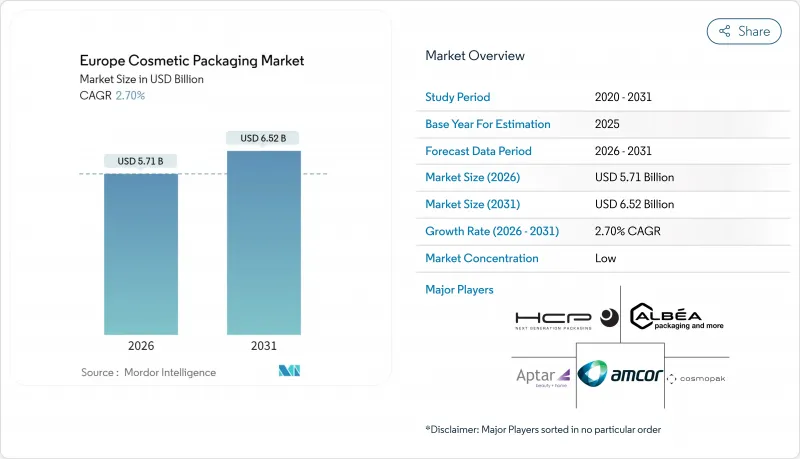

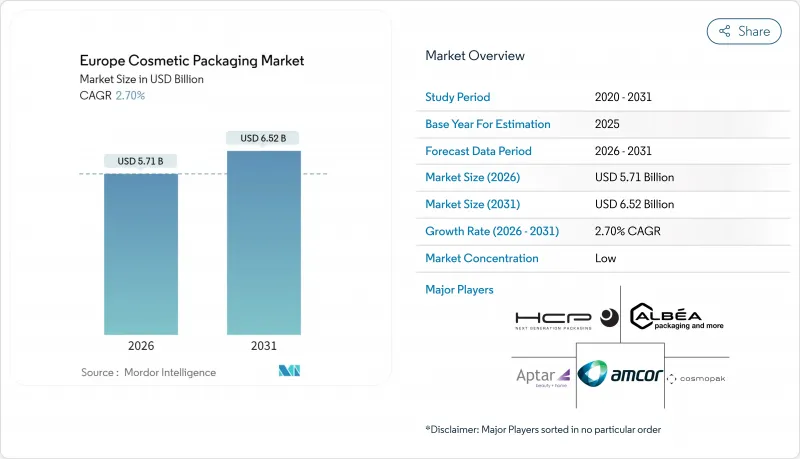

유럽의 화장품 포장 시장 규모는 2026년에 57억 1,000만 달러로 평가되었습니다.

이는 2025년 55억 6,000만 달러에서, 2031년에는 65억 2,000만 달러에 달할 것으로 예측되고 있습니다. 2026-2031년에 걸쳐 CAGR 2.7%로 성장할 전망입니다.

상당한 매출 성장은 EU 포장 및 포장 폐기물 규정이 재활용 가능한 포맷으로의 전환을 강제하고, 최소 재활용 함량 기준을 도입하며, 단일 소재 및 리필 가능 솔루션으로의 전환을 가속화함에 따라 광범위한 구조적 변화를 가리고 있습니다. 수요 패턴은 또한 전자상거래 주문 처리 요구사항, 미니멀리즘 미학을 선호하는 젊은 소비자층, 제품 진위 확인 및 행동 데이터 수집을 위한 스마트 기능의 급속한 통합에 의해 형성됩니다. 규모의 경제가 소재 혁신, AI 기반 디자인 도구, 수명 종료 수거 인프라 자금 조달에 핵심이 되면서 경쟁 강도가 높아지고 있습니다. 재활용 PET 공급망 병목 현상과 바이오 기반 폴리머의 비용 프리미엄은 전망을 다소 어둡게 하지만, 동시에 수직 통합형 또는 전문 기업들에게 백스페이스 기회를 창출합니다.

럭셔리 미학과 탄소 발자국 감소를 입증하는 브랜드들이 늘어나면서 주요 유럽 시장에서 리필 솔루션 판매가 62% 증가했습니다. 럼슨(Lumson)의 XTAG 에어리스 시스템은 프리미엄 외관과 촉감을 유지하면서 기존 포맷 대비 38%의 CO2 감축 효과를 제공합니다. 클라란스(Clarins)는 알베아(Albea)와 함께 첫 리필용 용기를 출시하며 프리미엄 브랜드 사이에서 주류 채택이 시작되었음을 알렸습니다. 소비자 인식도 긍정적입니다. 응답자의 64%가 리필 제품을 타협적 해결책이 아닌 진정한 친환경 솔루션으로 인식했습니다. FASTEN BV의 재활용 폴리프로필렌 용기는 적층형 인서트를 통해 재료 사용량을 70% 절감하는 등 기술적 혁신이 이루어지고 있습니다. 리필 모델은 반복적 수익 창출과 직접적 상호작용 빈도 증가를 통해 브랜드 충성도 강화 효과도 제공합니다.

2024년 12월 최종 채택된 포장 및 포장 폐기물 규정은 2030년까지 100% 재활용 가능 포장재와 최소 재활용 함량 의무화를 도입합니다. 화장품 유럽 협회는 통일된 규정의 비용 절감 효과를 인정하면서도 시각적 차별화에 영향을 미칠 수 있는 창의적 제약에 대한 우려를 표명했습니다. 소형 화장품 용기 금지는 진열대 존재감을 재구성하는 재설계를 촉진합니다. 이행 비용은 대형 업체에 유리하여 쿼드팩-텍센 합병과 같은 통합을 촉진합니다. 조화된 생산자 책임 확대 제도는 규제 분열을 줄이지만, 상이한 비EU 규정을 관리하는 세계의 브랜드에게는 복잡성을 가중시킵니다.

원유 가격 상승에도 불구하고 폴리락틱산과 바이오 PET 가격은 화석 기반 동등 제품보다 30-50% 높아, 규모의 경제를 활용하지 못하는 소규모 브랜드를 시장에서 배제합니다. 아시아 생산 능력의 급속한 확대로 유럽의 세계의 바이오 폴리머 생산 점유율은 13%에서 10%로 하락했습니다. 설탕 및 전분 작물이 식량 시장과 경쟁함에 따라 원료 제약이 변동성을 가중시킵니다. 바이오 기반 등급은 때때로 차단 코팅이나 안정제가 필요하여 재활용 흐름을 복잡하게 만들며, 이에 따른 재제조 비용도 증가합니다. 결과적으로 많은 변환업체들은 더 낮은 비용으로 PPWR 의무를 달성하기 위해 바이오 원료보다 재활용 함량 전략을 우선시합니다.

플라스틱 용기는 다용도성, 투명성 및 낮은 단가를 바탕으로 2025년 유럽 화장품 포장 시장의 61.78% 점유율을 차지했습니다. 동시에 생분해성 및 퇴비화 가능 옵션은 현재 규모는 작지만, 2028년 발효 예정인 PPWR 산업용 퇴비화 가능성 규정에 기반한 기술 발전과 규제적 호재로 2031년까지 연평균 4.42% 성장률을 기록할 전망입니다. 이 부문은 충격 저항성을 저하시키지 않으면서 얇은 벽 두께를 구현하는 사출-스트레치-블로우 기술 투자로 계속해서 혜택을 보고 있습니다. 그러나 수지 혼합 비율은 변화하고 있습니다. 매스밸런스 바이오-PET와 기계적 재생 PET가 특히 적정 가격 프리미엄을 수용하는 프리미엄 스킨케어 라인에서 점유율을 확대 중입니다. 유리는 고급스러운 이미지로 인해 향수 및 고급 세럼 시장에서 충성도 높은 틈새 시장을 유지하는 반면, 무한 재활용 가능성 덕분에 알루미늄 용기는 고체 헤어케어 바 분야에서 선호됩니다.

플라스틱이 여전히 규모 우위를 점하고 있지만, 주요 가공업체들은 모두 소재 순환성에 초점을 맞춘 연구개발 예산을 발표한 상태입니다. AINIA의 곡물 기반 바이오튜브는 식품 등급 원료로 상업적 실현 가능성을 입증했으며 퇴비화 요건도 충족합니다. 다층 차단재는 점차 Albea의 폴리프로필렌 립스틱 케이스와 같은 단일 소재 솔루션으로 대체되고 있습니다. 소재 결정이 성능과 수명 종료 시 결과를 균형 있게 고려함에 따라, 생분해성 바이오 기반 등급의 직접 대체 적용이나 폐쇄형 수지 인증을 확보한 가공업체들이 시장 점유율을 선점할 전망입니다.

병과 항아리는 2025년 매출의 36.10%를 차지했으나, 유통 채널이 온라인으로 전환되면서 유연 포장 파우치와 사첼은 2031년까지 연평균 5.02% 성장률을 기록할 전망입니다. 스탠드업 파우치는 경질 PET 대비 무게를 최대 70% 줄여 운송 배출량과 택배 비용을 절감합니다. 소형 포켓 멀티팩은 분량 조절과 공간 효율성을 결합해 디지털 물류 허브에 매력적인 특성을 지닙니다. 정밀 도징 노즐 덕분에 튜브는 여전히 색조 화장품과 자외선 차단제의 핵심 플랫폼으로 자리매김합니다. 캡과 어플리케이터는 재활용성을 높이는 단일 폴리머 디자인으로 진화 중이며, 알베아의 '브레즈스틱'이 폴리프로필렌으로만 제작된 사례가 이를 입증합니다.

경제형 라인에 한정되었던 유연 구조는 이제 고해상도 플렉소 그래픽과 고급형 오버나이트 마스크에 적합한 무알루미늄 가스 차단 기능을 갖추었습니다. 변환업체들은 한정판 인플루언서 협업에 맞춰 소량 생산을 위한 디지털 인쇄를 추진합니다. 접이식 카톤은 선물용으로 역할을 유지하지만 무게 경감과 플라스틱 창 제거를 거칩니다. 포트폴리오 관리자들은 보호용 강성과 최종 배송 단계의 스트레스 사이의 균형을 저울질하며 가상 낙하 테스트를 통해 최적화합니다.

The Europe cosmetic packaging market size in 2026 is estimated at USD 5.71 billion, growing from 2025 value of USD 5.56 billion with 2031 projections showing USD 6.52 billion, growing at 2.7% CAGR over 2026-2031.

Moderate top-line growth masks far-reaching structural change as the EU Packaging and Packaging Waste Regulation compels a pivot to recyclable formats, pushes minimum recycled content thresholds, and accelerates the shift toward mono-material and refillable solutions. Demand patterns are also shaped by e-commerce fulfillment requirements, a younger consumer base favoring minimalist aesthetics, and the rapid integration of smart features that authenticate products and capture behavioral data. Competitive intensity increases as scale economies become critical for financing material innovation, AI-enabled design tools, and end-of-life collection infrastructure. Supply chain bottlenecks for recycled PET and the cost premium on bio-based polymers temper the outlook yet simultaneously create white-space opportunities for vertically integrated or specialty players.

Sales of refill solutions increased 62% across major European markets as brands validate luxury aesthetics and lower carbon footprints. Lumson's XTAG airless system delivers a 38% CO2 reduction versus traditional formats while retaining a premium look and feel. Clarins introduced its first refillable jar with Albea, signaling mainstream adoption among prestige brands. Consumer sentiment is supportive, with 64% viewing refill products as genuinely eco-friendly rather than compromise solutions. Technical breakthroughs, such as FASTEN BV's recycled polypropylene jar cut material use by 70% through stackable inserts. The refill model also creates recurring revenue streams and strengthens brand loyalty by increasing direct interaction frequency.

Final adoption of the Packaging and Packaging Waste Regulation in December 2024 introduces binding targets for 100% recyclable packaging and minimum post-consumer recycled content by 2030. Cosmetics Europe acknowledged opportunities in cost savings from harmonized rules, yet expressed concern about creative restrictions that could impact visual differentiation. The ban on miniature cosmetic bottles compels redesigns that reshape the on-shelf presence. Implementation costs favor larger players, driving consolidation as seen in the Quadpack-Texen merger. Harmonized Extended Producer Responsibility schemes reduce regulatory fragmentation but add complexity for global brands managing divergent non-EU rules.

Prices for polylactic acid and bio-PET run 30% to 50% above fossil-based equivalents despite higher crude prices, locking out smaller brands that lack scale leverage. Europe's share of global bio-polymer output slipped from 13% to 10% as Asian capacity ramped faster. Feedstock constraints add volatility because sugar and starch crops compete with food markets. Reformulation costs also mount, as bio-based grades sometimes need barrier coatings or stabilizers, complicating recycling streams. Consequently, many converters prioritize recycled content strategies over bio-feedstocks to attain PPWR mandates at lower cost.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Plastic formats captured 61.78% share of the European cosmetic packaging market in 2025 on the back of versatility, clarity, and low unit cost. At the same time, biodegradable and compostable options, though small today, are set to post a 4.42% CAGR to 2031, reflecting technical advances and regulatory tailwinds anchored in the PPWR industrial compostability provision effective 2028. The segment continues to benefit from injection-stretch-blow investments that achieve thin-wall reductions without compromising impact resistance. Yet the resin mix is shifting. Mass-balance bio-PET and mechanically recycled PET are gaining shelf presence, especially among premium skin-care lines that accept moderate price premiums. Glass retains a loyal niche in fragrances and high-end serums due to perceived luxury, whereas aluminum containers win favor in solid haircare bars thanks to infinite recyclability.

Although plastics maintain a scale advantage, every major converter has announced R&D budgets focusing on material circularity. AINIA's cereal-based biotube demonstrates commercial feasibility with food-grade inputs and addresses compostability requirements. Multilayer barriers are gradually giving way to mono-material solutions such as Albea's polypropylene lipstick case. As material decision-making balances performance with end-of-life outcomes, converters that master drop-in bio-based grades or closed-loop resin certification stand to capture share.

Bottles and jars contributed 36.10% of 2025 revenue, yet flexible pouches and sachets are projected to log a 5.02% CAGR to 2031 as the channel mix tilts online. Stand-up pouches reduce weight by up to 70% versus rigid PET, trimming freight emissions and parcel costs. Sachet multi-packs combine portion control with space efficiency, traits attractive to digital fulfillment nodes. Tubes remain a core platform for color cosmetics and sun protection owing to precision dosing nozzles. Caps and applicators move toward single-polymer designs that aid recyclability, evidenced by Albea's Breizhstick, built entirely from polypropylene.

Flexible structures formerly limited to economy lines now feature high-definition flexo graphics and aluminum-free gas barriers suitable for prestige overnight masks. Converters push digital printing for small batch runs aligned with limited-edition influencer collaborations. Folding cartons keep a role in gifting but undergo weight reduction and removal of plastic windows. Portfolio managers weigh the trade-off between protective rigidity and last-mile shipping stress, optimizing through virtual drop tests.

The Europe Cosmetic Packaging Market Report is Segmented by Material Type (Plastic, Glass, Metal, and More), Product Type (Bottles and Jars, Tubes and Sticks, Folding Cartons, Pump, Dispenser and Droppers, and More), Cosmetic Type (Skin Care, Hair Care, Color Cosmetics, and More), Distribution Channel (Direct Sales Channel, and Indirect Sales Channel), and Geography. The Market Forecasts are Provided in Terms of Value (USD).