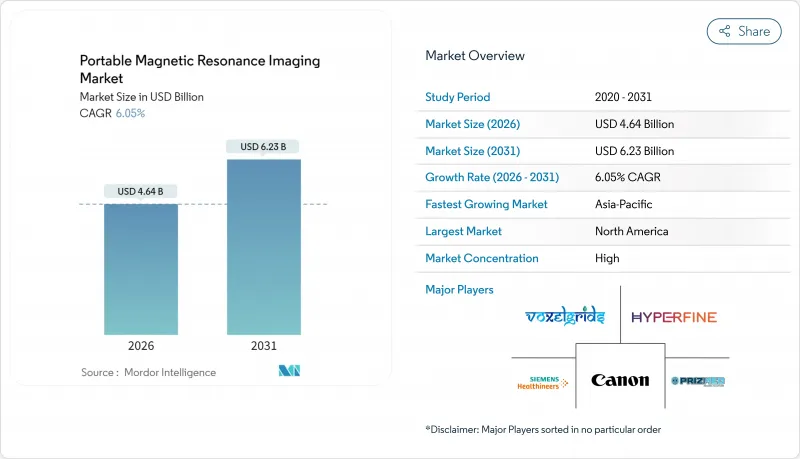

휴대용 MRI(자기공명영상) 시장은 2025년 43억 8,000만 달러로 평가되었으며, 2026년 46억 4,000만 달러에서 2031년까지 62억 3,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 6.05%로 예상됩니다.

이러한 성장은 초저자기장 설계, AI 기반의 이미지 강화 기술, 그리고 베드사이드 신경 집중 치료 진단에 대한 수요 증가가 더해져서 발생하고 있습니다. 병원이 가장 먼저 이 시스템을 도입하는 이유는 차폐실을 필요로 하지 않고 집중 치료 워크플로에 통합이 가능하기 때문이며, 벤처 자금은 제품 사이클을 단축하여 신속한 세계 전개를 가능하게 하고 있습니다. 이동식 뇌졸중 유닛으로의 통합으로 발병 후 1시간 이내의 뇌졸중 치료가 확대되고, 전장에서의 초기 시험에 의해 민간 시설을 넘은 대응 가능 기반이 확대되고 있습니다. 화상 해상도와 환급에 관한 과제는 여전히 남아 있지만, 2024년 11월의 CMS(미국 의료 보험 의료 서비스 센터)의 원격 스캔에 관한 가이드라인은 규제면에서의 전환점이 되어 제공업체의 신뢰성을 높이고 있습니다.

휴대용 장치는 차폐실이나 액체 헬륨 냉각을 필요로 하지 않으며, 자본 지출을 60% 이상 절감하고, 운용 비용과 기술자 요건을 낮춥니다. 카트식 스캐너 1대로 집중 치료실, 응급실, 지방 진료소로 이동하여 운용할 수 있어 고정식 장치의 평균 이용률을 대폭 상회할 수 있습니다. 총 소유 비용의 차이는 대규모 인프라 투자 없이 이미징 시스템을 확장해야 하는 예산 제약이 있는 의료 시스템에서 특히 중요합니다. 499달러에 달하는 전신 AI 강화 스캔과 같은 가격 혁신으로 일상적인 영상 진단에 대한 접근성이 더욱 민주화되고 있습니다.

Hyperfine의 9,000만 달러와 Chipiron의 1,700만 달러 규모 자금 조달 및 시뮬레이션 소프트웨어 기업에 대한 수백만 달러 규모의 시드라운드는 휴대용 MRI 시장이 응급, 지방 및 군사 분야를 동시에 커버할 가능성에 대한 투자자의 강한 확신을 보여줍니다. NVIDIA와 다중 스캐너 공급업체 간의 전략적 제휴는 AI 파이프라인을 가속화하고 이미징 하드웨어와 클라우드 컴퓨팅의 융합이 진행되고 있음을 뒷받침하고 있습니다.

0.064T에서 0.55T까지의 저자기장 자석은 1.5T 및 3T 시스템에 비해 신호 대 잡음비가 낮고 정밀한 해부학적 시각화를 손상시킵니다. AI에 의한 노이즈 제거로 차이가 줄어들지만, 물리적 한계에 의해 달성 가능한 공간 분해능에는 여전히 제약이 있으며 유연하고 경량인 코일은 고주파의 균질성을 저하시킵니다. 소아 신경종양학에서 미세 병변을 놓치는 문제는 3 차 의료 기관에서의 도입을 지연시키는 과제로 남아 있습니다.

2025년 휴대용 MRI 시장의 45.12%를 신경학 분야가 차지했으며, 신속한 베드사이드 뇌영상 진단이 초기 수요를 견인하고 있는 것으로 확인되었습니다. 이러한 이점은 휴대용 MRI 시장의 규모에서 해당 부문의 매출이 거의 절반을 차지함을 뒷받침하며 뇌졸중 및 외상성 뇌손상 사례에서 구체적인 워크플로 상의 이점을 드러냅니다. ACTION-PMR 다시설 공동시험은 긴급 대응 시간 프레임 내에서 고자기장 진단 판단과 90% 일치함으로써 신경과 의사의 신뢰성을 뒷받침하고 있습니다. 병원이 신경집중치료실(Neuro-ICU)에 스캐너를 설치하여 환자를 이송하지 않고 뇌부종이나 출혈을 감시하는 움직임이 퍼지는 가운데 성장이 계속되고 있습니다.

소아과 및 신생아 의료 분야는 CAGR 6.95%로 확대되고 있으며, 2031년까지 다른 모든 임상 분야를 웃도는 성장이 전망되고 있습니다. 베드사이드 이미징은 진정 위험을 줄이고 신생아의 이동을 필요로 하지 않습니다. 이는 집중 치료실에서 매우 중요한 요소입니다. 줄어든 음향 소음과 폐소 공포증을 일으키지 않는 개방형 보어 구조는 소아 환자의 불안을 완화합니다. AI 강화 재구성 기술에 의한 미세구조의 선명화에 의해 과거 유아의 뇌 스크리닝을 막고 있던 해상도 차이는 꾸준히 줄어들고 있습니다. 방사선과 의사가 하중 관절 평가에 체위 의존성 스캔을 활용함에 따라 근골격계에서의 사용이 증가하고 있습니다. 한편, 심혈관 및 복부 스캔은 시간 분해능과 공간 분해능이 향상될 때까지 제한적인 사용에 머무를 전망입니다.

북미는 2025년 세계 수익의 42.74%를 차지했으며 풍부한 벤처 자금, FDA 인가 제품, 조기 환급 협의를 배경으로 휴대용 MRI 시장을 견인했습니다. Hyperfine사의 누계 9,000만 달러 규모 자금조달이나 Chipiron사의 미국 시리즈 A 자금조달은 투자자의 의욕을 나타내는 한편, 국방부(DoD)의 조성금은 전장용 프로토타입의 개발을 뒷받침하며 이는 민간 외상 의료에 환원될 가능성이 있습니다. CMS(의료보험서비스센터)에 의한 원격검사기준의 승인은 향후 2년간 지불자코드의 확립을 촉진하는 규제면에서의 진전을 시사하고 있습니다.

아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 7.78%로 확대되어 지역별로 가장 높은 성장 속도가 예상됩니다. 중국의 농촌 진단 이니셔티브와 인도의 원격 방사선 네트워크는 비용 효율적인 이미징 솔루션의 비옥한 토양을 형성합니다. 일본은 6,300대의 설치 기반과 견고한 AI 연구 생태계를 통해 휴대용 MRI의 도입을 지원하고 있습니다. 이 지역에서는 첨단 영구 자석도 제조되고 있어 공급망의 단축과 가격 하락이 실현되고 있습니다. 이러한 요인은 중소득 국가에서 휴대용 MRI 시장의 확대를 촉진합니다.

유럽에서는 독일의 이동형 뇌졸중 유닛과 영국의 헬륨 프리 이동식 솔루션 등 각국의 의료 제도에 의한 실증이 진행되어 꾸준한 도입이 계속되고 있습니다. AI 탑재 휴대용 기기의 CE 마크 인증 취득에 의해 규제면에서의 경로는 정돈되었지만, 엄격한 의료 기술 평가(HTA) 심사에 의해 장기적인 성과가 실증될 때까지는 대규모 도입이 늦어지고 있습니다. 중동 및 아프리카와 남미는 여전히 개발도상 단계이지만 인구가 분산되어 영상진단 인프라가 한정된 지역에는 현장에 배치 가능한 유닛이 적합하며, 자금 조달 수단이 성숙하면 비약적인 보급의 기반이 갖추어질 전망입니다.

The Portable Magnetic Resonance Imaging Market was valued at USD 4.38 billion in 2025 and estimated to grow from USD 4.64 billion in 2026 to reach USD 6.23 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031).

Growth stems from the marriage of ultra-low-field magnet design, AI-based image enhancement, and a rising demand for bedside neuro-critical diagnostics. Hospitals adopt the systems first because they can embed them in intensive-care workflows without new shielded rooms, while venture funding shortens product cycles and enables rapid international roll-outs. Integration into mobile stroke units broadens first-hour stroke care, and early battlefield trials expand the addressable base beyond civilian facilities. Challenges around image resolution and reimbursement remain, yet November 2024 CMS guidelines on remote scanning mark a regulatory inflection that improves provider confidence.

Portable units avoid shielded rooms and liquid-helium cooling, cutting capital outlays by more than 60% while trimming operating costs and technician requirements. A single cart-based scanner can rotate among ICUs, emergency bays, or rural clinics, boosting utilization well above fixed-suite averages. The total-cost-of-ownership gap resonates in budget-constrained health systems that need imaging expansion without major infrastructure spend. Pricing innovations, such as USD 499 full-body AI-enhanced scans, further democratize routine imaging access.

USD 90 million raised by Hyperfine, USD 17 million by Chipiron, and multimillion-dollar seed rounds for simulation software firms illustrate deep investor conviction that the portable MRI market can serve emergency, rural, and military verticals simultaneously. Strategic tie-ups between NVIDIA and multiple scanner vendors accelerate AI pipelines and reinforce the thesis that imaging hardware and cloud computation are converging.

Low-field magnets between 0.064 T and 0.55 T generate lower signal-to-noise ratios than 1.5 T or 3 T systems, compromising fine anatomical visualization. While AI denoising narrows the gap, physics still caps achievable spatial resolution, and flexible lightweight coils reduce radio-frequency homogeneity. Missed micro-lesions in pediatric neuro-oncology remain a sticking point that slows adoption in tertiary centers.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Neurology accounted for 45.12% of the portable MRI market in 2025, confirming that rapid bedside brain imaging drives initial demand. This dominance supports a portable MRI market size commanding nearly half the segment revenue and demonstrates tangible workflow benefits in stroke and traumatic brain injury cases. The ACTION-PMR multicenter trial underpins neurologists' confidence by matching 90% of high-field diagnostic decisions within emergency timeframes. Growth continues as hospitals embed scanners in neuro-ICUs to monitor cerebral edema or hemorrhage without patient transfer.

Pediatrics and neonatal care is expanding at a 6.95% CAGR and is projected to outpace all other clinical groups through 2031. Bedside imaging mitigates sedation risks and eliminates neonatal transport, vital factors in intensive care nurseries. Reduced acoustic noise and an open, non-claustrophobic bore also lower distress in young patients. Subsequent AI-enhanced reconstruction further clarifies small structures, steadily narrowing the resolution gap that once barred infant brain screening. Musculoskeletal use grows as radiologists exploit position-dependent scans for weight-bearing joint assessment, while cardiology and abdominal scanning remain limited until temporal and spatial resolution improve.

The Global Portable MRI Market Report is Segmented by Application (Neurology, Musculoskeletal, Gastroenterology, Cardiology, Pediatrics/Neonatal, Others), Facility Type (Hospitals, Diagnostic Imaging Centers, Ambulatory Surgery Centers, Mobile Stroke Units & Field Deployments, Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

North America generated 42.74% of global revenue in 2025, anchoring the portable MRI market on the back of ample venture funding, FDA-cleared products, and the earliest reimbursement discussions. Hyperfine's USD 90 million cumulative raise and Chipiron's U.S. Series A exemplify investor appetite, while DoD grants sustain battlefield prototypes that could filter back to civilian trauma care. CMS recognition of remote scanning standards signals regulatory momentum likely to catalyze payer codes over the next two years.

Asia-Pacific is forecast to grow at an 7.78% CAGR through 2031, the highest regional pace. China's rural diagnostics initiatives and India's tele-radiology networks create fertile ground for cost-efficient imaging solutions. Japan supports portable MRI deployment through its 6,300-scanner installed base and robust AI research ecosystem. The region also manufactures advanced permanent magnets, shortening supply chains and lowering price points, factors that will expand the portable MRI market in mid-income economies.

Europe maintains steady adoption as national health systems validate mobile stroke units in Germany and helium-free truck solutions in the UK. CE-mark approvals for AI-powered portable units clear the regulatory pathway, yet stringent HTA reviews slow large-scale procurement until long-term outcomes are proven. Middle East & Africa and South America remain nascent, but field-deployable units are well suited to areas with dispersed populations and limited imaging infrastructure, setting the stage for leapfrog adoption once financing vehicles mature.