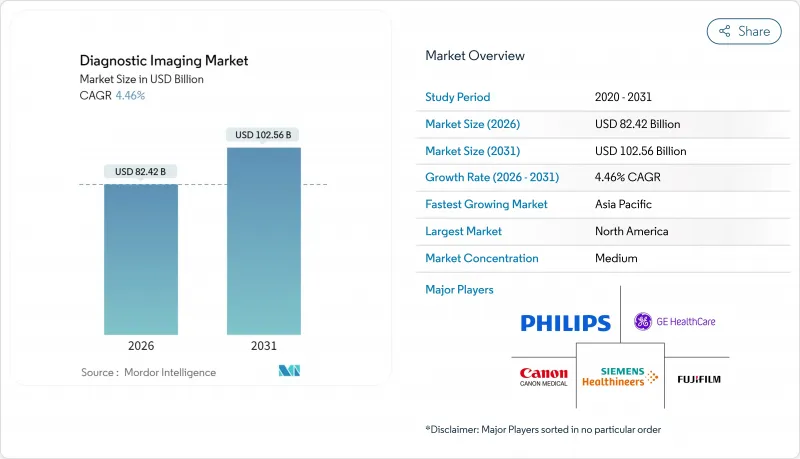

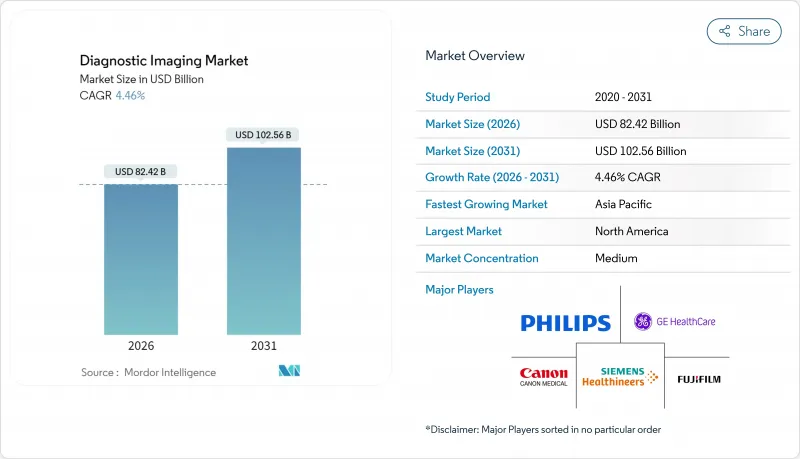

2026년 의료 영상 시장 규모는 824억 2,000만 달러로 추정되며, 2025년 789억 달러에서 성장한 수치입니다.

2031년까지 1,025억 6,000만 달러에 이르고, 2026년부터 2031년에 걸쳐 CAGR 4.46%로 확대될 전망입니다.

북미는 설치 기반이 촘촘하고 자본 예산에 의해 최대의 수익원으로 계속되고 있지만, 아시아태평양은 정부에 의한 병원 설비에의 자금 투입과, 국내 제조업체가 가격 경쟁력이 있는 시스템을 확대해 액세스를 확충하고 있는 것으로부터, 가장 강한 성장세를 보이고 있습니다. X선 검사는 구급의료나 정형외과 분야에서의 높은 빈도 이용 사례의 기반으로 계속되고 있지만, 고속 스캐너와 AI 지원에 의한 검출 및 트리어지의 제휴가 진행됨으로써, 컴퓨터 단층 촬영(CT)의 이용이 확대되고 있습니다. 병원은 여전히 주도적 입장에 있으며, 고가격대 시스템의 도입 자금을 확보할 수 있는 것 외에 화상 진단과 처치 서비스를 연계시킬 수 있습니다. 그러나 보험자 측이 서비스 제공 장소를 저비용 환경으로 유도하는 움직임에 따라 외래 영상 진단센터의 점유율이 확대되고 있습니다. 경쟁 환경은 다국적 대기업에 의한 과점 상태를 반영하고 있지만, 중국 기업의 진입에 의한 가격 압력이나 모바일 핸드헬드 소프트웨어 대응 워크플로우 등의 새로운 수요 영역의 출현에 의해 의료 영상 시장 전체의 유닛 경제성이 변화하고 있습니다.

만성 질환 부담은 의료 영상 시장의 지속적인 수요를 지원합니다. 심혈관 질환, 암, 당뇨병의 진단, 병기 분류, 치료 경과의 장기 모니터링에는 케어의 지속적인 과정에서 영상 진단이 필수적이기 때문입니다. 고령화와 생활습관의 변화에 의해 많은 중소득국에서 암 발생률이 상승하고 있으며, 이 동향은 표준화된 종양학 진료 경로에서의 CT 및 PET 검사 건수 증가로 이어지고 있습니다. 심장 CT 및 로드 MRI는 관상동맥 질환 위험 계층화를 위한 가이드라인 준수 관리에 통합되어 있으며, 특히 2형 당뇨병을 가진 성인의 경우 침습 진단을 대체하는 비침습 영상을 중시하는 모니터링 프로토콜이 현재 채택되고 있습니다. 노인층에서 만성 신장병의 유병률 확대는 가돌리늄 노출을 피하는 비조영 MRI 및 고급 시퀀싱의 역할을 확대하여 의료 영상화 시장에서 확산 강조 영상(DWI) 및 동맥 스핀 라벨링(ASL) 프로토콜의 소프트웨어 도입을 가속화하고 있습니다. 보험 상환 정책은 중요한 조정 수단으로 작용합니다. 메디케어의 고급 진단 영상에 대한 적정사용기준(AUC)은 임상적응과 검사방법의 선택을 정합시키고 정당한 이용기록을 작성하는 의사결정 지원 시스템의 통합을 의무화하고 있기 때문입니다.

가치 기반 계약으로 전환함으로써 의료 시스템은 다운스트림 비용을 피하기 위해 질병의 조기 발견을 추진하고 있으며, 이는 스크리닝 및 진단 검사에서 고수익 영상 진단의 역할을 확대하고 있습니다. 폐암 검진에 있어서의 저선량 CT는 미국 예방 의료 작업부회(USPSTF)로부터 그레이드 B의 추천을 받고 있어, 지역 의료 현장에서의 프로그램 성숙에 수반해 보험 적용 결정이 검사 건수 증가에 기여했습니다. 지방 수준의 치밀 유방 관련 법규 및 연방 정부의 밀도 보고 규칙은 고르지 않은 치밀 조직을 가진 여성에 대한 보조 초음파 검사 및 MRI 적용 경로를 확대하고 의료 영상 시장에서 자동 유방 초음파 장치 및 고처리량 MRI 장치에 대한 수요를 이끌고 있습니다. 뇌내 출혈과 폐색전증의 의심을 몇 분 이내에 식별하는 AI 강화 트리아지는 응급 부문의 우선순위화를 개선하고, 특히 지연이 치료 결과에 직결되는 뇌졸중 경로에서 보다 신속한 개입을 지원합니다. 컴플라이언스 고려 사항은 FDA 허가 취득을 위해 다양한 데이터 세트에서 의료기기로서 소프트웨어의 견고한 검증이 필요하며, 이는 의료 영상 시장의 제품 출시 빈도 및 현장 성능에 영향을 미칩니다.

프리미엄 MRI 및 하이브리드 PET-MRI 프로젝트는 1대당 300만 달러를 초과하는 자본 예산을 필요로 할 수 있으며 3차 의료기관 이외의 도입을 제한합니다. MRI실에는 전파차폐, 구조보강, 극저온안전시스템이 필요하며, 스캐너 가격 외에 설치비용이 추가됩니다. CT 시스템은 ALARA 원칙을 따르기 때문에 선량 조절 감시 기능을 내장하고 준거한 도입에는 하드웨어 소프트웨어 비용이 증가합니다. 병원 외래 진료에서 스캔 단가의 감소 또는 가로세로 경향은 신규 도입의 투자 회수 기간을 연장시킵니다.

X선 시스템은 2025년에 모달리티 점유율 29.12%를 차지하고 저비용 디지털 방사선 촬영이 신속한 진단 결과를 제공하고 의료 영상 시장에서 직원의 폭넓은 숙련도를 배경으로 응급 및 정형외과 워크플로우에서 정착한 이용을 반영하고 있습니다. 컴퓨터 단층촬영(CT)은 멀티 디텍터 어레이, 서브세컨드의 시간 분해능, AI 지원 워크플로우 툴로 고 볼륨 환경에서의 판독 시간 단축과 검출 감도 향상을 실현하여 2031년까지 연평균 복합 성장률(CAGR)6.39%에서 가장 빠르게 성장하는 모달리티입니다. MRI는 신경 및 근골격계 화상 진단에 있어서 여전히 중요한 역할을 담당하고 있습니다만, 200만 달러-300만 달러라는 시스템 가격대와 헬륨 공급의 불안정함으로부터, 의료 영상 시장에서는 일부 조달 팀이 재생품 1.5 T 시스템에의 이행을 검토하고 있습니다. 초음파 검사의 보급은 중량 500g 미만 및 가격 5,000달러 이하의 휴대형 장치에 의해 확대되고 있습니다. 이를 통해 기존 장바구니 장비를 즉시 사용할 수 없었던 1 차 진료 및 응급 팀이 진료 현장에서 영상 진단을 할 수 있습니다. 핵의학 검사는 방사성 의약품 파이프라인에 의존한 상황이 계속되고 있으며, PSMA PET 트레이서 등의 승인에 의해 전립선 종양학에서의 적응이 확대되어 3차 의료기관에서의 PET-CT의 이용 패턴에 영향을 주고 있습니다.

투시검사와 유방촬영은 성숙한 갱신 시장으로 유방촬영 품질 기준법(MQSA)의 틀과 진화하는 밀도 보고 규칙으로 이어져 급속한 장치 증가가 아니라 품질 및 안전 기준에 기초한 디지털화가 진행되고 있습니다. PET-CT나 PET-MRI와 같은 하이브리드 플랫폼은 종양학과 신경학으로 보완적인 강점을 융합시키고 있습니다만, 의료 영상 시장에 있어서, 학술 거점 이외의 도입은 보험자에 의한 부가가치의 조사에 의해 억제될 가능성이 있습니다. 벤더 각사는 구독에 의한 성능 해방을 실현하는 소프트웨어 정의 기능으로 이행중입니다. 여기에는 AI 재구성, 스펙트럼 모드, 기능 도입 및 하드웨어 전체 대체를 분리하는 워크플로 조정이 포함됩니다. 포톤 카운트 CT는 이러한 전환을 구현하고 OEM 각사는 스펙트럼 툴과 선량 우위성을 서비스 소프트웨어 번들과 조합하여 ROI의 명확화를 도모하고 있습니다. 이 조합은 의료 영상 시장에서 경쟁하는 공급업체에게 제공업체에게 안정적인 가치 실현과 지속 가능한 설치 기반 전략을 지원합니다.

북미는 2025년 시점에서 의료 영상 시장 규모의 41.95%를 차지하며, 확립된 상환구조에 따른 고스펙 시스템, 엔터프라이즈 이미지 플랫폼, AI 대응 워크플로우의 중심지로 계속되고 있습니다. 미국은 대규모 자본 예산과 영상 진단을 일상 진료 및 복잡한 치료에 통합하는 대규모 외래 환자 생태계를 보유하고 있기 때문에 세계 수익의 가장 큰 부분을 차지합니다. 캐나다에서는 일부 주에서 대기 시간의 제약이 발생하고 있어, 이것이 갱신 사이클을 늦추는 것과 동시에 관민 제휴를 촉진하고 있습니다. 이러한 요인은 조달 시기와 서비스 모델에 영향을 미칩니다. FDA의 의료기기 규제와 CMS의 보험 적용 결정은 기능 도입의 타이밍이나 임상 적응증에 영향을 미치고 의료 영상 시장에서 기존 하드웨어 라인과 연계하는 소프트웨어 툴의 조기 도입을 뒷받침하고 있습니다.

유럽에서는 성숙 단계의 수요를 보이고 있으며 집중형 입찰에 의해 이익률은 압축되는 것, 의료 영상 시장에 있어서의 모달리티 갱신 사이클의 복수년에 걸친 수요 가시성이 확보되고 있습니다. 독일과 프랑스는 영국보다 1인당 이용률이 높고, 영국에서는 예산 제약에 의해 설비 갱신이 제한되어 대륙 국가에 비해 스캐너 밀도가 낮아지고 있습니다. MDR(의료기기 규칙)의 실시에 의해 AI를 다용하는 소프트웨어의 컴플라이언스 작업 부하와 인증 기간이 증가하고, 의료 영상 시장에 있어서, 규제 대응 팀이 충실해, 체계적인 시판 후 조사 프로그램을 가지는 기존 기업이 유리한 입장에 있습니다. 중동유럽의 민간 의료기관은 가격 차이와 대기 시간의 차이로 서유럽으로부터의 의료 관광객을 매료시키는 지역 거점에 검사를 집약하는 움직임에 대응하기 위해 현대적인 화상 진단 설비에 대한 투자를 추진하고 있습니다.

아시아태평양은 5.54%의 연평균 복합 성장률(CAGR)로 가장 빠르게 성장하고 있으며, 중국, 인도, 동남아시아에서는 공공 투자와 민간 체인 확대로 접근이 확대되고 있습니다. 국내 제조업체는 의료 영상 시장에서 생산 능력을 증강하고 경쟁력 있는 가격대를 제공합니다. 일본에서는 대체 시장으로서의 특성을 볼 수 있습니다. 반면 호주와 한국에서는 첨단 기술 도입이 진행되는 반면 인구 규모의 영향으로 절대 수요량은 소규모입니다. ASEAN 역내에서는 규제의 분단화가 진행되고 있어 시장마다의 등록 수속이나 상환 계획의 책정이 필요합니다. 이는 의료 영상 시장에서 제조업체의 제품 투입 순서와 파트너 선정에 영향을 미칩니다. 중동에서는 경제 다각화 정책의 일환으로 3차 의료 거점에 대한 국가 투자가 프리미엄 영상 진단 장치의 조달을 촉진하고 있습니다. 한편, 사하라 이남 아프리카는 여전히 서비스가 부족하고 있으며, 인프라의 실정에 맞는 휴대형 및 재생품 솔루션에 의존하고 있습니다. 남미에서는 브라질의 도시 사립 병원이 영상 진단을 중심으로 서비스 라인을 구축하는 가운데 멕시코와 콜롬비아에 성장이 집중되고 있습니다. 한편, 공공 의료 시스템이나 지방 지역에서는 이동식 장치군이나 원격 진단 보고에 의한 액세스 확대가 진행되고 있습니다.

Medical imaging market size in 2026 is estimated at USD 82.42 billion, growing from 2025 value of USD 78.90 billion with 2031 projections showing USD 102.56 billion, growing at 4.46% CAGR over 2026-2031.

North America remains the largest revenue pool due to a dense installed base and capital budgets, while Asia-Pacific shows the strongest momentum as governments fund hospital capacity and domestic manufacturers scale price-competitive systems that expand access. X-ray continues to anchor high-volume use cases in emergency and orthopedic care, although computed tomography is gaining as faster scanners pair with AI-assisted detection and triage. Hospitals still lead because they can finance premium systems and link imaging to procedural services, yet outpatient imaging centers are taking share as payers steer site-of-service to lower-cost settings. Competitive dynamics reflect an oligopoly of multinational leaders that face price pressure from Chinese entrants and new demand pockets in mobile, handheld, and software-enabled workflows that change unit economics across the medical imaging market.

Chronic disease burden anchors sustained demand in the medical imaging market as cardiovascular disease, cancer, and diabetes require imaging for diagnosis, staging, and longitudinal monitoring across the care continuum. Cancer incidence is rising in many middle-income countries due to aging and lifestyle change, a trend that feeds CT and PET volumes within standardized oncology pathways. Cardiac CT and stress MRI have rolled into guideline-aligned care for coronary artery disease risk stratification, especially among adults with type 2 diabetes where surveillance protocols now emphasize noninvasive imaging in lieu of invasive diagnostics. Chronic kidney disease prevalence among older adults widens the role for non-contrast MRI and advanced sequences that avoid gadolinium exposure, which has accelerated software adoption for diffusion-weighted and arterial spin labeling protocols in the medical imaging market. Reimbursement policy is an important lever, since Medicare's Appropriate Use Criteria for advanced diagnostic imaging obliges decision-support integration that aligns clinical indications with modality selection and creates a defensible utilization record.

The shift toward value-based contracts motivates health systems to detect disease earlier to avoid downstream costs, which expands the role of high-yield imaging in screening and diagnostic workups. Low-dose CT for lung cancer screening has a Grade B recommendation from the U.S. Preventive Services Task Force, and coverage decisions increased scan volumes as programs matured in community settings. State-level dense-breast legislation and the federal density reporting rule have broadened pathways for supplemental ultrasound or MRI in women with heterogeneously dense tissue, which drives demand for automated breast ultrasound and higher-throughput MRI suites in the medical imaging market. AI-enhanced triage that flags suspected intracranial hemorrhage or pulmonary embolism within minutes improves emergency department prioritization and supports more timely interventions, particularly in stroke pathways where every delay impacts outcomes. Compliance considerations include the need for robust validation of Software as a Medical Device across diverse datasets for FDA clearance, which affects release cadence and field performance in the medical imaging market.

Premium MRI and hybrid PET-MRI projects can require capital budgets above USD 3 million per unit, which restricts adoption outside tertiary centers. MRI rooms need RF shielding, structural reinforcement, and cryogen safety systems, which add siting expense beyond the scanner price. CT systems incorporate dose modulation and monitoring to align with ALARA expectations, increasing hardware and software costs for compliant deployments. Declining or flat per-scan reimbursement in hospital outpatient settings lengthens payback periods for new installations.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

X-ray systems commanded 29.12% modality share in 2025, reflecting entrenched use in emergency and orthopedic workflows where low-cost digital radiography delivers fast answers with broad staff familiarity in the medical imaging market. Computed tomography is the fastest-moving modality at a 6.39% CAGR to 2031 based on multi-detector arrays, sub-second temporal resolution, and AI-aided workflow tools that cut review time and enhance detection sensitivity in high-volume settings. MRI retains a premium role in neuro and musculoskeletal imaging, though system pricing in the USD 2-3 million range and helium supply volatility push some procurement teams toward refurbished 1.5T systems in the medical imaging market. Ultrasound penetration expands with handheld devices that weigh under 500 grams and sell below USD 5,000, which puts point-of-care imaging in the hands of primary care and emergency teams that lacked immediate access to cart-based systems. Nuclear imaging remains tied to the radiopharmaceutical pipeline, with approvals like PSMA PET tracers widening indications in prostate oncology and influencing PET-CT utilization patterns in tertiary centers.

Fluoroscopy and mammography are mature replacement markets where digital upgrades are driven by quality and safety standards rather than rapid unit growth, guided by the Mammography Quality Standards Act framework and evolving density reporting rules. Hybrid platforms such as PET-CT and PET-MRI blend complementary strengths in oncology and neurology, though payer scrutiny of incremental value can temper adoption outside academic hubs in the medical imaging market. Vendors are shifting toward software-defined capabilities that unlock performance via subscriptions, including AI recon, spectral modes, and workflow orchestration that decouples feature adoption from full-hardware replacement. Photon-counting CT exemplifies this shift, as OEMs package spectral tools and dose advantages with service and software bundles for clearer ROI narratives. This mix supports stable value realization for providers and a durable installed base strategy for suppliers competing in the medical imaging market.

The Medical Imaging Market Report is Segmented by Modality (MRI, Computed Tomography, Ultrasound, X-Ray, and More), Application (Diagnostic, Therapeutic/Interventional, and Research & Clinical Trials), End User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). Market Forecasts are Provided in Terms of Value (USD).

North America held 41.95% share of the medical imaging market size in 2025 and remains the center of gravity for high-spec systems, enterprise imaging platforms, and AI-enabled workflows that align with established reimbursement structures. The United States accounts for the largest portion of global revenue due to capital budgets at scale and a large outpatient ecosystem that integrates imaging into routine care and complex procedures in the medical imaging market. Canada experiences wait-time constraints in some provinces that slow replacement cadences and stimulate public-private partnerships, factors that shape procurement timing and service models. FDA device oversight and CMS coverage decisions influence feature adoption timelines and clinical indications, which reinforces early uptake of software tools that pair with established hardware lines in the medical imaging market.

Europe shows mature demand with centralized tenders that compress margins yet offer multi-year volume visibility for modality refresh cycles in the medical imaging market. Germany and France maintain higher per-capita utilization than the United Kingdom, where budget constraints limit capital replacement and contribute to lower scanner density relative to continental peers. MDR implementation increased compliance workload and certification time for AI-rich software, which favors incumbents with deep regulatory teams and structured post-market surveillance programs in the medical imaging market. Private providers in Central and Eastern Europe invest to serve medical tourists from Western Europe, where pricing and wait-time differentials pull procedures to regional hubs with modern imaging suites.

Asia-Pacific is the fastest-growing region at a 5.54% CAGR as China, India, and Southeast Asia expand access through public investment and private-chain growth, with domestic manufacturers adding capacity and competitive price points in the medical imaging market. Japan behaves like a replacement market, while Australia and South Korea combine high technology adoption with smaller absolute volumes due to population size. Regulatory fragmentation across ASEAN requires market-by-market registration and reimbursement planning, which influences launch sequencing and partner selection for manufacturers in the medical imaging market. In the Middle East, sovereign investment in tertiary-care hubs drives premium imaging procurement as part of economic diversification agendas, while Sub-Saharan Africa remains underserved and relies on portable and refurbished solutions tailored to infrastructure realities. South America concentrates growth in Brazil, Mexico, and Colombia as urban private hospitals build imaging-led service lines, while public systems and rural areas extend access through mobile fleets and tele-reporting in the medical imaging market.