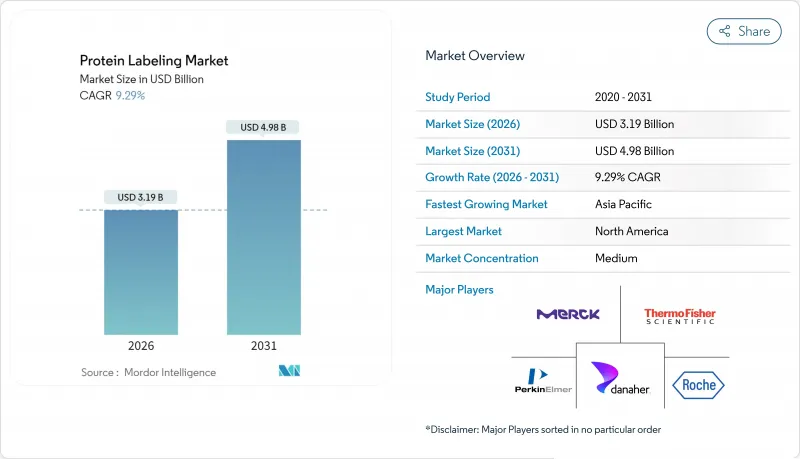

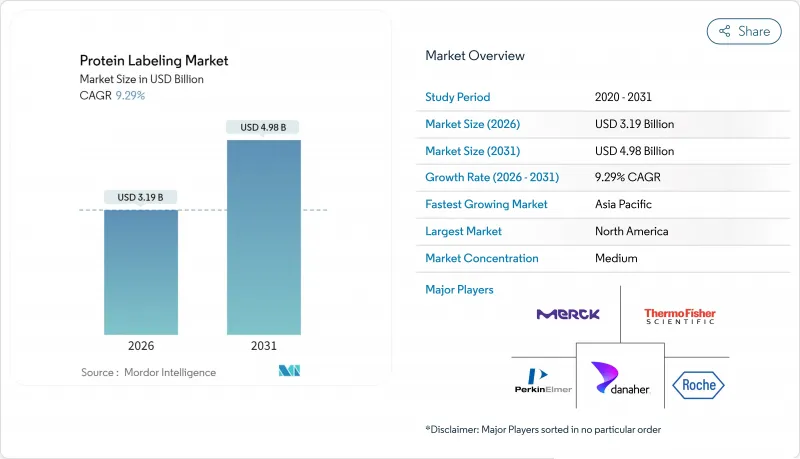

단백질 표지 시장은 2025년에 29억 2,000만 달러로 평가되었고, 2026년 31억 9,000만 달러에서 2031년까지 49억 8,000만 달러에 이를 것으로 보입니다. 예측기간(2026-2031년)의 CAGR은 9.29%를 나타낼 전망입니다.

단백질 구조에 미치는 영향을 최소화하면서 특정 부위에 표지를 부착할 수 있는 기술적 돌파구가 수요를 주도하고 있으며, 이는 현대의 고급 프로테오믹스, 생세포 이미징 및 생물치료제 워크플로우에 필수적인 요건입니다. 구조 예측을 위한 인공지능 도구 활용 확대, 항체-약물 접합체(ADC) 파이프라인 증가, 복잡한 생물접합 작업의 전문 CDMO(계약 개발 제조 기관)로의 이관은 상업적 기회를 공동으로 확대하고 있습니다. 동시에 자본 집약적 분석 플랫폼과 방사성 표지 접합체 관련 진화하는 규제는 여전히 실질적 장애물로 남아 있습니다. 기존 업체들이 독점적 화학 기술, 통합 서비스 모델, 의약품 개발사와의 전략적 제휴를 통해 차별화를 모색함에 따라 경쟁 강도는 높아지고 있습니다.

고해상도 질량 분석법과 AI 기반 모델링의 발전으로 단백질 특성 분석 연구의 양과 깊이가 급격히 증가했습니다. 2024년 출시된 ESM-3 및 AlphaFold 3은 구조 예측 정확도를 향상시켜 연구자들이 선택적 표지 및 생산을 위한 접근 가능한 잔기들을 정확히 찾아낼 수 있게 했습니다. 미국과 유럽 전역의 자금 지원 프로그램은 이제 정량화 및 공간 매핑을 위한 강력한 표지 화학에 의존하는 다중 오믹스 파이프라인을 우선시합니다. 이러한 역학은 차세대 프로브에 대한 프리미엄 가격을 유지하고 학술 핵심 연구소 및 중개의학 센터에서 고처리량 워크플로의 더 광범위한 채택을 예고합니다.

현재 임상시험 중인 신약의 약 40%가 역사적으로 치료 불가능한 단백질에 집중되면서 균일하고 부위 특이적인 표지 기술의 중요성이 부각되고 있습니다. 현재 360건 이상의 임상 연구가 진행 중인 항체-약물 접합체(ADC) 파이프라인은 효능 확보를 위해 정밀한 링커-페이로드 비율이 필요합니다. 표적 단백질 분해 플랫폼 역시 실시간 단백질 분해를 모니터링하는 생세포 표지 기술에 의존합니다. 이러한 활용 사례는 시약, 장비 및 맞춤형 접합 서비스 전반에 걸쳐 해결 가능한 수요를 확대합니다.

25kDa 이상의 대형 형광 표지자는 시험 단백질의 42%에서 세포 내 국소화를 변경했으며, 나노바디 접합체는 실험실 간 결합 효율에서 38%의 변동성을 보였습니다. 이러한 불일치는 특히 규제 환경에서 검증 요구 사항을 높이고, 프로젝트 일정을 연장하며, 소모품 사용량을 증가시킵니다.

2025년 단백질 표지 시장 매출의 70.62%를 차지한 시약 및 키트는 발견, 진단, 제조 전반의 일상적 워크플로우에서 핵심적 역할을 강조합니다. 즉시 사용 가능한 화학 물질은 프로토콜 표준화를 단순화하고 재현성을 지원하여 신기술 등장에도 수요가 탄력적으로 유지됩니다. 염료 밝기와 클릭 준비형 핸들의 지속적인 개선은 점진적 가격 결정력을 유지하고 반복 구매를 유도합니다.

그러나 서비스 부문은 10.31%의 연평균 복합 성장률(CAGR)로 전체 성장률을 앞지르고 있습니다. 이러한 급증은 항체-약물 접합체, 표적 분해 프로브, 생체 동물 영상제 등 내부 역량을 초과하는 기술적 복잡성의 증가를 반영합니다. CDMO 업체들은 대규모 페이로드 접합 및 충전-완성 작업을 수용하기 위해 론자의 2024년 비스프 확장 프로젝트와 같은 전용 1,000-2,000리터 규모의 설비를 추가하고 있습니다. 파이프라인 스폰서들이 신속하고 GMP 준수 솔루션을 추구함에 따라 아웃소싱 프로젝트의 단백질 표지 시장 규모는 꾸준히 확대될 전망입니다.

면역학적 기법은 ELISA, 웨스턴 블롯, 면역조직화학 분야의 수십 년간 최적화 성과를 바탕으로 2025년 34.05% 점유율로 단백질 표지 시장의 최대 비중을 유지할 전망입니다. 고처리량 및 임상 검증 프로토콜은 바이오마커 검증, 배치 출시 테스트, 일상적 병리학 분야에서 지속적인 중요성을 보장합니다.

그러나 세포 기반 분석법은 종양학, 신경학 및 재생 의학 분야에서 생리학적으로 관련성 높은 결과 측정을 연구자들이 우선시함에 따라 10.96%의 연평균 복합 성장률(CAGR)로 가장 빠른 진전을 기록하고 있습니다. 써모 피셔의 형광 프로브 포트폴리오는 수용체 활성화, 운송 및 복합체 조립을 실시간으로 모니터링할 수 있게 합니다. 자동화 이미징 및 고내용 분석이 스크리닝 실험실에 확산됨에 따라 동적 생세포 플랫폼이 차지하는 단백질 표지 시장 점유율은 확대될 전망입니다.

북미는 강력한 NIH 자금 지원, 밀집된 바이오제약 클러스터, 차세대 표지 기술의 조기 도입에 힘입어 2025년 매출의 37.35%를 차지했습니다. MIT의 CuRVE 기술 혁신은 하루에 수천만 개의 세포를 표지할 수 있어 파괴적 방법론 분야의 지역적 리더십을 보여줍니다. 항체-약물 접합체(ADC) 및 방사성면역접합체(RIA)에 대한 FDA 승인의 높은 빈도는 상업적 모멘텀을 더욱 공고히 합니다.

유럽은 Horizon Europe 보조금과 독일, 영국, 프랑스의 강력한 바이오제조 허브에 힘입어 2위를 차지했습니다. Sartorius의 Polyplus 인수는 대륙의 벡터 생산 역량을 확장시켜 바이러스 외피 단백질에 대한 고급 태깅 기술을 필요로 합니다. 규제 조화는 진전 중이지만, 방사성 동위원소 취급 방식의 차이로 시장 진입 비용은 여전히 높습니다.

아시아태평양 지역은 11.40%의 연평균 성장률(CAGR)로 가장 빠르게 성장하는 시장입니다. 우시 바이오로직스(WuXi Biologics)와 같은 중국 CDMO 기업들은 ‘우시바디(WuXiBody)’ 브랜드의 접합체 형식과 관련 링커 화학물질에 대한 활발한 수요를 보고하고 있습니다. 중국의 제14차 5개년 계획과 인도의 BIRAC 이니셔티브를 포함한 국가 산업 정책은 자본을 단백질체학 인프라로 유입시키고 있으나, 고급 MS 플랫폼에 대한 접근성은 여전히 불균등합니다. 삼성바이오로직스의 지원을 받는 한국의 항체-약물 접합체 시설의 급속한 확장은 지역적 부상을 더욱 공고히 합니다.

The protein labelling market was valued at USD 2.92 billion in 2025 and estimated to grow from USD 3.19 billion in 2026 to reach USD 4.98 billion by 2031, at a CAGR of 9.29% during the forecast period (2026-2031).

Demand is propelled by breakthroughs that allow site-specific tags with minimal impact on protein conformation, an essential requirement for today's advanced proteomics, live-cell imaging and biotherapeutic workflows. Widening use of artificial-intelligence tools for structure prediction, a growing pipeline of antibody-drug conjugates and the migration of complex bioconjugation tasks to specialist CDMOs jointly broaden commercial opportunities. At the same time, capital-intensive analytical platforms and evolving regulations around radio-labelled conjugates remain practical hurdles. Competitive intensity is rising as incumbents look to differentiate via proprietary chemistries, integrated service models and strategic alliances with drug developers.

Advances in high-resolution mass spectrometry and AI-driven modelling have sharply raised the volume and depth of protein characterisation studies. The release of ESM-3 and AlphaFold 3 in 2024 improved structure-prediction accuracy, allowing researchers to pinpoint accessible residues for selective tagging hai-production. Funding programs across the United States and Europe now prioritise multi-omics pipelines that depend on robust labelling chemistries for quantitation and spatial mapping. These dynamics sustain premium pricing for next-generation probes and herald broader uptake of high-throughput workflows in academic cores and translational-medicine centres.

Roughly 40% of investigational drugs now focus on historically undruggable proteins, elevating the role of homogeneous, site-specific labelling. Antibody-drug conjugate pipelines, currently exceeding 360 clinical studies, require precise linker-payload ratios for efficacy. Targeted protein degradation platforms similarly depend on live-cell tags that monitor real-time proteolysis. These use cases expand addressable demand across reagents, instrumentation and custom-conjugation services.

Large fluorescent tags above 25 kDa altered sub-cellular localisation in 42% of tested proteins, and nanobody conjugates showed 38% variability in binding efficiency across labs. Such inconsistencies raise validation requirements, extend project timelines and increase consumable usage, particularly in regulated environments.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Reagents and kits accounted for 70.62% of protein labelling market revenues in 2025, underscoring their essential role in day-to-day workflows across discovery, diagnostics, and manufacturing. Ready-to-use chemistries simplify protocol standardisation and support reproducibility, keeping demand resilient even as new techniques emerge. Continuous improvements in dye brightness and click-ready handles sustain incremental pricing power and entice repeat purchases.

The services segment, however, is outpacing headline growth at a 10.31% CAGR. This surge reflects the escalating technical complexity of antibody-drug conjugation, targeted degradation probes and live-animal imaging agents that exceed many in-house capabilities. CDMOs are adding dedicated 1,000-2,000 L suites, such as Lonza's 2024 expansion in Visp, to accommodate large-scale payload conjugation and fill-finish tasks. The protein labelling market size for outsourced projects is projected to expand steadily as pipeline sponsors seek rapid, GMP-compliant solutions.

Immunological techniques remained the largest slice of the protein labelling market with a 34.05% share in 2025, benefiting from decades of optimisation in ELISA, western blot and immunohistochemistry. High throughput and clinically validated protocols ensure enduring relevance in biomarker verification, lot-release testing and routine pathology.

Cell-based assays, however, record the most rapid advance at 10.96% CAGR as researchers prioritise physiologically relevant readouts in oncology, neurology and regenerative medicine. Fluorescent-probe portfolios from Thermo Fisher enable real-time monitoring of receptor activation, trafficking and complex assembly. The protein labelling market share captured by dynamic live-cell platforms is set to widen as automated imaging and high-content analytics permeate screening laboratories.

The Protein Labelling Market is Segmented by Product (Reagents and Kits, Services and Other Products), Application (Immunological Techniques, Cell-Based Assays and More), Labeling Method (In-Vitro Labelling and In-Vivo Labelling), End User (Pharmaceutical and Biotechnology Companies, Contract Research and Manufacturing Organisations and More) and Geography. The Market and Forecasts are Provided in Terms of Value (USD).

North America generated 37.35% of 2025 revenues, supported by robust NIH funding, a dense biopharma cluster and early adoption of next-generation labelling technologies. MIT's CuRVE breakthrough, capable of labelling tens of millions of cells in a single day, exemplifies regional leadership in disruptive methodology. A high cadence of FDA approvals for ADCs and radio-immunoconjugates further anchors commercial momentum.

Europe ranks second, buoyed by Horizon Europe grants and strong biomanufacturing corridors in Germany, the United Kingdom and France. Sartorius' acquisition of Polyplus expanded the continent's vector-production capabilities, necessitating advanced tagging for viral envelope proteins. Regulatory harmonisation is progressing, yet divergent approaches to radio-isotope handling keep market entry costs elevated.

Asia-Pacific is the fastest-growing arena, advancing at an 11.40% CAGR. Chinese CDMOs such as WuXi Biologics report vibrant demand for conjugation formats branded under WuXiBody and associated linker chemistries. National industrial policies, including China's 14th Five-Year Plan and India's BIRAC initiatives, funnel capital into proteomic infrastructure, although uneven access to high-end MS platforms persists. South Korea's rapid scale-up of antibody-drug conjugate facilities, backed by Samsung Biologics, further cements regional ascent.