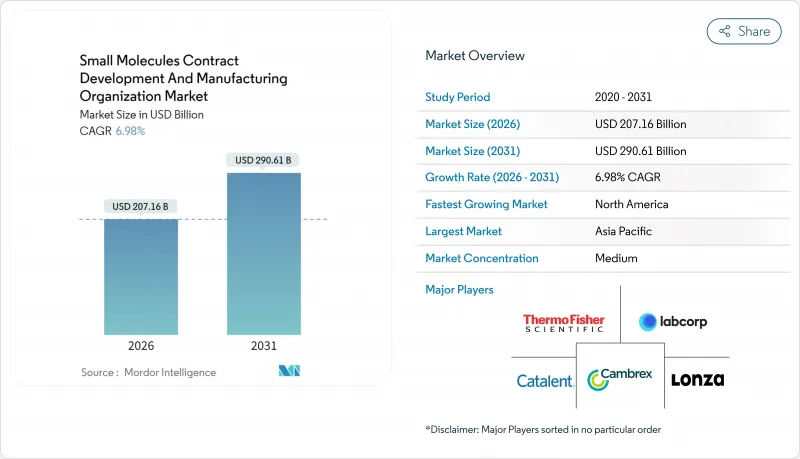

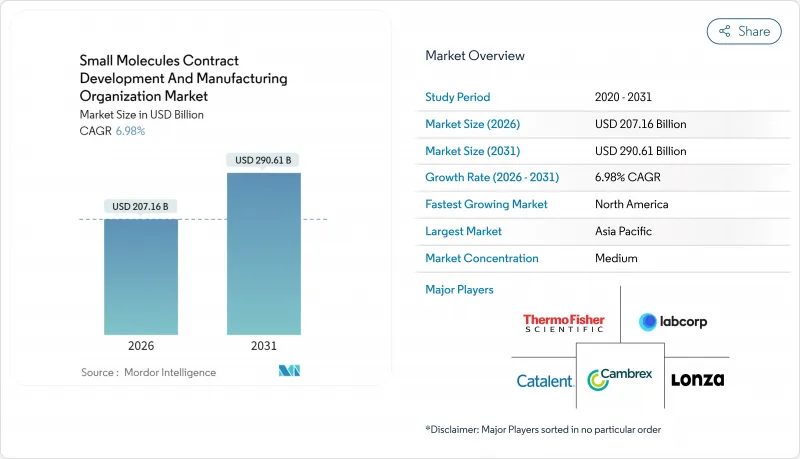

저분자 의약품 위탁개발생산(CDMO) 시장은 2025년 1,936억 4,000만 달러에서 2026년에는 2,071억 6,000만 달러로 예상되며 2026년부터 2031년에 걸쳐 CAGR 6.98%로 성장을 지속하여 2031년에는 2,906억 1,000만 달러에 달할 것으로 예측되고 있습니다.

이러한 성장 가속은 제약 혁신자가 자산 경량화 모델로 전략적으로 전환하고 있음을 반영합니다. 이는 복잡한 원료의약품 합성이나 의약품 제조를 외부로 위탁함으로써 보다 부가가치가 높은 연구개발에 자본을 집중할 수 있기 때문입니다. 연속제조기술, 인공지능에 의한 프로세스 최적화, 공급체인의 탄력성에 대한 규제당국의 주목 증가 등이 결합되어 최고 수준의 CDMO에 대한 수요가 높아지고 있습니다. 2024년 12월에 노보 홀딩스가 165억 달러에 인재를 인수한 사례는 차세대 치료제에 있어서 CDMO 시장이 중요한 인프라임을 뒷받침하고 있습니다. 규모의 이점과 전문화 압력이 높아지는 가운데, 저분자 의약품 제조 서비스가 현행 수익의 절반 이상을 차지하는 반면, 초기 단계의 파이프라인 지원과 통합형 CMC 솔루션이 가장 급속한 성장을 보이고 있습니다. 지역별로는 북미가 수익면에서 주도적 입장에 있는 반면, 아시아태평양은 비용면에서 우위성 있는 생산 능력의 증강과 다국적 프로그램을 유치하는 정부의 우대 조치에 의해 가장 높은 성장 궤도를 나타내고 있습니다.

많은 주요 제약 회사에서 제조는 더 이상 전략적 자산으로 간주되지 않으며, 경영진은 자본을 신약 개발 플랫폼과 후기 임상 프로그램에 집중시키고 있습니다. 2024년 12월에 체결된 Cambrex사와 일라이 릴리사의 전용 생산 능력 계약은 제약 대기업이 자사 공장을 증설하는 대신 외부 생산 능력을 확보하는 현상을 여실히 보여줍니다. 기술 이전이 완료되면 스폰서 기업이 이러한 외부 위탁을 철회하는 것은 드물며, 저분자 의약품 위탁개발생산(CDMO) 시장에는 순환적인 수요가 아니라 구조적인 수요가 태어나고 있습니다. 규제 대응의 실적이 길고 복수 제품에 대응하는 차폐 설비, 견고한 품질 관리 시스템을 가지는 CDMO는 스폰서 기업이 한계적인 비용 절감보다 신뢰성을 중시하기 때문에 프리미엄 가격을 획득하고 있습니다. 제약업계의 재편이 여러 번 이루어져 사내 제조 기술이 고갈된 결과 내부 인원 제약이 발생하고 있는 것도 아웃소싱의 기세를 뒷받침하고 있습니다. 이 지속적인 계약의 흐름은 자본 집약적인 CDMO의 확장과 관련된 위험을 줄이고 통합을 촉진합니다. 이는 공급 중단 없이 파이프라인의 폭과 세계적인 출시에 대응하기 위해서는 규모의 확대가 필수적이기 때문입니다.

2024년에 FDA가 승인한 신규 저분자 의약품 50건 중 91%가 종양 분야의 파이프라인에서 개발되었습니다. 정밀의료 연구의 성숙에 따라 이 기세는 계속될 것으로 예측됩니다. 고활성 API(원료의약품)에는 엄격한 차폐, 특수 개인보호구(PPE), 검증된 세척 프로토콜이 필요하며, 일부 CDMO만이 이들을 보유하고 있습니다. 2025년 1월 가동을 시작한 Olon 그룹의 2,500만 유로 규모 초고활성물질 시설은 이 분야에서 경쟁하는 데 필요한 인프라 투자 확대를 상징합니다. 종양 분야의 스폰서 기업은 기술 이전의 기간을 단축하기 위해 경로 탐색, 고활성 API 제조, 후기 단계의 제형 개발을 하나의 품질 시스템 하에 통합하는 CDMO를 높이 평가했습니다. 2024년 9월에 업데이트된 니트로소아민 가이드라인은 분석의 복잡성을 높여, 내부에 유전독성 불순물에 관한 전문 지식을 보유한 공급자와의 제휴를 혁신자에게 촉구하고 있습니다. 이 수요 패턴은 프로젝트의 백로그와 가동률을 높여 가격 규율을 강화함과 동시에 전문 공급자의 수익 가시성을 높이고 있습니다.

2024년 12월에 발효된 미국 수출 관리 규정 개정판에서는 전용 위험이 있는 지역에 대한 자동화된 펩티드 합성기, 연속 흐름 반응기 및 고급 차폐 스키드 수출을 제한합니다. 오스트레일리아 그룹의 병행 조치는 유럽 공급업체에 대한 라이선스 요구사항을 확대합니다. 아시아태평양의 신생 기업은 중요한 장비 조달에서 장기화 또는 완전 거부에 직면하고 확장 계획이 동결되어 검증 주기가 장기화되는 상황입니다. 구미의 CDMO(위탁개발생산)는 규제 대상 자산을 이미 보유한 검증된 벤더에 스폰서가 집중하기 때문에 단기적으로는 혜택을 받습니다. 그러나 국내 사업자는 벤더 풀이 한정됨으로써 자본 대체 비용 증가도 부담하게 됩니다. 저분자 의약품 위탁개발생산(CDMO) 시장에서는 이 정책 전환에 의해 지역 간에 불균등한 생산 능력이 생겨 초기 컴플라이언스 대응기간을 넘어 병목 현상이 계속되면 최종적으로는 세계 공급망의 회복력이 축소될 가능성이 있습니다.

2025년 저분자 의약품 제품 서비스는 저분자 의약품 위탁개발생산(CDMO) 시장의 52.02%를 차지했습니다. 이는 통합된 품질 시스템 하에서 제형, 충전 및 2차 포장을 관리하는 단일 소스 파트너에 대한 스폰서의 수요를 반영합니다. 이 부문은 2031년까지 연평균 복합 성장률(CAGR) 7.33%를 보일 것으로 예측되며, 신약 개발 기업이 장기 마스터 서비스 계약에서 물질과 제품의 요구를 통합하는 경향이 강해지는 가운데 API만의 업무를 능가하는 성장이 예상됩니다. 경구 고형 제제 프로젝트는 환자의 친숙함과 비용 효율적인 스케일 업으로 수량면에서 우위를 차지하지만, 고부가가치 성장은 특수 설비와 차폐 기술이 필요한 무균 주사제, 속용성 필름, 오남용 방지 정제에 존재합니다. 생물학적 제형이 유사한 저분자 및 나노결정 현탁액을 위한 고급 폴리소르베이트가 없는 제형은 제조를 더욱 복잡화하고 기존 기업을 보호하는 진입 장벽을 형성합니다.

수요 동향은 생산 능력 확장으로 이어지고 있으며, 예를 들어 2025년 1월 BioCina와 NovaCina의 합병에서는 미생물 발현 시스템과 무균 충전 및 포장 설비가 통합되었습니다. 스폰서 회사는 기술 이전 위험을 줄이고 규제 모니터링을 단순화하는 것을 통합 의약품 제조 위탁을 결정하는 주된 이유로 꼽았습니다. 이에 대해 CDMO 기업은 이러한 계약을 활용하여 미래의 생산 능력 확보를 보장하고 새로운 아이솔레이터 기술과 다제품 대응 동결건조 라인을 통합한 설비 투자계획을 뒷받침하고 있습니다. 그 결과로 태어난 에코시스템은 통합형 프로바이더가 저분자 의약품 위탁개발생산(CDMO) 시장에서 차지하는 점유율을 강화하는 동시에, 원료 전문기업이 다운스트림 공정 능력을 획득하거나 가격 중심의 조달 풀에 쫓기는 위험을 인식시키는 효과를 가져오고 있습니다.

2025년 시장 점유율에서 원료의약품 개발 및 제조는 48.35%를 차지했지만, 제제 개발 및 제조는 7.45%로 가장 높은 성장률을 나타내면서 스폰서가 턴키 방식의 화학 및 제조 및 관리 솔루션을 선호하는 경향이 밝혀졌습니다. 분석 및 규제 대응 서비스는 수익 규모는 작지만, 높은 이익률과 고객 종속을 실현하고 있습니다. 특히 세계의 니트로소아민 및 원소 불순물 가이드라인의 복잡화가 이를 뒷받침하고 있습니다. EUROAPI가 2025년 1월 SpiroChem과 맺은 제휴는 CRO와 CDMO의 융합을 위한 전환을 구현하는 것으로, 단일 계약 하에서 GMP 재료에 대한 합성 경로 연구를 제공합니다.

기존의 상품화로 간주되어 온 포장 및 직렬화는 미국, 유럽 연합 및 신흥 시장에서의 추적 관리 의무화에 의해 전략적 기반을 획득했습니다. 이는 여러 포장 계층에 걸친 데이터 집약이 가능한 직렬화 포장 라인이 요구되기 때문입니다. 레벨 4/레벨 5 IT 연결성에 조기 투자한 CDMO는 증분 수익을 획득하고 고객을 DSCSA 관련 페널티로부터 보호합니다. 예측기간에 있어서는 단순한 비용 효율이 아니라 폭넓은 서비스 포트폴리오가 저분자 의약품 위탁개발생산(CDMO) 시장에서의 점유율 확대를 결정할 것입니다.

북미는 2025년 매출액의 41.88%를 차지했습니다. 이는 FDA의 존재, 환자와 가까운 물류망, 국내 생산을 우대하는 정부 인센티브 때문입니다. 바이오시큐어법(BIOSECURE Act)의 논의가 활발해지는 가운데, 중요한 의약품 제조의 국내 회귀 움직임이 가속화되고, 크로다사가 펜실베니아주에 2025년 3월 설립한 23,680평방 피트의 지질 제조 시설과 같은 설비 투자로 이어지고 있습니다. 여러 주에 따른 우대 조치 패키지는 자본 집약적 확장의 실효 세율을 더욱 줄여 인건비가 높음에도 불구하고 이 지역은 매력적인 투자처가 되고 있습니다.

아시아태평양은 한국, 인도, 싱가포르에서 비용 우위를 지닌 클러스터를 기반으로 7.72%라는 최고 수준의 CAGR을 나타낼 것으로 예측됩니다. 한국식품의약품안전처(MFDS) 등의 규제당국은 연속제조라인에 대한 우선심사레인을 제공하여 현지 CDMO의 능력을 ICH의 기대치와 일치시키고 있습니다. 통화 조정 후 노동 단가 차이와 수직 통합된 화학 공급망이 결합되어 컴플라이언스를 손상시키지 않고 비용 경쟁력을 강화하고 있습니다. 다국적 스폰서 회사는 듀얼 사이트 전략에 의해 지정학적 위험을 관리합니다. 초기 단계 또는 비고활성 수요를 아시아태평양에 할당하면서 고활성 또는 상시에 필수적인 생산량은 구미의 사이트에 확보함으로써 포트폴리오 전체의 비용과 안전성 간의 균형을 도모하고 있습니다.

유럽은 성숙하면서도 혁신에 주력하는 시장 점유율을 가지고 있으며, EMA의 규제 조화, 엄격한 환경 규제, 연속 제조 설비로의 개보수를 뒷받침하는 에너지 절약 보조금에 뒷받침되고 있습니다. 스위스의 도티콘 ES는 2024년 9월 규제 안정성과 현지의 풍부한 인력층을 반영하여 저분자 의약품 생산 능력을 7억 스위스 프랑 규모로 확장한다고 발표했습니다. 유럽 그린딜에 내포된 지속가능성 목표는 용제 회수 시스템과 바이오매스 원료에 대한 수요를 높여 cGMP 준거에 더하여 저탄소 실적을 실현할 수 있는 CDMO에 새로운 서비스 분야를 창출하고 있습니다. 스폰서 각사가 추진하는 지리적 다양화 전략은 일반적으로 저분자 의약품 위탁개발생산(CDMO) 시장에 강인하고 다방향적인 성장 경로를 가져오고 있습니다.

The Small Molecules Contract Development And Manufacturing Organization market is expected to grow from USD 193.64 billion in 2025 to USD 207.16 billion in 2026 and is forecast to reach USD 290.61 billion by 2031 at 6.98% CAGR over 2026-2031.

This acceleration reflects pharmaceutical innovators' strategic pivot toward asset-light models, where outsourcing complex API synthesis and drug-product manufacturing frees capital for higher-value R&D. Continuous manufacturing, artificial-intelligence-driven process optimization, and heightened regulatory focus on supply-chain resilience amplify demand for best-in-class CDMOs. The Novo Holdings acquisition of Catalent for USD 16.5 billion in December 2024 underscores the market's status as critical infrastructure for next-generation therapeutics. Scale advantages coexist with specialization pressures: small-molecule drug-product services command more than half of current revenues, yet early-stage pipeline support and integrated CMC solutions register the fastest growth. Regionally, North America leads on revenue, whereas Asia-Pacific delivers the highest growth trajectory, supported by cost-advantaged capacity additions and government incentives that attract multinational programs.

Manufacturing is no longer regarded as a strategic asset inside many large pharmaceutical firms; instead, executives channel capital into discovery platforms and late-stage clinical programs. The Cambrex-Eli Lilly dedicated-capacity agreement concluded in December 2024 illustrates how Big Pharma now secures external capacity rather than erecting additional internal plants. Once transfer of know-how is complete, sponsors rarely reverse such outsourcing moves, creating a structural, rather than cyclical, pull on the small molecules contract development and manufacturing organization market. CDMOs with long regulatory track records, multiproduct containment suites, and robust quality systems capture premium pricing because sponsors prize reliability over marginal cost savings. Outsourcing momentum is reinforced by internal head-count constraints following multiple waves of pharma restructuring that depleted in-house manufacturing expertise. This sustained flow of contracts helps de-risk capital-intensive CDMO expansions and fuels consolidation, as scale becomes necessary to service pipeline breadth and global launches without supply interruptions.

The oncology pipeline produced 91% of the FDA's 50 novel small-molecule approvals in 2024, and the momentum is expected to continue as precision-medicine research matures. High-potency APIs require stringent containment, specialized personal protective equipment, and validated cleaning protocols, capabilities that only a subset of CDMOs have mastered. Olon's EUR 25 million ultra-potent facility activated in January 2025 exemplifies the escalating infrastructure investments needed to compete in this segment. Oncology sponsors value CDMOs that integrate route scouting, high-potency API production, and late-stage drug-product formulation under one quality system, shortening tech-transfer timelines. Updated nitrosamine guidance issued in September 2024 increases analytical complexity, incentivizing innovators to partner with providers possessing in-house genotoxic-impurity expertise. This demand pattern lifts project backlogs and utilization rates, reinforcing price discipline and strengthening revenue visibility for specialized providers.

Amendments to the U.S. Export Administration Regulations effective December 2024 restrict shipments of automated peptide synthesizers, continuous-flow reactors, and advanced containment skids to regions flagged for potential diversion. Parallel measures under the Australia Group extend license requirements to European suppliers. APAC startups now encounter protracted lead times or outright denials when sourcing critical equipment, freezing expansion plans and lengthening validation cycles. Western CDMOs benefit in the near term because sponsors gravitate toward proven suppliers that already possess restricted assets, but domestic operators also shoulder higher capital-replacement costs due to limited vendor pools. In the small molecules contract development and manufacturing organization market, the policy shifts create geographically uneven capacity additions, ultimately pressuring global supply resilience if bottlenecks persist beyond the initial compliance horizon.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Small-molecule drug-product services captured 52.02% of the small molecules contract development and manufacturing organization market in 2025, reflecting sponsor demand for single-source partners that manage formulation, filling, and secondary packaging under a unified quality system. The segment is forecast to post a 7.33% CAGR to 2031, outpacing API-only work as innovators increasingly bundle substance and product needs within long-term master service agreements. Oral-solid-dose projects dominate by volume thanks to patient familiarity and cost-efficient scaling, yet high-value growth resides in sterile injectables, fast-dissolving films, and abuse-deterrent tablets that require specialized equipment and containment expertise. Advanced polysorbate-free formulations for biologic-like small molecules and nanocrystal suspensions further complicate manufacturing, creating entry barriers that protect incumbents.

Demand patterns translate into capacity expansions such as the January 2025 BioCina-NovaCina merger that combines microbial expression systems with sterile fill-finish suites. Sponsors cite reduced tech-transfer risk and simplified regulatory oversight as primary reasons for awarding integrated drug-product mandates. In turn, CDMOs leverage these contracts to secure forward capacity commitments, supporting capex programs that embed new isolator technology and multiproduct lyophilization lines. The resulting ecosystem reinforces integrated providers' share of the small molecules contract development and manufacturing organization market size while encouraging API specialists to acquire downstream capabilities or risk relegation to price-centric procurement pools.

Drug-substance development and manufacturing retained 48.35% of 2025 revenues, yet drug-product formulation and manufacturing posted the fastest 7.45% growth, evidencing sponsor preference for turnkey chemistry, manufacturing, and controls solutions. Analytical and regulatory services, though smaller in revenue, deliver high margins and client lock-in, especially as global nitrosamine and elemental-impurity guidelines add complexity. EUROAPI's January 2025 collaboration with SpiroChem exemplifies the pivot toward CRO-CDMO convergence, offering route-scouting to GMP material under one contract.

Packaging and serialization, historically viewed as commoditized, now occupy strategic footing because track-and-trace mandates in the United States, European Union, and emerging markets require serialized packaging lines capable of aggregating data across multiple packaging hierarchies. CDMOs that invested early in Level-4/Level-5 IT connectivity capture incremental revenue and shield clients from DSCSA-related penalties. Over the forecast horizon, service-portfolio breadth, not isolated cost efficiency, will dictate share gains in the small molecules contract development and manufacturing organization market.

The Small Molecules Contract Development and Manufacturing Organization Market Report is Segmented by Product (Small-Molecule API, Small-Molecule Drug Product), Service Type (Drug-Substance Development & Manufacturing, and More), Stage of Development (Pre-Clinical and More ), Therapeutic Area (Cardiovascular, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America accounted for 41.88% revenue in 2025 thanks to FDA familiarity, near-patient logistics, and government incentives favoring domestic production. The BIOSECURE Act debate intensifies momentum for reshoring critical-medicine manufacturing, leading to facility investments like Croda's USD 23,680-square-foot lipid site in Pennsylvania, inaugurated March 2025. Multistate incentive packages further reduce effective tax rates for capital-intensive expansions, making the region attractive despite higher labor costs.

Asia-Pacific is projected to register the highest 7.72% CAGR, anchored by cost-advantaged clusters in South Korea, India, and Singapore. Regulatory agencies such as South Korea's MFDS now offer priority-review lanes for continuous-manufacturing lines, aligning local CDMO capabilities with ICH expectations. Currency-adjusted labor-rate differentials, combined with vertically integrated chemical supply chains, enhance cost competitiveness without compromising compliance. Multinational sponsors manage perceived geopolitical risk through dual-site strategies, allocating early-phase or non-potent demand to APAC while reserving high-potency or launch-critical volumes for Western sites, balancing cost and security across their portfolios.

Europe commands a mature but innovation-focused share, buoyed by EMA harmonization, stringent environmental rules, and energy-efficiency grants that favor continuous-manufacturing retrofits. Switzerland's Dottikon ES announced CHF 700 million in small-molecule capacity additions in September 2024, reflecting regulatory stability and local talent depth. Sustainability targets embedded in the European Green Deal elevate demand for solvent-recovery systems and biomass-based feedstocks, creating new service niches for CDMOs capable of delivering low-carbon footprints alongside cGMP compliance. Collectively, geographic diversification strategies pursued by sponsors fuel a resilient, multidirectional growth path for the small molecules contract development and manufacturing organization market.