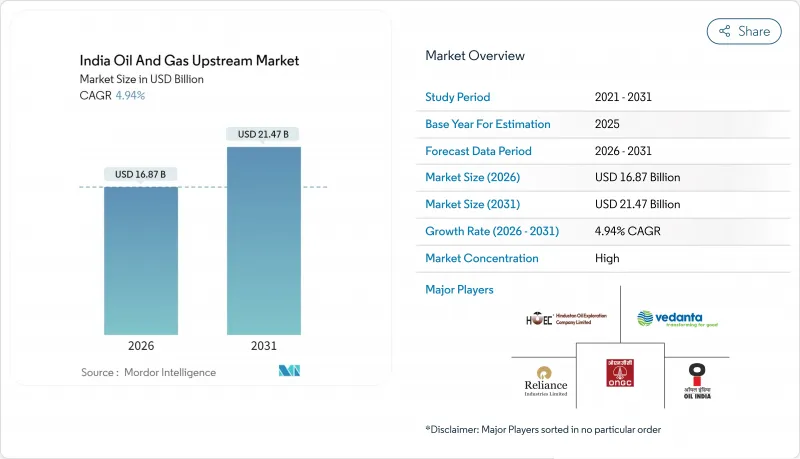

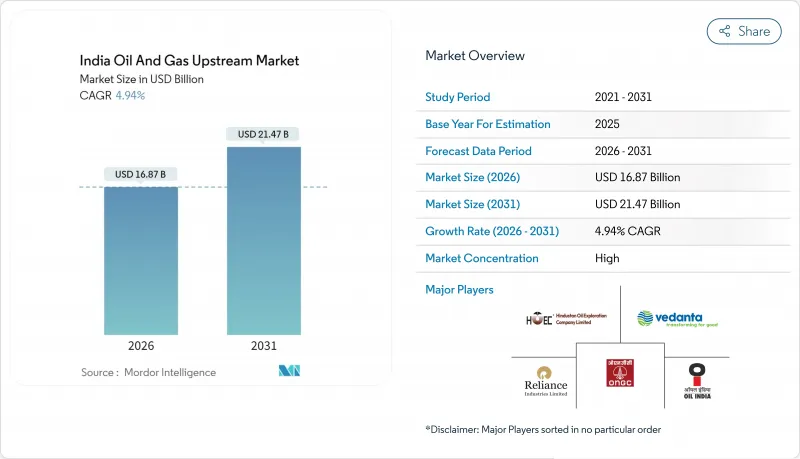

인도의 석유 및 가스 업스트림 시장은 2025년 160억 8,000만 달러에서 2026년에는 168억 7,000만 달러로 성장하고, 2026년에서 2031년에 걸쳐 CAGR 4.94%로 성장을 지속하여 2031년까지 214억 7,000만 달러에 달할 전망입니다.

강력한 정책지원, 디지털 유전 도입, 석유 회수 증진(EOR) 프로젝트가 지질학적 복잡성에 의한 억제요인을 상쇄하고, 사업자는 성숙 자산으로부터 추가 원유를 채굴할 수 있어 수입 증가의 둔화로 이어지고 있습니다. 자본은 심해 탐사 프로젝트로 이동하고 있으며, 대규모 발견은 기존 인프라와 연결 가능하지만, 인도의 1세대 해양 플랫폼이 수명에 가까워짐에 따라 해체 계약의 파도가 밀려오고 있습니다. 비공개회사는 민첩한 굴착 및 완성 기술을 도입하고 있지만, 국유기업은 광구 보유와 기존 인프라를 통해 전략적 지배권을 유지하고 있습니다. 드릴링 장비, 프로판트 및 해저 장비 공급망의 병목 현상은 여전히 주요 조업 과제이지만, "메이크 인 인디아" 정책 하에서 국내 제조가 확대됨에 따라 점차 완화되고 있습니다.

국내 석유 및 가스 생산량은 2017년도의 3,600만 톤에서 2024년도에는 2,940만 톤으로 감소하였으며, 성숙한 저류층에서의 ASP(알칼리-계면활성제-폴리머 공법), 폴리머, 혼화 가스 주입법의 도입이 사업자에게 명확한 인센티브가 되고 있습니다. Cairn Oil & Gas사는 2025년 4월 주주용 프레젠테이션에서 라자스탄주의 유전에 풀필드 ASP를 도입하기 위해 10억 달러를 투입하여 회수율을 15-20% 향상시키는 목표를 설정하였습니다. 아쌈주 라크와 유전 및 구자라트주 카롤 유전에서의 파일럿 프로그램은 하루에 4,000-6,000 배럴의 증산 효과가 입증되어 인도 국내 430곳의 성숙 유전 전체에서 재현 가능한 성과를 실증했습니다. 지표 설비의 대부분이 이미 정비되어 있기 때문에 투자 회수 기간이 4년 미만으로 단축되고 사업자는 현재 EOR을 위험이 높은 프론티어 탐사를 대신하는 이익률 향상책으로 활용하고 있습니다.

탄화수소 탐사 및 라이선싱 정책(HELP)에 의해 인도는 비용 회수형 생산 분여 제도에서 투명성이 높은 수익 분여 제도로 이행해, 감사 분쟁을 해소함과 동시에 가스 판매의 완전한 자유화를 실현했습니다. 탄화수소 총국에 따르면 2018년 이후 실시된 9회 OALP 입찰 라운드에서는 누계 134블록이 부여되어 13억 7,000만 달러 상당의 작업 계획이 보장되고 있습니다. BP 및 Eni사와 같은 주요 기업은 재래형 및 비재래형 자원을 포괄하는 통일 라이선스 조건에 매료되어 차기 라운드 X에 대한 사전 자격 심사를 통과하고 있습니다. 자유 구획 모델을 통해 입찰자는 정부의 입찰 선정을 기다리지 않고 탐광 대상지에 따른 다각형 구획을 설정할 수 있으므로 구획 취득 사이클이 가속됩니다.

라자스탄 주 버머 힐과 아쌈의 파쇄 탄산염 암석에서 저류층의 불균일성은 다단 수압 파쇄와 고밀도 수직 로깅을 필요로 하며 기존 갱정에 비해 드릴링 비용을 두배로 증가시킵니다. 탄화수소 총국은 투수 계수가 1mD 미만인 60개 이상의 탐광지를 '타이트 오일'로 분류하고 있습니다. 저류층 품질의 불확실성은 실패 위험을 높이고 운영자는 드릴링 중에 완성 하드웨어를 사전에 확보해야 하며 이는 자본을 구속하고 현장 수준의 손익 분기점을 밀어 올립니다. 파쇄 작업을 위한 물 조달도 자이살메르와 같은 건조 지역에서는 환경 모니터링을 강화하는 요인이 됩니다.

2025년 매출의 46.22%를 오프쇼어 유전이 차지했지만, 심해 타이백에 의한 회수 기간의 단축에 의해 2031년까지 연평균 복합 성장률(CAGR) 6.32%로 온쇼어 부문을 상회할 전망입니다. 인도의 석유 및 가스 업스트림 시장의 규모(오프쇼어 단독)는 2025년 74억 3,000만 달러에서 2031년까지 107억 3,000만 달러로 성장할 것으로 예측됩니다. 한편, 온쇼어 부문은 여전히 규모가 크지만, 쉽게 채굴 가능한 자원의 대부분이 이미 고갈되어 있기 때문에 CAGR 3.56%로 생산량이 두드러질 전망입니다.

해양 분야의 성장 요인으로는 ONGC사의 KG-DWN-98/2 클러스터, 릴라이언스 BP사의 MJ 및 위성 개발, 오일 인디아사와 페트로브라스사의 마하나디 분지 공동 사업을 들 수 있습니다. 해저증압설비, 다상펌프, 장거리 타이백 파이프라인 도입으로 수심 1,500미터를 넘는 해역에서도 단위 채굴 비용의 절감이 실현되고 있습니다. Panna Mukta Tapti 플랫폼의 폐지 조치는 규제 당국이 수명주기 말기에 부채를 관리할 수 있는 능력을 가지고 있음을 보여주며, 수명주기 종료 시의 의무를 우려하는 신규 참가자를 뒷받침합니다. 성숙한 인프라가 존재하는 온쇼어 분야의 기회는 여전히 매력적이지만, 엄격한 물 이용 규제와 토지 접근 지연은 단기 성장을 둔화시킬 수 있습니다.

원유는 2025년에 매출 점유율 67.45%를 유지했지만 천연가스 관련 매출은 2031년까지 34.80%를 차지할 것으로 예측됩니다. 이는 1차 에너지 점유율 15%라는 국가 목표 달성을 위한 가스 생산량이 증가하기 때문입니다. HELP(에너지, 환경 및 생활개선계획)에 따라 라이선싱된 가스 광구는 2025년 인도의 석유 및 가스 업스트림 시장의 규모(가스 부문)를 52억 3,000만 달러로 밀어 올렸으며 CAGR 6.88%로 확대될 전망입니다. 이 가속은 정책 인센티브와 저탄소화를 반영하여 4.18%의 성장률을 나타내는 석유 부문을 웃돌고 있습니다.

전국 가스망의 확장과 295개소의 신규 CNG 스테이션을 포함한 기반 정비에 의해 수요의 확실성이 탄생합니다. 가스 생산자는 2016년 이후 발견된 6조 입방 피트(Tcf)까지의 생산량에 대한 판매 자유를 누릴 수 있으며 기존의 가격 상한으로 인해 수익에 미치는 영향을 피할 수 있습니다. 한편, 석유중심 자산은 감산억제를 위한 석유 회수 증진(EOR) 투자에 의존하고 있으며, 이는 비용층을 추가하고 이익률 상승을 억제하고 있습니다. 수반 가스의 수익화는 아직 충분히 활용되지 않은 수단이며, ONGC의 뭄바이 하이 플레어백 프로젝트만으로도 완성 시 하루에 4억 입방 피트(0.4Bcf/d)의 공헌이 예상되어 석유 및 가스의 균형 잡힌 포트폴리오를 강화합니다.

The India Oil And Gas Upstream Market is expected to grow from USD 16.08 billion in 2025 to USD 16.87 billion in 2026 and is forecast to reach USD 21.47 billion by 2031 at 4.94% CAGR over 2026-2031.

Strong policy support, digital oilfield rollouts, and enhanced oil recovery (EOR) projects offset the drag from geological complexity, enabling operators to extract additional barrels from maturing assets and thereby slowing import growth. Capital is shifting toward deepwater prospects, where large discoveries can be tied back to existing infrastructure, while a wave of decommissioning contracts emerges as India's first generation of offshore platforms nears the end of their life. Private companies introduce agile drilling and completion technologies, yet state-owned enterprises retain strategic control through acreage holdings and legacy infrastructure. Supply-chain bottlenecks in rigs, proppants, and subsea equipment remain the principal operational headwinds but are gradually easing as domestic manufacturing expands under "Make in India" mandates.

National oil output fell from 36 million tonnes in FY2017 to 29.4 million tonnes in FY2024, creating a clear incentive for operators to deploy ASP, polymer, and miscible-gas flooding in mature reservoirs. Cairn Oil & Gas has earmarked USD 1 billion to retrofit its Rajasthan fields with full-field ASP, targeting a 15-20% uplift in recovery factors as per its April 2025 shareholder presentation. Pilot programs in Assam's Lakwa and Gujarat's Kalol fields recorded incremental gains of 4,000-6,000 barrels per day, demonstrating replicable gains across India's 430 mature fields. Operators now view EOR as a margin-accretive alternative to risky frontier exploration because most surface facilities are already in place, shortening payback periods to under four years.

The Hydrocarbon Exploration & Licensing Policy (HELP) has transitioned India from a cost-recovery production-sharing regime to a transparent revenue-sharing system, thereby eliminating audit disputes while granting full marketing freedom for gas. Since 2018, nine OALP rounds have cumulatively awarded 134 blocks and attracted work-program commitments worth USD 1.37 billion, according to the Directorate General of Hydrocarbons. Major industry players, such as BP and Eni, have pre-qualified for the upcoming Round X, enticed by unified license terms that cover both conventional and unconventional resources. The open-acreage model allows bidders to carve out prospect-specific polygons instead of waiting for government-curated bid maps, thereby accelerating acreage acquisition cycles.

Reservoir heterogeneity in Rajasthan's Barmer-Hill and Assam's fractured carbonates requires multi-stage hydraulic fracturing and high-density vertical logging, which doubles drilling costs compared to vintage wells. The Directorate General of Hydrocarbons lists more than 60 prospects with permeability below 1 mD, classifying them as tight oil. Reservoir-quality uncertainty elevates failure risk and forces operators to pre-commit completion hardware while drilling, tying up capital and inflating field-level break-evens. Water sourcing for frac jobs also raises environmental scrutiny in arid districts such as Jaisalmer.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Offshore fields delivered 46.22% of 2025 revenue, yet they are set to outpace onshore operations with a 6.32% CAGR through 2031 as deepwater tie-backs shorten payback periods. The India oil & gas upstream market size derived from offshore alone is projected to grow from USD 7.43 billion in 2025 to USD 10.73 billion by 2031. Meanwhile, the onshore domain, although still larger, faces a plateauing output at a 3.56% CAGR because most low-hanging resources have already been drained.

The offshore growth narrative is based on ONGC's KG-DWN-98/2 cluster, Reliance-BP's MJ and Satellite developments, and the collaboration between Oil India and Petrobras in the Mahanadi Basin. Sub-sea boosting, multiphase pumping, and long-tie-back pipelines reduce unit lifting costs, even in water depths exceeding 1,500 meters. Decommissioning of the Panna-Mukta-Tapti platforms also demonstrates the regulator's capacity to manage late-life liabilities, encouraging new entrants wary of end-of-life obligations. Onshore opportunities remain attractive where mature infrastructure exists; however, stringent water-use restrictions and land-access delays can dilute near-term growth.

Crude oil retained a 67.45% revenue share in 2025; however, natural-gas-linked revenue is expected to capture 34.80% by 2031 as gas output increases to meet the national goal of a 15% primary-energy share. Gas-rich blocks licensed under HELP contribute to an India oil & gas upstream market size of USD 5.23 billion in 2025 for gas, expanding at a 6.88% CAGR. This acceleration outpaces oil, which grows at 4.18%, mirroring policy incentives and lower carbon intensity.

Enabling infrastructure, including the National Gas Grid extension and 295 new CNG stations, creates offtake certainty. Gas producers enjoy marketing freedom for volumes up to 6 Tcf discovered post-2016, shielding returns from legacy price caps. Conversely, oil-focused assets rely on EOR spending to stem declines, adding cost layers that curb margin upside. Associated-gas monetization remains an under-exploited lever; ONGC's Mumbai High flare-back project alone could contribute 0.4 Bcf/d once completed, reinforcing balanced oil-gas portfolios.

The India Oil and Gas Upstream Market Report is Segmented by Location of Deployment (Onshore and Offshore), Resource Type (Crude Oil and Natural Gas), Well Type (Conventional and Unconventional), and Service (Exploration, Development and Production, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).