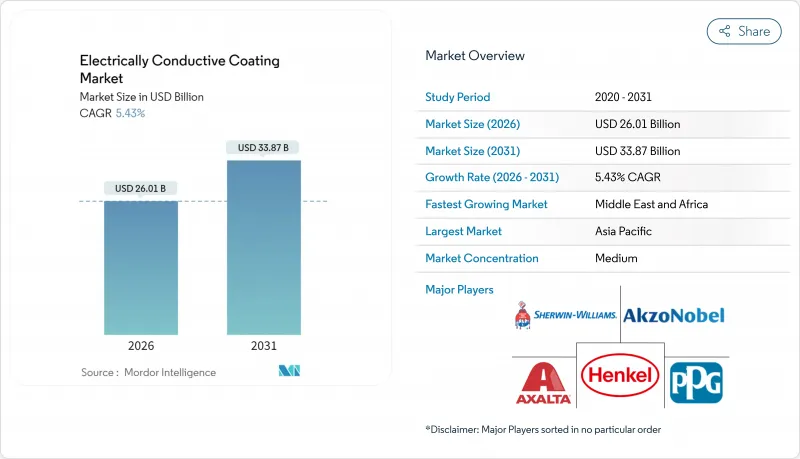

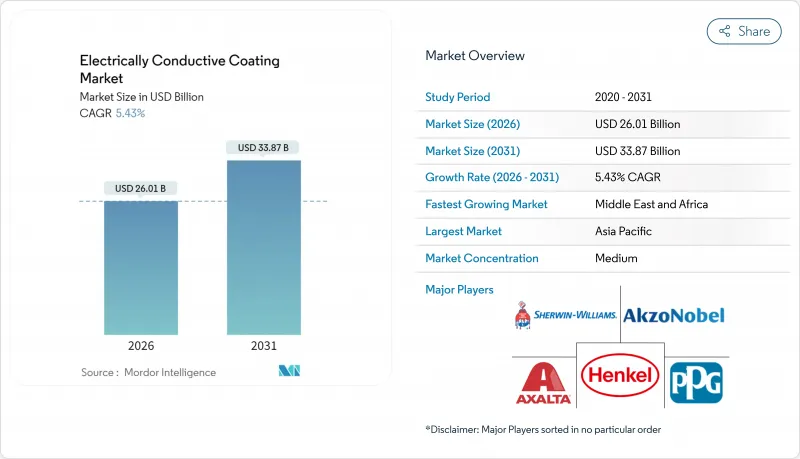

전도성 코팅 시장은 2025년 246억 7,000만 달러에서 2026년에는 260억 1,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 5.43%로 성장을 지속하여 2031년까지 338억 7,000만 달러에 달할 것으로 예측됩니다.

전도성 코팅 시장은 기존의 정전기 방지 용도에서 부가가치 용도인 전자기 방해(EMI) 차폐로 전환하고 있습니다. 이는 5G 인프라의 전개와 디바이스의 소형화를 뒷받침합니다. 은 충전 아크릴계는 여전히 주류 옵션이지만, 전도성 코팅 시장에서는 현재 전도성, 유연성 및 비용 균형이 우수한 구리계 및 폴리우레탄계 시스템이 선호되고 있습니다. 아시아태평양의 밀접한 전자부품 공급망은 조달 사이클을 단축하는 반면, 북미 및 유럽의 OEM 제조업체는 mm파 차폐, 열 안정성 및 REACH 규정 적합성을 갖춘 코팅에 프리미엄 가격을 지불합니다. 특수 소재 제조업체가 나노필러 분산 기술을 배터리 케이스에서 의료용 임플란트에 이르기까지 다양한 용도로 전개함에 따라 경쟁업체 간의 적대관계가 격화되고 있으며, 전도성 코팅 시장의 기회가 더욱 확대되고 있습니다.

반도체 제조 공장, 클린 룸, 첨단 자동차 조립 라인에서 정전기 방전 제어는 미션 크리티컬 요구사항으로 부피를 증가시키지 않고 표면 저항률을 유지하는 박막 정전기 방지층에 대한 지속적인 수요를 견인하고 있습니다. 탄소나노튜브 강화 아크릴 수지는 기존의 카본블랙 충전 시스템보다 우수한 내마모성을 나타내며, 고트래픽 생산 영역에서 유지보수 간격을 연장합니다. 자동차 부품 공급업체는 2024년에 개정된 IEC 61340 시험 프로토콜에 의한 합격 기준의 강화로 인해 기존에는 차폐 요건이 없었던 연료 모듈이나 HVAC 하우징에 코팅을 실시했습니다. 항공우주 및 의료기기 제조업체는 대륙 간 운송 중 고가치 전자기기의 보호를 위해 저배출 대전방지 필름을 지정하고 있으며 정전기 대책이 사후대응이 아니라 설계단계부터의 표준 요건이 되고 있습니다.

OEM 제조업체는 CAD 설계 단계에서 코팅을 제품 구조에 통합하여 전도성 코팅 시장을 조달 주도형에서 엔지니어링 주도형 구매 형태로 전환하고 있습니다. 플렉서블 폴리이미드 기판과 세라믹 복합재는 불균일한 형태에 사용되는 스프레이 코팅에 의존합니다. 통합 안테나를 갖춘 IoT 노드는 금속 캔보다는 박막 폴리머 필름을 선택하고 튜닝 불량을 방지하기 위해 공급업체는 예측 가능한 표면 임피던스를 보장해야 합니다. 공동 개발 계약은 프로토타입 단계에서 공정 엔지니어의 공동 배치를 규정하고 소재 전문 지식을 소비자용 전자기기의 로드맵에 통합합니다.

2024년 REACH 부속서 XVIII 협의에서는 삼산화 안티몬과 산화 카드뮴이 고도로 우려되는 물질로 지정되었으며, 배합 설계자는 Kg당 가격이 높음에도 불구하고 그래핀과 탄소나노튜브 시스템으로의 전환을 요구받고 있습니다. Tier 1 자동차 공급업체는 라이프사이클 평가를 활용하여 소재를 평가합니다. 특히 사용 종료 후 재활용 가능성에 따라 코팅재를 우선적으로 도입하고 있습니다. 의료 및 항공우주 분야의 구매자는 현재 납과 수은이 배합 공정에 유입되지 않도록 하는 공급업체의 보증을 요구하고 있으며, 금속 플레이크 충전에 의존하는 기존 라인에 대한 감사 부담이 증가하고 있습니다.

2025년 아크릴계 페인트는 전도성 코팅 시장에서 33.58%의 점유율을 차지했습니다. 이는 견조한 아시아 공급망과 지역 공기질 규정을 충족하는 수성 등급을 지원합니다. 폴리우레탄은 성장 엔진이며 전기자동차와 웨어러블 장비가 진동과 굴곡을 견딜 수 있는 탄성을 필요로 하기 때문에 5.95%의 연평균 복합 성장률(CAGR)로 확대되고 있습니다. 항공우주 분야에서는 200°C까지의 내열성을 보유한 고온 에폭시 수지가 계속 지정되고 있어 틈새 시장은 안정적이지만 규모 확대의 가능성은 희박합니다.

폴리에스테르계 수지는 저비용 소비자용 케이스에 사용됩니다. 실리콘 수지는 원자 산소에 노출되는 위성을 보호하고 불소 수지는 혈액 적합성이 요구되는 임베디드 리드를 보호합니다. ISO 9001 프로토콜은 공정의 재현성을 강조하고 코팅된 필름을 미터 단위로 검증하는 인라인 저항 스캐너가 개발되었습니다. 엔드 시장의 다양화로 인해 아크릴 수지는 영향을 적게 받지만, 플렉서블 디바이스로의 이행에 의해 폴리우레탄은 전도성 코팅 시장에서 미래 양산 리더 부문으로서의 지위를 확립하고 있습니다.

2025년 아시아태평양은 전도성 코팅 시장의 47.85%를 차지했습니다. 이는 중국의 가전 수출과 대만의 파운드리 복합 시설이 견인하고 있습니다. 지역 정부는 현지 공급망을 지원하고 물류 리드 타임을 수일로 단축하고 있습니다. 한국의 메모리 공장에서는 인라인 스퍼터링 대응 코팅이 도입되고, 일본에서는 고급 하이브리드차용으로 제로 VOC 배합 기술이 성숙하고 있습니다. 북미는 방위 주요 기업이 레이더 항공 전자기기를 차폐하는 코팅을 요구하기 때문에 큰 점유율을 차지합니다. 유럽은 미래의 REACH 개정에 대응하기 위해 무첨가 화학 기술을 추진하여 그린 배합의 거점으로서의 지위를 확립하고 있습니다.

중동 및 아프리카는 CAGR 5.75%로 확대될 것으로 전망되고 있습니다. 아랍에미리트(UAE)의 자유무역지역 우대책이 전자기기 수탁제조업체를 유치하고 있는 것이 그 배경입니다. 사우디아라비아는 '비전 2030' 산업단지에 전도성 코팅공장을 집중하여 수입 의존도의 감소를 도모하고 있습니다. 남미에서는 자동차 대기업이 위험 분산을 위해 아시아 외부로 생산 거점을 분산시키는 움직임에 따라 지역별 자동차 전자기기 생산 라인이 형성되어 국소적인 수요가 탄생하고 있습니다.

The Electrically Conductive Coating market is expected to grow from USD 24.67 billion in 2025 to USD 26.01 billion in 2026 and is forecast to reach USD 33.87 billion by 2031 at 5.43% CAGR over 2026-2031.

The electrically conductive coating market is shifting from legacy anti-static roles to value-added electromagnetic interference (EMI) shielding, supporting 5G infrastructure rollouts and device miniaturization. Silver-filled acrylics remain the mainstream choice; however, the electrically conductive coating market now favors copper-based and polyurethane systems that strike a balance between conductivity, flexibility, and cost. Asia-Pacific's dense electronics supply chains keep procurement cycles short, while North American and European original equipment manufacturers (OEMs) pay premiums for coatings that deliver millimeter-wave shielding, thermal stability, and REACH compliance. Competitive rivalry intensifies as specialty materials firms bring nano-filler dispersion know-how to applications ranging from battery enclosures to medical implants, further widening the electrically conductive coating market opportunity.

Electrostatic discharge control has become mission-critical in semiconductor fabs, cleanrooms, and advanced vehicle assembly lines, driving sustained demand for thin anti-static layers that maintain surface resistivity without adding bulk. Carbon-nanotube-reinforced acrylics exhibit greater abrasion resistance than traditional carbon-black-filled systems, thereby extending maintenance intervals in high-traffic production zones. Automotive suppliers are now coating fuel modules and HVAC housings that previously had no shielding requirements, in response to a 2024 update of IEC 61340 test protocols that tightened pass-fail margins. Aerospace and medical device OEMs specify low-outgassing anti-static films to protect high-value electronics during transcontinental shipment, effectively making static control a default design parameter rather than a last-minute fix.

OEMs embed coatings into product architecture at the CAD stage, turning the electrically conductive coating market into an engineering-driven rather than procurement-driven purchase. Flexible polyimide boards and ceramic composites rely on spray-applied coatings that stretch with odd-shaped enclosures. IoT nodes with integrated antennas opt for thin polymeric films over metal cans to prevent detuning, prompting suppliers to ensure predictable surface impedance. Joint-development agreements now stipulate co-location of process engineers during pre-production, embedding material expertise inside consumer-electronics roadmaps.

REACH Annex XVIII consultations in 2024 flagged antimony trioxide and cadmium oxide as substances of very high concern, compelling formulators to pivot to graphene and carbon nanotube systems, despite higher per-kilogram prices. Automotive tier-1 suppliers utilize life-cycle assessments to evaluate materials, prioritizing coatings based on their recyclability at the end of life. Medical and aerospace buyers now request supplier declarations that no lead or mercury enters the formulation pipeline, adding audit overhead for legacy lines that still rely on metal-flake loading.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Acrylics held a 33.58% share of the electrically conductive coating market in 2025, underpinned by robust Asian supply chains and waterborne grades that meet regional air-quality mandates. Polyurethanes are the growth engine, expanding at a 5.95% CAGR as electric vehicles and wearables rely on their elasticity to survive vibration and flexing. Aerospace continues to specify high-temperature epoxies rated to 200 °C, a niche that holds steady but rarely scales.

Polyester chemistries provide low-cost consumer cases. Silicones protect satellites exposed to atomic oxygen, while fluoropolymers cover implantable leads that require hemocompatibility. ISO 9001 protocols have emphasized process repeatability, resulting in inline resistivity scanners that validate every meter of coated film. End-market diversification insulates acrylics, yet the shift to flexible devices positions polyurethanes as the future volume leader within the electrically conductive coating market.

The Electrically Conductive Coating Market Report is Segmented by Type (Acrylics, Epoxy, Polyesters, Polyurethanes, and Other Types), Conductive Filler Material (Copper, Aluminum, Silver, and Other Material Types), Application (Electronics and Electrical, Automotive, Aerospace and Defense, and Other Applications), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific commanded 47.85% of the electrically conductive coating market in 2025, anchored by China's consumer-electronics exports and Taiwan's foundry complexes. Regional governments subsidize local supply chains, cutting logistics lead times to days. South Korea's memory fabs embrace in-line sputterable coatings, while Japan refines zero-VOC recipes for high-end hybrid vehicles. North America holds a significant share, where defense primes insist on coatings that shield radar avionics. Europe advances additive-free chemistries to comply with future REACH amendments, positioning itself as the hub for green formulations.

The Middle-East and Africa are projected to grow at a 5.75% CAGR, driven by the United Arab Emirates' free-zone incentives that attract contract electronics manufacturers. Saudi Arabia bundles conductive-coating plants into Vision 2030 industrial parks, thereby reducing its dependence on imports. South America sees localized automotive electronics lines as auto majors diversify beyond Asia for risk mitigation, creating pockets of regional demand.