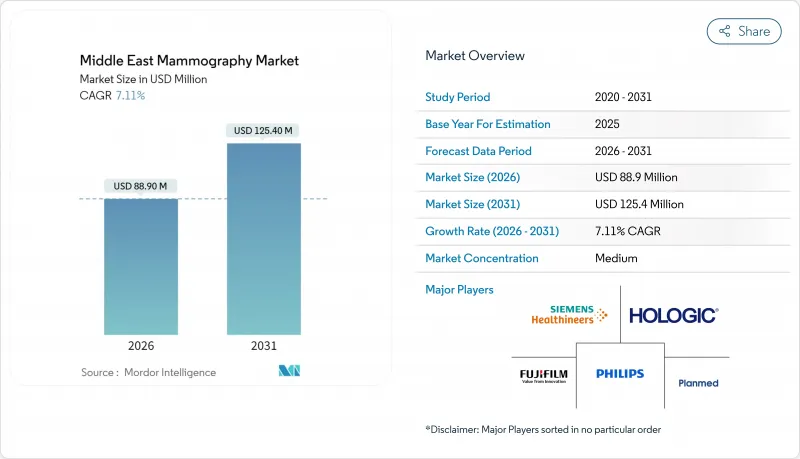

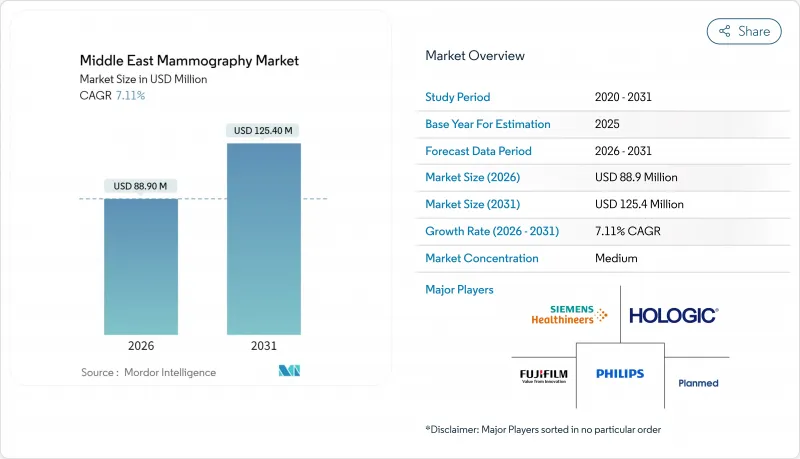

중동의 유방촬영술 시장의 규모는 2026년 8,890만 달러로 추정됩니다.

2025년 8,300만 달러에서 성장해 2031년에는 1억 2,540만 달러에 이를 전망으로, 2026년부터 2031년에 걸쳐 CAGR 7.11%로 확대될 것으로 예측되고 있습니다.

사우디아라비아와 아랍에미리트(UAE)의 정책 연동형 조달 사이클이 단기적인 수요를 지원하는 반면, 이집트에서는 공립 병원과 이동식 검진 프로그램을 통한 노력이 검진 기반의 확대를 촉진하고 있습니다. GCC 주요 시설의 입찰 사양에서는 토모신세시스 및 AI 대응 워크플로에 대한 예산 배분이 확대되고 있어, 벤더는 완전 통합형 플랫폼에 대한 선호를 강화할 전망입니다. 민간 진단 네트워크는 보험사와의 제휴와 고용주 부담에 의한 검진에 의해 도시에서 급속히 확대되고 있습니다. 이는 대기 시간이 긴 공공 시스템에서 환자 수를 재분배합니다. 여성 기술자의 부족이나 PACS 및 EHR 시스템간의 워크플로 단편화에 의한 용량의 병목 현상이 지속되고 있어, 후속 치료나 원격 방사선 진단에서 시설 간 제휴의 지연 요인이 되고 있습니다.

걸프 국가와 이집트의 발병 패턴은 더 젋은 스크리닝 대상층으로 이동하고 있으며, 이로 인해 첫 스크리닝을 40대 초반으로 앞당기는 가이드라인 변경이 가속화되고 있습니다. 사우디아라비아의 국가 보고에 따르면 주요 지역에서 진단 범위의 확대가 나타나고 있지만, 문화적 규범이나 접근 장벽에 의해 50세 미만 여성의 정기적인 영상 진단이 저해되는 지역에서는 여전히 발병 시기가 늦어지는 경우가 발생하고 있습니다. 이집트에서는 유방암 검진을 1차 의료 건강 진단이나 각 지방을 순회하는 이동 진료와 통합하여 검진 건수를 확대하는 한편, 연수나 기기 배치 수요가 정기적으로 급증하는 상황이 발생하고 있습니다. 아랍에미리트(UAE)에서는 40세부터 2년마다 유방 X선 검사를 의무화하는 제도에 따라 검진 건수가 증가하고, 단일 시프트 체제의 공공 시설에서는 대응 능력 부족 현상이 부각되고 있습니다. 튀르키예의 도시에서는 주말 검진이나 AI 지원에 의한 트리아지를 시험적으로 도입하여 제한된 자원에서도 고위험 환자의 우선 대응을 도모하고 있습니다. 한편, 신속한 후속 조치에 대한 환급은 의료 기관에 의해 여전히 변동을 보입니다.

도입 상황은 지역 내에서 양극화되고 있으며, GCC 국가의 시설과 고급 민영 체인에서는 3D 플랫폼이 표준화되는 한편, 이집트와 튀르키예 지방의 주요 지역에서는 아날로그에서 2D 디지털로의 단계적 업그레이드가 계속되고 있습니다. 사우디아라비아의 조달 가이드라인에서는 토모신세시스 대응 시스템과 병변 평가용 FDA 인가 AI 모듈이 우선시되어 하드웨어와 소프트웨어 모두에 대한 기준을 충족하는 벤더만이 계약 대상이 됩니다. 아부다비와 UAE 전역의 공인 스크리닝 센터는 토모신세시스 대응을 진행하고 있으며, 이로 인해 구식 디지털 장치의 조기 업데이트 사이클이 발생하고 있습니다. 카타르의 주요 병원에서는 고밀도 유방 집단에서의 특이도 향상을 위해 DBT(디지털 유방 토모신세시스)로의 업그레이드를 완료하여 원내 프로그램에서의 재검사율 저하가 보고되었습니다. 이집트에서는 지원 단체의 도입 계획에서 보험 적용 범위와 예산의 균형을 고려하여 소프트웨어에서 토모신세시스 기능을 활성화할 수 있는 2D 플랫폼이 우선시하고 있습니다. 한편, 튀르키예에서는 의료비 억제를 위해 사전 스크리닝을 통해 고밀도로 판정된 증례에 한정하여 DBT의 보험 적용을 실시하는 지불 정책이 도입되고 있습니다.

토모신세시스 플랫폼은 2D 디지털 시스템보다 고가이기 때문에 공공 구매자는 엔트리 레벨 구성과 단계적 업그레이드를 선택할 수 없습니다. 이집트의 지방 입찰에서는 도입 범위 확대를 위해 재생품이나 기본 디지털 옵션으로 가격이 설정되는 경우가 많아, 풀 DBT 장치의 구입이 제한되고 있습니다. 튀르키예에서는 형태에 관계없이 유방촬영술에 일률적인 보상이 지불되므로 의료 기관이 추가 민간 요금을 확보하지 않는 한 DBT 도입의 비즈니스 사례는 어려울 전망입니다. 사우디아라비아의 소규모 민간 시설에서는 2D 디지털 시스템을 선택하고 DBT 옵션은 필요할 때 추가 라이선스 및 서비스 비용을 정당화할 수 있는 단계에서 활성화하는 경우를 볼 수 있습니다. DBT 유지보수에는 검출기 교정, 다개년 주기의 관구 교환, AI 버전 업데이트 등이 포함되며, 이는 연간 예산에 지속적인 비용을 추가합니다. 쿠웨이트는 공급업체 금융을 통해 도입 비용을 장기간 분산할 수 있지만 이는 총 소유 비용(TCO)을 높이고 시설을 공급업체별 서비스 생태계에 묶어 놓습니다.

2025년 시점에서 디지털 시스템은 중동의 유방촬영술 시장의 59.68%를 차지하였으며 이는 사우디아라비아, UAE, 이집트 도시에서의 도입 실적을 반영하고 있습니다. 한편, AI 지원에 의한 체적 화상 처리의 입찰 및 인증 요건에 의해 토모신세시스가 추가 자본 지출을 견인할 것으로 예측됩니다. 중동의 유방촬영술 시장은 특히 인정 기준과 상호 운용성이 계약 획득을 좌우하는 GCC(걸프협력이사회) 회원국의 병원 내 고밀도 유방 스크리닝의 요구와 부합하는 저선량 및 AI 대응 플랫폼으로 이행하고 있습니다. 아날로그 장치는 전력 안정성과 운영 예산으로 업데이트가 제한되는 지역과 국경 지역에서 여전히 사용되고 있지만 부품을 입수하기 어려워지고 있습니다. 이동식 진료차량용 휴대용 디지털 시스템이나 산업 보건용 CESM 대응 구성 등 기타 제품 유형은 기동성과 고감도가 우선시되는 분야에서 확대되고 있습니다. 사우디아라비아와 UAE에서는 국가전략과 연동한 자본계획에서 DBT 대응과 통합화상관리를 중시하고 있으며, 이로써 서비스 네트워크가 충실하고 검증된 AI 모듈을 가진 벤더에 대한 지출을 촉진하고 있습니다.

공공 구매기관과 고급 민영 체인이 3D 기능에 주력하는 가운데, 토모신세시스가 성장의 대부분을 차지하고 있습니다. 이집트의 공공 조달은 직원 교육 및 PACS 업그레이드가 완료된 후 소프트웨어에서 토모신세시스 기능을 추가할 수 있는 디지털 장치를 선호하며, 향후 가동을 예상하면서 예산의 유연성을 유지하고 있습니다. 카타르와 쿠웨이트에서는 3차 의료시설에 3D 시스템을 도입하고, 1차 시설에는 2D 디지털 장치를 배치하여 환자의 중증도와 워크플로의 복잡성에 따라 기술을 선택하고 있습니다. 튀르키예에서는 포트폴리오의 폭과 현지 서비스 체제를 평가하는 멀티모달리티 입찰에서 유방촬영을 다른 영상 진단과 세트로 조달하는 경우가 많이 있습니다. GCC 지역의 격오지를 위한 이동 진료 프로그램은 견고한 휴대용 디지털 장치의 점유율을 확대하고 있지만, 내구성과 배터리 수명 요구사항이 현장 배포 비용을 밀어 올리고 있습니다.

Middle East mammography market size in 2026 is estimated at USD 88.9 Million, growing from 2025 value of USD 83 Million with 2031 projections showing USD 125.4 Million, growing at 7.11% CAGR over 2026-2031.

Policy-linked procurement cycles in Saudi Arabia and the United Arab Emirates are anchoring near-term demand, while Egypt's programmatic push through public hospitals and mobile initiatives is expanding the screening base. Tender specifications in core GCC facilities are shifting budgets toward tomosynthesis and AI-enabled workflows, which will reinforce vendor preferences for fully integrated platforms. Private diagnostic networks are scaling fast in urban hubs, enabled by insurer partnerships and employer-paid screening, which is redistributing volumes away from public systems with longer wait times. Capacity bottlenecks persist due to a shortage of female technologists and workflow fragmentation across PACS and EHR systems, which slows cross-site coordination for follow-up care and teleradiology reads.

Incidence patterns in the Gulf and Egypt have shifted toward younger screening cohorts, which is accelerating guideline changes that bring first-time screening forward to the early 40s. Saudi Arabia's national reporting highlights growing diagnostic reach in major regions, but late presentation still occurs where cultural norms and access barriers discourage routine imaging among women below 50. Egypt embedded breast-cancer screening into primary care checkups and mobile rotations in governorates, which is expanding volumes while creating periodic spikes in training and equipment deployment needs. In the UAE, mandated coverage for biennial mammography starting at age 40 has lifted screening volumes, which exposes capacity gaps in public facilities aligned to single-shift operations. Turkey's urban centers have piloted weekend screening and AI-supported triage to prioritize high-risk patients within resource limits, while reimbursement for rapid follow-up procedures remains uneven across institutions.

Adoption divides the region into two speed tiers as GCC facilities and premium private chains standardize on 3-D platforms, while Egypt and rural Turkey continue staged upgrades from analog to 2-D digital. Saudi procurement guidance now favors tomosynthesis-ready systems and FDA-cleared AI modules for lesion scoring, which narrows award pools to vendors meeting both hardware and software criteria. In Abu Dhabi and across the UAE, accredited screening centers are moving toward tomosynthesis compliance, which has triggered early replacement cycles for older digital units. Qatar's flagship hospitals completed DBT upgrades to improve specificity in dense-breast populations, reporting reduced recall rates within hospital programs. Egypt's donor-funded rollouts favor 2-D platforms with software-activatable tomosynthesis to balance coverage and budget, while Turkey's payer policies reimburse DBT selectively for high-density cases flagged by prior screens to control costs.

Tomosynthesis platforms carry a premium over 2-D digital systems, which pushes public buyers toward entry-tier configurations and staged upgrades. Egypt's provincial tenders often price for refurbished or basic digital rooms in order to expand footprint, which constrains purchases of fully featured DBT equipment. In Turkey, fixed-fee reimbursement for mammography regardless of modality dampens the business case for DBT unless providers secure supplemental private fees. Smaller private facilities in Saudi Arabia opt for 2-D digital systems with dormant DBT options that can be activated later when volumes justify additional licensing and service costs. Maintenance for DBT includes detector calibration, tube replacement on multi-year cycles, and AI version updates that add recurring costs to annual budgets. In Kuwait, vendor financing can spread acquisition costs over longer durations, but it raises total cost of ownership and ties centers to proprietary service ecosystems.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Digital systems held 59.68% of the Middle East mammography market in 2025, reflecting the installed base across Saudi Arabia, the UAE, and urban Egypt, while tomosynthesis is projected to lead incremental capital spend due to tender and accreditation requirements for volumetric imaging with AI support. The Middle East mammography market is moving toward lower dose, AI-ready platforms that align with dense-breast screening needs, especially in GCC hospitals where accreditation and interoperability criteria shape awards. Analog units persist in specific rural and border locations, largely where power stability and operating budgets constrain upgrades, but parts availability is tightening. Other product types, such as portable digital systems for mobile vans and CESM-enabled configurations for occupational health, are expanding where mobility or high sensitivity is prioritized. In Saudi Arabia and the UAE, capital programs tied to national strategies emphasize DBT readiness and integrated image management, which directs spending toward vendors with strong service networks and validated AI modules.

Tomosynthesis accounts for most of the incremental growth as public buyers and premium private chains converge on 3-D capability. Egypt's public procurements favor digital units that can unlock tomosynthesis via software when staff training and PACS upgrades are completed, preserving budget flexibility while planning for future activation. Qatar and Kuwait deploy 3-D systems in tertiary centers while routing 2-D digital to primary sites, matching technology to patient-acuity and workflow complexity. Turkey often bundles mammography with other imaging in multi-modality tenders that reward portfolio breadth and local service presence. In mobile programs serving remote GCC regions, ruggedized portable digital units are gaining share, although durability and battery-life requirements add costs to field deployments.

The Middle East Mammography Market Report is Segmented by Product Type (Digital Systems, Analog Systems, Breast Tomosynthesis (3-D), and Other Product Types), End User (Hospitals, Specialty Clinics, Diagnostic Centers, and Emergency Medical Services), and Geography (Saudi Arabia, United Arab Emirates, Egypt, Turkey, Qatar, Kuwait, and Rest of Middle East). The Market Forecasts are Provided in Terms of Value (USD).