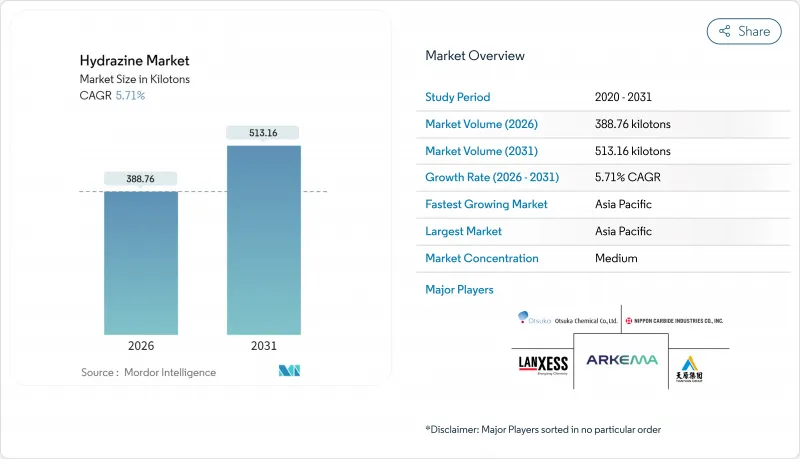

히드라진 시장은 2025년에 367.75킬로톤으로 평가되었고, 2026년 388.76킬로톤에서 2031년까지 513.16킬로톤에 이를 것으로 예측되고 있습니다.

예측기간(2026-2031년) 동안의 CAGR은 5.71%로 추계하고 있습니다.

히드라진은 농약, 부식 방지, 폴리머 폼 및 신흥 에너지 시스템에서 대체 불가능한 역할을 담당하면서 수요가 회복되고 있습니다. 유럽과 북미의 규제 감시는 지속적으로 강화되고 있지만, 아시아태평양의 생산 능력 향상은 다른 지역의 잠재적 생산량 감소를 상쇄하고 있습니다. 공급측 투자는 히드라진 수화물의 보다 안전한 제조 공정에 집중하고 있는 반면, 의약품 및 연료전지 기술의 다운스트림 사용자는 새로운 성장의 길을 열고 있습니다. 경쟁 우위는 원료 확보 및 컴플라이언스 비용 관리를 목적으로 하는 수직 통합 및 장기 계약에 초점이 맞춰져 있습니다.

중국, 인도, 브라질에서 농업 집약화의 진전으로 농약 소비량이 높은 수준을 유지하고 있으며, 히드라진은 말레익 히드라지드, 이소옥사졸리돈 및 기타 성장 조절제의 활성 성분에 필수적인 중간체로 사용되고 있습니다. 중국의 선도적인 제조업체는 국내 및 수출 파이프라인 모두에 공급하는 20만톤 이상의 전용 생산 능력을 가지고 있으며 이는 제형 제조업체의 공급 안정성을 뒷받침합니다. 나노엔지니어링된 히드라진 유도체에 대한 연구는 저용량으로 완전한 해충 방제를 가능하게 하고, 효과를 유지하면서 환경 부하를 저감할 수 있는 가능성을 나타내고 있습니다. 이 지역에서는 식량 안보에 대한 규제적 초점이 즉각적인 환경 규제보다 앞서기 때문에 히드라진 시장이 지속되고 있습니다.

히드라진 골격은 항결핵제, 항염증제, 항우울제의 선택적 합성을 가능하게 하고, 최근의 프로세스 혁신에 의해 온화하고 용제 효율이 높은 조건 하에서 89-97%의 수율이 달성되고 있습니다. 피롤 히드라존과 같은 임상 후보 물질은 치료 농도에서 결핵균을 억제하기 때문에 미국과 인도의 의약품 원료(API) 제조업체에서의 수요가 확대되고 있습니다. 독성 우려에 대처하기 위해, 생산자는 대량의 히드라진을 다룰 필요가 없는 간접적인 합성 경로를 확대하면서 그 특이적인 친핵성을 활용하고 있습니다. 그 결과, 의약품 분야는 히드라진 시장에서 가장 성장이 빠른 사용자층으로 지속될 것으로 예측됩니다.

히드라진은 유럽 화학물질청의 '고위험 물질 목록'에 등록되어 있으며, 엄격한 인가 요건과 작업상 노출 한계치가 적용됩니다. 현재는 밀폐식 이송 라인, 스크러버 시스템, 지속적인 대기 모니터링이 컴플라이언스 요건이 되고 있으며, 독일, 프랑스, 미국에서 제제 제조업체의 운영 비용 상승을 초래하고 있습니다. 간독성과 발암성과 관련된 책임 문제로 보험사는 보험료 인상을 요구하고 있으며 이는 신규 진입을 막고 있습니다. 아시아태평양의 규제는 현재 상대적으로 완만하지만, 다국적 기업 고객이 세계 기준의 컴플라이언스를 요구하는 경향이 강해지고 있으며, 세계적으로 높은 안전 기준이 점차 확대되고 있습니다.

히드라진 시장에서 2025년 판매량의 60.17%를 차지한 부문은 히드라진 수화물이며, 부문별 가장 높은 5.89%의 연평균 복합 성장률(CAGR)을 기록할 전망입니다. 수화물 등급이 선호되는 이유는 무수물에 비해 증기압이 낮으며 ISO 탱크 물류가 단순화되고 규제 인증이 원활하기 때문입니다. 보일러 수처리, 폴리머 발포, API 합성 플랜트는 현장의 위험 프로파일을 줄이기 위해 전용 수화물 저장 설비를 설치하여 수요 안정성을 강화하고 있습니다. 황산 히드라진과 같은 특수 염은 보다 엄격한 화학량 제어가 필수적인 전자기기 및 분석 분야의 틈새 시장에 공급되고 있습니다.

규제 당국은 현재 최대한 명확한 수화물 등급을 권장하고 있으며, 이에 따라 의약품 규제 적합을 목적으로 한 고순도 저금속 함유 배합 기술에 대한 공급자의 투자가 촉진되고 있습니다. 연료전지 개발자도 전력 밀도와 휘발성 관리를 양립하는 액체 캐리어 프로토타입에 일수화물을 도입하고 있으며 이는 수요의 점진적인 증가를 뒷받침하고 있습니다. 이러한 동향이 결합되어 히드라진 수화물의 우위성을 확고하게 하고 무수 형태에 대한 임박한 규제의 전면적인 영향으로부터 해당 부문을 보호하고 광범위한 히드라진 시장을 뒷받침하고 있습니다.

히드라진 시장 보고서는 유형별(히드라진 수화물, 질산 히드라진, 황산 히드라진, 기타), 용도별(부식 방지제, 폭발물, 로켓 연료, 의약품 원료 등), 최종 사용자 산업별(제약, 농약 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 구분됩니다. 시장 예측은 수량(톤) 단위로 제공됩니다.

아시아태평양은 2025년에 히드라진 시장의 55.51%를 차지하면서 시장을 견인하고 있으며, 2031년까지 연평균 복합 성장률(CAGR) 6.05%라는 가장 빠른 성장할 것으로 전망되고 있습니다. 중국에서는 암모니아 원료로부터 다운스트림에서의 농약에 이르는 통합된 밸류체인이 비용 우위성을 가져오고 인도에서는 의약품 산업의 확대가 고순도 수화물 수입을 촉진하고 있습니다. 안전상의 과제에도 불구하고 특수화학제품의 국내 생산에 대한 정부의 우대조치가 추가 생산능력 증강을 뒷받침하고 있습니다.

북미는 성숙하면서도 진화를 계속하는 시장입니다. 규제 준수에 의한 비용 상승이 발생하지만 방위 용도나 부식 방지 계약이 기본 히드라진 소비를 뒷받침하고 있습니다. 2024년 Calca Solutions에 대한 사모 펀드 인수는 안정적인 자유 현금 흐름과 차세대 고체 로켓 모터 계획을 통한 미래 수요 증가에 대한 투자자의 확신을 뒷받침합니다.

유럽은 REACH 승인의 압력이 높아지는 가운데 가장 엄격한 장벽에 직면하고 있습니다. 여러 중견 제조업체는 라이선싱 지연을 피하기 위해 생산 능력을 줄이거나 튀르키예 및 동유럽 계열사로 조달 전환을 진행하고 있습니다. 일반적으로 서로 다른 규제체제가 양극화된 히드라진 시장을 형성하고 있으며, 아시아태평양의 성장이 가속화되는 한편, 유럽은 통합이 진행되고 있으며, 북미는 리스크 관리와 전략적 필요성 사이에 균형을 맞추고 있습니다.

The Hydrazine Market was valued at 367.75 kilotons in 2025 and estimated to grow from 388.76 kilotons in 2026 to reach 513.16 kilotons by 2031, at a CAGR of 5.71% during the forecast period (2026-2031).

Demand resilience stems from hydrazine's irreplaceable role in agrochemicals, corrosion control, polymer foams, and emerging energy systems. Regulatory scrutiny in Europe and North America continues to tighten, yet capacity additions in Asia-Pacific offset potential volume losses elsewhere. Supply-side investments concentrate on safer production routes for hydrazine hydrate, while downstream users in pharmaceuticals and fuel-cell technology create fresh growth avenues. Competitive positioning focuses on vertical integration and long-term contracts to secure feedstock and manage compliance costs.

Escalating agricultural intensification in China, India, and Brazil keeps pesticide consumption high, and hydrazine remains the indispensable intermediate for maleic hydrazide, isoxazolidinone, and other growth-regulator actives. Large Chinese producers report dedicated capacities above 200,000 tons that feed both domestic and export pipelines, supporting supply security for formulating companies. Research into nano-engineered hydrazine derivatives achieves full pest mortality at lower dosage, signaling potential for reduced environmental loading while preserving efficacy. Regulatory focus on food security in these regions outweighs immediate environmental bans, thus sustaining the hydrazine market.

Hydrazine scaffolds enable the selective synthesis of anti-tubercular, anti-inflammatory, and antidepressant molecules, and recent process innovations deliver 89-97% yields under mild, solvent-efficient conditions. Clinical candidates such as pyrrole hydrazones inhibit Mycobacterium tuberculosis at therapeutic concentrations, widening demand among active pharmaceutical ingredient (API) manufacturers in the United States and India. To tackle toxicity concerns, producers are scaling indirect routes that avoid bulk hydrazine handling, yet still leverage its unique nucleophilic profile. As a result, the pharmaceutical segment is expected to remain the fastest-growing user base within the hydrazine market.

Hydrazine features on the European Chemicals Agency's Substances of Very High Concern list, triggering strict authorization and occupational exposure limits. Compliance now demands sealed transfer lines, scrubber systems, and continuous air monitoring, pushing operating costs higher for formulators across Germany, France, and the United States. Liability linked to liver toxicity and carcinogenicity also forces insurers to raise premiums, discouraging new entrants. Although Asia-Pacific regulations are comparatively lenient today, multinational customers increasingly require global compliance, slowly extending higher safety standards worldwide.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Hydrazine hydrate accounted for 60.17% of 2025 volume within the hydrazine market and recorded the segment-leading 5.89% CAGR outlook. Preference for aqueous grades stems from lower vapor pressure, simplified ISO-tank logistics, and smoother regulatory certification versus anhydrous material. Boiler-water treatment, polymer foaming, and API synthesis plants install dedicated hydrate storage to reduce on-site risk profiles, reinforcing demand stability. Specialty salts such as hydrazine sulfate serve electronics and analytical niches where tighter stoichiometric control is essential.

Regulators now explicitly recommend hydrate grades when feasible, catalyzing supplier investments in high-purity, low-metal formulations engineered for pharmaceutical compliance. Fuel-cell developers also gravitate toward monohydrate for liquid-carrier prototypes that balance power density with managed volatility, sustaining incremental offtake. Collectively, these trends entrench hydrazine hydrate's leadership and shield the segment from the full force of impending restrictions on anhydrous forms, supporting the broader hydrazine market.

The Hydrazine Report is Segmented by Type (Hydrazine Hydrate, Hydrazine Nitrate, Hydrazine Sulfate, and Other Types), Application (Corrosion Inhibitor, Explosives, Rocket Fuel, Medicinal Ingredient, and More), End-User Industry (Pharmaceuticals, Agrochemicals, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Asia-Pacific dominated the hydrazine market with a 55.51% hydrazine market share in 2025 and is forecast to post the fastest 6.05% CAGR through 2031. China's integrated value chain, from ammonia feedstock to downstream pesticides, confers cost leadership, while India's pharmaceutical build-out boosts high-purity hydrate imports. Government incentives for local specialty-chemical production stimulate further capacity additions despite safety headwinds.

North America remains a mature yet evolving arena. Regulatory compliance elevates operating costs, but defense applications and corrosion-control contracts sustain baseline hydrazine consumption. The 2024 private-equity acquisition of Calca Solutions underscores investor belief in steady free cash flow and future volume support from next-generation solid rocket motor programs.

Europe confronts the stiffest hurdles as REACH authorization pressures escalate. Several mid-tier formulators have trimmed capacity or shifted sourcing to affiliates in Turkey and Eastern Europe to circumvent licensing delays. Collectively, divergent regulatory regimes create a two-speed hydrazine market in which Asia-Pacific accelerates while Europe consolidates and North America balances between risk management and strategic necessity.