장 산업의 미래 수요 패턴을 형성할 것입니다.

드럼캔과 배럴은 2025년 시점에서 인도네시아의 산업용 포장 시장 규모의 34.92%를 차지하였으며, 화학약품, 윤활유, 건설용 첨가제의 표준 형태로 기능하고 있습니다. 이러한 보급은 표준화된 파렛트, 지게차 대응성 및 인도네시아 물류 사업자의 높은 유엔 인증 인지도에 의해 발생합니다.

중간 벌크 컨테이너(IBC)는 CAGR 7.97%로 확대될 전망입니다. 스마트 공장에서는 재고 관리를 효율화하는 레벨 센서와 RFID 태그를 통합한 1,000리터 유닛을 도입하고 있습니다. 2024년 마우저 패키징과 리쿠텍 간의 제휴는 순환성 목표를 충족하는 이중벽 구조의 재생재 함유 IBC 병으로의 이행을 나타냅니다. 파렛트와 크레이트는 전자상거래의 소포 처리와 건설기계의 물류로 수요가 높아지고 있으며, 단열포장은 도서 지역에서의 백신과 생물제제의 유통으로 확대되고 있습니다. 위험물, 배터리 전해액, 온도 관리가 필요한 식품 원료용 특수 포장이 인도네시아의 산업용 포장 시장의 다양화된 제품군을 보완하고 있습니다.

The Indonesia industrial packaging market was valued at USD 0.93 billion in 2025 and estimated to grow from USD 0.99 billion in 2026 to reach USD 1.36 billion by 2031, at a CAGR of 6.58% during the forecast period (2026-2031).

This outlook reflects the country's position as Southeast Asia's largest economy, where rising petrochemical capacity, government-led nutrition programs, and an e-commerce boom continue to expand end-user demand for bulk and transit packaging solutions. Investments such as Chandra Asri's 4.2 MTPA integrated petrochemical complex and the Ministry of Finance's IDR 422.7 trillion (USD 25.8 billion) infrastructure budget in 2024 strengthen domestic supply chains and stimulate packaging consumption across chemicals, food, and construction verticals. At the same time, regulations targeting sachet waste, new food-contact standards, and evolving Extended Producer Responsibility (EPR) rules are reshaping material choices and accelerating paper- and fiber-based alternatives for direct-food applications.

Indonesia's Free Nutritious Meals program requires packaging for 190 million meals every day beginning in 2025, creating consistent demand for portion-controlled food-grade containers. PepsiCo's USD 200 million Cikarang plant, the country's largest single F&B investment in 2025, is outfitted with high-speed, aseptic lines that rely on barrier drums, retort pouches, and temperature-stable cartons. Domestic majors Indofood and Mayora expanded capacity in 2024, with Mayora investing IDR 2.526 trillion (USD 154 million) in new facilities that require modified-atmosphere and multilayer paper-based solutions. Growing middle-class consumption and a 270 million-strong population underpin continuing output growth across snacks, ready-to-drink beverages, and convenience meals. Together these factors reinforce a steady uptick in the Indonesia industrial packaging market as processors diversify pack formats to meet portability, shelf-life, and sustainability mandates.

ExxonMobil's USD 15 billion integrated petrochemical complex and Lotte Chemical's ethylene cracker expansion represent the largest inflows of foreign capital into Indonesia's chemical value chain. Domestic resin supply from Chandra Asri's new 4.2 MTPA plant stabilizes input prices and drives higher adoption of large-volume drums, IBCs, and corrosion-resistant composite containers. Downstream growth in pharmaceuticals, agrochemicals, and specialty intermediates multiplies secondary demand for UN-approved packs and tamper-evident closures. National downstreaming policies that restrict raw material exports ensure more chemicals are processed locally, extending the addressable Indonesia industrial packaging market size for higher-value containment systems. Over the long term, chemical-cluster build-outs in Cilegon and Gresik support ongoing double-digit volume growth in bulk resin and solvent shipments.

The Ministry of Environment has mandated a national phase-out of multilayer sachets by 2030, compelling converters to redesign packs and invest in mono-material laminates that are recyclable at scale. EPR rules require brand owners and pack producers to finance collection and recycling, adding 15-20% to unit production costs. BPOM's November 2024 food-contact regulation, notified to the WTO, imposes broad-spectrum migration testing and factory audits prior to commercialization. A new plastic-credit market introduced under Indonesia's January 2025 carbon trading platform further increases compliance burdens but opens revenue opportunities for high-recovery operators. These overlapping policies tighten margins and lengthen certification cycles within the Indonesia industrial packaging market, particularly for SME converters with limited capital.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

The plastic segment captured 47.12% of the Indonesia industrial packaging market share in 2025, supported by abundant domestic resin and well-established extrusion and blow-molding infrastructure. The Indonesia industrial packaging market size for plastic solutions is expected to remain sizeable through 2030 despite tightening single-use rules, as petrochemical expansion in West Java and Banten ensures stable feedstock. High-density polyethylene drums, polypropylene woven sacks, and multilayer films underpin bulk transport across chemicals, agrocommodities, and e-commerce sectors.

Paper and fiber-based materials post the highest 7.62% CAGR, propelled by BPOM's new SNI 8218:2024 food-contact standard that favors paperboard over polystyrene for direct-food packs. Corrugated grades for high-speed e-commerce lines, molded-fiber inserts, and laminated kraft sacks gain traction as brand owners adopt easy-recycling strategies. Metal, composite, and bio-based polymers fill niche requirements in corrosive chemical containment, high-temperature filling, and compostable foodservice items. Coke bottler PT Amandina Bumi Nusantara's 3,000 tons/month rPET line highlights the shift toward recycled content in beverage secondary packaging. Continuous material substitution and improved resin circularity will shape future demand patterns in the Indonesia industrial packaging industry.

Drums and barrels retained 34.92% of the Indonesia industrial packaging market size in 2025, serving as the default format for chemicals, lubricants, and construction additives. Their ubiquity stems from standardized pallets, forklift compatibility, and UN certification familiarity among Indonesian logistics providers.

Intermediate bulk containers are growing at an 7.97% CAGR, as smart factories adopt 1,000 L units with integrated level sensors and RFID tags that streamline inventory tracking. Mauser Packaging's 2024 partnership with RIKUTEC demonstrates a shift to double-walled, recycled-content IBC bottles that meet circularity targets. Pallets and crates benefit from e-commerce parcel handling and construction equipment logistics, while insulated containers expand in vaccine and biologics distribution across remote islands. Specialized packs for hazardous materials, battery electrolytes, and temperature-sensitive food ingredients round out the diversified product landscape in the Indonesia industrial packaging market.

The Indonesia Industrial Packaging Market Report is Segmented by Material (Plastics, Metal, and More), Product Type (Jerry Cans, Ibcs, and More), End-User Industry (Chemicals and Pharmaceuticals, Food and Beverage, Automotive, Oil Gas and Petrochemicals, and More), Packaging Capacity (<=50L, 51-500L, 501-1000L, 1001-2000L, >2000L). The Market Forecasts are Provided in Terms of Value (USD).