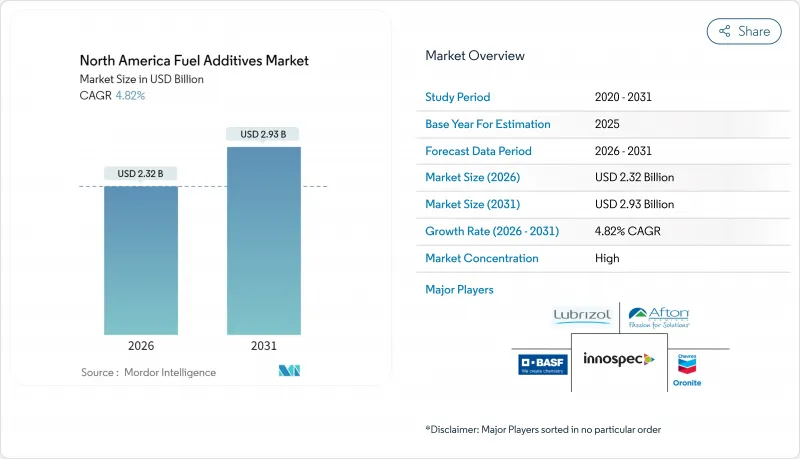

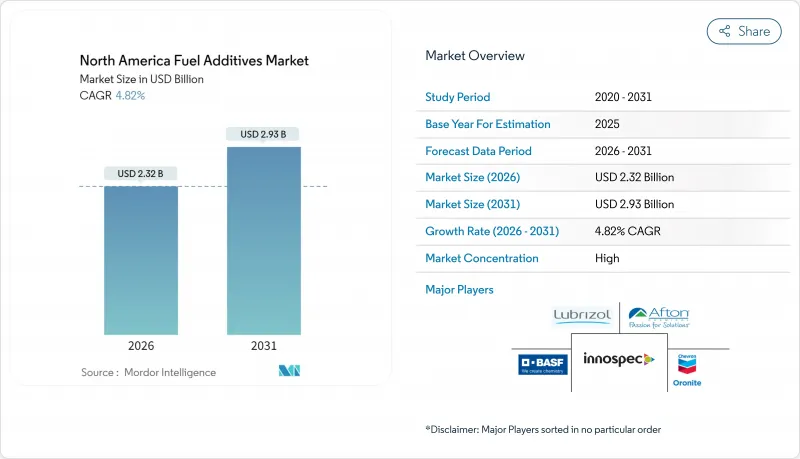

북미의 연료첨가제 시장은 2025년 22억 1,000만 달러로 평가되었고, 2026년에는 23억 2,000만 달러로 성장할 것으로 예측됩니다. 2026-2031년에 걸쳐 CAGR 4.82%로 성장할 것으로 보이며, 2031년까지 29억 3,000만 달러에 이를 전망입니다.

현재의 성장은 적극적인 황 저감 규정, 노후화된 내연 기관 차량의 내구성 요구, 재생 가능 대체 연료가 주류 공급에 진입함에 따라 가솔린 및 디젤 엔진의 효율성을 유지해야 할 필요성에 기반하고 있습니다. 가솔린 직접분사(GDI) 엔진이 기존 포트분사 플랫폼보다 오염되기 쉬워 침전물 제어 화학물질이 주류를 이루는 반면, 정유사들이 방향족 화합물 급증 없이 높은 엔진 압축비를 추구함에 따라 옥탄가 향상용 노킹 방지제가 가장 빠르게 채택되고 있습니다. 상업용 디젤 사용자들은 초저유황디젤(ULSD)의 단점을 상쇄하는 윤활성 및 세탄가 향상제 수요를 촉진합니다. 공급업체들은 정유소 출고 가격보다 마진 기회가 더 큰 애프터마켓 채널을 통해 추가 수익을 창출합니다. 배터리 전기차(BEV) 보급률이 상승 중임에도 북미의 연료 첨가제 시장은 여전히 확장세를 유지하는데, 이는 액체 연료 풀이 기존 승용차, 대형 차량, 선박 연료, 지속가능 항공 연료(SAF) 분야에 계속 공급되기 때문입니다.

Tier-3 가솔린의 황 함량 상한선 10ppm과 배출 규제 구역(ECA)의 선박용 연료 황 함량 0.1% 규정은 첨가제 수요를 영구적으로 재설정했습니다. 정유사들은 손실된 윤활성을 대체하고, 옥탄가를 유지하며, 침전물을 분산시키고, 부식을 방지하는 다기능 패키지에 의존합니다. 캘리포니아에서는 ‘고급 청정 자동차 II(Advanced Clean Cars II)’ 프레임워크가 2035년까지 저유황 의무화를 연장함에 따라 준수 비용이 더욱 상승합니다. 동시에 터미널 운영사들은 저유황 저장 시즌 동안 미생물 오염을 방지하는 살균제를 도입하고 있습니다. 이러한 누적 효과는 북미의 연료 첨가제 시장 전반에 걸쳐 처리율의 구조적 상승을 주도하며, 기준선 휘발유 및 디젤 처리량이 정체되더라도 물량 탄력성을 유지합니다.

초저유황디젤(ULSD)은 자연 윤활성이 낮으며, GDI 엔진은 포트 시스템 대비 10배 빠른 속도로 흡기 밸브 침전물을 생성합니다. 이 교차점은 고온 베이킹 현상에 저항하는 폴리이소부틸아민 및 폴리에테르아민 혼합물과 같은 세정 화학 분야의 급속한 혁신을 촉진합니다. EPA Tier 3 배출 제한은 자동차 제조사가 촉매 효율을 유지하도록 의무화하며, 코킹 증가 시 이 효율이 저하됩니다. 수소화 재생 디젤의 동시 성장은 기존 석유 분획에서는 발생하지 않았던 윤활성 격차를 야기합니다. 이러한 요소들이 복합적으로 작용하여 북미의 연료 첨가제 시장에서 세정제, 윤활성 향상제, 세탄가 향상제의 기능적 범위와 수익 기회를 확대하고 있습니다.

인구 밀집 지역에서는 2030년까지 신규 경량 차량 판매의 절반이 전기차로 전환될 것으로 전망됩니다. 전기차(EV)가 한 대씩 증가할 때마다 가솔린 수요가 영구적으로 대체되며, 북미의 연료 첨가제 시장의 잠재적 규모가 점차 축소됩니다. 택배 배송 및 시내버스 차량군이 배터리 플랫폼을 시험함에 따라 디젤의 방위적 우위가 약화되어, 고처리량 상업 고객 대상 기존 첨가제 판매가 위축됩니다. 공급업체들은 전기화가 여전히 큰 장벽인 항공, 해운, 산업 분야로 전환하며 대응하고 있습니다.

침전물 제어 패키지는 북미의 연료 첨가제 시장 점유율의 33.02%를 차지했습니다. 폴리에테르아민 및 폴리이소부틸렌 숙신이미드를 기반으로 한 다기능 세제는 현대식 GDI 플랫폼에서 증식하는 밸브, 인젝터 및 연소실 침전물을 제거합니다. 고압축 엔진은 옥탄가 수요를 촉진하여 2031년까지 예상 연평균 성장률(CAGR) 5.28%로 노크 방지제 판매를 끌어올립니다.

저온 유동성 개선제는 캐나다 및 미국 북부 주에서 -10°F 이하에서도 디젤 연료의 가동성을 유지하며, 세탄가, 윤활성 및 부식 방지제는 낮은 방향족 및 황 함량을 가진 재생 디젤 혼합물에서 새로운 중요성을 찾고 있습니다. 공급업체들은 이러한 화학 물질을 단일 패키지로 묶어 정유사가 ASTM, EPA 및 캐나다 교통부 규격을 충족하면서 처리 비용을 절감할 수 있도록 하고 있습니다. 검증 장벽이 높아지면서 소수의 기술 보유 기업들이 협상력을 강화하고 있지만, 바이오디젤 안정제 및 고인화점 선박용 첨가제 같은 하위 부문에서는 여전히 특수 업체들이 경쟁 구도를 형성하며 북미의 연료 첨가제 시장의 경쟁을 촉진하고 있습니다.

북미의 연료 첨가제 보고서는 제품 유형(침전물 제어제, 세탄가 향상제, 윤활성 첨가제, 산화 방지제, 부식 방지제, 저온 유동성 개선제, 노킹 방지제, 기타 제품 유형), 용도(디젤, 가솔린, 제트 연료 및 기타 용도), 지역(미국, 캐나다, 멕시코)별로 분류됩니다. 시장 예측은 금액 기준(달러)으로 제공됩니다.

The North America Fuel Additives Market is expected to grow from USD 2.21 billion in 2025 to USD 2.32 billion in 2026 and is forecast to reach USD 2.93 billion by 2031 at 4.82% CAGR over 2026-2031.

Current growth rests on aggressive sulfur-reduction rules, the durability needs of an aging internal-combustion fleet, and the need to keep both gasoline and diesel engines efficient as renewable drop-ins enter mainstream supply. Deposit control chemistries dominate because gasoline direct-injection (GDI) engines foul more readily than legacy port-injection platforms, while octane-boosting antiknock agents record the quickest uptake as refiners strive for higher engine compression ratios without aromatics spikes. Commercial diesel users push demand for lubricity and cetane improvers that offset ultra-low-sulfur diesel (ULSD) shortcomings. Suppliers further benefit from aftermarket channels where margin opportunities remain stronger than at the refinery gate. Even with battery-electric vehicle (BEV) penetration climbing, the North America fuel additives market continues to expand because the liquid-fuel pool still serves legacy passenger vehicles, heavy-duty fleets, marine bunkers, and sustainable aviation fuel applications.

Tier-3 gasoline caps at 10 ppm sulfur and Emission Control Area marine requirements of 0.1% sulfur have permanently reset additive demand. Refiners rely on multifunctional packages that replace lost lubricity, maintain octane, disperse deposits, and guard against corrosion. Compliance costs rise further in California, where the Advanced Clean Cars II framework extends low-sulfur mandates through 2035. Terminal operators simultaneously adopt biocides that prevent microbial contamination during low-sulfur storage seasons. The cumulative effect drives a structural uptick in treat rates across the North America fuel additives market, keeping volumes resilient even when baseline gasoline and diesel throughput plateaus.

ULSD carries lower natural lubricity, while GDI engines generate intake-valve deposits at 10X the rate of port systems. This intersection fuels rapid innovation in detergency chemistries such as polyisobutylamine and polyetheramine blends that resist high-temperature bake-on. EPA Tier 3 emission limits obligate automakers to maintain catalyst efficiency, which is compromised when coking rises. Concurrent growth in hydrogenated renewable diesel raises lubricity gaps that traditional petroleum fractions never posed. Together, these vectors expand the functional scope-and revenue opportunity-of detergent, lubricity, and cetane improvers across the North America fuel additives market.

Forecasts point to half of new-light-duty sales being electric by 2030 in densely populated corridors. Each incremental EV permanently displaces gasoline demand and gradually trims the North America fuel additives market addressable volume. Diesel's defensive moat erodes as parcel-delivery and municipal bus fleets test battery platforms, curtailing traditional additive sales to high-throughput commercial accounts. Suppliers respond by pivoting toward aviation, marine, and industrial channels where electrification hurdles remain significant.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Deposit control packages held 33.02% of the North America fuel additives market share. Multifunctional detergents based on polyetheramines and polyisobutylene succinimides strip valve, injector, and combustion-chamber deposits that proliferate in modern GDI platforms. Higher compression engines spur octane demand, lifting antiknock agent sales at a projected 5.28% CAGR through 2031.

Cold-flow improvers preserve diesel operability below -10 °F in Canadian and Northern U.S. states, while cetane, lubricity, and corrosion inhibitors find fresh relevance in renewable diesel blends that arrive with low aromatics and sulfur. Suppliers increasingly bundle these chemistries into single packages, allowing refiners to reduce treat cost while meeting ASTM, EPA, and Transport Canada specifications. Escalating validation hurdles consolidate bargaining power within a handful of technology owners, yet specialty players still carve out sub-segments such as biodiesel stabilizers and high-flash-point marine additives, ensuring competitive churn inside the North America fuel additives market.

The North America Fuel Additives Report is Segmented by Product Type (Deposit Control, Cetane Improvers, Lubricity Additives, Antioxidants, Anticorrosion, Cold Flow Improvers, Antiknock Agents, and Other Product Types), Application (Diesel, Gasoline, Jet Fuel, and Other Applications), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).