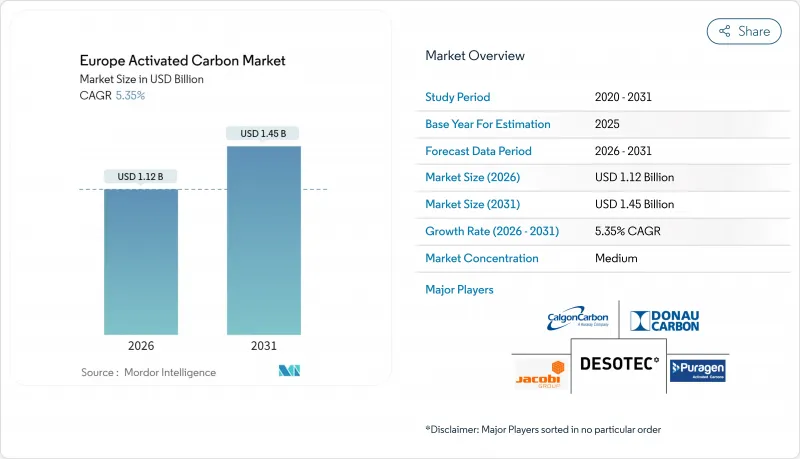

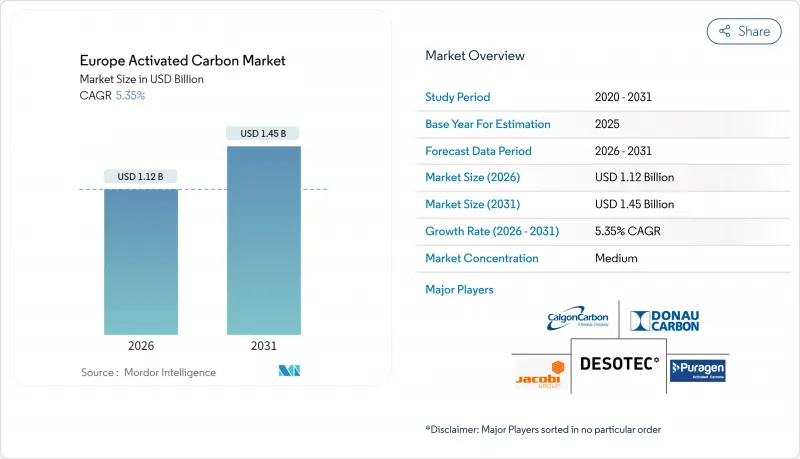

유럽의 활성탄 시장은 2025년의 10억 6,000만 달러에서 2026년에는 11억 2,000만 달러로 성장하고 2026년부터 2031년에 걸쳐 CAGR 5.35%로 성장을 지속하여 2031년까지 14억 5,000만 달러에 이를 것으로 예측됩니다.

이러한 성장은 환경 규제 강화, 지자체에 의한 수질 기준 확대, 산업 배출 제한 엄격화 등의 요인이 더해져 지역 전체에 신속하게 도입 가능한 흡착 기술에 대한 수요가 높아지면서 발생합니다. 수도사업의 강력한 업그레이드 주기, 2026년에 도래하는 PFAS 규제 준수 기한, 산업 배출 지침 2.0의 확대에 의해 최종 사용자는 장기 공급 계약을 체결하고 예측 가능한 가격 설정과 재활성화 서비스를 확보하도록 요구받고 있습니다. 유럽의 활성탄 시장은 원료 가격의 변동성에 대응하기 위해 수입 코코넛 껍질탄을 지역의 활엽수탄 및 갈색탄과 혼합하는 한편, 순환형 재활용에 대한 투자를 추진하고 있습니다. 이를 통해 폐기 비용을 줄이고 스코프 3 배출량을 줄일 수 있습니다.

산업 배출 지침의 개정에 의해 규제 대상이 대규모 연소 플랜트로부터 중규모 보일러, 제련소, 파운드리로 확대되어, 종래는 규제 대상 밖이었던 수천개의 시설이 수은 및 분진 배출 상한을 준수하도록 요구받고 있습니다. 배출 상한치는 기존 플랜트에서 1-4μg/m3, 신규 건설에서 1-2μg/m3로 설정되어 공식 BAT(최고 이용 기술) 참고문서에서는 수은 목표 달성의 주요 수단으로 활성탄 주입이 명기되어 있습니다. 플랜트 운영자는 분말 제형을 선택하는 경향이 있습니다. 덕트측 주입 시스템은 설계, 발주 및 시운전을 18개월 이내에 완료할 수 있는 반면, 직물 필터 개조나 습식 스크러버는 50개월을 넘는 경우가 많기 때문입니다. EU 결속 기금은 2027년까지 대기 정화 목표로 1,470억 유로를 기부하고 있어 소규모 배출 사업자의 자본 장벽을 경감합니다. 이에 따라 유럽의 활성탄 시장에서는 유황분이 풍부한 배기가스용 고요오드 함유 PAC 등급에 대한 선주문이 증가하고 있습니다. 설비 OEM 제조업체는 탄소 공급, 사일로 렌탈 및 사용 탄소 포집을 포함한 서비스 계약이 급증하고 있음을 보고하고 있으며, 이는 고객이 부품 조달보다 턴키 방식의 규제 대응을 선호하는 경향을 반영합니다.

독일, 프랑스, 네덜란드, 벨기에의 수도 사업자는 보다 엄격한 미량 오염물질 제거 기준에 직면하고 있으며, GAC(입상 활성탄)의 교환 빈도 증가와 필터 공급, 용기 업그레이드 및 재활성화를 8년 단위의 서비스 계약에 통합한 대규모 입찰로 이어지고 있습니다. 독일에서만 상수도 정화 처리용으로 연간 1억 3,000만 유로 상당의 활성탄을 소비하고 있으며, 이는 연간 약 5만 5,000톤의 신규 및 재생 활성탄에 상당합니다. 개정 도시폐수지침에 근거하여 도입되는 미량물질 규제에서는 80-93%의 제거효율이 요구되지만, 저회분 코코넛 껍질 또는 갈탄 기반의 GAC를 생물활성필터와 병용함으로써 이 수준이 안정적으로 달성되고 있습니다. 조달 기록에 의하면, 수도 사업자는 수두 손실을 억제하면서 필터 수명을 18-24개월 연장하는 이중층 필터 설계를 선호하고 있습니다.

동남아시아의 코코넛 생산지역에서는 가뭄으로 인한 껍질 부족 현상이 발생하여 2024년 1분기부터 2025년 3분기에 걸쳐 CIF 유럽 가격이 38% 상승했습니다. 동시에 동유럽의 지정학적 긴장에 의해 석유 코크스 대체 원료가 제한되어 유럽의 소규모 소성로 몇개사가 입찰 피크 시에 유지보수를 위해 가동을 정지해야만 했습니다. 대규모 다원료 제조업체들은 필리핀 코플라 공장과 콜롬비아 석탄 수출업체와의 장기 공급 계약으로 위험을 완화했지만, 가격 급변동은 여전히 지수 연동 계약이 없는 유통업체의 이익률을 압박하고 있습니다. 유틸리티 및 식품회사는 연간 5%를 상한으로 하는 가격 상승 조항을 요구하는 경우가 증가하고 있으며, 변동 위험의 일부를 공급업체에 전가함으로써 유럽의 활성탄 시장 전체의 운전자금 부담을 증가시키고 있습니다. 유럽의 활엽수 탄화 프로젝트에 대한 투자는 일정한 완충재가 되지만, 규모가 제한되어 있기 때문에 고순도 용도에서 바이오 원료는 수입 코코넛 껍질을 완전히 대체할 수 없습니다.

분말 활성탄은 2025년 시점에서 유럽의 활성탄 시장의 47.63%를 차지하였으며, 갈탄 및 바이오매스 보일러의 배기가스 주입 시스템에서 정착한 용도를 반영하고 있습니다. 중규모 플랜트는 산업배출지침의 대상이 되는 케이스가 증가함에 따라 CAGR 5.63%로 확대될 것으로 전망됩니다. PAC의 45μm 미만의 입자 크기와 할로겐 함침 처리에 의해 수은 흡착 용량은 1.8-2.4 mg Hg/g 탄소에 이르고, 이는 기준이 되는 석탄 유래 분말을 상회하고 있습니다.

미립자 활성탄은 PFAS 규제의 기한에 견인되어 수처리 분야 지출의 대부분을 차지하고 있습니다. 압출 성형탄은 원통 형상이 압력 손실을 줄이고 고속 유동층에서의 마모를 견디기 때문에 용제 회수나 제약용 공기 정화에 여전히 필수적입니다. 향후 전망으로는 PAC 공급업체는 저회분과 미세공 구조를 겸비한 코코넛 껍질 원료의 실험을 진행하고 있으며, 석탄화력발전소의 폐지 후에도 수요를 유지하기 위해 수은과 다이옥신 양쪽의 포착을 목표로 하고 있습니다. 이러한 혁신은 유럽의 활성탄 시장이 상품화에 뒤쳐지지 않고 제품의 지속적인 업데이트가 보장되도록 합니다.

유럽의 활성탄 시장의 보고서는 유형별(분말 활성탄, 미립자 활성탄, 압출성형 또는 펠릿화 활성탄), 용도별(가스 정화, 수처리, 금속 추출, 의약품 등), 지역별(독일, 영국, 프랑스, 이탈리아, 스페인 및 기타 유럽 국가)으로 분류됩니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

The Europe Activated Carbon Market is expected to grow from USD 1.06 billion in 2025 to USD 1.12 billion in 2026 and is forecast to reach USD 1.45 billion by 2031 at 5.35% CAGR over 2026-2031.

This growth rests on converging environmental regulations, expanding municipal water quality mandates, and tightening industrial emission limits that collectively reinforce demand for rapid-deployment sorbent technologies across the region. Strong replacement cycles in water utilities, a looming PFAS compliance deadline in 2026, and the enlargement of the Industrial Emissions Directive 2.0 are pushing end users to lock in long-term supply contracts, securing predictable pricing and reactivation services. The European activated carbon market is also adapting to feedstock volatility by blending imported coconut shell char with regional hardwood or lignite sources, while simultaneously investing in circular reactivation capacity that cuts disposal fees and lowers scope-3 emissions for customers

Revisions to the Industrial Emissions Directive broaden compliance coverage from large combustion plants to mid-scale boilers, smelting and foundries, compelling thousands of facilities previously below threshold to meet mercury and dust caps. Emission ceilings now stand at 1-4 µg/m3 for existing stacks and 1-2 µg/m3 for new builds, and the official BAT reference document explicitly names activated carbon injection as the primary path to meet the mercury target. Plant operators gravitate toward powdered formulations because duct-side injection systems can be engineered, ordered, and commissioned within an 18-month window, whereas fabric filter retrofits or wet scrubbers often exceed 50 months. EU Cohesion Funds reserve EUR 147 billion for clean-air objectives through 2027, shaving capital hurdles for smaller emitters. Consequently, the European activated carbon market registers rising forward orders for high-iodine PAC grades tailored to sulfur-rich flue gas. Equipment OEMs also report a surge in service contracts bundling carbon supply, silo rental, and spent carbon haul-back, reflecting customers' preference for turnkey compliance over component procurement.

Utilities in Germany, France, the Netherlands, and Belgium confront stricter micropollutant removal thresholds, leading to more frequent GAC change-outs and larger bids that roll media supply, vessel refurbishments, and reactivation into eight-year service lots. Germany alone consumes activated carbon worth EUR 130 million annually for municipal water polishing, equating to roughly 55,000 tons of virgin and reactivated material per year. Trace-substance rules being transposed under the revised Urban Wastewater Directive require 80-93% removal efficiency, levels consistently achieved by low-ash coconut shell or lignite-based GAC in tandem with biologically active filters. Procurement records show utilities favor dual-bed filter designs that retain hydraulic head yet extend media life by 18-24 months.

Coconut growing regions in Southeast Asia witnessed drought-driven shell shortages, sending CIF Europe prices up 38% between Q1 2024 and Q3 2025. Simultaneously, geopolitical tension in Eastern Europe constrained petcoke alternatives, forcing several small European kilns to idle capacity for maintenance during peak tender season. Large multi-feedstock players mitigated risk through long-term offtake agreements with Philippine copra mills and Colombian coal exporters, but price whiplash still squeezes profit margins for distributors lacking index-linked contracts. Utilities and food companies increasingly request price escalation clauses capped at 5% per annum, transferring part of the volatility to suppliers and intensifying the working-capital load across the Europe activated carbon market. Investment in European hardwood char projects provides some buffer, yet limited scale means bio-feedstock cannot fully displace imported coconut shell in high-purity applications.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Powdered Activated Carbons jointly captured 47.63% Europe activated carbon market share in 2025, reflecting entrenched use in flue-gas injection systems across lignite and biomass boilers, and it is projected to grow at a 5.63% CAGR as more mid-scale stacks fall under the Industrial Emissions Directive. PAC's sub-45 µm particle size coupled with halogen impregnation elevates mercury uptake capacity to 1.8-2.4 mg Hg/g carbon, outperforming baseline coal-derived powders.

Granular Activated Carbons account for most water purification spending, driven by PFAS deadlines. Extruded carbons remain indispensable in solvent recovery and pharmaceutical air purification because their cylindrical geometry lowers pressure drop and resists attrition in high-velocity beds. Looking forward, PAC suppliers are experimenting with coconut-shell precursors that combine low ash content with micropore dominance, targeting both mercury and dioxin capture to stay relevant once coal plants retire. These innovations ensure the Europe activated carbon market maintains continuous product renewal rather than slipping into commoditization.

The Europe Activated Carbon Report is Segmented by Type (Powdered Activated Carbons, Granular Activated Carbons, and Extruded or Pelletized Activated Carbons), Application (Gas Purification, Water Purification, Metal Extraction, Medicine, and Others), and Geography (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).