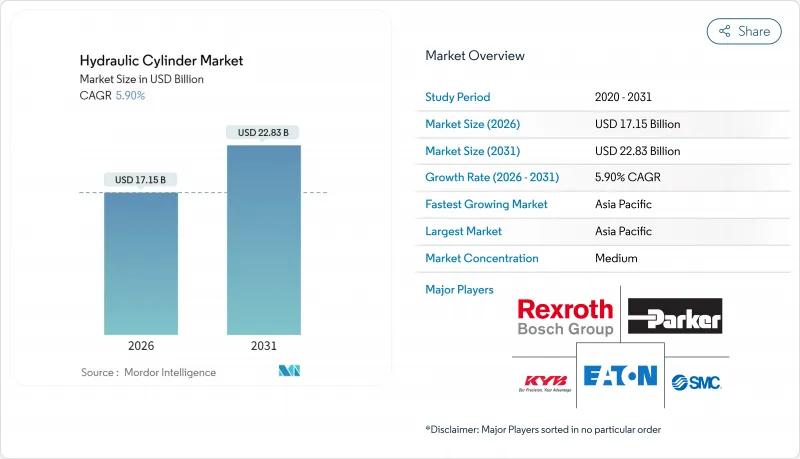

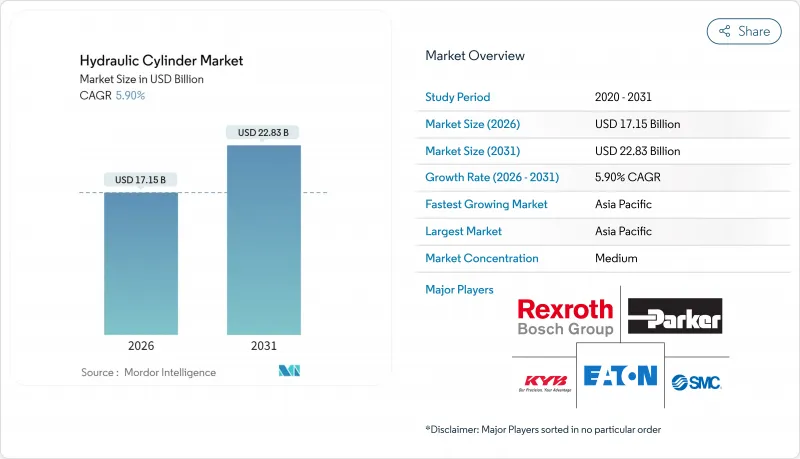

유압 실린더 시장은 2025년 161억 9,000만 달러에서 2026년에는 171억 5,000만 달러로 성장할 것으로 예측되고, 2026-2031년에 걸쳐 CAGR 5.9%로 성장을 지속하여 2031년까지 228억 3,000만 달러에 이를 전망입니다.

인프라 프로젝트에 대한 강력한 자본 지출, 창고 자동화의 급속한 확산, 스마트 전기-유압 솔루션의 도입이 유압 실린더 시장을 견인하고 있습니다. 비록 투입 비용 변동성과 선택적 전기화가 확장을 억제하고 있지만 말입니다. 수요는 건설 기계(굴삭기 한 대만 해도 최대 6개의 실린더를 통합함)와 고주파 리프트 및 틸트 시스템을 요구하는 전자상거래 물류 네트워크에 의해 주도됩니다. 아시아태평양 지역은 중국의 제조 규모와 인도의 공공사업 지출을 바탕으로 우위를 유지하는 반면, 북미는 1조 2,000억 달러 규모의 인프라 투자 및 일자리 법안의 혜택을 받고 있습니다. 최종 시장 전반에 걸쳐 공급업체들은 센서, IoT 게이트웨이, 재생 드라이브 아키텍처를 내장함으로써 경쟁 우위를 확대하고 있습니다. 이는 수명 주기 에너지 비용을 절감하고 예측 유지보수 수익원을 창출합니다.

인프라 지출은 굴삭기, 로더, 고소 작업대 등 각각 다수의 고톤수 실린더가 장착된 장비에 대한 연쇄적 수요를 촉진합니다. 미국에서는 연방 지출이 중장비 플릿을 부활시키고 가동률을 높이며, 이 효과는 해상 에너지 설비 투자(Capex)가 전년 대비 15% 증가하는 아시아에서도 동일하게 나타납니다. OEM 업체들은 유압 손실을 최대 64% 절감하는 에너지 회수 회로가 적용된 실린더를 지정함으로써 대응하고 있으며, 이는 연료 소모를 줄이고 기업의 탈탄소화 요구와 부합합니다. 금리 안정화로 가능해진 단기 금융 사이클은 유압 구동에 특히 의존하는 소형 장비 수요를 더욱 촉진합니다.

인도, 브라질, 사하라 이남 아프리카의 기계화 프로그램은 트랙터 보급률을 가속화하고 유압 시스템의 복잡성을 높입니다. 3점식 연결 장치, 로더 암, 조향 보조 장치 모두 먼지가 많고 고온인 환경에서도 정밀한 유량 조절이 가능한 실린더에 의존합니다. 하이브리드 유압-전기 구동계에 대한 현장 연구는 쟁기질 시 최대 토크가 18.8% 감소함을 보여주며, 유압력 밀도를 유지하면서 연료 절감 잠재력을 입증합니다. 지역별 조립 허브는 제조사가 관세 체계를 우회하고 리드 타임을 단축하는 데 도움을 주어, 농업 분야에서 유압 실린더 시장의 회복탄력성을 강화합니다.

75-80%의 효율 향상과 누출 없는 작동으로 전기 액추에이터는 정밀 포장, 실험실 자동화, 소형 로더 분야에서 매력적인 선택지가 됩니다. 1억 스트로크 이상의 높은 사이클 수명은 이러한 틈새 시장에서 수명 주기 경제성을 유압식보다 유리하게 만듭니다. 제조업체들은 포트폴리오를 확장하여 하이브리드 및 완전 전기식 제품을 포함시킴으로써 위험을 완화하고, 유압 실린더 산업이 선택적 대체를 경험하는 상황에서도 시장 점유율 유지를 보장합니다.

2025년 매출의 57.74%를 차지한 복동식 설계는 유압 실린더 시장 전반에 걸쳐 버킷, 프레스, 스티어링 컬럼의 양방향 하중 제어에서 그 역할을 공고히 하고 있습니다. 내장형 압력 트랜스듀서는 정밀도를 높여 OEM이 자동 용접 라인에서 반복성 목표를 달성할 수 있게 합니다. 중력 복귀 구조가 펌프 크기 및 유체량을 줄여 가위식 리프트 및 덤프 바디에 매력적인 절충안을 제공함에 따라 단동식 모델은 5.93%의 연평균 성장률(CAGR)을 기록합니다. 재생 회로 옵션은 에너지 소비를 추가로 절감하여 비용에 민감한 구매자를 위한 적용 가능한 사용 사례를 확대합니다.

이중 시장 역학은 맞춤형 조달 전략을 촉진합니다. 대량 생산 비도로 건설 장비 제조사들은 동기화된 유로 경로를 갖춘 복동 실린더에 대해 다년간 공급 계약을 체결하는 반면, 애프터마켓 유통업체들은 이질적인 장비 군에 대응하기 위해 모듈식 단동 SKU를 선호합니다. 공통 가공 셀에서 두 설계 간 생산 전환이 가능한 공급업체는 전환 가동 중단 시간을 최소화하고 총마진 스프레드를 확대하여 유압 실린더 시장 내 경쟁력을 강화합니다.

용접 실린더는 일체형 본체의 강도와 유리한 비용 대비 압력 비율 덕분에 2025년 매출의 44.15%를 차지했습니다. 농업 및 광업 분야의 OEM 업체들은 설치 시간을 단축하는 통합 글랜드를 활용하여 최대 3,000 PSI 용접 모델을 지정합니다. 텔레스코픽 실린더는 기반이 작음에도 도시 작업 현장에서 소형 보관 길이 및 확장된 도달 거리를 요구함에 따라 6.14%의 연평균 성장률(CAGR)로 가속화되고 있습니다. 텔레마틱 다단 시스템은 외부 체인 없이 7단까지 확장되며, 무정비 작동과 사이클 시간 이점을 제공합니다.

타이로드 및 밀 타입 설계는 각각 공장 자동화 및 금속 가공 분야에서 여전히 중요성을 유지하며, 서비스성 또는 극한 작업 요구사항이 제품 선택을 좌우합니다. 공급업체들은 서비스 주기를 연장하는 독자적인 씰 스택과 인더스트리 4.0 데이터 수집 요건을 충족하는 인라인 위치 감지 기술을 통해 차별화합니다. 이러한 광범위한 사양 스펙트럼은 유압 실린더 시장이 힘, 스트로크, 듀티 사이클 축 전반에 걸쳐 목적에 맞는 옵션을 제공하도록 보장합니다.

아시아태평양 지역은 2025년 매출의 40.62%를 차지하며 6.73%의 연평균 복합 성장률(CAGR)을 기록했습니다. 이는 인도의 고속철도 회랑 및 중국의 해상풍력 발전 확대와 같은 메가 프로젝트에 힘입은 결과입니다. 헝리(Hengli)와 같은 국내 선도 기업들은 수직 통합 공장을 확장하여 수입 고급 실린더를 대체함으로써 리드 타임과 도착 비용을 절감하고 있습니다. 공급업체 근접성은 지역 OEM 업체들이 채택한 적기 생산 방식과도 부합합니다.

북미는 2위를 차지하고 연방 정부의 인프라 투자에 의해 건설 차량의 갱신이나 내륙 항만의 자재관리 시스템이 쇄신됨으로써 지원되고 있습니다. 현지 제조업체는 첨단 야금 기술과 디지털 통합의 차별화를 도모해, 예측 유지보수의 도입 확대에 수반해 최종 사용자가 요구하는 데이터 풍부한 설비 요구에 대응하고 있습니다.

유럽에서는 지속가능성과 소음 저감이 중시되어 에너지 낭비를 억제하는 스마트한 전기 유압 설계의 채택이 진행되고 있습니다. EU 그린딜 지령의 법적 자극을 받아 OEM 제조업체는 생분해성 작동유와 누설 방지 기술을 갖춘 실린더의 수주를 촉진하고 있습니다.

유럽은 지속가능성과 소음 저감을 중시하여 에너지 낭비를 줄이는 스마트 전기-유압식 설계의 채택을 촉진합니다. OEM 업체들은 EU 그린딜 지침으로부터 입법적 자극을 받아 생분해성 유체와 누출 방지 기술을 적용한 실린더 주문이 증가하고 있습니다.

The hydraulic cylinder market is expected to grow from USD 16.19 billion in 2025 to USD 17.15 billion in 2026 and is forecast to reach USD 22.83 billion by 2031 at 5.9% CAGR over 2026-2031.

Robust capital spending on infrastructure projects, rapid warehouse automation, and the deployment of smart electro-hydraulic solutions together propel the hydraulic cylinder market, even as input-cost volatility and selective electrification temper expansion. Demand is anchored by construction machinery, where each excavator alone integrates up to six cylinders, and by e-commerce logistics networks that specify high-cycle lift and tilt systems. Asia-Pacific retains primacy on the back of Chinese manufacturing scale and Indian public-works outlays, while North America benefits from the USD 1.2 trillion Infrastructure Investment and Jobs Act. Across end-markets, suppliers widen their moats by embedding sensors, IoT gateways, and regenerative drive architectures that shrink lifetime energy costs and unlock predictive-maintenance revenue streams.

Infrastructure outlays stimulate a cascading need for excavators, loaders, and aerial platforms, each fitted with multiple high-tonnage cylinders. In the United States, federal spending revives heavy-equipment fleets and raises utilization rates, an effect echoed in Asia where offshore-energy capex is growing 15% year-on-year. OEMs respond by specifying cylinders with energy-recovery circuits that save up to 64% of hydraulic losses, cutting fuel burn and aligning with corporate decarbonization mandates. Shorter financing cycles, enabled by stabilizing interest rates, further unlock compact-equipment demand that disproportionately relies on hydraulic actuation.

Mechanization programs in India, Brazil, and sub-Saharan Africa accelerate tractor penetration and elevate hydraulic complexity. Three-point hitches, loader arms, and steering assist all depend on cylinders capable of precise flow-modulation under dusty, high-temperature conditions. Field research on hybrid hydraulic-electric drivelines shows peak-torque cuts of 18.8% during plowing, validating the technology's fuel-savings potential while preserving hydraulic force density. Localized assembly hubs help manufacturers sidestep tariff regimes and shorten lead times, reinforcing the hydraulic cylinder market's resilience in agriculture.

Efficiency gains of 75-80% and zero-leakage operation make electric actuators attractive for precision packaging, lab automation, and compact loaders. High-cycle life beyond 100 million strokes also tilts lifecycle economics away from hydraulics in these niches. Manufacturers mitigate risk by expanding portfolios to include hybrid and all-electric offerings, ensuring wallet-share retention even as the hydraulic cylinder industry experiences selective substitution.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Double-acting designs generated 57.74% of 2025 revenue, cementing their role in two-way load control for buckets, presses, and steering columns across the hydraulic cylinder market. Embedded pressure transducers elevate precision, enabling OEMs to achieve repeatability targets in automated welding lines. Single-acting models post a 5.93% CAGR as gravity-return architectures reduce pump sizing and fluid volume, a compelling trade-off for scissor-lifts and tipper bodies. Regenerative circuit options further cut energy draw, expanding addressable use-cases for cost-sensitive buyers.

The dual-market dynamic fosters tailored sourcing strategies. High-volume off-highway builders lock in multi-year supply agreements for double-acting cylinders with synchronized flow paths, while aftermarket distributors favor modular single-acting SKUs to match heterogeneous equipment fleets. Suppliers that can flex production between the two designs on common machining cells minimize changeover downtime and widen gross-margin spreads, reinforcing their competitiveness within the hydraulic cylinder market.

Welded cylinders contributed 44.15% of 2025 turnover thanks to their one-piece body strength and favorable cost-to-pressure ratio. OEMs in agriculture and mining specify welded models up to 3,000 PSI, leveraging integrated glands that shorten installation time. Telescopic cylinders, despite a smaller base, accelerate at a 6.14% CAGR as urban job-sites demand compact stowed lengths and extended reach. Telematik multi-section systems stretch seven stages without external chains, offering maintenance-free operation and cycle-time advantages.

Tie-rod and mill-type designs retain relevance in factory automation and metals processing respectively, where serviceability or extreme-duty requirements dictate product choice. Vendors differentiate through proprietary seal stacks that extend service intervals and through inline position sensing that satisfies Industry 4.0 data-collection mandates. This broad specification spectrum ensures the hydraulic cylinder market provides fit-for-purpose options across force, stroke, and duty-cycle axes.

The Hydraulic Cylinder Market Report is Segmented by Function (Single-Acting, and Double-Acting), Specification (Welded, Tie-Rod, Telescopic, and Mill-Type), Bore Size (Below 50 Mm, 50-150 Mm, and Above 150 Mm), End-User Industry (Construction Equipment, Agriculture, Material Handling and Forklifts, Mining, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific secured 40.62% of 2025 revenue and records an 6.73% CAGR, driven by megaprojects such as India's high-speed rail corridors and China's offshore wind build-out. Domestic champions like Hengli scale vertically integrated plants to replace imported high-end cylinders, trimming lead times and landed costs. Supplier proximity also aligns with just-in-time practices adopted by regional OEMs.

North America ranks second, buoyed by federal infrastructure spending that refreshes construction fleets and upgrades inland-port material-handling systems. Local producers differentiate via advanced metallurgy and digital integration, meeting end-user demand for data-rich equipment as predictive-maintenance adoption rises.

Europe emphasizes sustainability and noise reduction, prompting the uptake of smart electro-hydraulic designs that curtail energy waste. OEMs receive legislative stimulus from EU Green Deal directives, spurring orders for cylinders with biodegradable fluids and leak-prevention technologies.

The Middle East sees demand swings tied to oil-price cycles, but gas-processing expansion in Saudi Arabia revives large-bore cylinder orders for pipeline construction. Africa and Latin America benefit from agricultural mechanization subsidies and mining concessions, though currency volatility challenges importers. Across all regions, suppliers that offer localized service networks and rapid spare-parts fulfillment gain advantage in the hydraulic cylinder market.