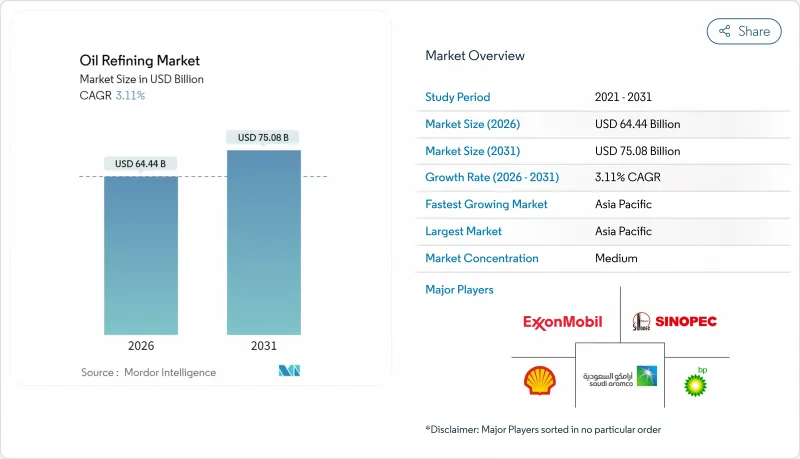

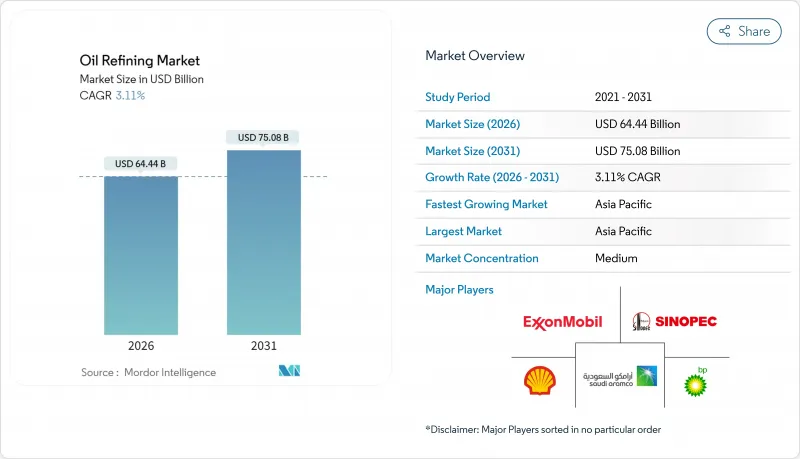

정유 시장은 2025년 625억 달러로 평가되었고, 2026년 644억 4,000만 달러에서 2031년까지 750억 8,000만 달러에 이를 것으로 예측되며, 예측기간(2026-2031년)의 CAGR은 3.11%로 전망됩니다.

이 성장 궤도는 석유화학 통합으로의 급속한 전환, 대규모 탈황 설비의 개조, 가솔린 수요의 침체로부터 마진을 보호하는 재생가능한 디젤 플랫폼에 의해 발생합니다. 전환율, 디지털 최적화, 다양한 연료 라인업을 결합한 사업자들은 계속해서 뛰어난 실적을 유지하는 한편, 단일 연료 경제에 묶인 플랜트나 원료의 유연성이 부족한 플랜트는 폐쇄 또는 특수 용도로의 전환이 진행되고 있습니다. 정유소의 처리 능력 증가는 아시아태평양, 중동 및 특정 아프리카 시장에서 가장 강력하게 변화하고 있습니다. 이 지역에서는 정부가 다운스트림 부문의 자급 자족과 수출 목표를 뒷받침하고 있습니다. 한편 OECD 국가에서의 합리화와 ESG 관련 자본의 부족이 선진 지역에서의 신규 건설을 제한하고 있어 고품질 원유와 안정된 크랙 스프레드를 둘러싼 세계의 경쟁을 격화시키고 있습니다.

아시아의 정유소는 촉매 크래커와 폴리프로필렌 라인을 통합하여 밸류체인의 업스트림화를 진행하고 있습니다. 중국 해양석유총공사(CNOOC)의 닝보 정유소 업그레이드는 연간 45만 톤의 폴리프로필렌 생산 능력을 추가하여 원유 처리량이 50% 증가했습니다. 이로써 해당 복합시설은 견조한 국내 화학제품 수요에 접근하게 되었습니다. 인도에서도 같은 투자가 이루어져 2030년까지 3,500만-4,000만톤의 신규 생산 능력 획득을 목표로 하고 있으며 나프타를 방향족과 올레핀 체인 생산에 사용할 계획입니다. 통합은 전기자동차의 이익률 저하를 방지하면서 정유 시장 전체에서 장기 수익의 지속성을 뒷받침하는 높은 석유화학 스프레드를 획득하고 있습니다.

유황 상한에 대한 규제는 연료 품질에 대한 기대를 계속 재구성하고 있습니다. 엑손 모빌의 폴리 투자에는 연간 5억 7,000만 갤런의 저황 디젤을 생산하는 수소화 처리 장치가 포함되어 있습니다. 내륙부의 정제업자도 탈황장치를 업그레이드하여 고품질의 선박 연료를 공급함으로써 공급 지역의 확대와 재정 거래 선택사항의 개선을 도모하고 있습니다. 규제 대응 목적의 설비 업그레이드를 위한 지속적인 자본 유입은 수소 및 촉매 시스템에 대한 수요를 강화하고 처리량의 유연성을 유지함과 동시에 정유 시장을 뒷받침하고 있습니다.

유럽과 북미에서는 기업이 기후정책을 준수하는 가운데 오래된 플랜트의 폐쇄와 용도 변경이 진행되고 있습니다. 토탈에너지스는 Grandpuits 정유소를 원유 제로 플랫폼으로 전환하여 지속 가능한 항공 연료와 바이오 폴리머를 생산합니다. 쉘은 2025년 웨셀링에서 원유 처리를 종료하고 기유 생산으로 전환하였습니다. 이러한 움직임은 지역 공급을 촉진하고, 생존 플랜트의 가동률을 높이며, 제품 수입 패턴을 재구축하지만, 정유 시장 내 생산 능력 확대에는 한계가 있습니다.

2025년 중질유는 정유 시장에서 37.12%의 점유율을 유지했습니다. 이는 세계 여행 수요와 신흥 시장의 화물 운송 회복과 함께 제트 연료와 경유 부문이 회복되었기 때문입니다. 경질유는 개발도상국에서의 자동차 소유 대수 증가로 계속 혜택을 받고 있지만 성숙 지역에서는 구조적인 감소에 직면하고 있습니다. 중유는 선박 및 발전 분야에서의 규제 강화 영향으로 잔사유의 고도화를 목적으로 한 코크스화 장치 및 수소화 분해 장치에 대한 투자가 촉진되고 있습니다. 석유화학원료 부문은 통합형 오퍼레이터가 나프타나 LPG를 수익성이 높은 폴리머 체인으로 전환하려는 움직임에 의해 3.85%의 연평균 복합 성장률(CAGR)로 가장 높은 성장률을 나타내고 있습니다. 화학물질로의 전환은 마진의 안정성을 높이고 정유 시장에서 수익 기반의 확대를 뒷받침합니다.

첨단 통합은 장치의 복잡성을 높이고 원유의 유연성을 향상시켜 다양한 제품 구성을 제공할 수 있습니다. 중국 해양석유총공사(CNOOC) 닝보 정유소에서의 폴리프로필렌 증설과 2028년 예정인 쉘 하이주 확장계획은 화학제품 중심의 조업 동향을 부각하고 있습니다. 이러한 프로젝트는 고전환율 자산의 정유 시장 내 규모를 확대하고 전기자동차의 가솔린 수요 대체로부터 마진을 보호합니다.

정유 시장 보고서는 제품 구성(경질유, 중질유, 중유 및 잔사유, 석유화학원료), 소유 형태(국영석유회사, 통합석유회사, 독립 및 도매 정제업체), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 규모와 예측은 수익(달러) 기준으로 제공됩니다.

아시아태평양은 정유 시설 확장으로 주도적 지위를 유지하고 있습니다. 중국 해양석유총공사(CNOOC)가 27억 4,000만 달러를 투입한 닝보 정유소의 증강으로 원유 처리능력은 24만 배럴/일에 달하고, 국내 플라스틱 수요에 대응하기 위해 폴리프로필렌 제조설비가 추가되었습니다. 인도에서는 19-22조 루피 규모의 용량 증설 계획이 CAGR 4%로 확대되는 소비를 뒷받침합니다. 동남아시아에서는 베트남과 인도네시아에서 제품 수입 의존도 저감을 목적으로 한 신규 프로젝트가 진행되고 일본과 한국은 고효율 조업과 기술 수출에 주력하고 있습니다. 이 지역의 통합 모델과 정부 지원은 정유 시장의 확대를 뒷받침하고 있습니다.

북미는 여전히 주요 수출 지역입니다. 셰일 유래 경질유의 공급으로 미국 멕시코 걸프 지역의 정유소에서 원료 비용이 절감되었습니다. Philips 66의 스위니 정유소 설비 업그레이드에 의해 가솔린과 화학 원료의 생산을 우선시한 유연한 조업이 가능하게 되었습니다. 발레로는 재생가능 디젤을 포함한 저탄소 프로젝트에 54억 달러를 투자하여 배출 목표와 이익 확보 간의 균형을 맞추고 있습니다. 캐나다와 멕시코는 정책 전환으로 자산 근대화를 다투고 있지만 미국은 풍부한 원료와 심해 물류 네트워크를 통해 정유 시장에서 구조적 우위를 유지하고 있습니다.

유럽에서는 가장 급속한 구조 변화가 발생하고 있습니다. 토탈에너지스는 Grandpuits 정유소를 재생에너지 거점으로 전환하고 있습니다. 쉘은 웨셀링 정유소를 재사용하여 기존 생산 능력을 줄이는 한편 지속 가능한 항공 연료 및 기유 생산을 추가했습니다. 탄소 가격 도입으로 중질유의 운영 비용이 증가하고 유닛 전환 및 수소 통합이 촉진됩니다. 폐쇄로 인한 공급 압박은 중동 및 미국으로부터의 수입 증가를 초래하여 대서양 횡단 무역을 활성화함과 동시에 정유 시장에서 존속 플랜트 간의 경쟁력 격차를 확대하고 있습니다.

The Oil Refining Market was valued at USD 62.5 billion in 2025 and estimated to grow from USD 64.44 billion in 2026 to reach USD 75.08 billion by 2031, at a CAGR of 3.11% during the forecast period (2026-2031).

This forward trajectory stems from refiners' accelerated push into petrochemical integration, large-scale desulfurization retrofits, and renewable diesel platforms that help shield margins from soft gasoline demand. Operators that combine conversion depth, digital optimization, and diversified fuel slates continue to outperform, while plants locked into single-fuel economics or lacking feedstock flexibility are closing or converting to specialty uses. Refinery throughput growth remains strongest in the Asia-Pacific, the Middle East, and select African markets, where governments support downstream self-sufficiency and export ambitions. Simultaneously, OECD rationalization and ESG-linked capital scarcity limit green-field build in developed regions, intensifying the global contest for high-quality barrels and resilient cracks.

Asia's refiners integrate catalytic crackers and polypropylene lines to move up the value chain. CNOOC's Ningbo upgrade added 450,000 tpy polypropylene capacity and lifted crude runs by 50%, giving the complex access to robust domestic chemical demand. Similar investments in India aim to target 35-40 million tonnes of new capacity by 2030, with naphtha being directed to aromatic and olefin chains. Integration protects margins from erosion driven by electric vehicles, while capturing higher petrochemical spreads that underpin long-term earnings resilience across the oil refining market.

The sulfur cap continues to reshape fuel quality expectations. ExxonMobil's Fawley investment includes a hydrotreater that produces 570 million gallons of low-sulfur diesel annually. Inland refiners also retrofit desulfurizers to supply premium bunker fuel, expanding geographic supply and improving arbitrage options. Sustained capital inflows toward compliance upgrades reinforce demand for hydrogen and catalyst systems, sustaining throughput flexibility and supporting the oil refining market.

Europe and North America are closing or repurposing older plants as firms align with climate policies. TotalEnergies is converting Grandpuits into a zero-crude platform producing sustainable aviation fuel and biopolymers. Shell will end crude runs at Wesseling by 2025, shifting to base oils. These actions tighten regional supply, elevate utilization at surviving sites, and reshape product import patterns, yet cap capacity growth within the oil refining market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Middle distillates retained a 37.12% oil refining market share in 2025, as jet fuel and diesel recovered alongside global travel and emerging-market freight. Light distillates continue to benefit from rising vehicle ownership in developing economies, yet face structural declines in mature regions. Heavy fuel oil struggles with stricter marine and power regulations, prompting investments in cokers and hydrocrackers to upgrade residues. The petrochemical feedstock category grows at the fastest rate, with a 3.85% CAGR, as integrated operators channel naphtha and LPG into high-margin polymer chains. The chemicals pivot enhances margin stability and supports a broader revenue base within the oil refining market.

Greater integration increases unit complexity, enhancing crude flexibility and enabling the selection of a diverse slate. CNOOC's polypropylene addition in Ningbo and Shell's Huizhou expansion, scheduled for 2028, highlight the trend toward operations centered on chemicals. Such projects expand the oil refining market size for high-conversion assets and shield earnings from gasoline displacement by electric vehicles.

The Oil Refining Market Report is Segmented by Product Slate (Light Distillates, Middle Distillates, Fuel Oil and Residuals, and Petro-Chemical Feed-Stocks), Ownership (National Oil Companies, Integrated Oil Companies, and Independent/Merchant Refiners), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Size and Forecasts are Provided in Terms of Revenue (USD).

Asia-Pacific's refining complex expansion underpins its leadership. CNOOC's USD 2.74 billion Ningbo upgrade lifted crude runs to 240,000 bpd, adding polypropylene units to meet domestic plastics demand. India's planned capacity builds worth INR 1.9-2.2 lakh crore support sustained supply as consumption expands at 4% CAGR. Southeast Asia is seeing new projects in Vietnam and Indonesia aimed at reducing product import dependence, while Japan and South Korea are focusing on high-efficiency operations and technology exports. The region's integrated models and government backing continue to enlarge the oil refining market.

North America remains a pivotal exporter. Shale-driven light crude availability reduces feedstock costs for Gulf Coast refineries. Phillips 66's Sweeny upgrades allow flexible runs that favor gasoline and chemical feedstock production. Valero channels USD 5.4 billion into low-carbon projects, including renewable diesel, to balance emissions objectives with margin capture. Canada and Mexico vie to modernize their assets amid policy shifts, yet the U.S. maintains a structural advantage in the oil refining market through its abundant feedstocks and deepwater logistics networks.

Europe experiences the fastest structural change. TotalEnergies converts Grandpuits to a renewable platform, while Shell repurposes Wesseling, removing conventional capacity yet adding sustainable aviation and base-oil output. Carbon pricing increases operating costs for heavy-fuel streams, incentivizing the conversion of units and the integration of hydrogen. Supply tightness from closures increases imports from the Middle East and the United States, elevating trans-Atlantic trade and reinforcing competitiveness gaps among surviving plants within the oil refining market.