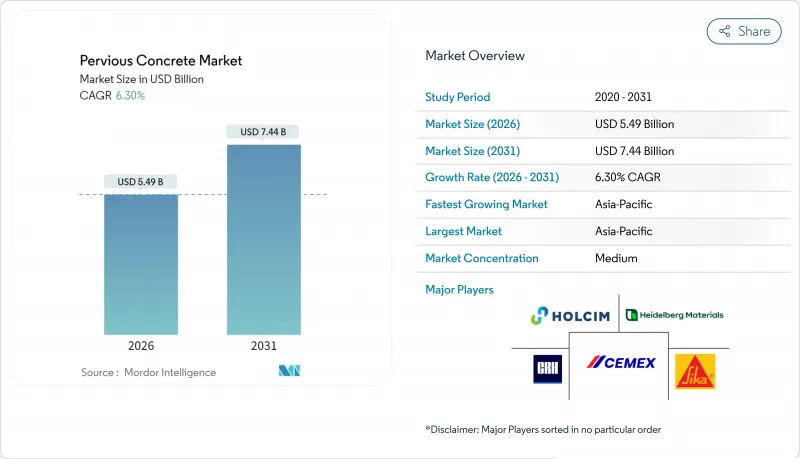

투수 콘크리트 시장 규모는 2026년에는 54억 9,000만 달러로 평가되었고, 2025년 51억 6,000만 달러에서 성장할 것으로 예상됩니다. 2031년까지의 예측은 74억 4,000만 달러에 이르렀으며, 2026-2031년에 걸쳐 연평균 복합 성장률(CAGR) 6.3%로 성장할 것으로 전망되고 있습니다.

도시 지역에서 발생하는 돌발 홍수 증가, 저영향개발(LID) 의무 규정, 지속가능한 건설에 대한 기업의 약속은 주거 및 상업 및 공공 인프라 프로젝트 전반에 걸쳐 투수 콘크리트에 대한 꾸준한 수요를 뒷받침하고 있습니다. 지방자치단체의 세제 혜택과 스펀지 도시 프로그램은 채택을 더욱 가속화하는 한편, 혼합 설계 및 폴리머 개질 기술의 발전은 이 재료의 구조적 적용 사례를 확대하고 있습니다. 다국적 시멘트 제조사들이 투수성 솔루션을 저탄소 포트폴리오에 통합하고 지역 건설사들이 전문 시공 장비에 투자함에 따라 경쟁 강도는 여전히 중간 수준을 유지하고 있습니다. 대도시의 숙련된 노동력 부족 및 골재 희소성과 같은 공급 측면의 어려움은 성장 전망을 계속해서 제약하고 있으나, 투수 콘크리트 시장의 전반적인 상승 추세를 저지하지는 못하고 있습니다.

지자체들은 빗물을 발생원에서 관리하기 위해 투수 콘크리트 적용을 확대하고 있으며, 이는 노후화된 하수 네트워크에 과부하를 주는 최대 유량을 감소시킵니다. 이 재료는 분당 평방피트당 최대 8갤런의 침투 능력을 보유하여 집중호우 시 유출량을 줄여주며, 중국 대도시 지역에서 10,000개 이상 설치된 스폰지 도시 프로젝트가 이를 입증하고 있습니다. 기후 변화와 연계된 강수 강도 증가는 포장면을 수동적 표면이 아닌 능동적 배수 자산으로 전환함으로써 가치 제안을 강화합니다. 지방 정부는 포장 및 우수 인프라를 단일 자본 지출로 통합하는 투과성 콘크리트의 이중 기능성을 선호합니다. 중간 강우 기후에서의 입증된 현장 성능은 과도한 회색 인프라 배관에 대한 비용 효율적 대안으로서의 지위를 더욱 공고히 합니다.

규제 동향은 투수성 포장재를 선택적 지속가능성 요소에서 규정적 요구사항으로 전환시키고 있습니다. 로스앤젤레스의 2024년 LID 조례는 대규모 불투수성 면적을 추가하거나 교체하는 부지에 대해 부지 내 저류 목표를 충족하도록 의무화하여 투수 콘크리트를 일괄적 규정 준수 경로로 자리매김하고 있습니다. 뉴욕시의 통합 우수 관리 규정은 저류 우선 원칙을 추구하며, 이로 인해 투수 콘크리트는 광범위한 녹색 인프라 체계 내에서 동등한 위상을 확보하게 되었습니다. 개발자들은 투수 콘크리트가 우수 관리, 열섬 현상 완화, LEED 인증 획득 등 여러 의무 사항을 단일 사양으로 충족시키기 때문에 이를 선호합니다. 더 많은 관할 구역에서 유사한 규정을 마련함에 따라, 투수 콘크리트 시장의 가시성은 2020년대 말까지 더욱 강화될 전망입니다.

성공적인 시공은 정확한 공극률 유지와 균일한 다짐을 요구하며, 이는 기존 콘크리트 시공 방식과 현저히 다릅니다. NRMCA의 인증 체계는 품질을 보장하지만, 특히 교육 자원이 부족한 신흥 시장에서 자격을 갖춘 시공자 풀을 제한합니다. 특수 롤러 스크리드와 포장 시험기는 계약업체의 초기 비용을 증가시켜 강력한 정책 지원이 있는 지역에서도 역량 확장을 늦춥니다. 이러한 인력과 장비 병목 현상은 프로젝트 일정 위험을 초래하고 입찰 가격을 상승시켜 투수 콘크리트 시장의 단기 성장을 저해할 수 있습니다.

2025년 투수 콘크리트 시장 점유율의 57.20%를 차지한 수문학적 사양은 주차장, 보도, 광장 등 현장 우수 관리 도구로서의 역할을 공고히 하고 있습니다. 지방자치단체의 저영향 개발(LID) 규정 및 스펀지 도시 프로젝트는 이 설계 유형에 지속적으로 새로운 수요를 유입시켜 투수 콘크리트 시장 내 지배력을 강화하고 있습니다. 표면 침투 시험 및 혼합물 최적화 기술 발전은 유지보수 비용을 절감하여 예산 제약 하에 운영되는 공공 부문 구매자에게 지속적인 매력을 제공하고 있습니다.

구조용 설계는 현재 절대 규모는 작지만, 공극 연결성을 저해하지 않으면서 압축 강도를 향상시키는 고분자 개질 바인더의 추진력으로 2031년까지 연평균 6.59% 성장률을 기록할 전망입니다. 연구에 따르면 수멘비율 0.3이 강도 향상과 수리적 성능이 교차하는 변곡점으로 확인되어, 엔지니어들이 저속 도로 갓길, 주차장, 버스 정류장에 구조용 투수성 포장재를 지정하도록 장려하고 있습니다. 현장 데이터가 이러한 하중 지지력 향상을 입증함에 따라, 구조용 혼합물의 투수 콘크리트 시장 규모는 중형 교통 및 경공업 분야로 확대될 전망입니다.

아시아태평양 지역은 연평균 복합 성장률(CAGR) 6.78%로 가장 빠르게 성장하는 지역이며, 36.05%의 최대 점유율을 차지하고 있습니다. 이는 중국의 스폰지 도시 계획이 주도하고 있으며, 이 계획만으로도 홍수 취약 도시 지역에 수천 킬로미터에 달하는 투수성 포장 도로가 조성되고 있습니다. 인도 제조사인 울트라테크(UltraTech)는 몬순 배수 요구에 부응하기 위해 투수성 혼합물을 현지화하고 있으며, 일본 엔지니어들은 현장 설치 주기를 단축하는 프리캐스트 모듈식 형식을 활용하고 있습니다. 이러한 혁신들은 종합적으로 예측 기간 중반에 북미 지역 규모를 추월할 수 있는 해당 지역의 잠재력을 강조합니다.

북미의 시장은 성숙한 규제 체계, 강력한 계약자 인증 프로그램, 그리고 관대한 지방자치단체 인센티브가 특징입니다. 미국 환경보호청(EPA)은 투수성 포장재를 최우수 관리 기법(BMP)에 포함시켜 연방 차원의 지지를 표명했으며, 이는 주 정부 조달 지침으로까지 확산되고 있습니다.

유럽은 회원국들이 투수성 포장 지침을 개선하고 재활용 골재 등 순환경제 원칙을 통합함에 따라 규제 주도형 수요가 꾸준히 증가하고 있습니다. 2024년 발표된 독일 설계 규정은 수리 성능 기준을 공식화하여 기존 도입을 저해했던 기술적 모호성을 해소했습니다. 남미와 중동 및 아프리카 지역은 현재 비중이 작지만, 가속화되는 도시화와 기후 적응 자금 지원이 투수성 포장 시범 사업을 촉진할 것으로 예상되며, 이로 인해 신흥 지역 전반에 걸쳐 투수 콘크리트 시장이 점차 확대될 전망입니다.

Pervious Concrete market size in 2026 is estimated at USD 5.49 billion, growing from 2025 value of USD 5.16 billion with 2031 projections showing USD 7.44 billion, growing at 6.3% CAGR over 2026-2031.

Rising urban flash-flood events, mandatory low-impact-development (LID) codes, and corporate commitments to sustainable construction underpin steady demand for pervious concrete across residential, commercial, and public infrastructure projects. Municipal tax incentives and sponge-city programs further accelerate adoption, while advances in mix design and polymer modification are widening the material's structural use cases. Competitive intensity remains moderate as multinational cement producers integrate permeable solutions into low-carbon portfolios and regional contractors invest in specialized placement equipment. Supply-side challenges, such as chiefly skilled-labor shortages and aggregate scarcity in megacities, continue to temper growth prospects but have not derailed the broader upward trajectory of the pervious concrete market.

Municipalities increasingly deploy pervious concrete to manage stormwater at its source, thereby reducing peak flows that overload aging sewer networks. The material's ability to infiltrate up to 8 gallons per square foot per minute lowers runoff volumes during cloudbursts, as evidenced by sponge-city projects that now exceed 10 000 installations across Chinese metropolitan areas. Escalating precipitation intensities linked to climate change enhance the value proposition by turning pavements into active drainage assets rather than passive surfaces. Local governments favor the dual-functionality of pervious concrete because it consolidates pavement and stormwater infrastructure into one capital outlay. Proven field performance in moderate-rainfall climates further cements its status as a cost-effective alternative to oversized gray-infrastructure pipes.

Regulatory momentum is shifting permeable pavements from optional sustainability features to prescriptive requirements. Los Angeles' 2024 LID Ordinance obliges sites adding or replacing large impervious expanses to meet on-parcel retention targets, positioning pervious concrete as a turnkey compliance pathway. New York City's Unified Stormwater Rule pursues a retention-first hierarchy that equally elevates the material within broader green-infrastructure frameworks. Developers gravitate toward pervious concrete because it satisfies multiple mandates-stormwater, heat-island mitigation, and LEED credits-within one specification. As more jurisdictions draft parallel codes, forecast visibility for the pervious concrete market strengthens through the end of the decade.

Successful installations rely on maintaining correct void ratios and uniform compaction, tasks that differ markedly from conventional concrete practice. The NRMCA's certification framework ensures quality but restricts the pool of qualified installers, especially in emerging markets where training resources are thin. Specialized roller screeds and pavement testers elevate start-up costs for contractors, slowing capacity expansion even in regions with strong policy tailwinds. This talent and equipment bottleneck imposes project scheduling risks and can inflate bid prices, dampening near-term growth in the pervious concrete market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hydrological specifications accounted for 57.20% of pervious concrete market share in 2025, anchoring the category's role as an on-site stormwater management tool for parking lots, sidewalks, and plazas. Municipal LID ordinances and sponge-city projects continue to funnel new demand into this design archetype, reinforcing its dominance in the pervious concrete market. Advances in surface infiltration testing and mix optimization are also reducing maintenance costs, preserving the appeal for public-sector buyers that operate on constrained budgets.

Structural designs, while currently smaller in absolute terms, are on course for a 6.59% CAGR to 2031, propelled by polymer-modified binders that elevate compressive strength without sacrificing void connectivity. Research pinpoints a 0.3 water-cement ratio as an inflection point where strength gains and hydraulic performance intersect, encouraging engineers to specify structural pervious pavements for low-speed roadway shoulders, parking garages, and bus stops. As field data validate these load-bearing enhancements, the pervious concrete market size for structural mixes is expected to broaden into mid-duty transit and light-industrial applications.

The Pervious Concrete Market Report is Segmented by Design (Hydrological and Structural), Application (Hardscape, Floors, and Other Applications), End-User Industry (Residential, Commercial, and Infrastructure), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific is the fastest-growing territory with a CAGR of 6.78% and also holds the largest share of 36.05%, spearheaded by China's sponge-city initiative, which alone accounts for thousands of pervious pavement kilometers across flood-prone urban districts. Indian manufacturers such as UltraTech are localizing permeable mixes to align with monsoon-drainage needs, while Japanese engineers leverage precast modular formats that shorten site installation cycles. Collectively, these innovations underscore the region's potential to eclipse North American volume midway through the forecast period.

North America's market is characterized by mature regulatory frameworks, robust contractor certification programs, and generous municipal incentives. The U.S. Environmental Protection Agency lists permeable pavements among its best-management practices, signaling federal endorsement that filters down to state procurement guidelines.

Europe posts steady, regulation-led demand as member states refine permeable pavement guidelines and integrate circular-economy principles, including recycled aggregates. German design codes published in 2024 formalize hydraulic-performance benchmarks, removing technical ambiguities that previously hampered adoption. While South America and the Middle-East and Africa contribute smaller shares for now, accelerating urbanization and climate-adaptation funding are expected to catalyze permeable-pavement pilots that will gradually scale the pervious concrete market across these emerging regions.