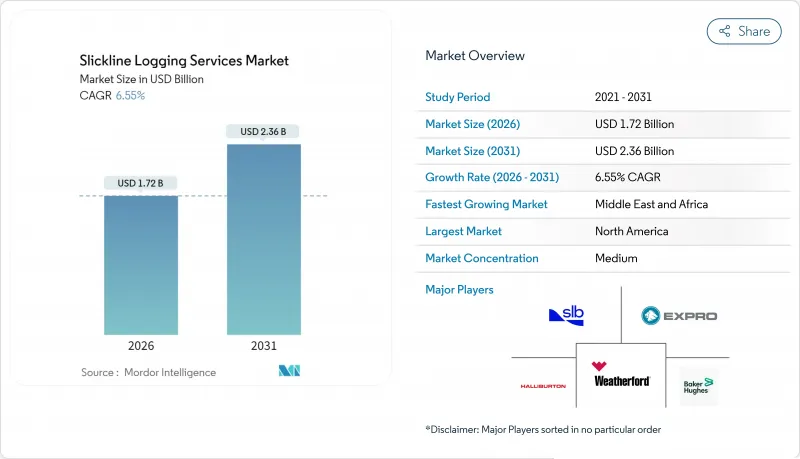

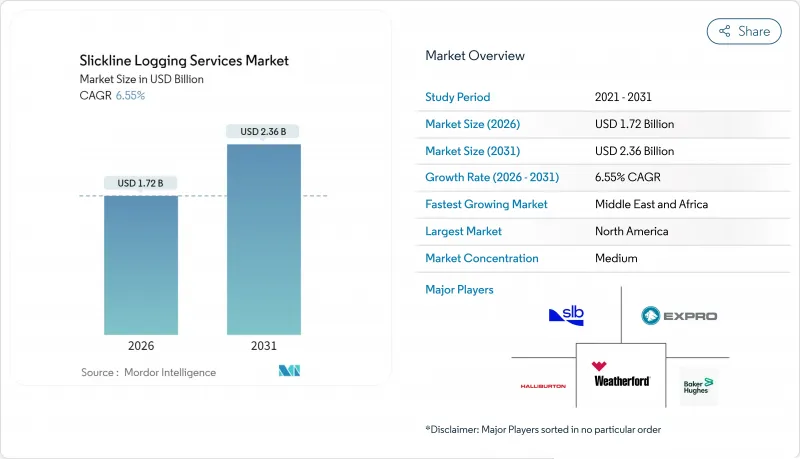

슬릭라인 로깅 서비스 시장은 2025년에 16억 1,000만 달러로 평가되었으며, 2026년 17억 2,000만 달러에서 2031년까지 23억 6,000만 달러에 이를 것으로 예측됩니다.

예측기간(2026-2031년)의 CAGR은 6.55%로 예상됩니다.

수요는 기존 갱정 생산 최적화에 대한 운영자의 지향, 심해 및 초심해 프로젝트의 꾸준한 증가, 생산 정지 없이 실시간 갱내 진단을 가능하게 하는 디지털 슬릭라인 플랫폼의 급속한 도입에 의해 추진되고 있습니다. 기타 촉진요인으로는 노후화된 갱정의 백로그 증가, 국영석유회사의 통합서비스 입찰, 저침습 로깅을 필요로 하는 신흥 탄소 포집 파일럿 프로그램 등을 들 수 있습니다. 인공지능과 자율운영의 지속적인 진보로 기존의 기계적 리노베이션 작업은 자산 수명을 연장하고 채굴 비용을 절감하는 데이터 기반 개입으로 변모하고 있습니다.

2025년 심해 드릴링 리그의 가동률은 82%를 유지하였고 일당 단가를 견조하게 유지함과 동시에 극한의 압력 및 온도 조건 하에서의 견고한 슬릭라인 개입 수요를 뒷받침했습니다. 우드사이드사의 트리온 개발 프로젝트(수심 2,500m의 18개 갱정)와 같은 이슈는 지층 평가와 갱정 건전성 감시의 지속적인 필요성을 촉진하는 복잡성을 보여줍니다. 국영 석유회사는 운영 시너지 획득 및 리그 이동 감소를 목적으로 여러 연간 통합 드릴링 계약에 슬릭라인 서비스를 통합하고 있습니다. 실시간 슬릭라인 로깅은 AI 대응 드릴링 플랫폼과 통합되어 갱정 제어 유지 및 저류층 접촉 최적화를 실현하고 있습니다. 원격 해역에서의 장기 캠페인은 추가적인 동원 없이 기계 작업, 로깅, 청소 작업을 완료하는 다기능 슬릭라인 스트링의 가치를 높이고 있습니다.

세계의 가동 중인 26만 곳의 갱정 가운데 약 3분의 2가 2030년까지 가동 기간 10년을 경과할 전망이며, 오퍼레이터가 갱정당 평균 10%의 생산량 향상을 목표로 하는 가운데 세계 개입 지출은 580억 달러에 달할 것으로 예측됩니다. 슬릭라인은 단순한 기계적 회수로부터 진화해, 고화질 카메라 또는 전자 게이지를 탑재하는 플랫폼으로 발전하여 리그 기반 리노베이션 작업을 대체하는 저비용 옵션을 제공합니다. 북해의 오퍼레이터는 슬릭라인을 통한 스트래들 가스 리프트 작동을 시험적으로 운용하고 있으며, 이를 통해 심해에서의 업그레이드 비용을 반으로 줄일 수 있습니다. 기타 응용 사례로는 로봇에 의한 스크린 회수나 화학약품의 투입 등을 들 수 있으며, 이들 모두 신규 굴착보다 표적형 개입의 경제적 합리성을 강화하는 사례입니다.

미국의 독립 기업은 서비스 비용이 하락했음에도 불구하고 2024년 자본 계획을 617억-654억 달러로 줄였습니다. 이는 가격 변동이 임의의 개입을 연기시킬 가능성을 부각시킵니다. 대기업은 230억-250억 달러라는 엄격한 범위 내에서 지출을 계속하고 있으며, 신중한 자금 배분 자세를 강화하고 있습니다. 슬릭라인 작업은 종종 선택적이므로 WTI가 손익 분기점 아래로 떨어지면 운영자는 우선순위가 낮은 작업을 연기합니다. 엔지니어링 및 설치 서비스의 인플레이션은 개입 예산에 추가 압력을 가하고 있습니다. 공급자는 현장에서의 작업 시간이 아니라 증분 회수 배럴 수에 지불을 연동시키는 성과 연동형 가격 설정이나 복수 갱정 패키지로 대응하고 있습니다.

케이싱 홀 작업은 2025년 슬릭라인 로깅 서비스 시장 점유율의 59.12%를 차지하였고 2026년부터 2031년에 걸쳐 6.88%라는 가장 높은 CAGR을 나타낼 것으로 예측되고 있습니다. 이는 운영자가 신규 드릴링보다 기존 갱정에서 부가가치를 창출하는 것을 선호함을 나타냅니다. 이 이점은 노후화 갱정의 증가로 인해 발생합니다. 2030년까지 3분의 2 이상이 가동 기간 10년을 넘을 전망이며, 관을 유지하면서 실시 가능한 기계적 수리, 생산 프로파일링, 시멘트 본드 평가에 대한 수요가 높아지고 있습니다. 디지털 슬릭라인 플랫폼은 압력, 온도, 유량 데이터 지표를 실시간으로 전송합니다. 이를 통해 단일 작업으로 로깅과 기계적 작업을 통합하고 실시간 진단을 가능하게 하며 비생산시간을 줄일 수 있습니다. 따라서 케이싱 홀 작업과 관련된 슬릭라인 로깅 서비스 시장의 규모는 작업 빈도 상승과 도구 복잡성의 이중 혜택을 누리고 있습니다. 인공지능은 최적의 툴 스트링 구성을 즉시 제안하고 증분 회수 배럴량을 극대화합니다.

오픈 홀 작업은 활동 규모가 작지만, 초기 갱정 구축 시나 저류층 접촉점의 정밀한 평가가 필수적인 상황에서 지층 평가의 요점이 됩니다. 이러한 작업은 암반에 직접 접근해야 하지만 시추 예산의 제약과 케이싱 시공 후 재작업 빈도 감소로 인해 수익성이 제한적입니다. 자율형 슬릭라인 트랙터의 진보에 의해 오퍼레이터는 복수 스트링을 통해 작업을 수행하고 좁은 프로파일을 통한 브릿지 플러그나 스트래들 패커의 전개가 가능하게 되어 케이싱 시공 후의 서비스 범위가 확대하고 있습니다. 셰일 플레이 재파쇄 계획은 수요를 더욱 확대하고 있습니다. 슬릭라인으로 운반되는 격리 툴은 성숙한 갱정에서 추정 최종 회수량을 50% 이상 증가시킬 수 있는 표적 자극이 가능하기 때문입니다. 이러한 요인들이 더하여 케이싱 홀 작업은 수익 확대의 주요 원동력으로 자리매김하는 한편, 오픈 홀 서비스는 보다 광범위한 슬릭라인 포트폴리오를 보완하는 고부가가치 틈새 용도를 계속 제공합니다.

북미는 2025년에도 수익 점유율 38.55%를 유지하였습니다. 이는 엄청난 노후화 갱정 수와 활발한 재파쇄 프로그램에 의해 지원됩니다. 이글퍼드 및 버켄 지역에서는 슬릭라인을 활용한 재파쇄 시 EUR(추정 최종 회수량)이 50% 이상 증가하여 본 기술의 경제적 유효성이 입증되었습니다. 페르미안 분지에서는 다운타임 단축과 메탄 배출량 저감을 목적으로 AI 강화형 디지털 슬릭라인 유닛의 도입이 확대되고 있습니다. 캐나다의 대서양 해안과 멕시코의 트리온 심해 프로젝트는 셰일 이외의 지역 수익원 확대가 예상됩니다.

중동 및 아프리카는 7,300억 달러 규모의 업스트림 투자와 발전에서 액체 연료 대체를 목표로 하는 가스 우선 전략에 의해 2031년까지 연평균 복합 성장률(CAGR) 7.05%로 확대될 것으로 예측되고 있습니다. 아부다비 국영 석유회사(ADNOC)와 사우디 아람코는 슬릭라인 서비스와 굴착, 갱정 완성, 탄소 포집 모니터링을 통합한 다개년 계약의 포괄 입찰을 실시했습니다. 나이지리아의 초심해 발견이나 나미비아의 프론티어 지역의 발견에는 고압 및 고온 대응 슬릭라인 공구열이 필요하여 전문 서비스 플릿에 기회가 태어나고 있습니다.

아시아태평양과 유럽은 균형잡힌 성장을 보이고 있습니다. 중국과 인도는 남중국해 및 벵골만에서 더 깊은 시추를 진행하고 있으며, 고압 고온 저류층에서는 실시간 텔레메트리용으로 광섬유 슬릭라인이 필요합니다. 유럽의 북해에서는 운영자가 리그리스 슬릭라인 패키지로 작업 비용 50% 절감을 목표로 하는 가운데 안정적인 개입 작업량이 유지되고 있습니다. 남미는 브라질의 프리솔트층 개발과 아르헨티나의 바카 무에르타 혈암층 개발에 의해 뒷받침되고 있으며, 모두 3-5년간의 다중 서비스 제공을 확보하는 통합 서비스 모델을 도입하고 있습니다.

The Slickline Logging Services Market was valued at USD 1.61 billion in 2025 and estimated to grow from USD 1.72 billion in 2026 to reach USD 2.36 billion by 2031, at a CAGR of 6.55% during the forecast period (2026-2031).

Demand is being propelled by operators' preference for production optimisation on existing wells, the steady rise in deep- and ultra-deepwater projects, and the rapid deployment of digital slickline platforms that enable real-time downhole diagnostics without halting production. Other supportive factors include the growing backlog of ageing wells, national oil companies' integrated service tenders, and emerging carbon-capture pilot programmes that require low-invasion logging. Continued advancements in artificial intelligence and autonomous operations are transforming conventional mechanical workovers into data-rich interventions that extend asset life and reduce lifting costs.

Deepwater rig utilisation stood at 82% in 2025, keeping day-rates firm and sustaining demand for robust slickline intervention under extreme pressure and temperature conditions. Projects such as Woodside's Trion development-18 wells in 2,500 m water-illustrate the complexity that fuels a continual need for formation evaluation and well-integrity surveillance. National oil companies are locking slickline services into multi-year integrated drilling contracts to capture operational synergies and reduce rig moves. Real-time slickline diagnostics now integrate with AI-enabled drilling platforms to maintain well control and optimize reservoir contact. Longer campaign durations in remote waters heighten the value of multi-function slickline strings that complete mechanical, logging, and clean-out tasks without additional mobilisation.

Roughly two-thirds of the world's 260,000 active wells will be more than 10 years old by 2030, pushing global intervention spend toward USD 58 billion as operators chase a 10% average output uplift per well. Slickline has evolved from simple mechanical retrieval into a platform for high-definition cameras and electronic gauges, offering a low-cost alternative to rig-based workovers. North Sea operators are piloting slickline-mediated straddle gas-lift activation that cuts deepwater workover costs by half. Additional applications include robotic screen retrieval and chemical deployment, all of which strengthen the economic case for targeted intervention over fresh drilling.

US independents trimmed their 2024 capital plans to USD 61.7-65.4 billion, despite lower service costs, highlighting how price swings can postpone discretionary interventions. Major companies continue to spend within a tight USD 23-25 billion band, reinforcing cautious cash allocation. Because slickline work is often elective, operators defer lower-priority jobs when WTI falls below breakeven thresholds. Inflation in engineering and installation services adds further pressure to intervention budgets. Providers respond with outcome-based pricing and multi-well packages that tie payment to incremental barrels recovered rather than time on-site.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cased hole interventions commanded 59.12% of slickline logging services market share in 2025 and are forecast to register the fastest 6.88% CAGR from 2026-2031, underscoring operators' preference to extract additional value from existing wellbores rather than drill new ones. This dominance is rooted in the growing inventory of ageing wells-more than two-thirds will surpass 10 years of service by 2030-which keeps demand high for mechanical repairs, production profiling, and cement-bond evaluation that can be executed without pulling tubing. Digital slickline platforms stream live pressure, temperature, and flow data to the surface, enabling real-time diagnostics and reducing non-productive time by combining logging and mechanical tasks in a single run. The slickline logging services market size associated with these cased operations, therefore, benefits from both higher job frequency and expanding tool complexity, as artificial intelligence recommends optimal tool-string configurations on the fly to maximize incremental barrels recovered.

Open hole work represents the smaller share of activity, yet remains essential for formation evaluation during initial well construction or when precise reservoir contact is critical. While these jobs require direct rock exposure, their revenue potential is limited by drilling budgets and fewer repeat visits once a well is cased. Advancements in autonomous slickline tractors now enable operators to navigate multi-string completions and deploy bridge plugs or straddle packers through restrictive profiles, thereby widening the scope of cased services. Re-fracturing programs in shale plays further amplify demand, as slickline-conveyed isolation tools enable targeted stimulation that can increase estimated ultimate recovery by 50% or more in a mature well. Together, these factors position cased hole operations as the primary engine of revenue expansion, while open hole services continue to deliver high-value niche applications that complement the broader slickline portfolio.

The Slickline Logging Services Market Report is Segmented by Hole Type (Open Hole and Cased Hole), Location of Deployment (Onshore and Offshore), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

North America retained a 38.55% revenue share in 2025, driven by a vast ageing well stock and prolific re-fracturing programs. The Eagle Ford and Bakken plays recorded EUR gains exceeding 50% when slickline-enabled re-fracs were executed, confirming the technique's economic relevance. AI-augmented digital slickline units are increasingly deployed in the Permian Basin to cut downtime and lower methane intensity. Canada's Atlantic offshore and Mexico's Trion deepwater project are set to widen regional revenue streams beyond shale.

The Middle East & Africa is forecast to grow at a 7.05% CAGR to 2031, supported by USD 730 billion of upstream spending and gas-directed strategies aimed at substituting liquid fuels in power generation. ADNOC and Saudi Aramco are issuing multi-year, integrated tenders that bundle slickline services with drilling, completion, and carbon capture monitoring. Nigeria's ultra-deepwater discoveries and Namibia's frontier finds require high-pressure, high-temperature slickline tool strings, creating opportunities for specialized service fleets.

Asia-Pacific and Europe provide balanced growth. China and India are drilling deeper in the South China Sea and Bay of Bengal, where HPHT reservoirs need fibre-optic slickline for live telemetry. Europe's North Sea continues to generate steady intervention volumes as operators target 50% work-over cost cuts through rigless slickline packages. South America remains buoyed by Brazil's pre-salt developments and Argentina's Vaca Muerta shale, both adopting integrated service models that secure multi-service lineups for three-to-five-year windows.