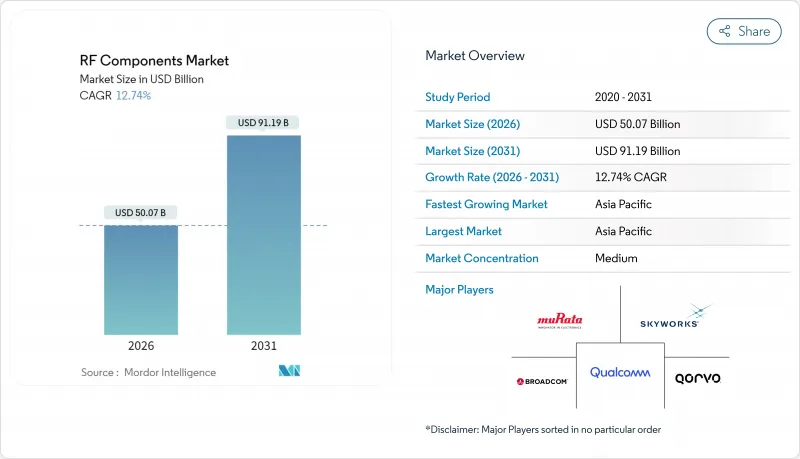

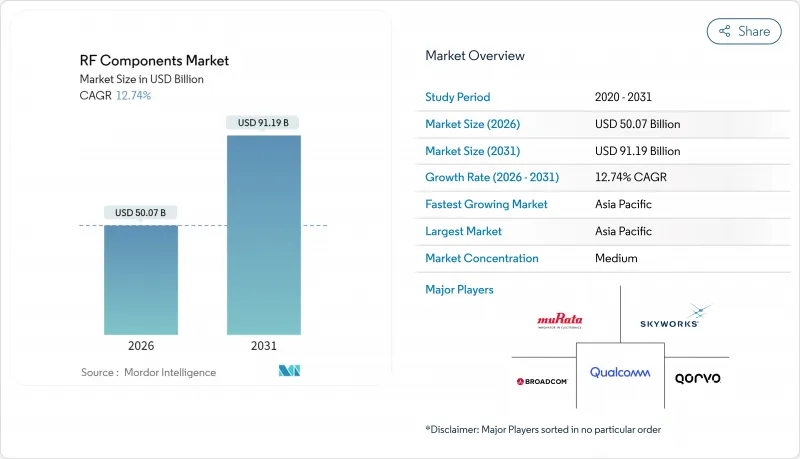

RF 컴포넌트 시장은 2025년 444억 1,000만 달러로 평가되었으며, 2026년 500억 7,000만 달러에서 2031년까지 911억 9,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 12.74%로 예상됩니다.

이러한 성장 경로는 5G 기지국, 레이더 중심의 자율주행 차량, 우주 통신 플랫폼의 급격한 도입을 반영합니다. 반도체 공급망의 현지화를 추진하는 정부 프로그램, 40GHz 이상의 주파수대에서의 기술적 혁신, 스마트폰의 고기능화가 함께 수요의 기세를 뒷받침하고 있습니다. 경쟁 전략에서는 수직 통합, AI 지원 설계 자동화, 첨단 열 관리 패키징이 중시되고 있으며, 지정학적 어려움을 극복하면서 성능과 비용 간의 균형을 유지하는 공급업체에게 기회가 열리고 있습니다. RF 컴포넌트 시장은 또한 주파수에 대해 민첩하고 전력 효율적인 아키텍처를 필요로 하는 Open RAN, 저궤도(LEO) 위성 별자리, 엣지 AI 산업 자동화에 대한 정책 주도 투자의 혜택을 받고 있습니다.

이동통신사는 5G 매크로셀 네트워크의 밀도를 계속해서 높이고 있으며, 고효율 파워 앰프, 저손실 필터, 고열 부하에 견딜 수 있는 빔 스티어링 스위치가 요구되고 있습니다. 이 전략은 Open RAN 프로그램과 특히 4억 5,000만 달러 규모의 '공공 무선 공급망 혁신 기금'에 의해 강화되어 멀티벤더 상호 운용성을 갖춘 소프트웨어 정의 아키텍처를 강조하고 있습니다. MaxLinear와 RFHIC에 의한 55.2% 효율의 GaN 파워 앰프 개발 등의 제휴는 대규모 전개에서의 에너지 절약에 대한 주력을 나타내고 있습니다. 매크로셀은 스몰셀보다 높은 출력을 제공하므로 성숙한 GaN 프로세스를 가진 공급업체가 경쟁 우위를 얻습니다. 2027년까지의 정책 지원으로 수요가 지속되고, RF 컴포넌트 시장은 중기적인 수익 전망에 견고한 기반을 얻고 있습니다.

레벨 3 대응 차량에는 현재 전용 V2X 트랜시버 외에도 여러 77-81GHz 레이더 센서가 탑재되어 2023년 모델에 비해 유닛당 RF 컴포넌트 수가 두배로 증가하고 있습니다. 북미 및 유럽 규제 당국은 첨단 운전 지원 시스템(ADAS)에 기능 안전 표준을 준수하도록 의무화하고 있으며, 이로 인해 자동차 제조업체는 완전히 인증된 자동차 등급 RF 공급업체를 선택할 수 없습니다. ISO 26262 인증 및 FCC Part 15 준수 요구사항은 검증된 신뢰성을 갖춘 공급업체에 대한 조달을 더욱 제한합니다. 레이더와 V2X의 이중 용도는 설계의 복잡성을 증가시키고 절연성과 공존성을 양립시키는 통합 프론트엔드 모듈에 대한 수요를 높입니다. 높은 Q값의 유전체 재료에 대한 리드 타임은 여전히 길어 단기적인 공급 위험을 초래하는 반면 인증된 재고품의 가격 상승을 뒷받침하고 있습니다.

신규 화합물 반도체 라인의 건설 비용은 20억-50억 달러에 이르며 TSMC의 애리조나 공장의 완공에 1,650억 달러를 넘는 투자가 필요한 점이 그 실태를 나타내고 있습니다. CHIPS법의 우대조치가 있어도 중소 진출기업은 분자선 에피택시(MOCVD) 장치에 대한 자금 조달에 고전하고 있습니다. 연방 정부의 지원을 받은 MACOM의 1억 8,000만 달러 규모 확장 계획은 정부 원조가 자본 장벽을 상쇄할 수 있지만 해소할 수는 없음을 보여줍니다. 수년에 걸친 건설 및 인증 사이클은 시장 진입을 늦추고 업계 재편을 촉구하며 감가상각된 자산을 가진 기존 기업에 유리하게 작용합니다.

2025년 시점에서 RF 컴포넌트 시장에서는 파워 앰프가 가장 큰 점유율을 차지하여 162억 3,000만 달러에 달했습니다. 매크로셀 무선, 레이더 모듈, 홈 게이트웨이 기기에서의 확고한 역할이 수량 수요를 뒷받침하여 효율화에 대한 대처가 강화되는 가운데서도 그 지위는 흔들리지 않습니다. 한편, RF 튜너블 디바이스는 2031년까지 연률 13.74%로 성장할 전망입니다. 기업은 특히 Open RAN LEO 단말기에서 소프트웨어 정의 아키텍처를 통한 네트워크 업그레이드 효율성을 높이기 위해 원활한 크로스 트랜지션을 제공하는 이러한 구성 요소를 도입하고 있습니다. 퀄컴의 X85 모뎀-RF 플랫폼은 필터와 스위치를 동적으로 조정하는 AI 엔진을 통합하여 보다 스마트한 프론트엔드로의 발전을 시사합니다. 파워 앰프, 저잡음 증폭기 및 튜너를 단일 모듈에 통합하는 공급업체는 고객에게 기판 면적 축소와 열 설계 완화를 제공하며, 이 동향은 Qorvo의 최신 Wi-Fi 7 프론트엔드 모듈에서도 현저합니다.

2차적인 효과도 이 흐름을 뒷받침하고 있습니다. 5G NR Release 18의 고차 MIMO 토폴로지는 기지국당 신호 경로 수를 증가시키고 경로당 전력 소비가 감소하더라도 전력 증폭기 소켓 수를 증가시킵니다. 스마트폰에서는 비연속 캐리어 어그리게이션을 활용하는 5G 대기 모드의 보급에 따라 안테나 스위치 다중화가 증가하여 RF 스위치의 매출을 견인하고 있습니다. 통합 필터 스위치 뱅크는 전체 서브 6GHz 대역에서 공존을 지원하여 선형성을 유지하면서 부품 비용을 줄입니다.

서브 6GHz 대역은 LTE 및 초기 5G 무선 기기의 압도적인 보급으로 인해 여전히 RF 컴포넌트 시장 점유율의 62.10%를 차지하고 있습니다. 그러나 40-100GHz 대역은 기업용 고정 무선 액세스(FWA), 백홀 링크, 신규 6G 연구 회랑에 힘입어 13.63%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있습니다. NTIA(미국 통신 정보국)의 6G 이용 사례에 대한 공적 협의는 차세대 기가비트 서비스를 위해 이러한 고주파 대역을 활용하려는 정부의 의도를 강조합니다. 열 설계를 의식한 패키징 기술에 뛰어난 공급업체는 이 새로운 파도를 활용하는 태세를 갖추고 있습니다. 24-40GHz대는 밀집한 도시에서의 mm파 5G의 열설계, 설치 물류, 백홀 비용의 영향으로 꾸준하면서도 완만한 보급이 예상되지만 대규모 전개 속도는 억제되고 있습니다.

기술의 성숙은 경쟁을 촉진합니다. 위상 시프터가 내장된 빔 스티어링 IC는 데이터센터 옥상 링크에 필요한 안테나 개구부를 축소하고 GaN-on-SiC 파워 앰프는 관리 범위 내의 드레인 전압으로 더 높은 EIRP를 실현합니다. FCC의 mm파 서비스 규정 등의 규제 무결성은 확실성을 높이지만, 위성 기존 사업자와의 고도의 공존 관리가 여전히 요구되고 있습니다.

2025년 아시아태평양은 RF 컴포넌트 시장을 독점하여 55.85%의 점유율을 차지했습니다. 이 급성장은 중국에서만 18개의 신규 공장이 가동을 시작한 것이 주요 요인입니다. 정부 보조금은 단가를 효과적으로 줄이고 주요 OEM 제조업체에 대한 지리적 근접성이 가시성을 높입니다. 기판 재료나 필터용 세라믹 분야에서는 한국과 일본이 계속 주도적 입장에 있는 한편, 대만의 파운드리는 멀티칩 모듈용 선진 패키징 기술로 최첨단을 달리고 있습니다. 생산 연동형 장려책(PLI)을 배경으로 한 인도의 5G 추진은 백엔드 조립 공정의 유치로 이어지고 있지만, 현재는 대규모 웨이퍼 제조 공장이 부족합니다. 무역제한이 강화되는 가운데 아시아태평양의 비용 우위성은 향후 10년간 세계 출하량의 절반 이상을 지원할 것을 보장하고 있습니다.

북미는 CHIPS법의 물결을 타고 있습니다. TSMC의 애리조나 공장은 4나노미터급 공정의 도입 뿐만 아니라, 선진적인 RF 패키징을 미국 고객에게 공급하는 역할도 담당하고 있습니다. 이 움직임은 물류 위험을 크게 줄이고 방위 공급망의 안전을 강화합니다. 또한 무선 혁신기금에서 제공한 1억 1,700만 달러의 연방 보조금이 국내 오픈 RAN 무선 개발을 추진하고 사업을 미국의 RF 전문 기업으로 유도하고 있습니다. 캐나다는 중주파수대 5G용 통신 인프라를 강화하고 있지만 부품 수입은 주로 미국에 의존하고 있습니다. 한편, 멕시코의 EMS(전자기기 수탁제조) 부문은 소비자용 가정기기(CPE)용 저비용 조립 계약을 활용하고 있습니다. 유럽은 2030년까지 세계 반도체 시장에서 20% 점유율 획득을 목표로 '유럽 CHIPS법'을 통한 전략적 자율성 확립을 추진하고 있습니다. 독일과 프랑스에서는 자동차 OEM 클러스터가 Euro NCAP 안전 기준을 충족하는 레이더 모듈의 생산 기지를 설립하여 현지 팹 가동률 향상에 기여하고 있습니다. 영국의 1,600만 파운드 규모의 LEO 프로그램은 Ka 밴드 부품의 연구 개발을 지원하고 신흥 우주 공급망을 육성하고 있습니다. 북유럽 국가들은 지역 광대역을 위한 mm파 고정 무선 액세스를 시험적으로 도입하고 미국 및 일본 공급업체에서 GaN 프론트엔드 장비를 조달하고 있습니다. 그러나 REACH 화학물질 규제와 같은 규제상의 과제로 인해 부품의 인증주기가 장기화되고 있으며 유럽의 컴플라이언스 실적을 가진 기존 기업에 의도치 않게 유리하게 작용하고 있습니다.

The RF components market was valued at USD 44.41 billion in 2025 and estimated to grow from USD 50.07 billion in 2026 to reach USD 91.19 billion by 2031, at a CAGR of 12.74% during the forecast period (2026-2031).

The growth path reflects surging deployments of 5G base stations, radar-centric autonomous vehicles, and space-based communications platforms. Government programs that localize semiconductor supply chains, breakthroughs in frequencies above 40 GHz, and rising content per smartphone collectively reinforce demand momentum. Competitive strategies emphasize vertical integration, AI-assisted design automation, and advanced thermal packaging, opening opportunities for suppliers able to balance performance and cost while navigating geopolitical headwinds. The RF components market also benefits from policy-driven investments in Open RAN, low-Earth-orbit (LEO) constellations, and edge-AI industrial automation, all of which require frequency-agile, power-efficient architectures.

Mobile operators continue to densify 5G macro-cell networks, requiring high-efficiency power amplifiers, low-loss filters, and beam-steering switches that can withstand elevated thermal loads. The strategy is reinforced by Open RAN programs, notably the USD 450 million Public Wireless Supply Chain Innovation Fund, which incentivizes multi-vendor interoperability software-defined architectures. Partnerships, such as MaxLinear RFHIC's 55.2% efficiency GaN power amplifier, underline the focus on energy savings for large-scale deployments. As macro cells deliver higher power than small cells, suppliers with a mature GaN process gain a competitive edge. Policy support through 2027 ensures sustained demand, giving the RF components market a strong anchor for mid-term revenue visibility.

Each Level-3-ready vehicle now features multiple 77-81 GHz radar sensors, alongside dedicated V2X transceivers, which doubles the RF content per unit compared to 2023 models. North American and European regulators require advanced driver-assistance systems (ADAS) to meet functional safety norms, nudging OEMs toward fully qualified automotive-grade RF suppliers. ISO 26262 certification and FCC Part 15 compliance further restrict sourcing to vendors with proven reliability records. The dual use of radar and V2X intensifies design complexity, increasing demand for integrated front-end modules that balance isolation and coexistence. Lead times for high-Q dielectric materials remain elevated, posing short-term supply risks yet reinforcing premium pricing for qualified inventories.

A new compound-semiconductor line can cost USD 2-5 billion, underscored by TSMC's Arizona outlay that eclipses USD 165 billion when fully built. Even with CHIPS Act incentives, smaller entrants struggle to secure financing for molecular-beam epitaxy MOCVD tools. MACOM's USD 180 million expansion, subsidized by federal backing, illustrates how government aid can offset but not erase capital hurdles. The multiyear build--qualify cycle delays market entry, encouraging consolidation, and favoring incumbents with depreciated assets.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Power amplifiers generated the largest slice of the RF components market in 2025, accounting for USD 16.23 billion. Their entrenched role in macro-cell radios, radar modules, home-gateway equipment anchors volume demand, even as efficiency mates intensify. Meanwhile, RF tunable devices compound at 13.74% annually through 2031. Enterprises adopt these components to enable seamless cross-b transition, especially in Open RAN LEO terminals, where software-defined architectures streamline network upgrades. Qualcomm's X85 modem-RF platform integrates an AI engine that dynamically tunes filters and switches, highlighting the march toward smarter front ends. Suppliers that merge power amps, low-noise amps, and tuners into single modules help customers shrink board area while easing thermal budgets, a trend visible in Qorvo's latest Wi-Fi 7 front-end modules.

Second-order effects reinforce this trajectory. Higher-order MIMO topologies in 5G NR Release 18 boost the number of signal paths per base station, multiplying power-amplifier sockets even when per-path wattage tapers. In smartphones, antenna-switch multiplexing rises with 5G STBY modes that leverage non-contiguous carrier aggregation, driving RF switch shipments. Integrated filter-switch banks support coexistence across Sub-6 GHz spectra, preserving linearity while containing BOM costs.

The Sub-6 GHz domain still owns 62.10% of the RF components market share thanks to the sheer footprint of LTE early 5G radios. However, the 40-100 GHz band grows the fastest at a 13.63% CAGR, favored by enterprise fixed-wireless access (FWA), backhaul links, and emerging 6G research corridors. NTIA's public consultation on 6G use cases underscores governmental intent to leverage these higher bands for next-generation gigabit services. Suppliers adept at thermal-conscious packaging position themselves to capitalize on this incremental wave. The 24-40 GHz class observes steady, yet slower, adoption in dense urban mmWave 5G-thermal design, siting logistics, and backhaul costs temper mass rollout velocity.

Technical maturation drives competitive behavior. Beam-steering ICs with embedded phase shifters shrink the antenna aperture needed for data-center roof links, while GaN-on-SiC power amplifiers unlock higher EIRP at manageable drain voltages. Regulatory alignment, such as the FCC's millimeter-wave service rules, fosters certainty but still demands sophisticated coexistence management with satellite incumbents.

The RF Components Market Report is Segmented by Component Type (Power Amplifiers, RF Filters, Antenna Switches, and More), Frequency Band (Sub-6 GHz, 6-24 GHz, and More), Semiconductor Material (GaAs, Silicon, Gan, Sige), End-User Industry (Consumer Electronics, Telecommunication, Automotive, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

In 2025, Asia-Pacific dominated the RF components market, claiming a 55.85% share. This surge was largely fueled by the inauguration of 18 new fabs in China alone. Government subsidies have effectively reduced unit costs, and the region's proximity to key OEMs has bolstered visibility. While South Korea and Japan continue to lead in substrate materials and filter ceramics, Taiwan's foundries are at the forefront, providing advanced packaging for multichip modules. India's push for 5G, backed by the Production-Linked Incentive (PLI) scheme, is drawing backend assembly operations, though the country currently lacks a significant wafer-fab scale. Even with rising trade restrictions, Asia-Pacific's cost advantages ensure it anchors over half of the global shipments for the foreseeable decade.

North America is riding the wave of the CHIPS Act. TSMC's facility in Arizona is not only introducing 4-nanometer class processes but also bringing advanced RF packaging closer to U.S. clients. This move significantly reduces logistics risks, bolstering the security of defense supply chains. Additionally, federal grants amounting to USD 117 million, sourced from the wireless innovation fund, are championing domestic Open RAN radio development, steering business towards American RF specialists. While Canada is upgrading its telco infrastructure for mid-band 5G, it predominantly relies on U.S. component imports. Meanwhile, Mexico's EMS sector is capitalizing on low-cost assembly contracts for customer premises equipment (CPE) devices. Europe, eyeing a 20% share of the global semiconductor market by 2030, is positioning itself for strategic autonomy through the European Chips Act. In Germany and France, automotive OEM clusters are anchoring radar modules to meet Euro NCAP safety standards, boosting local fab utilization. The UK's GBP 16 million LEO program is backing Ka-band component R&D, nurturing a nascent space supply chain. Nordic nations are experimenting with millimeter-wave fixed wireless access for rural broadband, procuring GaN front-end equipment from U.S. and Japanese suppliers. However, regulatory challenges, such as the REACH chemistry rules, are extending part qualification cycles, inadvertently benefiting established players with a history of European compliance.