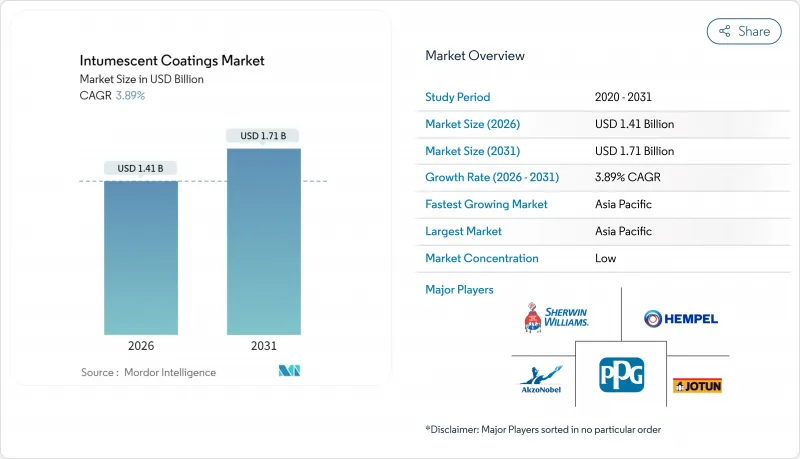

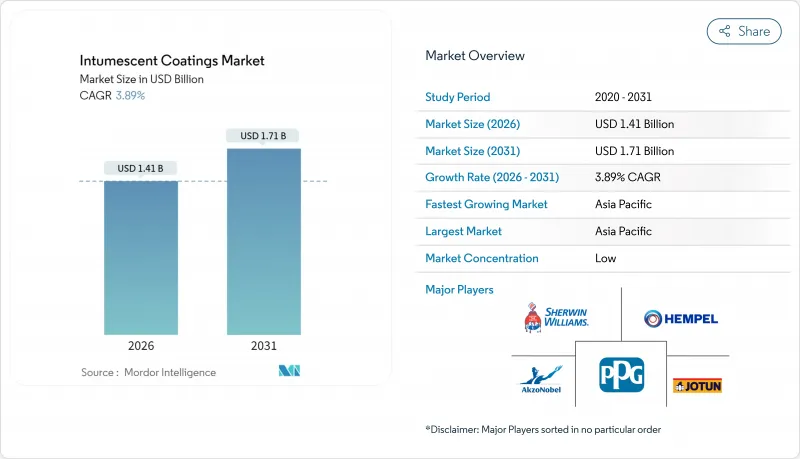

2026년 팽창성 코팅 시장 규모는 14억 1,000만 달러로 추정되며, 2025년 13억 6,000만 달러에서 성장한 수치입니다. 2031년에는 17억 1,000만 달러에 이르고, 2026년부터 2031년까지의 연평균 성장률(CAGR)은 3.89%를 나타낼 전망입니다.

채택의 배경에는 세계적으로 엄격화하는 방화 안전 기준, 환경 친화적인 건축자재로의 결정적인 이행, 그리고 보호 성능을 손상시키지 않고 구조용 강재를 노출시키고 싶은 요망이 있습니다. 수요 증가는 폭발적이라는 점점 더 점진적이며, 이는 투기적인 건설 붐이 아니라 법규 준수 사이클에 기반한 회복력을 시사하는 경향입니다. 수성화학제품은 이미 수익의 40%를 차지하고 있으며, 휘발성 유기화합물에 대한 규제 강화로 저취기 솔루션을 선호하는 설계자 증가에 따라 이 비율은 앞으로도 계속 상승할 전망입니다. 고밀도 도시, 해상 에너지 거점, 모듈식 공장에서의 방화 리스크의 사전 경감책의 선호가 높아지고 있는 것은 열에 노출되면 단열성이 있는 탄화층에 팽창하는 박막을 중시하는 폭넓은 이용 사례를 나타내고 있습니다. 내구성, 경화 속도의 향상, 도포 두께의 저감에 관한 병행한 기술 혁신에 의해 제품 수명이 연장되고 있기 때문에 팽창성 코팅 시장에서의 수익 성장은 순수한 수량 증가가 아니라, 평방 피트당의 평생 가치의 상승을 점점 반영하는 경향에 있습니다.

24미터를 넘는 타워에 대한 새로운 요구사항으로 박막 코팅은 거의 필수가 되어, 구조 중량을 추가하지 않고 2시간의 보호를 제공하는 제품을 개발자에게 제공합니다. 중국과 인도의 인증 제도는 제3자 시험을 중시하고 있으며, 진입 장벽을 높이는 동시에 조기 참가자에게 우위성을 가져오고 있습니다. 따라서 도시의 고층화가 진행되어 피난 시간이 단축되는 가운데, 팽창성 코팅 시장은 구조적인 추풍을 받고 있습니다. 제품 라벨을 현지 건축 기준에 맞춘 공급업체는 입찰 목록에 쉽게 등록할 수 있으며, 현재 취득한 허가는 여러 프로젝트 단계에 걸쳐 있는 경우가 많아 수익 전망이 향상되고 있습니다.

탄화수소 전용 제품은 2024년에 44.2%의 점유율을 차지했습니다. 이는 해양 상부 구조물, LNG 플랜트, 정유소가 1,100℃를 초과하는 수영장 화재 온도를 다루어야 하기 때문입니다. 북미 전역의 셰일 관련 건설은 조선소의 가동을 유지하고 에폭시 팽창성 필름의 안정적인 수주를 계속하고 있습니다. 공급 및 설치를 일괄 계약하는 계약업체는 운영자가 단일 계약에 따른 책임 체제를 중시하기 때문에 더 높은 이익률을 유지할 수 있습니다. UL 1709와 같은 프로토콜 시험을 통과한 페인트는 사양 목록에 오랫동안 게재되는 경향이 있으며 팽창성 코팅 시장의 지속적인 수익원을 지원합니다.

원재료 비용 변동은 특히 스팟화물 구매를 수행하는 아시아 생산자에게 이익률을 압박합니다. 다년간 공급 계약은 부분적인 보호를 제공하지만 원료 가격이 급등할 경우 위험을 완전히 배제할 수 없습니다. 예산 초과는 프로젝트 시작 지연과 표준이 허용하는 범위 내에서 제품 대체를 일으킬 수 있으며 팽창성 코팅 시장의 성장을 일시적으로 둔화시킬 수 있습니다.

셀룰로오스계 도료는 2025년의 수익의 52.60%(7억 1,540만 달러)를 차지하고, 상업 및 주택용 강재의 대규모 수요가 저속 연소 화재로부터의 보호를 필요로 하기 때문에 계속해서 주류입니다. 비교적 저가이기 때문에 중층 프로젝트로의 보급이 진행되고 있으며, 규제 시행만이 촉진요인이 아닙니다. 건축가는 명확한 비용 효과가 예상되고 반복적으로 채택되는 경향이 있습니다. 이는 탄화수소계 제품 수요가 급증하더라도 견고한 기반 수요가 유지된다는 것을 시사합니다. 한편, 탄화수소 내화등급 제품은 6억 4,460만 달러의 매출을 계상했지만, 2031년까지 연평균 복합 성장률(CAGR) 4.92%로 시장 전체를 웃도는 성장이 전망되고 있습니다. 이러한 제품은 제트 화재 시험과 수영장 화재 시험을 견뎌야 하며, EPC 기업이 브랜드를 한 번 인증하면 프로젝트 도중에 변경하는 것은 드뭅니다. 이 연속성은 장기 유지 보수 업무를 고정화하여 예측 가능한 판매 후 수익을 창출합니다. 따라서 탄화수소계 하위분할은 톤수가 낮더라도 계약당 수익을 높여 팽창성 코팅 시장 내에서 가치 집중을 강화합니다.

탄화수소계 페인트의 높은 성장률은 걸프 지역과 중동의 새로운 FPSO 유닛, LNG 수출 플랜트, 정유 공장 업그레이드와 직접 연결되어 있습니다. 해양자산에서는 열충격 하에서도 밀착성을 유지하는 도료가 요구되기 때문에 에폭시계 시스템이 여전히 표준 플랫폼이 되고 있습니다. 탄화수소 응용 분야의 팽창성 코팅 시장 규모는 각국의 에너지 전략이 하류 부문의 자급 자족에 주력함에 따라 확대가 예상됩니다. 한편, 셀룰로오스계 제품은 도시의 밀집화에 따라 노출된 강재가 현대적인 미관을 제공하는 분야에서 수요를 유지하고 있습니다. 이 두 가지 방화 시나리오는 서로 다른 길을 걷고 있지만, 동일한 면적을 겨루는 것이 아니라 각기 다른 안전 요구에 대응하기 때문에 전반적인 시장 침투를 강화하고 있습니다.

수성 솔루션은 2025년 수익의 40.80%를 차지하고 있으며, 5.22%의 연평균 복합 성장률(CAGR)로 계속 성장하고 있으며, 낮은 VOC 시공 기법으로의 전환을 견인하고 있습니다. 강한 냄새가 없기 때문에 입주자가 남은 상태에서의 도장이 가능해, 개수 작업의 물류를 간소화하는 실용적인 이점이 있습니다. 이로 인해 건물 소유자는 가동 중지 시간 비용을 최소화하고 간과되는 경향이 있지만 반복 구매의 중요한 촉진요인이 되었습니다. 솔벤트 시스템과 하이브리드 에폭시 화학제품은 여전히 남은 비율을 차지하고 있으며, 저온에서 신속한 경화가 필수적인 환경, 특히 해양 시설과 한랭지에서 선호되고 있습니다. 그럼에도 불구하고 공급업체는 솔벤트 블렌딩을 조정하고 VOC 수준을 미래의 규제 기준치 이하로 억제함으로써 급격한 폐지가 아니라 단계적 전환을 시사합니다.

규제 상한이 엄격화되는 가운데, 사양 책정자는 내화 성능뿐만 아니라, 제조 과정에 있어서의 탄소 배출량(엠보디드 카본)도 기술 평가의 기준으로 하고 있습니다. 수성 도막은 양면에서 높은 평가를 얻고 있으며, 프로젝트 엔지니어가 기존의 용매계 도료로부터의 전환을 촉진하고 있습니다. 팽창성 코팅 시장 규모는 제조에서 시공까지의 낮은 배출을 평가하는 라이프사이클 평가의 영향을 향후 점점 받을 전망입니다. 하이브리드 에폭시는 기계적 강도와 환경성능의 향상을 양립시킴으로써 지위를 유지하고 있으며, 성능과 지속가능성의 목표가 점차 수렴하고 있음을 나타내고 있습니다.

팽창성 코팅 보고서는 용도별(셀룰로오스계, 탄화수소계), 기술별(용제계, 수성계, 에폭시계), 수지 유형별(에폭시, 아크릴, 폴리우레탄 등), 최종 사용자 산업별(건설, 자동차 등), 지역별(아시아태평양, 북미, 유럽 등)으로 업계를 세분화하고 있습니다. 시장 예측은 금액(달러)으로 제공됩니다.

아시아태평양은 2025년에 4억 7,060만 달러(세계 수익의 34.60%)를 창출해 2031년까지 연평균 복합 성장률(CAGR) 5.57%로 상승할 것으로 예측되고 있습니다. 중국은 고층 빌딩의 안전성과 석유화학의 자급자족이라는 이중 목표를 추진하고 있으며, 셀룰로오스계와 탄화수소계의 두 카테고리에서 안정적인 수요를 지지하고 있습니다. 인도의 스마트시티계획에서는 수동적 방화대책이 지자체 입찰 체크리스트에 내장되어 있어 주정부 자금에 의한 타워 건설에 있어서 팽창성 코팅공급이 사실상 필수 조건이 되고 있습니다. 현지에 공장을 입지하는 제조업체는 외환 리스크를 경감할 수 있는 것 외에 국내 제조를 우대하는 세제 우대 조치의 혜택을 받을 수 있습니다.

북미는 팽창성 코팅 시장의 핵심 지주로 계속되고 있습니다. 셰일가스 개발이 새로운 LNG 및 파이프라인 자산을 견인하는 한편, 노후화한 교량 스톡은 FHWA 가이드라인에서 언급되는 팽창성 코팅에 의한 개수를 촉진하고 있습니다. 달러화 공급망은 통화 위험을 줄이고 광범위한 현지 서비스 네트워크가 신속한 점검 및 보수 작업을 가능하게 하여 원재료 가격의 변동을 상쇄하고 있습니다. 공장내 스프레이 시공에 의한 공기 단축에 의해 모듈식 건축이 새로운 수요층을 더하고 있습니다.

유럽에서는 페인트 지침에 근거한 강력한 규제 견인력이 나타나 있으며, 수성 페인트의 혁신을 장려하고 있습니다. 독일 및 스칸디나비아의 녹색 빌딩 인증은 조달을 제품 함유 탄소 스코어링과 연동시킴으로써 수요를 확대하고 있습니다. 유럽 그린딜을 기반으로 한 자금 지원은 리그닌 기반 첨가제의 파일럿 라인을 지원하고 공급업체가 지역 연구소 내에서 바이오 제조 경로를 테스트하는 것을 촉진합니다. 그 결과 유럽은 종종 저탄소 등급의 선행 채택지역이 되고 나중에 전 세계적으로 널리 보급되는 이들 제품은 팽창성 코팅 시장의 경쟁 방향을 더욱 형성합니다.

The Intumescent Coatings Market size in 2026 is estimated at USD 1.41 billion, growing from 2025 value of USD 1.36 billion with 2031 projections showing USD 1.71 billion, growing at 3.89% CAGR over 2026-2031.

Adoption is anchored in stricter global fire-safety standards, a decisive shift toward greener building materials and the desire to keep structural steel visible without compromising protection. Demand increases are incremental rather than explosive, a pattern that hints at resilience built on code compliance cycles instead of speculative construction booms. Water-based chemistries already generate 40% of revenue, and regulatory limits on volatile organic compounds suggest this share will keep rising as specifiers prefer low-odor solutions. The growing preference for proactive fire-risk mitigation in high-density cities, offshore energy hubs and modular factories points to broad use cases that value thin films which expand into an insulating char when exposed to heat. Parallel innovation around durability, faster cure and lower applied thickness is extending product life, so revenue growth increasingly reflects a higher lifetime value per square foot rather than pure volume gains in the Intumescent coatings market.

New requirements for towers above 24 m make thin-film coatings nearly mandatory, giving developers products that deliver two-hour protection without adding structural weight. Certification regimes in China and India reward third-party testing, raising entry hurdles and giving early movers an edge. The Intumescent coatings market therefore enjoys a structural boost as skyline density grows and evacuation windows tighten. Suppliers that align product labels with local codes enter bid lists more easily, and approvals granted now often span multiple project phases, improving revenue visibility.

Hydrocarbon-specialized products held 44.2% share in 2024 because offshore topsides, LNG plants and refineries must manage pool-fire temperatures above 1,100 °C. Shale-linked construction across North America keeps fabrication yards busy, sustaining a steady order flow of epoxy intumescent films. Contractors that bundle supply with installation achieve greater margin retention as operators value single-contract accountability. Once a coating wins protocol testing like UL 1709 it tends to remain on specification lists for years, supporting recurring income streams in the Intumescent coatings market.

Fluctuations in raw material costs squeeze margins, especially for Asian producers that buy spot cargoes. Multi-year supply contracts provide partial insulation yet cannot eliminate exposure when feedstock prices spike quickly. Budget overruns may delay project starts or trigger product substitution where standards allow, temporarily slowing growth in the Intumescent coatings market.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Cellulosic coatings accounted for 52.60% of 2025 revenue equal to USD 715.4 million and continue to dominate because large volumes of commercial and residential steel require protection against slow-burn fires. Their relatively lower price broadens accessibility for mid-rise projects, so regulatory enforcement is not the sole driver. Architects see a clear cost-to-benefit ratio that supports repeat use, implying resilient baseline demand even if hydrocarbon volumes escalate faster. In contrast, hydrocarbon-rated lines generated USD 644.6 million yet are forecast to outpace the headline market with a 4.92% CAGR to 2031. These products must survive jet-fire and pool-fire testing, and once an EPC firm qualifies a brand it rarely changes mid-project. That stickiness locks in extended maintenance work, creating predictable after-sales income. The hydrocarbon subset therefore raises revenue per contract even if tonnage remains lower, reinforcing value concentration within the Intumescent coatings market.

The stronger growth rate in hydrocarbon films ties directly to new FPSO units, LNG export trains and refining upgrades in the Gulf Coast and Middle East. Offshore assets demand coatings that adhere under thermal shock, so epoxy systems remain the default platform. The Intumescent coatings market size for hydrocarbon applications is projected to climb as national energy strategies focus on downstream self-sufficiency. Cellulosic lines, meanwhile, keep pace with densifying cities where exposed steel delivers modern aesthetics. Together, the two fire scenarios carve distinct paths, but each strengthens overall penetration because they address separate safety imperatives rather than competing for the same square footage.

Water-borne solutions held 40.80% of 2025 revenue and are advancing at a 5.22% CAGR, leading the push toward low-VOC construction practices. Their absence of strong odor permits coating while tenants remain in place, a practical gain that simplifies refurbishment logistics. Building owners thus minimize downtime costs, an overlooked yet significant driver of repeat purchasing. Solvent-based and hybrid epoxy chemistries still account for the balance, favored where rapid cure at low temperature is mandatory, particularly offshore or in cold climates. Even so, suppliers tweak solvent blends to push VOC levels below future regulatory thresholds, signaling an evolutionary rather than abrupt phase-out.

As regulatory ceilings tighten, specifiers benchmark technologies not only on fire endurance but also on embodied carbon. Water-based films score well on both counts, encouraging project engineers to switch from older solvent types. The Intumescent coatings market size is expected to be increasingly influenced by lifecycle assessments that reward low emissions from manufacturing through application. Hybrid epoxies retain altitude by offering mechanical robustness plus improved environmental scores, illustrating a gradual convergence of performance and sustainability objectives.

The Intumescent Coatings Report Segments the Industry by Application (Cellulosic, Hydrocarbon), Technology (Solvent Based, Water Based, Epoxy Based), Resin Type (Epoxy, Acrylic, Polyurethane and More), End-User Industry (Construction, Automotive and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific generated USD 470.6 million or 34.60% of global revenue in 2025 and is forecast to climb at 5.57% CAGR through 2031. China enforces dual goals of high-rise safety and petrochemical self-reliance, underpinning steady volume in both cellulosic and hydrocarbon categories. India's Smart Cities program embeds passive fire protection into municipal tender checklists, effectively making intumescent supply a prerequisite for state-funded towers. Producers that localize factories in the region mitigate exchange-rate risk and capture tax incentives that favor domestic manufacturing.

North America remains a core pillar of the Intumescent coatings market. The shale play drives fresh LNG and pipeline assets while an aging bridge stock invites intumescent retrofits referenced in FHWA guidelines. Supply chains hedged in USD reduce currency exposure, and broad field-service networks enable rapid inspection and remedial work that offset raw-material swings. Modular construction adds a new demand layer, since factory spraying compresses build schedules.

Europe demonstrates strong regulatory pull derived from the Paints Directive, which rewards water-borne innovations. German and Scandinavian green-building labels amplify demand by linking procurement to embodied carbon scoring. Funding under the European Green Deal subsidizes pilot lines for lignin-based additives, encouraging suppliers to test bio-based routes inside regional labs. As a result, Europe often becomes the first adopter of low-carbon grades that later scale globally, further shaping the competitive direction of the Intumescent coatings market.