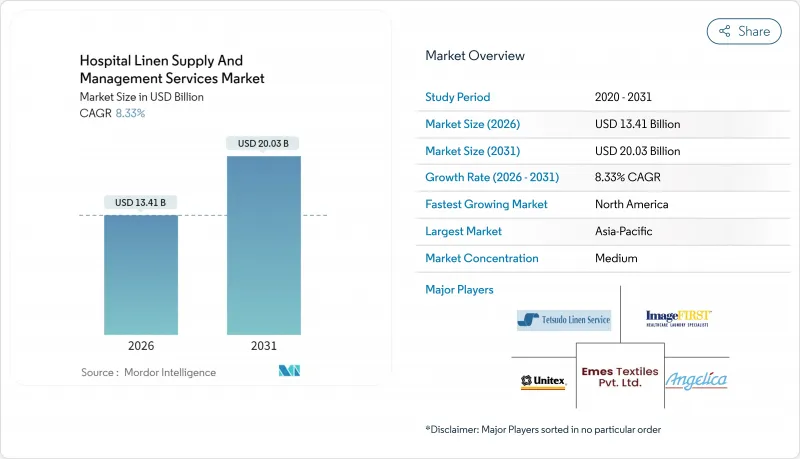

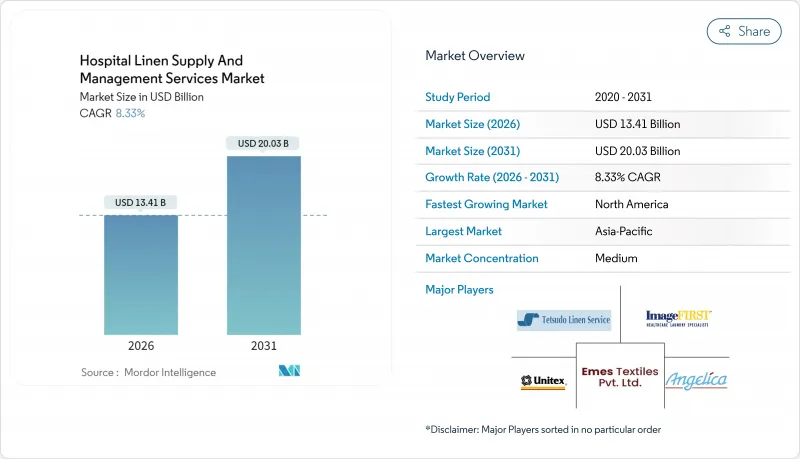

2026년 병원용 린넨 공급 및 관리 서비스 시장 규모는 134억 1,000만 달러로 평가되었고, 2025년 123억 8,000만 달러에서 성장을 계속하고 있습니다.

2031년에는 200억 3,000만 달러에 달할 것으로 예상되며, 2026-2031년에 걸쳐 CAGR 8.33%로 성장할 것으로 예측되고 있습니다.

지속적인 감염 관리 의무화, 병원 아웃소싱 전략, 신흥 경제국의 인구 구조 변화가 이러한 성장세를 뒷받침하고 있으며, 사모펀드 지원 통합 기업들이 기술 업그레이드에 자본을 투입해 린넨 손실을 10% 이상 줄이고 있습니다. 북미 공급업체들은 성숙한 규제 체계와 높은 준수 비용으로 인해 제3자 계약이 유리해 수익을 내는 반면, 아시아태평양 지역에서는 병원이 수천 개의 신규 병상을 추가하고 의료 관광 수요가 지속적으로 증가하면서 수요가 급증하고 있습니다. 소재 선택은 진화 중이며, 마이크로파이버가 빠른 건조 시간과 지속가능성 인증으로 인해 직조 면을 추월하고 있습니다. 동시에 마이크로플라스틱에 대한 감시가 공급업체의 혁신을 촉구하고 있습니다. 한편, 변동성 높은 린넨 및 에너지 가격은 영업 마진을 압박하여 공급업체들이 AI 기반 수요 예측 도구를 도입하도록 유도하고 있습니다. 이로 인해 표준 재고량을 20% 절감하고 비용 급등을 상쇄할 수 있습니다.

아시아태평양 지역의 급속한 병원 건설로 관리자들이 임상 서비스를 우선시함에 따라 전문 린넨 아웃소싱 수요가 증가하고 있습니다. 인도만 해도 향후 5년 내 22,000개 이상의 민간 병상을 추가할 계획으로, 이는 2019-2024 회계연도 기록을 훨씬 뛰어넘는 규모입니다. 증가하는 생활습관병과 중산층 확대가 이러한 수요 증가를 뒷받침합니다. 신규 수용 규모의 확대로 운영사들은 신속한 가동 및 규제 준수를 위해 비핵심 업무를 아웃소싱해야 합니다. 아웃소싱 업체들은 지역별 메가 세탁소를 설치해 세탁량을 통합하고 노선 밀집도를 활용해 단위 비용을 낮추는 방식으로 대응하고 있습니다.

미국 의료시설 인증기구(The Joint Commission)의 2024년 개정판은 표면 청결에 대한 기준을 강화하고 중복 조항을 삭제해 린넨 작업 흐름에 대한 감시를 강화했습니다. CDC 지침은 병원체 전파를 차단하기 위해 분리 처리, 개인 보호 장비(PPE), 인증된 처리 환경을 요구합니다. 미국 연방 규정 38 CFR 51.190은 이 의무를 강화하여 시설 관리자에게 경영진 책임을 부과합니다. 소규모 병원들은 규정 준수 장비에 대한 문서화 및 자본 지출에 어려움을 겪으며, 검증된 프로세스와 직원 교육을 묶은 전문 계약으로 전환하고 있습니다. 공급업체들은 모든 세탁 주기에 타임스탬프를 기록하는 규정 준수 대시보드를 활용하여 규제 기관과 보험사 모두를 만족시키는 감사 가능한 기록을 제공합니다.

린넨 수요는 인구 증가 속도보다 약간 빠르게 상승 중이며, 중국, 베트남, 방글라데시가 주요 수입국으로 남아 공급망 변동 위험을 증폭시키고 있습니다. 유기농 및 지속가능 린넨에 대한 프리미엄은 다년간 고정가격 계약 하에서 세탁업체가 전가하기 어려운 추가 비용층을 형성합니다. 한편 천연가스 및 전기 가격 급등은 병원 위생 관리에 필요한 고온 세탁 공정으로 인해 마진 완충 효과를 잠식하고 있습니다. 업체들은 연료 할증료 재협상과 열회수 시스템 설치를 통해 대응하고 있으나, 에너지 선물 시장이 안정화되기 전까지는 가격 압박이 지속될 전망입니다.

침대 시트 및 담요 부문이 2025년 병원 린넨 공급 및 관리 서비스 시장에서 43.12% 점유율로 최대 매출을 창출했습니다. 보편화된 침대 교체 프로토콜로 인해 병원은 매트리스당 여러 세트를 유지해야 하므로 높은 교체 주기와 안정적인 계약 물량이 발생합니다. 환자 가운 및 의류는 가장 빠르게 확장되는 품목으로, 일일 수술 건수 증가와 일회용 규정 강화로 2031년까지 연평균 9.05%의 성장률을 보일 전망입니다.

감염 예방 프로그램은 가운의 빈번한 교체를 권장하여 인구 변동성을 넘어 수요 탄력성을 높입니다. 타월 및 목욕용 린넨은 장기 요양 시설에서 꾸준한 수요를 보이며, 수술용 드레이프는 외래 시술량 증가와 함께 성장합니다. 환자 편의 지표를 높이는 프라이버시 커튼 교체 및 담요 온열 프로그램이 수요를 촉진하여, 공급업체가 고가 직물과 규정 준수 추적 기능을 묶어 제공할 수 있는 여지를 제공합니다. RFID 태깅은 이제 대부분의 고회전 품목에 적용되어 재고 부족을 줄이고 고객 유지력을 강화하는 디지털 청구 워크플로우를 지원합니다.

병원용 린넨 공급 및 관리 서비스 시장 보고서는 제품별(침대 시트, 베개 커버, 담요, 침대 커버, 기타), 소재별(직물, 부직포), 최종 사용자별(병원, 진단센터, 독립 클리닉), 지역별(북미, 유럽, 아시아태평양, 중동, 아프리카, 남미)로 업계를 세분화하고 있습니다. 지난 5년간의 데이터와 향후 5년간의 예측을 얻을 수 있습니다.

북미는 확고한 아웃소싱 문화, 엄격한 감염 관리 시행, 부가가치 서비스에 대한 공급자의 지불 의지 덕분에 2025년 41.88%의 점유율로 선두를 유지했습니다. Cintas는 2025 회계연도 3분기 매출 26억 1,000만 달러와 50.6%의 매출 총이익률을 기록하며 이 성숙한 지역의 가격 책정 영향력을 입증했습니다. Aramark의 Vestis 분사는 전문 유니폼 및 의료용 린넨에 대한 전략적 집중을 시사하며 지속적인 수요를 확인시켜 줍니다.

아시아태평양 지역은 2031년까지 연평균 11.42%의 성장률로 가장 빠르게 성장하는 지역입니다. 인도 민간 병원의 병상 22,000개 이상 증설과 중국 병상 확장이 이를 주도합니다. 의료 관광 유입은 서비스 품질 기대치를 높여 공급업체들이 서구식 규정 준수 기준과 디지털 추적 시스템을 도입하도록 촉진합니다. 사모펀드 유입은 공장 건설과 기술 이전을 촉진해 선진 지역과의 격차를 좁히고 있습니다.

유럽은 노후화된 인프라와 엄격한 환경 규제가 상충하는 가운데, 물 회수 시스템을 갖춘 세탁소를 선호하는 추세로 안정세를 유지하고 있습니다. 남미와 중동, 아프리카는 의료비 지출 증가와 인증 기관의 표준화된 린넨 관리 프로토콜 추진으로 신생이지만 성장 중인 시장입니다. 현지 보건부와 협력하는 초기 진입 기업들은 선점 효과를 얻고 장기적인 운영권을 확보하고 있습니다.

The hospital linen supply and management services market size in 2026 is estimated at USD 13.41 billion, growing from 2025 value of USD 12.38 billion with 2031 projections showing USD 20.03 billion, growing at 8.33% CAGR over 2026-2031.

Persistent infection-control mandates, hospital outsourcing strategies, and demographic shifts in emerging economies underpin this momentum, with private equity-backed roll-ups injecting capital for technology upgrades that lower linen loss by more than 10%. North American providers profit from mature regulatory frameworks and high compliance costs that favor third-party contracts, while Asia-Pacific demand escalates as hospitals add thousands of new beds and medical-tourism volumes keep climbing. Material choices are evolving, with microfiber gaining on woven cotton because of faster drying times and sustainability credentials, even as microplastic scrutiny pressures suppliers to innovate. Meanwhile, volatile cotton and energy prices squeeze operating margins, prompting providers to deploy AI-driven demand-sensing tools that trim par-stock by 20% and offset cost spikes.

Rapid hospital construction in Asia-Pacific is escalating demand for professional linen outsourcing as administrators prioritize clinical services. India alone plans to add more than 22,000 private beds within five years, dwarfing additions recorded between FY19-24. Growing lifestyle diseases and a rising middle class underpin this pipeline. The scale of new capacity forces operators to outsource non-core tasks to achieve quicker ramp-up and regulatory compliance. Outsourced providers respond by installing regional mega-laundries that pool loads and exploit route density to keep unit costs down.

The Joint Commission's 2024 revision sharpened focus on surface cleanliness while trimming redundant clauses, increasing scrutiny on linen workflows. CDC guidance now requires segregated handling, PPE, and certified processing environments to curb pathogen transmission. U.S. federal rule 38 CFR 51.190 reinforces the obligation, putting executive liability on facility managers. Smaller hospitals struggle with documentation and capital outlays for compliant equipment, prompting a shift toward specialist contracts that bundle validated processes and staff training. Providers leverage compliance dashboards that timestamp every wash cycle, supplying auditable trails that satisfy regulators and insurers alike.

Cotton demand is climbing slightly faster than population growth, with China, Vietnam, and Bangladesh remaining top importers, amplifying supply-chain swing risk. Premiums on organic and sustainable cotton add cost layers that laundries struggle to pass through under multi-year fixed-price contracts. Meanwhile, natural-gas and electricity spikes erode margin buffers given the high-temperature cycles required for hospital sanitation. Providers respond by renegotiating fuel surcharges and installing heat-recovery systems, yet pricing pressure persists until energy futures stabilize.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Bed Sheets & Blankets generated the largest revenue pool, commanding 43.12% share of the hospital linen supply and management services market in 2025. Ubiquitous bed-turnover protocols compel hospitals to maintain multiple sets per mattress, driving high replacement cycles and stable contract volumes. Patient Gowns & Apparel represent the fastest-expanding line, set to grow at a 9.05% CAGR to 2031 as day-surgery counts rise and single-use rules tighten.

Infection-prevention programs favor frequent gown changes, boosting demand elasticity beyond census variability. Towels and bath linens see steady pull from long-term care centers, whereas surgical drapes advance with outpatient procedure volumes. Stimulus comes from privacy curtain rotations and blanket-warming programs that heighten patient-comfort metrics, giving providers scope to bundle premium-priced textiles with compliance tracking. RFID tagging now spans most high-turnover items, shrinking stockouts and supporting digital billing workflows that fortify client retention.

The Hospital Linen Supply and Management Services Market Report Segments the Industry Into by Product (Bed Sheet & Pillow Covers, Blanket, Bed Covers, Others), by Material (Woven, Non-Woven), by End User (Hospital, Diagnostic Centers, Standalone Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Get Five Years of Historical Data and Five-Year Forecasts.

North America retained leadership with 41.88% share in 2025 thanks to entrenched outsourcing culture, rigorous infection-control enforcement, and provider willingness to pay for value-added services. Cintas posted USD 2.61 billion in fiscal Q3 2025 revenue with a 50.6% gross margin, underscoring pricing leverage in this mature region. Aramark's spinoff of Vestis signals strategic focus on specialized uniforms and healthcare linens, validating sustained demand.

Asia-Pacific is the fastest-growing territory at an 11.42% CAGR through 2031, propelled by bed additions exceeding 22,000 in Indian private hospitals and expanding Chinese capacity. Medical-tourism inflows intensify service-quality expectations, pushing providers to adopt western compliance benchmarks and digital tracking. Private-equity inflows fuel plant construction and technology transfer, compressing the gap with developed regions.

Europe remains steady, balancing aging infrastructure with stringent environmental directives that favor laundries boasting water-recovery systems. South America and the Middle East & Africa represent nascent but rising opportunities as healthcare spending grows and accreditation bodies promote standardized linen protocols. Early entrants partnering with local health ministries gain first-mover advantage and secure long-term concessions.