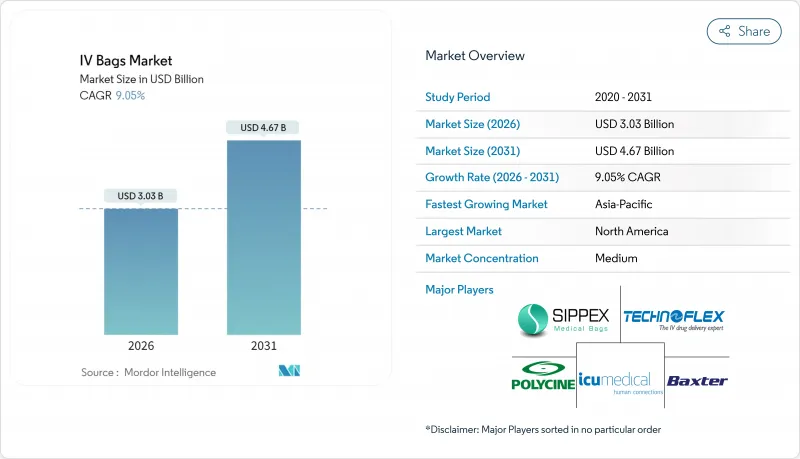

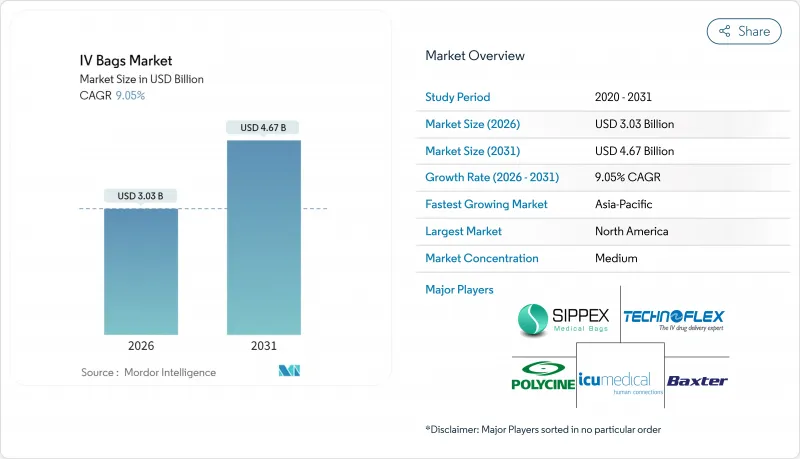

IV백 시장은 2025년 27억 8,000만 달러에서 2026년에는 30억 3,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 9.05%로 성장을 지속하여 2031년까지 46억 7,000만 달러에 달할 것으로 예측되고 있습니다.

수요는 만성 질환의 유병률, DEHP 미함유 제제로의 규제 추진, 재택 점적 인프라의 확대에 의해 발생하고 있습니다. 병원은 여전히 구매의 대부분을 차지하고 있지만, 가치 기반 의료로 인해 정맥내 치료는 외래 및 재택 의료 환경으로 이동하고 있습니다. 캘리포니아의 DEHP 금지 조치는 비PVC 재료의 세계적인 채택을 가속화했습니다. 반면에 최근 허리케인으로 인한 공급 부족 현상은 공급망 중복성의 필요성을 부각시켰습니다. 북미가 가장 큰 수익 기반을 유지하는 반면, 아시아태평양에서는 정부의 임상 능력 근대화와 의료 관광 수요 회복과 함께 수량 기준으로 가장 빠른 성장이 예상됩니다.

고령화와 당뇨병, 암, 심혈관질환의 급증으로 입원기간이 장기화되어 정맥내 약제의 사용이 증가하고 있습니다. 경구 생체이용률이 낮은 약물은 지속 주입에 의존하는 경우가 많으며, 따라서 1회당 백 소비량이 증가합니다. 암 치료와 투석은 또한 수액량을 증가시킵니다. 가치 기반 환급 제도는 단가가 아닌 치료 결과의 질을 강조하기 때문에 임상의는 치료 효과를 최적화하는 정밀 정맥내 제형을 선호합니다.

팬데믹 후 감염 관리 프로토콜은 일회용 의료기기를 선택에서 표준으로 격상시켰습니다. 일회용 백은 구입 가격이 높음에도 불구하고 멸균 작업이 필요 없으며 교차 오염의 위험을 줄이고 약물 작용 효율을 높입니다. 병원과 외래 진료센터는 현재 라이프사이클 비용 전체를 산정하고 있으며, 고품질의 즉시 사용가능한 솔루션의 도입이 강화되고 있습니다.

PVC, EVA, 폴리프로필렌 수지는 원유 가격 변동에 연동합니다. 공급원의 다양성이 제한되어 있기 때문에 지정학적 충격 시 가격변동폭이 확대됩니다. 장기 계약에 의한 헤지가 곤란한 중소 제조업체는 추가 비용을 전가하고 이는 입찰을 지연시켜 프리미엄 비PVC제 백의 도입을 억제하고 있습니다.

비PVC 제제는 2025년 수익의 46.25%를 차지하였으며 2031년까지 연평균 복합 성장률(CAGR)10.55%로 추이할 것으로 예측됩니다. EVA의 화학적 불활성 특성은 항암제에 이상적이며 폴리올레핀은 장 영양제의 증기 멸균 안정성을 제공합니다. 비PVC 제품 라인으로 인한 IV백 시장의 규모는 가소제 함유 PVC로부터의 전환을 반영하며 2031년까지 23억 6,000만 달러에 이를 것으로 추정됩니다. 캘리포니아 주와 매사추세츠 주에서는 이미 DEHP 미함유 조달을 의무화하고 있으며, 아프리카의 기증자 자금을 통한 녹색 입찰은 보다 광범위한 세계적 수용을 시사하고 있습니다.

PVC는 가격에 민감한 분야에서 여전히 뿌리 깊은 수요가 있지만, 폐기물 처리세와 탄소 회계를 고려할 때 총 비용 우위가 떨어집니다. 2027년 이후의 금형 갱신 사이클은 컨버터가 EVA나 PP에 대응한 미래를 위해 금형에 재투자하는 자연스러운 전환점이 될 것입니다. 이 소재의 조합 변경은 전환 장벽을 높이고 선구자의 이익 확대로 이어집니다.

500-1,000ml 크기의 백은 표준 수술에서의 수분 공급 요구를 충족시켜 2025년 36.45%의 점유율을 차지했습니다. 1,000ml 초과 용기는 지속적인 소생을 필요로 하는 장기 이식이나 외상 수술의 장기화를 배경으로, CAGR 11.05%의 성장할 것으로 전망됩니다. 대용량 IV백의 시장 점유율은 2031년까지 25.30%에 달할 가능성이 있으며, 테르모의 경량 설계 'TERUPACK Eco'가 수지 사용량을 23% 낮춰 수송 시의 배출량과 폐기물 처리비를 저감하는 점이 성장을 뒷받침합니다.

0-250ml의 소용량 백은 소아과 및 틈새 생물학적 제제용입니다. 수량 기준으로는 수익을 상회하지만, 안전 기술을 통합한 신흥 폐쇄형 커넥터가 이익률을 높일 전망입니다. 전체 용량에서 RFID 태그는 유효기간 관리를 가속화하고 약물 폐기량을 줄이기 때문에 병원 조달 부문의 디지털 표시는 암시적 입찰 요구사항입니다.

본 IV백 보고서는 소재별(PVC, 비PVC), 용량별(0-250ml, 250-500ml, 500-1,000ml, 1,000ml 초과), 포트 유형별(싱글 포트, 듀얼 포트), 수액 유형별(정질액, 교질액, 혈액 및 혈액제제), 최종 사용자별(병원, 진료소, 재택 의료, 외래수술센터, 기타), 지역별(북미, 유럽, 아시아태평양 등)으로 분류됩니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

북미는 2025년 수익의 41.80%를 차지하였으며 이는 11억 6,000만 달러에 해당합니다. 연방 정부의 장려책이 국내 멸균액 생산을 촉진하는 한편, 캘리포니아주의 DEHP 금지령에 의해 EVA로의 전환이 가속하고 있습니다. 미국의 IV백 시장의 규모는 2031년까지 21억 8,000만 달러에 달할 것으로 예측됩니다. 최근 허리케인에 의한 공급 부족으로 의회는 예비 생산 라인에 세액 공제를 제안하고 있으며, 지리적 다양화가 조달 기준이 되고 있습니다.

유럽에서는 매출 증가가 완만하지만 제품의 고도화가 현저합니다. 독일과 프랑스에서는 이미 비PVC 도입률이 60%를 넘어섰으며, 영국에서는 폐쇄형 폴리올레핀 리사이클 방식의 시험 운용에 의해 의료용 플라스틱 배출량이 28% 감소하였으며 2027년까지 전국적인 도입이 예정되어 있습니다. 의료기기규칙(MDR)에 대한 대응 비용이 진입장벽을 높여 규제 대응 자원을 보유한 기존 기업을 보호하고 있습니다.

아시아태평양은 11.45%라는 가장 높은 CAGR을 달성했습니다. 중국의 지속적인 병원 건설과 인도의 외과 수술 건수 증가가 단위 수요를 뒷받침하고 있지만 가격면에서 여전히 PVC로 기울어져 있습니다. 호주 정부는 박스터사의 시드니 서부 공장 확장에 2,000만 호주 달러(1,320만 달러)를 제공했으며 이는 자급률 강화와 지역산업정책의 전환을 시사하고 있습니다. 태국 등의 의료 관광 거점에서는 서구 수준의 안전성을 요구하는 환자의 요구에 부응하여 듀얼 포트 EVA 시스템으로의 갱신이 진행되고 있습니다.

남미와 중동 및 아프리카는 각각 매출액의 12% 미만을 차지하지만 두 자릿수의 성장이 예상되는 지역이 존재합니다. 브라질의 민간 병원 체인에서는 일회용 프로토콜의 표준화가 진행되어 걸프 국가에서는 도로 인프라 확충에 수반하는 외상 센터용으로 대량의 비경구 제제를 조달하고 있습니다.

The IV bags market is expected to grow from USD 2.78 billion in 2025 to USD 3.03 billion in 2026 and is forecast to reach USD 4.67 billion by 2031 at 9.05% CAGR over 2026-2031.

Demand stems from chronic-disease prevalence, the regulatory push toward DEHP-free formulations, and expanding home-infusion infrastructure. Hospitals still account for the bulk of purchases, yet value-based care is re-routing intravenous therapy toward outpatient and residential settings. California's DEHP ban has accelerated global adoption of non-PVC materials, while recent hurricane-related shortages exposed the need for supply-chain redundancy. North America retains the largest revenue pool, but Asia-Pacific delivers the fastest unit growth as governments modernize clinical capacity and medical-tourism flows rebound.

An aging population and surging incidence of diabetes, cancer, and cardiovascular disorders lengthen hospital stays and intensify intravenous drug use. Medications with poor oral bio-availability often rely on continuous infusion, raising per-episode bag consumption. Oncology regimens and dialysis further amplify fluid volumes. Because value-based reimbursement centers on outcome quality rather than unit cost, clinicians prefer precise IV formulations that optimize therapeutic efficacy.

Post-pandemic infection-control protocols elevated disposable devices from tactical choice to strategic standard. Single-use bags eliminate sterilization labor, cut cross-contamination liability, and streamline pharmacy workflows despite higher purchase prices. Hospitals and outpatient centers now calculate total life-cycle costs, reinforcing premium, ready-to-administer solutions.

PVC, EVA, and polypropylene resins track crude-oil swings. Limited supplier diversity inflates price amplitude during geopolitical shocks. Smaller manufacturers unable to hedge long-term contracts pass surcharges on, delaying tenders and tempering adoption of premium non-PVC bags.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Non-PVC formulations captured 46.25% of 2025 revenue and are forecast to log a 10.55% CAGR through 2031. EVA's chemical inertness makes it ideal for oncology drugs, while polyolefins offer steam-sterilization stability for parenteral nutrition. The IV bags market size attributable to non-PVC lines is estimated at USD 2.36 billion by 2031, reflecting the shift away from plasticizer-laden PVC. California and Massachusetts have already mandated DEHP-free procurement, and donor-funded green tenders in Africa signal broader global catch-up.

PVC remains entrenched in price-sensitive segments, yet its total-cost advantage erodes once disposal levies and carbon accounting enter the calculus. Mold-replacement cycles after 2027 provide a natural pivot point at which converters are likely to reinvest in future-proof tooling compatible with EVA or PP. This material re-mix raises switching barriers and enlarges profit pools for first movers.

Bags sized 500-1,000 ml held 36.45% share in 2025 as they meet standard peri-operative hydration needs. Containers exceeding 1,000 ml are projected to clock an 11.05% CAGR, fueled by longer organ-transplant and trauma procedures requiring continuous resuscitation. The IV bags market share for large-volume formats could crest 25.30% by 2031, aided by Terumo's lightweight TERUPACK Eco design that trims resin use 23%, lowering freight emissions and waste charges.

Micro-volume 0-250 ml bags service pediatrics and niche biologics. Their unit volumes outpace revenue, but emerging closed-system connectors promise margin uplift by bundling safety technology. Across all capacities, RFID tagging expedites expiry tracking and reduces pharmacy spoilage, making digital labeling an implicit tender requirement for hospital procurement teams.

The IV Bags Report is Segmented by Material (PVC, Non-PVC), Capacity (0-250 Ml, 250-500 Ml, 500-1, 000 Ml, >1, 000 Ml), Port Type (Single Port, Dual Port), Fluid Type (Crystalloids, Colloids, Blood & Blood Products), End User (Hospitals, Clinics, Home Care, Ambulatory Surgical Centers, Others), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America held 41.80% of 2025 revenue, equating to USD 1.16 billion. Federal incentives promote domestic sterile-fluid output, while California's DEHP ban cements material migration toward EVA. The IV bags market size for the United States is forecast to touch USD 2.18 billion by 2031. Recent hurricane-sparked shortages led Congress to propose tax credits for redundant manufacturing lines, making geographic diversification a procurement criterion.

Europe displays slower topline expansion yet sharper product sophistication. Germany and France already report non-PVC adoption above 60%, and the United Kingdom trialed a closed-loop polyolefin recycling scheme that cut clinical-plastic emissions 28%, with national rollout slated by 2027. MDR compliance costs escalate entry barriers, protecting incumbents endowed with regulatory bandwidth.

Asia-Pacific delivers the fastest 11.45% CAGR. China's ongoing hospital build-out and India's expanding surgical volumes underpin unit demand, albeit still skewed toward PVC on price grounds. Australia committed AUD 20 million (USD 13.2 million) to scale Baxter's Western Sydney plant, bolstering self-reliance and signalling broader regional industrial policy shifts. Medical-tourism hubs like Thailand upgrade to dual-port EVA systems, aligning with visiting-patient expectations for Western-grade safety.

South America and the Middle East & Africa each contribute under 12% of revenue but promise pockets of double-digit growth. Brazil's private hospital chains are standardizing single-use protocols, while Gulf states procure large-volume parenterals for trauma centers aligned with expanding road-infrastructure.