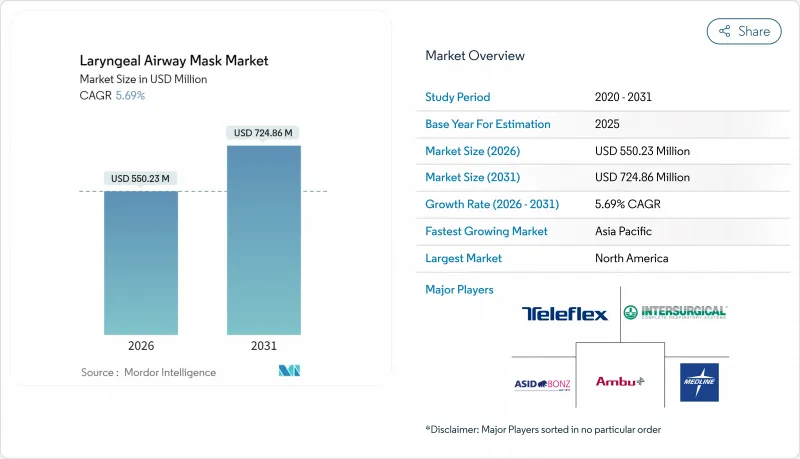

후두 마스크 기도기(LMA) 시장은 2025년 5억 2,060만 달러로 평가되었고, 2026년에 5억 5,023만 달러로 성장할 것으로 보입니다. 2026-2031년에 걸쳐 CAGR 5.69%의 성장이 예상되며, 2031년까지 7억 2,486만 달러에 이를 것으로 예측됩니다.

향후 5년간 고령 인구층의 선택적 수술 증가, 기관내 튜브 대비 강력한 비교 효과성 데이터, 팬데믹 이후 일회용 성문상 기도 장치로의 전환이 수술실, 외래 센터, 응급 서비스 전반에 걸쳐 높은 교체 수요를 유지할 것입니다. 위 배액 기능을 통합하고 더 높은 밀폐 압력을 달성하는 2세대 기기는 복강경 수술, 비만 수술, 외상 사례로 임상 적응증을 확장하는 한편, 진료실 기반 마취 및 병원 전 프로토콜은 이 기술을 새로운 치료 환경으로 끌어들이고 있습니다. 경쟁 강도는 여전히 중간 수준이지만, 공급업체들이 제품 업그레이드, 서비스 계약, 새로운 지속가능성 주장을 통해 브랜드 충성도를 방어함에 따라 혁신 주기는 가속화되고 있습니다.

기대 수명이 증가함에 따라 선택적 및 긴급 수술 건수가 계속 증가하여, 병원은 회전율을 단축하고 기도 외상을 최소화하는 장치를 선호하게 되었습니다. 2024년 심방세동 절제술 대상 성향 점수 매칭 분석에 따르면, 후두 마스크가 기관내관을 대체했을 때 회복 과정이 더 원활하고 기도 합병증이 적게 발생했습니다. 동반 질환이 많은 고령자는 더 부드러운 기도 관리 옵션의 혜택을 받으며, 이로 인해 후두상 장치는 정형외과, 종양학, 심장 수술 프로그램에 필수적입니다. 현재 지불 모델은 회복 시간 단축을 보상하므로, 수술실 책임자들은 처리량 증대를 위해 후두 마스크를 점점 더 표준화하고 있습니다.

소아 집단 대상 무작위 연구에서 LMA가 튜브 대비 호흡기 이상 반응 발생률이 낮은 것으로 확인되었습니다. 성인 데이터 역시 이 결과를 뒷받침하며, 신경외과 수술 중 혈역학적 스트레스 감소 및 이비인후과 시술 시 마취 유도 속도 향상을 보고합니다. 이러한 이점은 회복 촉진 프로토콜과 부합하여 전문 학회의 지침 업데이트를 촉진하고 있습니다.

위 배액 채널이 있음에도 불구하고, 많은 외상 및 산과 프로토콜은 여전히 위가 가득 찬 환자에게 기관내관을 기본으로 사용합니다. 새롭게 개정된 전투 의료 지침은 흡인 우려로 인해 특정 단계에서 성문상 장치를 제외합니다.

일회용 마스크는 2025년 후두 마스크 기도기 시장 매출의 61.92%를 차지했습니다. 감염 관리 측면의 우위성으로 인해 감염 예방 위원회가 다수 병원에서 “일회용 전용” 정책을 채택하도록 설득했습니다. 위액 배출 기능과 높은 밀폐 압력을 특징으로 하는 2세대 일회용 제품은 연평균 7.72% 성장률(CAGR)로 발전하며 평균 판매 가격을 상승시키고 일반 제품군의 ASP 압박을 상쇄하고 있습니다. 재사용 제품은 자원 제약이 있는 의료 시스템에서 여전히 사용되지만, 멸균 인건비와 추적성 비용이 일회용 제품 수준으로 상승함에 따라 점유율이 감소하고 있습니다. 비만 수술 및 로봇 수술용으로 설계된 특수 마스크는 수익성 높은 마이크로 부문를 개척하며 지속적인 연구개발을 촉진하고 있습니다.

OEM 업체들은 이제 무균 파우치 물류와 간소화된 재고를 최적화하여 수술 일정과 정확히 맞추고 있습니다. 규제 심사는 멸균 공정 검증을 중점적으로 다루며, ISO 준수 품질 시스템을 보유한 브랜드 공급업체를 선호합니다. 환경적 반발은 현실이지만, 초기 단계의 바이오플라스틱 프로토타입은 감염 관리와 순환 경제 의무 사이의 실현 가능한 중간 경로를 제시하고 있습니다.

후두 마스크 기도기(LMA) 시장 보고서는 제품 유형(일회용, 재사용 가능, 특수용도/2세대), 연령층(성인, 소아, 신생아), 최종 사용자(병원, 외래수술센터(ASC), 전문 클리닉, 응급 의료), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분석되고 있습니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

북미는 선진화된 수술실 인프라, 마취학 교육의 깊이, 메디케어 보상 안정성으로 2025년 글로벌 매출의 36.90%를 차지했습니다. 미국 병원들은 LMA를 지역 마취 주사 바늘 및 모니터링 일회용품과 묶어 공급하는 다년 유통 계약을 체결하여 물량 가시성을 확보하고 있습니다. 캐나다는 이러한 추세를 반영하는 반면, 멕시코의 민간 병원들은 국경 간 의료 관광 경쟁을 위해 2세대 마스크를 도입하고 있습니다.

아시아태평양 지역은 보건 인프라 지출과 급속히 증가하는 수술 역량에 힘입어 2031년까지 8.85%의 가장 빠른 연평균 성장률(CAGR)을 보일 전망입니다. 중국 지방 입찰에서는 성문상 기기와 마취 회로를 묶어 공급하며, 인도의 공공-민간 병원은 감염 관리 목표를 충족하기 위해 일회용 마스크를 지정하고 있습니다. 다국적 브랜드들은 공개된 임상 증거와 현지 제조 협력으로 1급 의료기관 시장 점유율을 방어하는 반면, 국내 신생 기업들은 2급 도시에서 가격 경쟁을 펼칩니다. ISO 13485 규격과의 규제 통합으로 해외 등록이 용이해졌으나 현장 감사가 요구되어 중소 수출업체의 진입 비용이 증가했습니다. 유럽은 중간 단일자리 수 성장률을 보이지만 환경 규제를 선도합니다. 새로운 전자 지침 프레임워크는 공급업체의 서류 작업 비용을 절감하지만, 2026년 포장 의무화로 규정 준수 비용이 증가합니다. 중동 시장은 사우디아라비아와 UAE의 병원 메가 프로젝트로 급성장 중이며, 양국 모두 고난도 수술 사례에 의존합니다. 아프리카 수요는 기부금 지원 외상센터에 집중되는 반면, 남미 확장은 브라질의 MDR(의료기기 규정)에 부합하는 규제 개혁이 주도합니다. 이러한 지역별 역학 관계로 인해 후두 마스크 기도기 시장은 프리미엄 혁신에 집중하는 고소득 시장과 접근성 높고 비용 효율적인 솔루션을 추구하는 신흥 경제국 사이에서 계속 분할될 전망입니다.

The laryngeal mask airways market is expected to grow from USD 520.6 million in 2025 to USD 550.23 million in 2026 and is forecast to reach USD 724.86 million by 2031 at 5.69% CAGR over 2026-2031.

Over the next five years, elective-surgery growth among aging populations, strong comparative-effectiveness data versus endotracheal tubes, and the post-pandemic shift to single-use supraglottic airway devices will sustain high replacement demand across operating rooms, ambulatory centers, and emergency services. Second-generation devices that integrate gastric drainage and achieve higher seal pressures expand clinical indications into laparoscopic, bariatric, and trauma cases, while office-based anesthesia and pre-hospital protocols pull the technology into new care settings. Competitive intensity remains moderate, yet innovation cycles are accelerating as suppliers defend brand loyalty through product upgrades, service contracts, and emerging sustainability claims.

Elective and urgent procedures keep climbing as life expectancy rises, pushing hospitals to favor devices that shorten turnover and minimize airway trauma. A 2024 propensity-score matched analysis in atrial-fibrillation ablation reported smoother emergence and fewer airway complications when laryngeal masks replaced endotracheal tubes. Comorbidity-laden seniors benefit from gentler airway options, making supraglottic devices integral to orthopedics, oncology, and cardiac surgery programs. Payment models now reward shorter recovery times, so operating-room directors increasingly standardize on LMAs to boost throughput.

Randomized studies in pediatric cohorts documented lower respiratory adverse-event rates with LMAs versus tubes. Adult data echo the findings, citing reduced hemodynamic stress during neurosurgery and faster anesthesia induction in ENT procedures. These benefits dovetail with enhanced-recovery protocols, prompting guideline updates from professional societies.

Despite gastric-drainage channels, many trauma and obstetric protocols still default to tubes for full-stomach patients. Newly revised combat-care guidelines omit supraglottic devices from certain phases due to aspiration fear.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Disposable masks generated 61.92% of laryngeal mask airways market revenue in 2025. Their infection-control edge convinced infection-prevention committees to adopt "single-use only" policies across many hospitals. Second-generation disposable units featuring gastric drainage and higher seal pressures are advancing at an 7.72% CAGR, raising average selling prices and offsetting commodity-line ASP compression. Reusables linger in resource-constrained health systems but lose ground as sterilization labor and traceability costs rise toward disposable parity. Specialty masks engineered for bariatric and robotic procedures carve out profitable micro-segments that encourage continuous R&D.

OEMs now optimize sterile-pouch logistics and lean inventory to match just-in-time surgery schedules. Regulatory audits spotlight sterilization process validation, favoring branded vendors with ISO-compliant quality systems. Environmental pushback is real, yet early-stage bioplastic prototypes indicate a feasible middle path between infection control and circular-economy mandates.

The Laryngeal Mask Airways Report is Segmented by Product Type (Disposable, Reusable, Specialty/Second-Generation), Age Group (Adult, Pediatric & Neonatal), End User (Hospitals, Ambulatory Surgical Centres, Specialty Clinics, Pre-Hospital Care), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

North America captured 36.90% of global revenue in 2025 due to advanced OR infrastructure, anesthesiology training depth, and Medicare reimbursement stability. U.S. hospitals sign multi-year distributor contracts that bundle LMAs with regional block needles and monitoring disposables, locking in volume visibility. Canada mirrors these trends, while private hospitals in Mexico adopt second-generation masks to compete for cross-border medical tourism.

Asia-Pacific exhibits the fastest 8.85% CAGR to 2031, propelled by health-infrastructure spending and rapidly rising surgical capacity. Chinese provincial tenders bundle supraglottic devices with anesthesia circuits, and India's public-private hospitals specify single-use masks to meet infection-control targets. Multinational brands defend share in tier-1 centers through published clinical evidence and local manufacturing tie-ups, while domestic challengers compete on price in tier-2 cities. Regulatory convergence with ISO 13485 eases foreign registrations yet demands on-site audits, raising entry costs for smaller exporters. Europe delivers mid-single-digit growth but pioneers environmental regulation. The new electronic-instructions framework cuts paperwork costs for suppliers, yet 2026 packaging mandates heighten compliance spend. Middle East markets grow swiftly on hospital mega-projects in Saudi Arabia and the UAE, both reliant on high-acuity surgical caseloads. African demand remains concentrated in donor-funded trauma centers, while South American expansion is led by Brazil's MDR-aligned regulatory reforms. Together, these regional dynamics ensure that the laryngeal mask airways market continues to divide between high-income markets focused on premium innovations and emerging economies seeking accessible, cost-reliable solutions.