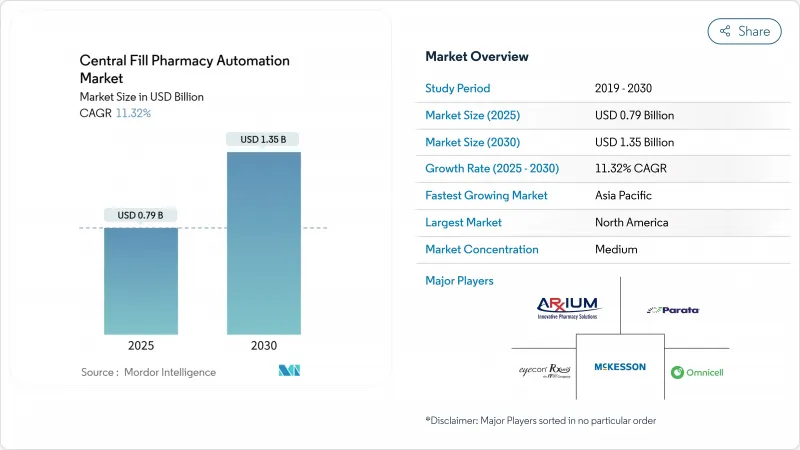

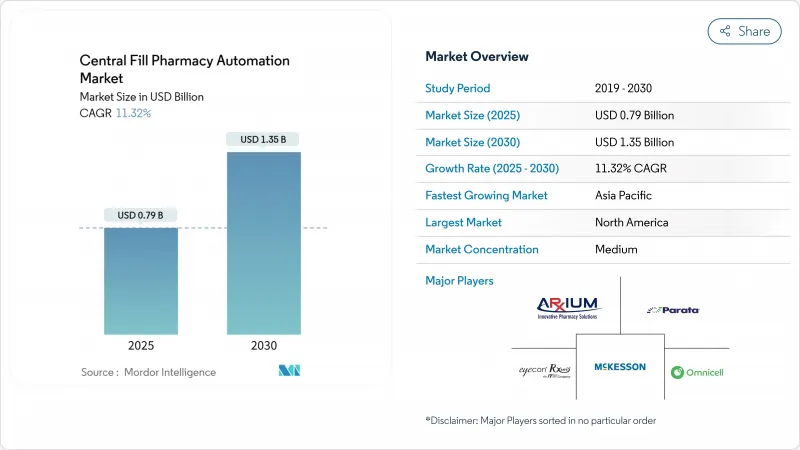

중앙 조제 약국 자동화 시장 규모는 2025년에 7억 9,000만 달러, 2030년에는 13억 5,000만 달러에 이를 것으로 예상되며, CAGR은 11.32%를 나타낼 전망입니다.

이 성장 궤도는 인건비 상승, 약사 부족 심각화, 이미 매월 1,600만 건이 넘는 처방전 통신 판매량의 가속을 반영합니다. 투자 추세는 의약품 공급망 보안법(Drug Supply Chain Security Act)에 따른 추적 및 추적 규칙의 엄격화, 투약 정확성에 대한 수요 증가, 마이크로플루필먼트 허브를 전개한 월그린의 연간 5억 달러의 풀필 삭감과 같은 소매업체의 비용 절감 성공으로 더욱 강해지고 있습니다. 의약품 부족을 발견하는 인공지능 툴, 24시간 365일 가동하는 IoT 연동 로봇, 서비스 기반의 자금 조달 모델은 병원, 소매, 통판 사업자의 대응 가능 베이스를 계속 확대하고 있습니다. 이러한 힘을 종합하면 중앙 조제 약국 자동화 시장은 세계의 약국 공급망 근대화에서 미션 크리티컬 기둥으로 자리매김하고 있습니다.

하루 20,000건 이상의 처방전을 처리하는 시설에는 산업 수준의 처리 능력을 유지하는 고급 로봇 셀이 필요합니다. 월그린의 최신 마이크로플루필먼트 허브는 약 200개 지역 점포에서 연간 약 1,300만 장의 처방전을 처리하고 있으며, 현재 달성 가능한 규모의 우위성을 강조하고 있습니다. 처방전 1장당 비용을 13% 삭감하고, 재고 회전율을 향출시키고, 조제 미스를 억제하는 자동화상 검증 체크포인트를 포함하고 있기 때문입니다. 우편 주문의 취급량은 2020년 이후 126% 증가하고 있으며, 처방전은 더욱 적지만 대규모 거점에 집중하고, 사람에 의한 감시는 적고, 24시간 365일 가동하고 있습니다. 이 추세는 소비자의 유통과 마찬가지로 처방전의 완성도를 컨베이어 순서화, 로봇 유도, 팔레타이제이션이 필요한 제조 워크플로우로 빠르게 재정의하고 있습니다.

약사의 졸업자 수가 10% 감소하는 반면, 지원자 수는 지난 10년간 60% 감소했으며 임금 압력이 높아지고 있습니다. 캘리포니아 주 의회 법안 1286은 강제적인 인력 배치 비율을 추가하고 체인에 급여를 증가시키지 않고 능력을 강화하도록 촉구합니다. 자동화된 셀은 엔지니어의 준비 시간을 59% 줄이고 약사의 검사 시간을 80% 줄일 수 있어 높은 비용의 도시 시장에서 신속한 투자 회수를 창출합니다. 또한 24시간 가동 로봇은 시간외 노동의 할증을 없애고 스케줄링의 갭을 완화함으로써 약사가 예방접종 등의 임상 서비스로 이동할 수 있습니다.

로봇화된 약국은 투약 규제, 소프트웨어 통합 및 기계적 문제 해결의 상호작용에 익숙한 기술자를 필요로 합니다. 그러나 특히 직업훈련 프로그램이 지연된 신흥 시장에서는 기술인력이 여전히 부족합니다. 6개월에서 12개월의 전문 코스가 필요하며, 약학부의 정원 균열이 인재 유로를 더욱 좁히고 있습니다. 시장 리더은 현재 현장에서의 훈련과 원격 감시를 번들로 하여 갭을 보완하고 있지만, 인력 부족은 여전히 도입 스케줄을 장기화시키고 지원 비용을 끌어올리고 있습니다. 일부 지역에서는 서비스 생태계가 성숙 할 때까지 업그레이드를 완전히 연기 할 수 있습니다.

2024년 중앙 조제 약국 자동화 시장에서는 장비가 63.67%의 점유율을 차지했으며, 고속 로봇 분주, 자동 파우치 포장기, 비전 기반 검증 라인이 그 중심이 되었습니다. ScriptPro의 SP 시리즈와 같은 자동화 장비는 변화 당 수천 개의 스크립트를 준비하면서 99.6%의 가동 시간을 보고합니다. 그러나 서비스의 중앙 조제 약국 자동화 시장 규모는 소유자가 예지 보전, 최적화 분석 및 컴플라이언스 지원을 요구하기 때문에 CAGR 13.56%로 빠르게 확대되고 있습니다. Omnicell의 XT Amplify로 대표되는 성과 연동 프로그램은 임상 벤치마크와 장비 업그레이드를 통합하여 오류 감소 및 처리량을 극대화합니다. 로봇에 의한 픽패스의 미세 조정, 새로운 직렬화 의무의 습득, 감사원의 만족도를 높이기 위해서, 시설은 분야 횡단적인 전문지식이 필요하기 때문에 컨설팅이나 노동력 트레이닝의 계약은 증가하고 있습니다.

그린필드의 허브는 컨베이어, 자동 창고, 라벨링 터널, 디스패치 분류기가 필요하기 때문에 장비의 중앙 조제 약국 자동화 시장 점유율의 우위는 손상되지 않습니다. 그럼에도 불구하고 벤더는 지속적인 서비스 수익의 매력으로 인해 하드웨어 새로 고침주기, 클라우드 소프트웨어 및 24시간 365일 원격 모니터링을 포함한 구독 번들을 만들 것을 촉구합니다. 결과적으로 Central Fill Pharmaceutical Automation Industries는 개별 자본 판매에서 수년간의 수익 가시성을 보장하는 솔루션 라이프 사이클 파트너십으로 전환하고 있습니다.

북미는 2024년 중앙 조제 약국 자동화 시장의 46.87%를 차지하며, 장기간에 걸쳐 DSCSA의 직렬화 기한과 대규모 거점에 유리한 체인 약국의 통합에 지원되었습니다. Omnicell, BD, ScriptPro는 광범위한 서비스 플릿과 데이터 중심의 계약을 유지하여 신속한 배포와 사이트 간 벤치마킹을 가능하게 합니다. 35개 주에서 전자처방 및 캘리포니아 주 인력 비율 규칙을 포함한 주 의무화는 광범위한 자동화 사례를 더욱 강화합니다. CoverMyMeds의 서비스 기반 모델과 같은 독창적인 자금 조달은 중규모 그룹의 채택을 계속 확대하고 있습니다.

아시아태평양은 CAGR 12.56%로 예측되는 급성장 지역입니다. 의약품 제조의 디지털화를 추진하는 중국의 정책은 시노팜의 자동 창고와 같은 대규모 도입을 뒷받침하고 있습니다. 일본에서는 고령화와 의약품 안전성의 의무화로 병원이 파우치 검사와 추적성에 대한 투자를 진행하고 있습니다. 인도, 한국, 싱가포르에서는 스마트 제조 기술에 대한 정부 보조금이 로봇 조제, 재고 분석, 콜드체인 포장의 도입 기반을 확대합니다.

유럽은 의약품 검사 협력 체계와 각국 특유의 e-건강 개혁에 힘입어 계속 안정적인 성장에 기여하고 있습니다. 이탈리아에 있는 Dr.Max의 1만 4,000m2 오토메이션 센터는 SSI SCHAEFER 셔틀 타워와 Geekplus AMR을 사용하여 전국에 스크립트를 제공하고 멀티벤더의 대규모 오케스트레이션을 선보입니다. 덴마크의 2024년 약국법 개정을 통해 병원 약국이 외래 환자에게 직접 조제할 수 있게 되어 주소 지정이 가능한 허브 네트워크가 확산됩니다. 지속가능성의 목표는 유럽 사업자가 에너지 효율적인 셔틀 시스템을 도입하고 로봇 조제와 함께 재활용 가능한 패키징 스트림을 통합하는 동기부여입니다.

The central fill pharmacy automation market size is valued at USD 0.79 billion in 2025 and is forecast to reach USD 1.35 billion in 2030, reflecting an 11.32% CAGR.

The growth trajectory mirrors rising labor costs, widening pharmacist shortages, and accelerating mail-order volumes that already exceed 16 million prescriptions each month. Investment momentum is further reinforced by stricter track-and-trace rules under the Drug Supply Chain Security Act, heightened demand for medication accuracy, and retailer cost-saving successes such as Walgreens' USD 500 million in annual fulfillment savings after rolling out micro-fulfillment hubs. Artificial-intelligence tools that spot drug shortages, IoT-linked robotics that run 24/7, and service-based financing models continue to expand the addressable base of hospital, retail, and mail-order operators. Collectively, these forces position the central fill pharmacy automation market as a mission-critical pillar in pharmacy supply-chain modernization worldwide.

Facilities processing above 20,000 prescriptions per day now require advanced robotic cells that sustain industrial-level throughput. Walgreens' newest micro-fulfillment hub handles about 13 million prescriptions annually for roughly 200 regional stores, underscoring the scale advantage now achievable. High-volume locations are posting a 13.65% CAGR because they lower per-script costs by 13%, improve inventory turns, and embed automated image-verification checkpoints that curb dispensing errors. Mail-order volumes have grown 126% since 2020, further concentrating scripts into fewer but larger hubs that operate 24/7 with less human oversight. The trend is rapidly redefining prescription fulfillment as a manufacturing workflow requiring conveyor sequencing, robotic induction, and palletization similar to consumer-goods distribution.

Graduating pharmacist numbers have fallen 10% while applicant pools have shrunk 60% over the past decade, widening wage pressures that automation helps contain. California's Assembly Bill 1286 adds mandatory staffing ratios, spurring chains to augment capacity without inflating payroll. Automated cells can cut technician prep time 59% and reduce pharmacist check time 80%, creating a swift payback in high-cost urban markets. Around-the-clock robotics also eliminate overtime premiums and mitigate scheduling gaps, allowing pharmacists to shift toward clinical services such as vaccinations, which climbed 40% once tasks moved to a hub model.

Robotics-enabled pharmacies require technicians versed in interplay between medication regulations, software integration, and mechanical troubleshooting. Yet technical talent remains scarce, particularly in emerging markets where vocational programs lag. Six-to-twelve-month specialized courses are needed, and declining pharmacy-school cohorts further shrink the talent funnel. Market leaders now bundle on-site training and remote monitoring to offset gaps, but scarcity still lengthens implementation timelines and raises support costs. In some regions, operators defer upgrades altogether until service ecosystems mature.

Other drivers and restraints analyzed in the detailed report include:

For complete list of drivers and restraints, kindly check the Table Of Contents.

Equipment held 63.67% share of the central fill pharmacy automation market in 2024, anchored by high-speed robotic dispensing, automated pouch packagers, and vision-based verification lines. Automated units such as ScriptPro's SP Series report 99.6% uptime while preparing thousands of scripts per shift. The central fill pharmacy automation market size for services, however, is expanding faster at a 13.56% CAGR as owners seek predictive maintenance, optimization analytics, and compliance support. Outcome-linked programs, typified by Omnicell's XT Amplify, integrate clinical benchmarking with equipment upgrades to maximize error reduction and throughput. Consulting and workforce-training engagements are growing because facilities need cross-disciplinary expertise to fine-tune robotic pick paths, master new serialization mandates, and satisfy auditors.

The central fill pharmacy automation market share advantage for equipment remains intact because each greenfield hub needs conveyors, automated storage, labeling tunnels, and dispatch sorters. Even so, the recurring-revenue appeal of services is prompting vendors to create subscription bundles that include hardware refresh cycles, cloud software, and 24/7 remote monitoring. As a result, the central fill pharmacy automation industry is shifting from discrete capital sales toward solution lifecycle partnerships that lock in multiyear revenue visibility.

The Central Fill Pharmacy Automation Market Report is Segmented by Products & Services (Equipment and Services), End-User Type (Hospital-Owned Central Fill Pharmacies, Retail Chain Central Fill Facilities, and More), Throughput Capacity, Medium, and High), Geography (North America, Europe, Asia-Pacific, The Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

North America captured 46.87% of the central fill pharmacy automation market in 2024, anchored by long-standing DSCSA serialization deadlines and chain-pharmacy consolidation that favors large hubs. Omnicell, BD, and ScriptPro maintain extensive service fleets and data-driven contracts, enabling rapid rollouts and cross-site benchmarking. State mandates-including e-prescribing laws in 35 states and California's staffing ratio rule-further strengthen the case for broad automation. Financing creativity, such as CoverMyMeds' service-based model, continues to broaden adoption among midsize groups.

Asia-Pacific is the fastest-growing territory, projected at 12.56% CAGR. China's policy push for pharmaceutical manufacturing digitalization underpins large-scale deployments such as Sinopharm's automated warehouse, the country's first of its kind. Japan's aging demographics and drug-safety mandates drive hospitals to invest in pouch inspection and traceability. Government subsidies for smart-manufacturing technology in India, South Korea, and Singapore expand the install base for robotic dispensing, inventory analytics, and cold-chain packaging.

Europe remains a steady growth contributor, underpinned by the Pharmaceutical Inspection Co-operation Scheme and country-specific e-health reforms. Dr. Max's 14,000 m2 automation center in Italy delivers nationwide scripts with SSI SCHAEFER shuttle towers and Geekplus AMRs, showcasing multi-vendor orchestration at scale. Denmark's 2024 Pharmacy Act amendment allows hospital pharmacies to dispense directly to outpatients, widening the addressable hub network. Sustainability targets motivate European operators to install energy-efficient shuttle systems and integrate recyclable packaging streams alongside robotic dispensing.