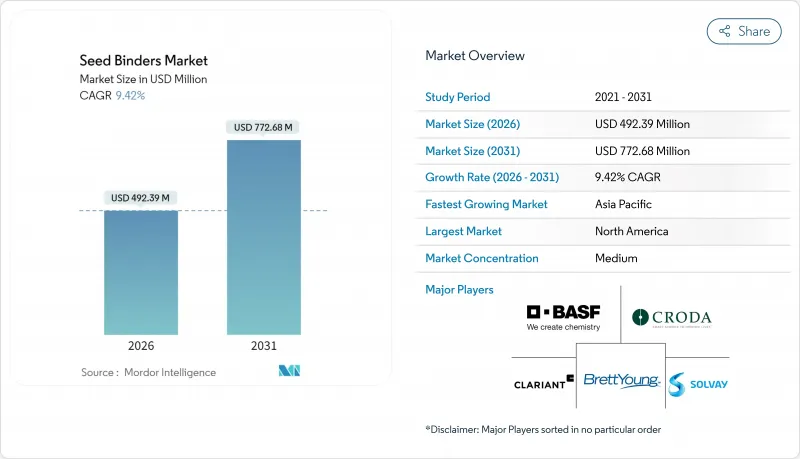

2026년 종자용 바인더 시장의 규모는 4억 9,239만 달러로 추정되며, 2025년 4억 5,000만 달러에서 성장할 전망입니다.

2031년까지 7억 7,268만 달러에 달하고, 2026년부터 2031년에 걸쳐 CAGR 9.42%로 확대될 전망입니다.

정밀 파종기기에 대한 투자 확대, 유효성분 함량에 상한을 지정하는 규제 강화, 농장의 통합 확대가 함께 종자의 유동성 향상, 형상 균일화, 생물학적 피복률 향상을 실현하는 바인더의 수요를 끌어올리고 있습니다. 필름 코팅 및 펠릿화 용도가 파종기의 설계 결정에 영향을 미치게 되면서 종자용 바인더 시장은 종자회사와 기기 제조업체 모두에게 전략적 투입이 필요한 자재 카테고리로 변모하고 있습니다. 벤처 캐피탈이 폴리비닐알코올과 동등한 취급 특성을 유지하면서 마이크로플라스틱 위험을 줄이는 생분해성 폴리머의 혁신 기업을 지원하고 있기 때문에 투자의 기세는 계속 견조합니다. 석유화학 원료의 가격 변동과 잔류기준 적합 비용이 단기적인 수익성을 억제하는 한편, 공급업체가 재생가능 화학제품과 통합형 생물학적 배합에 주력함으로써 고부가가치 작물 전체에서 프리미엄 가격 설정의 기회가 계속 창출되고 있습니다.

필름 코팅은 유동성을 향상시키고 파종 시 먼지를 줄입니다. 이는 작물의 정착률을 향상시키고 작업자의 노출 위험을 억제합니다. 옥수수 종자 시험을 통해 파종 누출과 이중 파종이 감소하여 코팅 비용을 초과하는 수율 향상이 확인되었습니다. 특수 채소 생산자는 종자 비용이 총 생산 예산에 차지하는 비율이 작기 때문에 투자 회수가 즉시 실현되는 본 기술을 신속하게 도입하고 있습니다. BASF사는 환경 부하가 없는 마이크로플라스틱 프리 시스템을 발표하여 폴리비닐알코올과 동등한 성능을 실현했습니다. GPS 대응 파종기와 실시간 파종 분석에 의해 균일한 단립 파종의 이점이 정량화되는 시장에서의 침투가 가장 먼저 진행되고 있습니다. 필름 코팅이 농약 유출을 줄이는 규제 당국의 승인도 도입을 더욱 가속화하고 있습니다.

현대의 파종기는 99%의 분리율을 유지하기 위해 엄밀한 종자 사이즈 허용차를 요구하고, 종자 제조업체는 형상을 표준화하는 펠렛팅이나 인클러스팅 처리의 도입을 요구받고 있습니다. 농학 연구에서는 부적절한 종자 배치가 15-20%의 수익 손실로 이어지는 것으로 나타나 생산자의 균일화처리 도입을 촉진하고 있습니다. 정밀 농업은 현재 브라질, 중국, 인도로 확대되고 있으며, 형상화된 씨앗의 필요성이 전통적인 미국과 유럽의 주요 지역을 넘어 확산되고 있습니다. 이에 비해 장비 제조업체는 코팅 종자용으로 조정된 파종기를 판매함으로써 대응하며, 종자용 바인더 시장을 기계화 동향에 더욱 통합하고 있습니다. 농업 노동 비용의 상승은 관개 원예에서 기계화 파종을 표준 방법으로 정착시켜 장기적인 추진력을 더하고 있습니다.

폴리머 등급 프로필렌의 가격은 2025년 중반까지 톤당 110.23달러 상승한 것으로 나타났으며 이는 폴리비닐알코올 생산자의 이익률을 압박하고 있습니다. 가격 연계 계약에 의존하는 바인더 공급업체는 비용 전가의 가속화를 고민하고 이는 종자 바인더 시장에서 단기 수익성을 낮추고 있습니다. 지정학적 요인에 따른 운임 프리미엄은 아시아보다 유럽에서 원료의 양륙비용을 높여 지역 간 불균형을 낳고 있습니다. 일부 제조업체는 장기 계약으로 위험을 회피하지만 이러한 수단은 위험을 늦추는 것에 불과합니다. 가격 변동으로 인해 고객은 바이오 대체품을 시험적으로 도입하고 이는 석유 유래 제품으로부터의 이행을 가속화하고 있습니다.

2025년 시점에서 폴리비닐알코올은 종자 바인더 시장에서 41.10%의 점유율을 차지하였으며, 예측 가능한 점도, 입증된 접착성, 저비용이라는 오랜 강점이 이를 뒷받침하고 있습니다. 이 부문의 강점은 살충제, 살균제, 착색제와의 폭넓은 상용성에 뿌리를 두고 있으며, 이러한 이점에 의해 폴리비닐알코올은 곡물 및 사료용 종자 분야에서 우위성을 유지하고 있습니다. 바이오폴리머계 대체품 부문의 종자용 바인더 시장 내 규모는 유럽연합에서 마이크로플라스틱의 잔류에 대한 규제 감시 강화로 인해 제품 카테고리 중 가장 높은 11.55%의 연평균 복합 성장률(CAGR)로 확대될 것으로 전망됩니다. 단백질 유래 및 리그닌 유래의 바인더가 최근 등장하여 마이크로플라스틱 프리 표시가 가격 프리미엄을 낳는 고급 원예 종자 시장에 대응하고 있습니다. 공중합체 블렌드 및 아크릴계 제품은 알칼리성 토양 내성과 같은 틈새 요구에 대응하고, 폴리아크릴레이트는 서방형 영양소 매트릭스에서 독특한 역할을 유지합니다. 식물성 오일계 폴리우레탄 네트워크의 혁신에 의해 습윤한 열대 기후 하에서 종자 저장 시에 기존의 화학제품을 뛰어넘는 방습 기능을 실현하고 있습니다.

바이오폴리머의 도입은 천연 폴리머의 열분해를 방지하는 저온 건조 사이클에 대응하는 코팅 라인의 개조에 따라 가속화되고 있습니다. 가공업자는 처리 종자 1톤 당 최대 15%의 에너지 절약 효과를 보고했으며, 이는 기업의 탄소 감축 목표와 부합하는 이차적인 이점입니다. 선행 종자 기업은 특히 합성 폴리머 잔류물이 인증을 방해하는 유기농 분야에서 바이오폴리머의 효과를 활용하여 브랜드 포트폴리오의 차별화를 도모하고 있습니다. 브라질에서는 사탕수수 발효를 통한 원료 공급이 확대되고 있어, 미래의 코스트 패리티의 실현을 시사하고 있습니다. 전체적으로 제품 구성은 재조정될 전망이지만 기존 폴리비닐알코올의 생산 능력과 가격경쟁력에 의해 예측기간 중에는 기존과 신규 화학제품의 공존이 확실시됩니다.

북미는 2025년 세계 시장에서 31.60%의 점유율을 달성했습니다. 이 지위는 대규모 농장 규모, 높은 재배자 도입률 및 종자 처리를 농지 밖으로의 화학물질 이동의 완화책으로 인정하는 규제에 의해 뒷받침됩니다. BASF사의 Xarvio 바이오에너지 지표와 같은 실시간 탄소 추적 모듈의 통합은 성장 확립을 넘어 코팅 효과를 정량화하는 새로운 의사결정 지원 층을 추가합니다. 미주리에 신설된 베크사의 대두 가공 플랜트는 처리 능력에 대한 지속적인 자본 유입을 뒷받침하고 종자 바인더 시장을 지원하는 지역 서비스 생태계를 강화하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 11.85%로 급성장할 것으로 예상되는 지역입니다. 중국의 연간 1,200만 미터톤의 종자 수요와 인도의 500억 달러 규모 특수화학 기반이 정밀 파종을 촉진하는 정부 프로그램과 함께 성장을 견인합니다. 벼농사 및 옥수수 생산의 급속한 기계화가 펠렛화 수요를 밀어 올리고, 아연 결핍 토양의 광범위한 분포가 미량 영양소 피복 기술의 보급을 가속화하고 있습니다. 중국 연안부에서는 생분해성 폴리머의 현지 생산이 확대되어 지역 종자 기업의 관세 부담 경감과 리드 타임 단축이 도모되고 있습니다.

유럽에서는 엄격한 마이크로플라스틱 지침으로 2028년까지 기존 폴리머로부터의 전환이 추진되어 완만한 성장률을 나타냅니다. 인코텍사는 조기에 마이크로플라스틱 프리 제품을 투입함으로써 규제 대응을 중시하는 구매 환경에서 유리한 입장을 확립하고 있습니다. 남유럽의 과일 및 채소 부문에서는 엄격한 소매 감사 대상이 되는 농산물에서의 살균제 잔류를 줄이는 고성능 생물 코팅이 도입되고 있습니다. 남미의 성장률은 완만한 페이스로 추이하고 있으며, 이는 브라질의 이모작 시스템이 한정된 파종 기간 중 발아를 촉진하는 펠렛화 및 피복 씨앗으로의 경제적 수익을 확대하고 있기 때문입니다. 아르헨티나가 추진하는 현지 농약 제조는 수지 공급 안정화에 기여하여 바인더 구매자의 환율 노출을 줄이고 있습니다.

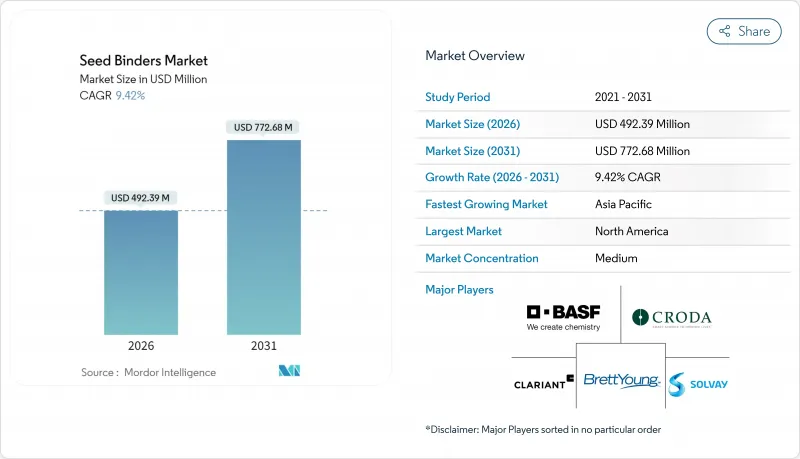

The seed binders market size in 2026 is estimated at USD 492.39 million, growing from 2025 value of USD 450 million with 2031 projections showing USD 772.68 million, growing at 9.42% CAGR over 2026-2031.

Higher spending on precision planting hardware, mounting regulations that cap active-ingredient loads, and widespread farm consolidation jointly lift demand for binders that improve seed flow, shape uniformity, and biological coverage. Film coating and pelleting applications now influence planter engineering decisions, turning the seed binders market into a strategic input category for both seed companies and equipment manufacturers. Investment momentum stays strong as venture capital backs biodegradable polymer innovators that reduce microplastic risk while matching the handling properties of polyvinyl alcohol. Petrochemical feedstock volatility and residue-limit compliance costs temper near-term profitability, yet supplier focus on renewable chemistries and integrated biological formulas continues to unlock premium pricing opportunities across high-value crops.

Film coating improves flowability and cuts planter dust, which in turn raises crop establishment rates and limits operator exposure. Corn seed trials show lower skips and doubles, delivering yield gains that outweigh coating costs. Specialty vegetable growers adopt the technology quickly because seed costs form a minor share of total production budgets, making return-on-investment immediate. BASF launched a microplastic-free system that matches polyvinyl alcohol performance without environmental baggage. Penetration is strongest in markets where GPS-enabled planters and real-time sowing analytics quantify the benefit of uniform seed singulation. Regulatory endorsement that film coatings lower pesticide runoff further accelerates uptake.

Modern planters require tight seed-size tolerance to maintain 99% singulation, pressing seed companies to adopt pelleting and encrusting that standardize geometry. Agronomic studies link poor seed placement to 15-20% profit loss, which motivates grower adoption of uniformity treatments. Precision agriculture now expands in Brazil, China, and India, spreading the need for shaped seeds beyond traditional U.S. and European strongholds. Equipment makers reciprocate by marketing planters calibrated for coated seeds, further locking the seed binders market into the mechanization trend. Rising farm labor costs cement mechanized sowing as the default in irrigated horticulture, adding long-term momentum.

Polymer-grade propylene prices are projected to climb USD 110.23 per metric ton by mid-2025, squeezing margins for polyvinyl alcohol producers. Binder suppliers that rely on formula-pricing contracts struggle to pass costs through quickly, reducing short-term profitability within the seed binders market. Freight premiums linked to geopolitical events elevate feedstock landed cost in Europe more than in Asia, creating a regional imbalance. Some manufacturers hedge with long-term contracts, yet such instruments only delay exposure. Volatility motivates customers to test bio-based substitutes, accelerating the shift away from petroleum derivatives.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

In 2025, polyvinyl alcohol commanded 41.10% of the seed binders market share, underscoring a legacy of predictable viscosity, proven adhesion, and low cost. The segment's strength remains anchored in broad compatibility with insecticides, fungicides, and colorants, advantages that keep polyvinyl alcohol dominant in cereals and forage seeds. The seed binders market size for biopolymer-based alternatives is projected to post a 11.55% CAGR, the fastest among product classes, as regulatory scrutiny over microplastic persistence intensifies in the European Union. Recent launches of protein-based and lignin-derived binders cater to premium horticultural seeds where microplastic-free labeling commands price premiums. Copolymer blends and acrylics address niche needs such as alkaline-soil tolerance, while polyacrylates maintain distinct roles in controlled-release nutrient matrices. Innovation in vegetable-oil polyurethane networks unlocks moisture-barrier functions that outperform legacy chemistries when seeds are stored in humid tropical climates.

Biopolymer adoption accelerates as coating lines retrofit to handle lower-temperature drying cycles that prevent thermal degradation of natural polymers. Processors report up to 15% energy savings per metric ton of treated seed, a side benefit that aligns with corporate carbon-reduction pledges. Early-mover seed companies leverage biopolymer claims to differentiate brand portfolios, notably in organic segments where synthetic polymer residue disqualifies certification. Raw-material supply is scaling through sugar-cane fermentation in Brazil, signaling future cost parity. Overall, the product mix is set to rebalance, yet entrenched polyvinyl alcohol capacity and price competitiveness ensure the coexistence of legacy and novel chemistries during the forecast horizon.

The Seed Binders Market Report is Segmented by Product Type (Polyvinyl Alcohol, Polyacrylate, Biopolymer-Based, and Others), Crop Type (Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, and Other Crops), Function (Film Coating, Pelleting, and Encrusting), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 31.60% of global value in 2025, a position anchored by large farm sizes, high planter adoption, and regulations that recognize seed treatments as a mitigation tool for off-field chemical movement. Integration of real-time carbon-tracking modules, such as BASF's Xarvio Bioenergy metric, adds a new layer of decision support that quantifies coating benefits beyond stand establishment. Beck's latest soybean processing plant in Missouri underscores continuing capital flow toward treating capacity, reinforcing a regional service ecosystem that sustains the seed binders market.

Asia-Pacific is the breakout geography with a 11.85% CAGR to 2031 as China's 12 million metric tons annual seed requirement and India's USD 50 billion specialty-chemicals base intersect with government programs that encourage precision sowing. Rapid mechanization of rice and maize production lifts pelleting demand, while widespread zinc-deficient soils accelerate micronutrient encrusting adoption. Local production of biodegradable polymers expands in coastal China, lowering tariff exposure and shortening lead times for regional seed companies.

Europe posts a moderate growth rate as its stringent microplastics directive pushes end-users to transition away from conventional polymers by 2028. Incotec's early launch of microplastic-free offerings positions the company favorably in a compliance-driven purchasing environment. Southern Europe's fruit and vegetable sectors adopt high-load biological coatings that lessen fungicide residue on produce destined for strict retailer audits. South America advances at slow growth rate because Brazil's double-cropping system magnifies the economic return on pelleted and encrusted seeds that speed emergence during compressed planting windows. Argentina's push for local agrochemical manufacturing supports resin availability, reducing foreign-exchange exposure for binder buyers.