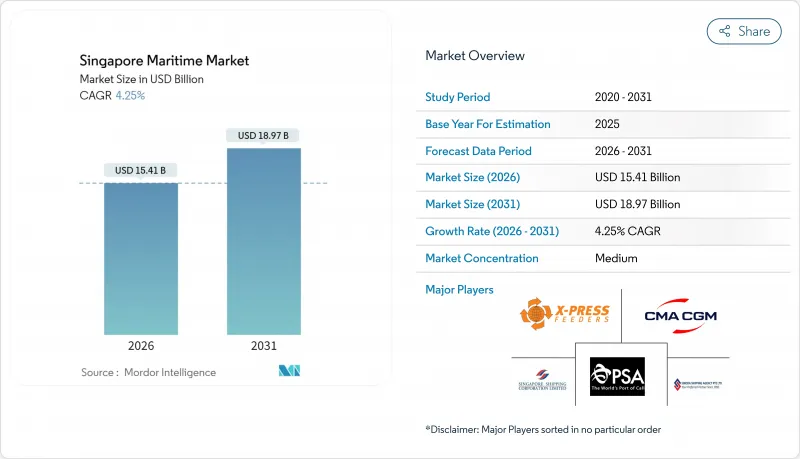

싱가포르의 해사 시장의 규모는 2026년 154억 1,000만 달러로 추정됩니다.

이는 2025년 147억 8,000만 달러에서 성장하여, 2031년에는 189억 7,000만 달러에 이를 것으로 예측됩니다. 2026년부터 2031년까지는 CAGR 4.25%로 성장할 전망입니다.

투아스 항구의 자동화 가속화, 전자 연료 공급 증명서(EBDN)의 의무화, 녹색 연료 회랑의 확대가 싱가포르의 해사 시장의 성장을 뒷받침하고 있습니다. 한편, EU 배출량 거래 제도(EU-ETS)의 추가 요금이 정기선의 이익률을 압박하는 상황이 계속되고 있습니다. 2024년 컨테이너 취급량은 역대 최고인 4,112만 TEU를 기록했으며, 홍해 항로 우회로 인한 혼란에도 불구하고 싱가포르가 중계 거점으로서의 강인성을 가지고 있음을 보여주었습니다. 2024년 연료유 취급량은 5,492만 톤에 이르렀으며, 싱가포르가 세계 최대의 연료 공급 거점임을 재확인함과 동시에 LNG, 메탄올, 암모니아의 시험 운용이 급속히 확대되고 있습니다. 2025년 중반에 도입된 해사 5G 네트워크는 선박 교통의 실시간 조정을 실현하고 X-Press Feeders사의 21.8%에 이르는 선대 확대는 유연성이 있는 운항자가 스케줄 신뢰성에 의한 프리미엄을 획득하는 방법을 나타냅니다.

2만 TEU를 넘는 초대형 컨테이너선이 주차로 싱가포르에 기항하는 빈도가 증가해, 화물이 소수의 항만 로테이션에 집중되고 있으며 이로 인해 버스 지연 페널티가 현저해집니다. 2024년의 취급량은 4,112만 TEU에 달하였고, 그 중 약 85%가 환적화물이었습니다. 홍해 우회항로의 영향으로 아시아-유럽항로의 스케줄은 최대 2주간 지연되었고 90%의 항공편이 예정 밖으로 운행되어 잉여화물이 싱가포르로 유입되었습니다. 기존 터미널에서는 야드 밀도가 급증하여 압박 상태를 초래했기 때문에 해사 항만청(MPA)은 디지털 PORT@SG에 의한 예측 분석을 이용한 버스 할당을 도입했지만, 완전한 효과 발현에는 전체 항만의 실시간 데이터 연계가 필수적입니다.

투아스 항구는 2040년대까지 연간 6,500만 TEU의 처리 능력을 목표로 하고 있으며 기존 4개의 터미널을 통합한 거대 시설을 정비할 예정입니다. 이 시설에서는 무인 운송 차량(AGV), 원격 조작식 부두 크레인, 디지털 트윈 플랫폼 "iWX"를 도입합니다. 1단계는 가동 중이며 PSA는 2024년 10월 세관 사전 통관과 창고 로봇을 통합한 200만 평방 피트의 자동화 공급망 허브 착공에 들어갔습니다. 200억 싱가포르 달러 규모의 투자는 인건비 절감을 보장하지만, 지역 경쟁자가 저비용 반자동화 터미널을 전개하는 가운데 기술 진부화의 위험이 수반됩니다.

후티 반군의 공격에 의해 아시아-유럽 항로는 희망봉을 돌아가게 되었으며 항해 기간이 최대 14일 연장되어 유효 선대 용량의 약 15%가 감소했습니다. 스케줄 신뢰성은 10%까지 급락했고, 싱가포르의 기존 터미널에서는 야드 밀도가 급증했습니다. 디지털 포트 @SG는 버스를 동적으로 재분배하지만, 운영은 정확한 도착 예측에 의존하고 있으며, 지정학적 혼란 시에는 예측하기 어려운 상황이 계속되고 있습니다.

항만 및 터미널 운영은 4,112만 TEU의 취급량과 PSA 인터내셔널의 규모를 배경으로 2025년 총수익의 40.78%를 차지했습니다. 연료 공급 서비스는 규모가 작지만, 전자 연료 공급 증명서 규정과 대체 연료 수요의 급증에 의해 전 사업 중 가장 높은 CAGR 4.62%가 예상됩니다. 싱가포르의 해사 시장 내 연료 공급 부문의 규모는 정기선 및 유조선 선대에서의 LNG, 메탄올, 암모니아 채택 확대에 따라 꾸준히 확대될 것으로 전망됩니다. 해운회사 서비스는 아시아-유럽 항로의 화물 우회로 원동력을 받는 한편 EU 배출량거래제도(EU-ETS)의 비용 전가 부담을 안고 있습니다. 조선, 수리 및 보수 분야는 드라이독 능력을 통합해 환경 업그레이드 프로젝트에 대한 체제를 정비한 Seatrium의 설립 후 가속하고 있습니다. 해양 지원 서비스는 사업자가 CII 평가 및 탄소 크레딧 조달에 임하는 가운데 컴플라이언스 조언 수요에 의해 지원됩니다.

자동 버스 할당과 Maritime-5G는 터미널 업무의 생산성을 더욱 향상시킵니다. 반면에 분산된 항만 작업선 부문은 전동화 목표 달성을 방해하고 항만 수역에서 단기 배출 감소 효과를 제한합니다. Seatrium사가 암모니아 대응 개조에 주력하는 자세는 싱가포르 국내에 그린 연료의 풀 사이클 인프라를 구축한다는 투아스 항만의 전략과 합치하고 있습니다. 금융 및 법무 자문기업은 싱가포르의 보통법 프레임워크를 활용해 그린 이행 대출을 조성하여 싱가포르의 해사 시장에서 전문 서비스 수익의 확대에 공헌하고 있습니다.

싱가포르의 해사 시장의 보고서는 활동별(항만 및 터미널 운영, 해운회사 서비스, 연료 보급 서비스 등), 선박 유형별(컨테이너선, 벌크선, 유조선, 여객선, 기타), 최종 사용자 산업별(전자기기 및 반도체, 화학제품 및 석유화학제품, 식품 및 음료 등)로 세분화되어 있습니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

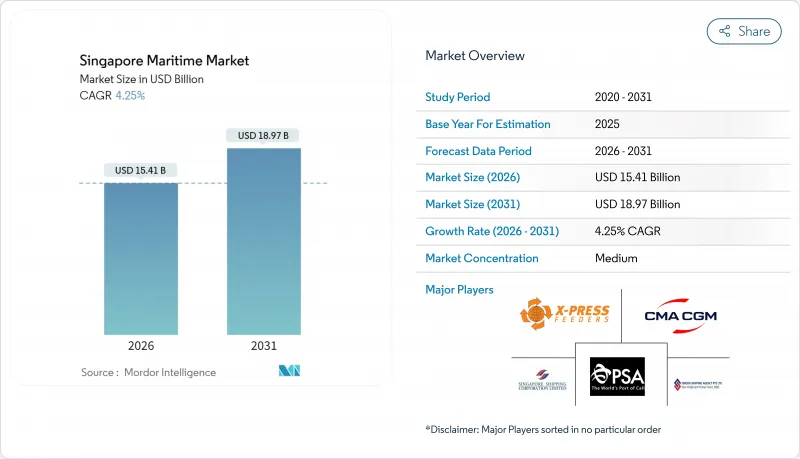

The Maritime Sector In Singapore Market size in 2026 is estimated at USD 15.41 billion, growing from 2025 value of USD 14.78 billion with 2031 projections showing USD 18.97 billion, growing at 4.25% CAGR over 2026-2031.

Accelerated automation at Tuas Port, the electronic bunker-delivery-note mandate, and expanding green-fuel corridors underpin the Maritime Sector in Singapore market's momentum, even as EU Emissions Trading System (EU-ETS) surcharges compress liner margins. Container throughput hit a record 41.12 million TEU in 2024, highlighting the city-state's resilience as a trans-shipment nexus despite Red Sea rerouting disruptions. Bunker volumes of 54.92 million tonnes in 2024 reaffirm Singapore's role as the world's largest bunkering hub, with LNG, methanol, and ammonia trials scaling quickly. Maritime-5G coverage due in mid-2025 promises real-time vessel-traffic coordination, while X-Press Feeders' 21.8% fleet expansion shows how agile operators capture schedule-reliability premiums.

Ultra-large container vessels exceeding 20,000 TEU now call weekly at Singapore in greater numbers, concentrating cargo into fewer port rotations and magnifying berth-delay penalties. Throughput reached 41.12 million TEU in 2024, about 85% of which was transshipment cargo. Red Sea diversions added up to two weeks on Asia-Europe schedules, pushing 90% of sailings off timetable and funneling overflow to Singapore.Legacy terminals strained under yard-density spikes, prompting the Maritime and Port Authority (MPA) to deploy predictive-analytics berth allocation via digitalPORT@SG, although full effectiveness depends on universal real-time data feeds.

Tuas Port targets 65 million TEU annual capacity by the 2040s, consolidating four legacy terminals into a mega-facility featuring automated guided vehicles, remote-controlled quay cranes, and the iWX digital-twin platform. Phase 1 is operational, and PSA broke ground in October 2024 on a 2 million-sq-ft automated supply-chain hub that integrates customs pre-clearance and warehouse robotics. The SGD 20 billion investment promises labor-cost savings but carries technology-obsolescence risk as regional rivals roll out lower-cost semi-automated terminals.

Houthi attacks forced Asia-Europe services around the Cape of Good Hope, adding up to 14 days per voyage and removing roughly 15% of effective fleet capacity. Schedule reliability plunged to 10%, driving yard-density surges at legacy Singapore terminals. While digitalPORT@SG reallocates berths dynamically, it depends on accurate arrival forecasts that remain elusive during geopolitical disruptions.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Port and Terminal Operations contributed 40.78% to overall 2025 revenue, benefiting from 41.12 million TEU throughput and PSA International's scale. Bunkering Services, although smaller, are set for 4.62% CAGR, the quickest among activities, thanks to the electronic bunker-delivery-note rule and surging alternative-fuel demand. The Maritime Sector in Singapore market size for bunkering is expected to widen steadily as LNG, methanol, and ammonia adoption rises across liner and tanker fleets. Shipping Line Services capture upside from diverted Asia-Europe volumes but bear EU-ETS pass-through costs. Shipbuilding, Repair, and Maintenance accelerate after Seatrium's creation, which consolidated dry-dock capacity and positioned the yard for green-retrofit projects. Maritime Support Services thrive on compliance advisory demand as operators navigate CII ratings and carbon-credit procurement.

Automated berth allocation and Maritime-5G will further lift productivity for terminal activities. Conversely, the fragmented harbour-craft segment drags on electrification targets, limiting near-term emissions gains in port waters. Seatrium's focus on ammonia-ready conversions aligns with Tuas Port's strategy of anchoring full-cycle green-fuel infrastructure within Singapore. Financing and legal advisory firms leverage Singapore's common-law framework to structure green-transition loans, drawing additional professional-services revenue into the Maritime Sector in Singapore market.

The Maritime Sector in Singapore Report is Segmented by Activity (Port and Terminal Operations, Shipping Line Services, Bunkering Services, and More), Vessel Type (Container Vessels, Bulk Carriers, Tankers, Passenger Vessels, Others), End User Industry (Electronics and Semiconductors, Chemicals and Petrochemicals, Food and Beverage, and More). The Market Forecasts are Provided in Terms of Value (USD).